PRELIMINARY OFFERING CIRCULAR – MARCH 4, 2026

SUBJECT TO COMPLETION

AN OFFERING STATEMENT PURSUANT TO REGULATION A RELATING TO THESE SECURITIES HAS BEEN FILED WITH THE SECURITIES AND EXCHANGE COMMISSION. INFORMATION CONTAINED IN THIS PRELIMINARY OFFERING CIRCULAR IS SUBJECT TO COMPLETION OR AMENDMENT. THESE SECURITIES MAY NOT BE SOLD NOR MAY OFFERS TO BUY BE ACCEPTED BEFORE THE OFFERING STATEMENT FILED WITH THE COMMISSION IS QUALIFIED. THIS PRELIMINARY OFFERING CIRCULAR SHALL NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY NOR MAY THERE BE ANY SALES OF THESE SECURITIES IN ANY STATE IN WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE UNLAWFUL BEFORE REGISTRATION OR QUALIFICATION UNDER THE LAWS OF ANY SUCH STATE. WE MAY ELECT TO SATISFY OUR OBLIGATION TO DELIVER A FINAL OFFERING CIRCULAR BY SENDING YOU A NOTICE WITHIN TWO BUSINESS DAYS AFTER THE COMPLETION OF OUR SALE TO YOU THAT CONTAINS THE URL WHERE THE OFFERING CIRCULAR WAS FILED MAY BE OBTAINED.

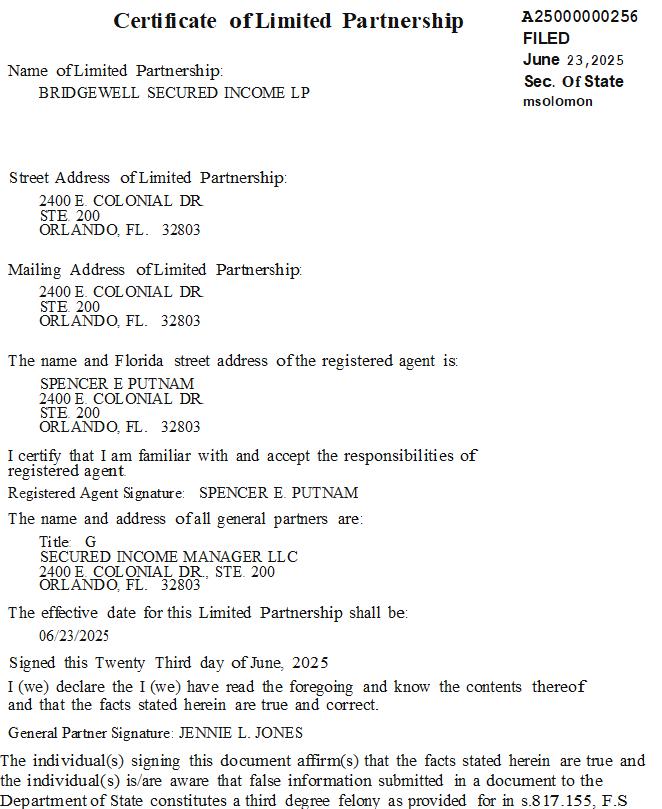

BRIDGEWELL SECURED INCOME LP

2400 E. Colonial Dr., Ste 200

Orlando, FL 32803

Phone No.: (877) 700-4800

manager@bridgewellfunds.com

https://www.earn7now.com/

$75,000,000.00 Maximum Offering Amount

BridgeWell Secured Income LP, a Florida limited liability partnership (which we refer to as “we,” “us,” “our” or “Partnership”), is offering up to 75,000 units of partnership interest (the “Interests(s),” or “Securities”) in the Partnership at $1,000.00 per Interest, for a maximum of $75,000,000.00 (“Maximum Offering Amount”), if all offered Interests are sold (the “Offering”). There are no minimum offering amount and no provision to escrow or return investor funds if any minimum number of Interests is not sold. All funds raised by the Partnership from this Offering will be immediately available for the Partnership’s use. The minimum investment amount established for each investor is $10,000.00, which may be waived by the Partnership on a case-by-case basis for any reason or no reason at all.

Concurrently with this offering, the Partnership is offering Interests through an offering exempt from registration under Regulation D, Rule 506(c), and had 5,646.20 Interests issued and outstanding as of January 31, 2026.

The sale of Interests will commence once this offering circular, as amended, is qualified by the Securities and Exchange Commission (“SEC”). We will conduct separate closings within seven (7) days of receiving investor funds and completed subscription documents. This offering will terminate at the earlier to occur of: (i) all Interests offered hereby are sold, (ii) three years from the date this offering circular, as amended, is qualified with the SEC, or (iii) such earlier date as determined by the Partnership.

| Price to public(1) | Underwriting discount and commissions(2) | Proceeds to Issuer(3) | ||||||||||||

| Per Interest | $ | 1,000.00 | $ | 0.00 | $ | 105.05 | ||||||||

| Total Maximum(4) | $ | 75,000,000.00 | $ | 0.00 | $ | 23,815,923.60 | ||||||||

| (1) | All amounts in this chart and circular are in U.S. dollars unless otherwise indicated. All investor funds will be held in a segregated Partnership account until the investor’s subscription is accepted by the Partnership, at which time such funds will become available for the Partnership’s use. |

| (2) | We have not engaged a broker dealer or selling agent and all proceeds from the Offering will be payable to the Partnership. See “Plan of Distribution” on page 33 for further details. |

| (3) | The Partnership will incur expenses relating to this Offering, including, but not limited to, legal, accounting, marketing, escrow, technology, and travel expenses, which expenses are not reflected in the above table. Such expenses may be advanced by Secured Income Manager LLC, a Florida limited liability company (“General Partner”), our General Partner, with or without reimbursement. |

1

| (4) | This Offering is being made on a best-efforts basis. There is no minimum offering amount and no provision to escrow or return investor funds if any minimum number of Interests are not sold. All investor funds will be immediately available for use upon acceptance. |

Our Interests are not now listed on any national securities exchange, quotation system or the Nasdaq stock market and there is no market for our securities. There is no guarantee, and it is unlikely, that an active trading market will develop in our securities. Investors should be prepared to hold our Interests indefinitely.

This Offering is highly speculative, and these securities involve a high degree of risk and should be considered only by persons who can afford the loss of their entire investment. See “Risk Factors” on page 5 for a description of some of the risks that should be considered before investing in our Interests. These risks include, but are not limited to, the following:

Summary of Key Risk Factors

| Risk Category | Risk Factor | Description |

| Investment Structure | Blind Pool Risk | Investors will not be able to review or approve specific investments before funds are deployed and must rely entirely on management’s judgment, making the investment more speculative. |

| Investment Structure | Limited Liquidity | Interests are not publicly traded and may be difficult or impossible to sell, and investors should be prepared to hold their investment for an extended period or lose some or all of their capital. |

| Portfolio Construction | Concentration Risk | Investments may be concentrated in certain regions, property types, or individual loans, increasing exposure to localized economic downturns or borrower defaults. |

| Portfolio Construction | Limited Diversification | Investing in fewer, larger loans may increase the impact of a single loan default on overall performance. |

| Loan Structure | Subordinated and Junior Loans | Some investments may be junior to other debt and may receive little or no recovery if a borrower defaults or a senior lender forecloses. |

| Loan Structure | Intercreditor Restrictions | Agreements with senior lenders may limit the Partnership’s ability to enforce remedies or protect its position following a default. |

| Valuation | “As-Completed” Valuation Risk | Loan values are sometimes based on expected future property values, which may not be realized, reducing recoveries in the event of default. |

| Loan Terms | Balloon Payment Risk | Certain loans require large payments at maturity that depend on refinancing or property sales, which may not occur. |

| Credit Exposure | Non-Recourse Loans | In many cases, recovery is limited to the property securing the loan, which may be worth less than the amount owed. |

| Development | Construction & Renovation Risk | Loans funding construction or renovation are riskier due to cost overruns, delays, contractor issues, and market changes. |

| Development | Project Non-Completion | If a project is not completed or becomes uneconomic, the value of the collateral may decline significantly. |

| Legal | Mechanics’ Lien Risk | Contractors or suppliers may assert liens that impair the Partnership’s security interest. |

| Enforcement | Foreclosure Delay & Expense | Foreclosure and bankruptcy proceedings may take years, involve significant costs, and reduce investor returns. |

| Enforcement | Bankruptcy Risk | Bankruptcy courts may reduce loan balances, change repayment terms, or limit enforcement rights. |

2

| Government Action | Tax Sale & Eminent Domain | Government actions, including tax sales or eminent domain proceedings, could reduce or eliminate recoveries. |

| REO Ownership | Real Estate Ownership Risk | If the Partnership takes ownership of property, it may incur operating losses, environmental liabilities, or legal claims. |

| Liquidity | Difficulty Selling Properties | Real estate assets may be difficult to sell or may sell for less than anticipated, particularly during market downturns. |

| Borrower Risk | Borrower Financial Deterioration | A borrower’s financial condition may worsen after loan origination, increasing the risk of default. |

| Borrower Risk | Permanent Financing Risk | Borrowers may be unable to obtain refinancing needed to repay loans at maturity. |

| Market Risk | Interest Rate Risk | Rising interest rates may increase borrower defaults and reduce property values. |

| Market Risk | Real Estate Market Volatility | Property values and rental income may decline due to economic conditions beyond management’s control. |

| Management | Reliance on Management | The success of the investment depends heavily on the General Partner and its affiliates, which have limited operating history. |

| Governance | Limited Investor Rights | Investors have limited voting rights and minimal ability to influence management decisions or strategy changes. |

| Operations | Multiple Offerings Risk | Conducting multiple offerings may increase compliance costs, litigation risk, and management distraction. |

| Financial Reporting | Reduced Reporting Obligations | As a Tier 2 Reg A issuer, reporting requirements are less frequent and detailed than those of fully public companies. |

| Leverage | Use of Borrowings | Borrowing against assets increases the risk of loss and may reduce cash available for distributions. |

| Liquidity | Cash Flow Constraints | Distributions depend on available cash flow and may be reduced or suspended. |

| Structure | No Guaranteed Distributions | There is no guarantee that investors will receive distributions or recover their invested capital. |

| Regulatory | Regulatory Compliance Risk | Failure to comply with complex lending and servicing regulations could result in fines, losses, or unenforceable loans. |

| Legal | Litigation Risk | The Partnership may face lawsuits that could result in significant legal costs or liabilities. |

| Investor Rights | Class Action Waiver | Investors agree to bring claims individually, which may limit recovery and increase legal costs. |

| Insurance | Uninsured Losses | Certain events may not be covered by insurance, resulting in losses to the Partnership. |

| Insurance | Insurance Lapse Risk | Properties securing loans may become uninsured following borrower default. |

| Environmental | Environmental Hazards | Properties may contain environmental issues or mold that result in cleanup costs or liability. |

| Tax | Taxable Income Without Cash | Investors may owe taxes on allocated income even if no distributions are received. |

| Tax | Limited Use of Losses | Tax losses may be limited under passive activity rules and may not offset other income. |

| Early Stage | Limited Operating History | The Partnership is newly formed and has limited operating and investment history. |

| Capital | Capital Raising Risk | Failure to raise sufficient capital could limit investment opportunities and operating scale. |

| Capital Use | Use of Proceeds Risk | Management has discretion over use of proceeds, which may not generate expected returns. |

THE U.S. SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OF OR GIVE ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SOLICITATION MATERIALS. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION.

This Offering is being made pursuant to Tier 2 of Regulation A following the Form 1-A offering circular disclosure format.

3

TABLE OF CONTENTS

4

This summary highlights some of the information in this circular. It is not complete and may not contain all of the information that you may want to consider. To understand this offering fully, you should carefully read the entire circular, including the section entitled “Risk Factors,” before making a decision to invest in our securities. Unless otherwise noted or unless the context otherwise requires, the terms “we,” “us,” “our,” and “Partnership” refer to BridgeWell Secured Income LP together with our wholly and majority owned subsidiaries.

The Partnership

BridgeWell Secured Income LP was organized as a limited liability partnership in Florida on June 23, 2025. The Partnership intends to acquire real estate secured loans (fixed and variable interest rate), primarily bridge loans and other loans secured by real estate (“Mortgage Loans”). The Partnership’s principal address is 2400 E. Colonial Dr., Ste 200, Orlando, FL 32803.

Business Overview

BridgeWell Secured Income, LP is an emerging growth company which was formed on June 23, 2025. We have been operating for approximately eight months as of the date of this offering circular. We intend on generating revenues primarily from interest received on mortgage notes acquired. However, under certain favourable market conditions, we may generate revenues from direct ownership of real estate which could generate revenues in two ways: cash flow from lease of the properties, or resale profits. We intend to acquire all the mortgage notes from BridgeWell Capital (“BW Capital”), which is an affiliate of our General Partner. However, we reserve the right to acquire mortgage notes from other companies. We may also purchase non-performing notes in certain favourable market environments which could generate revenues by facilitating performance on the notes or by foreclosing and then profiting from real estate owned as described above.

As of January 31, 2026, the Partnership had a loan portfolio balance of $5,462,974.09 spread across 23 total Mortgage Loans. All Mortgage Loans as of that date are performing and the Partnership has no real estate owned properties. The weighted average Mortgage Loan interest rate is 10.03%. Commercial loans comprise 59.1% and residential loans comprise 40.9% of the Partnership’s holdings. The Mortgage Loans are concentrated in the following states: MI 20%, FL 18%, NC 18%, GA 10%, TN 10%, MO 9%, SC 5%, Other 9% (states with less than 5% representation).

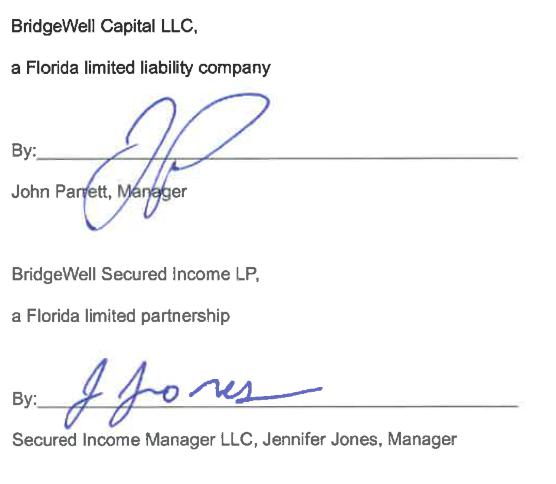

Management

The Partnership’s General Partner is Secured Income Manager LLC, a Florida limited liability company. Jennifer L. Jones is the manager of the General Partner. Our General Partner shall manage and administer partnership assets and perform all other duties prescribed for in our limited partnership agreement dated September 16, 2025 (the “Agreement”) and the Florida Revised Uniform Partnership Act. No other person shall have any right or authority to act for or bind the Partnership except as permitted in our Agreement or as required by law. Our General Partner shall have no personal liability for the obligations of the Partnership.

Capitalization

The Partnership is authorized to issue an unlimited number of Interests. As of January 31, 2026, the Partnership had 5,646.20 Interests issued and outstanding. Following the completion of this Offering, assuming all offered Interests are sold and no other Interests of the Partnership are issued, the Partnership will have 80,646.20 Interests issued and outstanding. However, the Partnership is offering Interests through an offering exempt from registration under Regulation D, Rule 506(c) concurrently with this offering and so investors in this offering will be subject to dilution from Interests sold in the Regulation D offering. The Partnership has no SAFEs, warrants, or convertible notes outstanding.

Distributions

Cash Flow generated by the Partnership will be distributed to the partners of the Partnership (the “Partners”) as described below. All Partners other than the General Partner are referred to as “Limited Partners” herein. “Cash Flow” means the cash proceeds realized by the Partnership plus cash interest payments received with respect to such proceeds, decreased by the sum of: (i) the amount of such proceeds applied by the Partnership to pay debts and liabilities of the Partnership; and (ii) any reserve established by the General Partner for the reinvestment of capital contributions into additional Mortgage Loans or anticipated cash disbursements that will have to be made before additional cash receipts from third parties will provide the funds thereof.

5

The General Partner has the sole discretion to reinvest capital contributions into additional Mortgage Loans when principal on a Mortgage Loan is repaid to the Partnership.

Operating Cash Flow

Except as provided elsewhere in the Agreement, operating cash flow of the Partnership shall be distributed to the Partners monthly, so long as the General Partner determines it is available for distribution, in the following order of priority.

(a) First, ratably to the Limited Partners the payment of any previously deferred and compounded Preferred Return (defined below) owed to any Partner pursuant to Section 7.03 of the Agreement as described below.

(b) Second, ratably to the Limited Partners a non-cumulative, non-compounded preferred return of seven percent (7%) per annum calculated on their capital contributions (the “Preferred Return”).

(c) Third, one hundred percent (100%) to the General Partner.

* For the avoidance of doubt, if investors do not receive payment of their full Preferred Return in a particular year, the unpaid portion will not carry forward to the next year.

Capital Transactions

Except as provided elsewhere in the Agreement, Cash Flow of the Partnership resulting from capital transactions shall be distributed to the Partners, so long as the General Partner determines it is available for distribution, in the following order of priority as well as Cash Flow from dissolution.

(a) First, ratably to the Limited Partners the payment of any previously deferred and compounded Preferred Return owed to any Partner pursuant to Section 7.03 of the Agreement.

(b) Second, ratably to the Limited Partners until they have received one hundred percent (100%) of any unreturned capital contributions.

(c) Third, one hundred percent (100%) to the General Partner.

Deferment of Cash Flow.

Upon admission to the Partnership or any time thereafter, subject to the approval of the General Partner in its sole discretion, a Limited Partner may request in writing to the Partnership for the deferment of payment of its Preferred Return to which it is entitled pursuant to Section 7.01(b) of the Agreement. Any payment of the Preferred Return deferred shall compound monthly until paid. For the avoidance of doubt, if Limited Partners do not receive their entire Preferred Return for a particular year, only the amount received by non-deferred Limited Partners will compound for those Limited Partners who have elected deferment. A Limited Partner may rescind their election of deferment at any time by providing the General Partner five (5) days’ written notice. The Partnership, in the sole discretion of the General Partner, may terminate any election of deferral of the Preferred Return at any time by providing the Limited Partners five (5) days’ written notice of such termination. Deferral of any Preferred Return shall not result in the purchase or issuance of additional Interests to a Partner.

Going Concern

The consolidated financial statements have been prepared on a going concern basis, which contemplates the realization of assets and satisfaction of liabilities in the normal course of business. As of the date of these financial statements, the Partnership has not generated sufficient revenues to sustain operations and requires additional capital to fund its operating activities and meet its obligations as they become due. The Partnership’s ability to continue as a going concern is dependent upon its ability to raise additional funds and to achieve profitable operations.

6

Management intends to raise additional capital through a Regulation D offering, and this offering; however, there can be no assurance that such financing will be available on acceptable terms, if at all. The failure to obtain sufficient additional financing and/or to achieve profitable operations raises substantial doubt about the Partnership’s ability to continue as a going concern. The consolidated financial statements do not include any adjustments that might result from the outcome of these uncertainties.

Use of Proceeds

In general, the Partnership will use net proceeds from this Offering for Offering expenses, the purchase of Mortgage Loans, working capital, and legal and accounting costs. See “Use of Proceeds” on page 36 for more details.

The Offering

This offering circular relates to the sale of up to 75,000 Interests at a price of $1,000.00 per Interest, for gross proceeds of up to $75,000,000. The minimum investment amount established for each investor is $10,000.00, which may be waived by the Partnership on a case-by-case basis for any reason or no reason at all. There are no minimum offering amount and no provision to escrow or return investor funds if any minimum number of Interests is not sold. All funds raised by the Partnership from this Offering will be immediately available for the Partnership’s use.

In order to subscribe to purchase Interests, a prospective investor deliver a completed a subscription agreement to the Partnership by email or mail to the Partnership’s principal address at 2400 E. Colonial Dr., Suite 200, Orlando, FL 32803, and send payment by personal check, cashier’s check, or bank wire. Interests are being offered on a best-efforts basis through the management and authorized employees of the Partnership, for which no independent compensation will be paid. Investors must answer certain questions to determine compliance with the investment limitation set forth in Regulation A Rule 251(d)(2)(i) under the Securities Act of 1933 (the “Securities Act”), which states that in offerings such as this one, where the securities will not be listed on a registered national securities exchange upon qualification, the aggregate purchase price to be paid by an investor who is a natural person for the securities cannot exceed ten percent (10%) of the greater of the investor’s annual income or net worth, unless the purchaser is an accredited investor. In the case of an investor who is not a natural person, revenues or net assets for the investors’ most recently completed fiscal year are used instead.

This Offering will terminate at the earlier to occur of: (i) the date all Interests offered hereby are sold, (ii) three years from the date this offering circular, as amended, is qualified with the SEC, or (iii) such earlier date as determined by the Partnership.

Voting Rights

Interests represent units of partnership interest of the Partnership (“Partnership Interest”). Partnership Interest means in respect to any Partner, all such Partner’s right, title and interest in and to the net profits, net losses and cash flow of the Partnership or the capital thereof or any interest therein. The percentage interest (“Percentage Interest”) of each Partner is the percentage that results from multiplying one hundred (100) by the quotient of the number of Interests held by such Partner divided by the total number of Interests held by all the Partners of the Partnership. Limited Partners have no right to participate in the management of the Partnership and have limited voting rights. Limited Partners may vote on the removal of the General Partner, a vacancy of the General Partner, dissolution of the Partnership, a proposed change to the distribution structure for Limited Partners, and an amendment to the Partnership Agreement.

Transfer Restrictions

Our Partnership Agreement contains significant restrictions on transfer of Interests. Except as permitted in Section 10.06 of the Agreement, no Partner may transfer, sell, convey, assign, pledge, hypothecate or encumber in any manner his, her or its respective Partnership Interest without the prior written approval of the General Partner, which approval may be withheld in the General Partner’s sole and absolute discretion. Furthermore, transfers of our Interests may only be made pursuant to exemptions under the Securities Act and as permitted by applicable state securities laws.

7

The following transfers by the Partners shall not require the prior consent of the Limited Partners:

(a) With the written consent of the General Partner, any Partner who is a person may transfer his or her Partnership Interest or any portion thereof to a trust established for the exclusive benefit of such Partner, his or her spouse and/or lineal descendants, provided such Partner acting alone may bind the trust;

(b) Any Partner who is a person may transfer his or her Partnership Interest to his or her spouse and/or lineal descendants by will upon the death of such Partner;

(c) Any Successor to a Limited Partner pursuant to Section 10.02(e); and

(d) With the written consent of the General Partner, any Partner may transfer such Partner’s Partnership Interest to any other Partner.

(e) Subject to transfer restrictions imposed on the Interests, transfers shall be permitted without a transfer fee for Partners holding Interests through a qualified plan (i.e. any pension, profit sharing or stock bonus plan that is qualified under Code Section 401(a)), tax exempt entities, including individual retirement accounts (i.e. IRA and Roth IRA).

There is no market for our Interests, and none is likely to develop in the future.

Withdrawal

No Limited Partner may withdraw within the first six (6) months of a Limited Partner’s admission to the Partnership. Thereafter, the Partnership will use its best efforts to fulfil requests for a return of capital and payment of any deferred Preferred Return pursuant to Section 7.03 of this Agreement subject to, among other things, the Partnership’s then available cash flow, financial condition, and approval by the General Partner. The maximum aggregate amount of capital that the Partnership will return to the Limited Partners each calendar quarter is limited to ten percent (10%) of the total outstanding capital of the Partnership as of December 31 of the prior year. Additionally, the General Partner has the discretion to limit aggregate withdrawals during any single calendar year to not more than 10% of the total outstanding capital of the Partnership as of December 31 of the prior year. Notwithstanding the foregoing, the General Partner may, in its sole discretion, waive such withdrawal requirements if a Limited Partner is experiencing undue hardship. Please review the section entitled “Securities Being Offered” on page 69 and the Partnership Agreement attached as Exhibit 2.2 for the full withdrawal provisions.

General Partner Election to Liquidate a Limited Partner

At any time for any reason, the General Partner may elect to liquidate a Limited Partner’s Partnership Interest. The General Partner shall provide notice of liquidation to the Limited Partner in writing. Upon 100% return of capital and payment of any deferred preferred returns to the Limited Partner, the Limited Partner shall no longer be a Limited Partner of the Partnership.

We have prepared this offering circular to be filed with the SEC for our offering of securities. The offering statement includes exhibits that provide more detailed descriptions of the matters discussed in this offering circular.

You should rely only on the information contained in this offering circular and the exhibits to the offering statement. We have not authorized any person to provide you with any information different from that contained in this offering circular. The information contained in this offering circular is complete and accurate only as of the date of this offering circular, regardless of the time of delivery of this offering circular or sale of our Interests. This offering circular contains summaries of certain other documents, but reference is hereby made to the full text of the actual documents for complete information concerning the rights and obligations of the parties thereto. All documents relating to this offering and related documents and agreements, if readily available to us, will be made available to a prospective investor or its representatives upon request.

The industry and market data used throughout this offering circular have been obtained from our own research, surveys or studies conducted by third parties and industry or general publications. Industry publications and surveys generally state that they have obtained information from sources believed to be reliable. We believe that each of these studies and publications is reliable. We have not engaged any person or entity to provide us with industry or market data.

8

No information contained herein, nor in any prior, contemporaneous or subsequent communication should be construed by a prospective investor as legal or tax advice. We are not providing any tax advice as to the acquisition, holding or disposition of the securities offered herein. In making an investment decision, investors are strongly encouraged to consult their own tax advisor to determine the U.S. Federal, state and any applicable foreign tax consequences relating to their investment in our securities. This written communication is not intended to be “written advice,” as defined in Circular 230 published by the U.S. Treasury Department.

The Interests offered hereby are highly speculative in nature, involve a high degree of risk and should be purchased only by persons who can afford to lose their entire investment. There can be no assurance that our investment objectives will be achieved or that a secondary market will ever develop for the Interests. The risks described in this section should not be considered an exhaustive list of the risks that prospective investors should consider before investing in the Interests. Prospective investors should obtain their own legal and tax advice prior to making an investment in the Interests and should be aware that an investment in the Interests may be exposed to other risks of an exceptional nature from time to time. The following considerations are among those that should be carefully evaluated before making an investment in the Interests.

Risks Related to the Offering and our Securities

The purchase of Interests may not be a diversified investment.

The Partnership intends to primarily invest in Mortgage Loans and in real property. There is no requirement for the Partnership to diversify the Mortgage Loans or properties it acquires. Therefore, an investment in the Partnership may not be a diversified investment. The poor performance of the Mortgage Loans or the properties could adversely affect the return to investors.

There is no guarantee of a return on an investor’s investment.

The Partnership’s business objectives must be considered highly speculative. There is no assurance that an investor will realize a return on their investment or that they will not lose their entire investment. For this reason, each investor should read this offering circular and all exhibits carefully and should consult with their attorney and business advisor prior to making any investment decision.

The Offering price of the Interests may not accurately represent the current value of the Partnership or our assets at any particular time. Therefore, the purchase price you pay for the Interests may not be supported by the value of our assets at the time of your purchase.

Our General Partner has determined the Interests offered by the Partnership. The price of the Interests we are offering was arbitrarily determined based upon the illiquidity and volatility of our Interests, our current financial condition and the prospects for our future cash flows and earnings, and market and economic conditions at the time of the Offering. This is a fixed price Offering, which means that the Offering price for the Interests is fixed and will not vary based on the underlying value of our assets at any time. Our General Partner determined the Offering price in its sole discretion without the input of an investment bank or other third party. The fixed Offering price for the Interests has not been based on appraisals of any assets we own or may own, or of the Partnership as a whole, nor do we intend to obtain such appraisals. Therefore, the fixed offering price established for the Interests may not be supported by the current value of the Partnership or our assets at any particular time.

There is no current market for the Interests of the Partnership.

You should be prepared to hold this investment indefinitely. There is no established market for these securities and there may never be one. As a result, if you decide to sell these securities in the future, you may not be able to find a buyer. Investors should assume that they may not be able to liquidate their investment or be able to pledge their Interests as collateral.

9

There are restrictions on an investor’s ability to sell its Interests making it difficult to transfer, sell or otherwise dispose of the Interests.

Each state has its own securities laws, often called “blue sky” laws, which limit sales of securities to a state’s residents unless the securities are registered in that state or qualify for an exemption from registration. Before a security is sold in a state, there must be a registration in place to cover the transaction, or it must be exempt from registration. Our Interests will not be registered under the laws of any states. There may be significant state blue sky law restrictions on the ability of investors to sell, and on purchasers to buy, our Interests. Investors should consider the resale market for our Interests to be limited. Investors may be unable to resell their Interests, or they may be unable to resell them without the significant expense of state registration or qualification. In addition, there are significant transfer restrictions contained in our Partnership Agreement that prohibit transfers unless approved by our General Partner, in its sole discretion, and the transferee and transferor have met other conditions established by our Partnership Agreement.

There is no minimum offering amount.

Interests are being offered on a “best- efforts” basis. There is no minimum offering amount and all Offering proceeds will be immediately available for the Partnership’s use. Offering proceeds may be used to pay for Offering expenses such as legal expenses and marketing, and other expenses. If the Partnership is unable to raise sufficient funds to operate, its results of operations and investor returns could be materially negatively impacted, or investors could lose some or all of their investment.

The best-efforts structure of this offering may yield insufficient gross proceeds to fully execute our business plan.

Interests are being offered on a best-efforts basis. We are not required to sell any specific number or dollar amount of Interests but will use our best efforts to sell the Interests offered by us. As a “best efforts” Offering, there can be no assurance that the offering contemplated by this offering circular will result in any proceeds being made available to us.

We may not register or qualify our securities with any state agency pursuant to blue sky regulations.

The holders of our Interests and persons who desire to purchase them in the future should be aware that there may be significant state law restrictions upon the ability of investors to resell our Interests. We currently do not intend to and may not be able to qualify securities for resale in states which require Interests to be qualified before they can be resold by our members.

We may experience investment delays.

There may be a delay between the time an investor’s subscription is accepted by the Partnership and the time the proceeds of this Offering are deployed. During these periods, the Partnership may invest these proceeds in short-term certificates of deposit, money-market funds, or other liquid assets with FDIC-insured and/or NCUA-insured banking institutions, which will not yield a return as high as if deployed towards other assets such as the Mortgage Loans.

Interests are being offered under an Offering exemption, and if it were later determined that such an exemption was not available, purchasers would be entitled to rescind their purchase agreements.

Interests are being offered to prospective investors pursuant to Tier 2 of Regulation A under the Securities Act. Unless the sale of Interests qualifies for such exemption the investors might have the right to rescind their purchase of Interests. Since compliance with these exemptions is highly technical, it is possible that if an investor were to seek rescission, such investor would succeed. A similar situation prevails under state law in those states where Interests may be offered without registration. If a number of investors were to be successful in seeking rescission, the Partnership would face severe financial demands that could adversely affect the Partnership and, thus, the non-rescinding investors. Inasmuch as the basis for relying on exemptions is factual, depending on the Partnership’s conduct and the conduct of persons contacting prospective investors and making the Offering, the Partnership will not receive a legal opinion to the effect that this Offering is exempt from registration under any federal or state law. Instead, the Partnership will rely on the operative facts as documented as the Partnership’s basis for such exemptions.

10

Non-compliance with certain securities regulations may result in the liquidation and winding up of the Partnership.

We are not registered and will not be registered as an investment company under the Investment Company Act of 1940, as amended (“Investment Company Act”), and neither our General Partner nor its manager is or will be registered as an investment adviser under the Investment Advisers Act of 1940, as amended (“Investment Advisers Act”), and thus the Interests do not have the benefit of the protections of the Investment Company Act or the Investment Advisers Act. We and our General Partner have taken the position that the Investment Company Act or the Investment Advisers Act do not apply to our operations. This position, however, is based upon applicable law that is inherently subject to judgments and interpretation. If we were to be required to register under the Investment Company Act or our General Partner were to be required to register under the Investment Advisers Act, it could have a material and adverse impact on the results of operations and expenses of the Partnership and our General Partner may be forced to liquidate and wind up the Partnership or rescind the offering of Interests.

Maintenance of an Investment Company Act exemption imposes limits on the Partnership’s operations, and if the Partnership were to become subject to the Investment Company Act, it likely could not continue its business. The Partnership intends to conduct its operations so that it is not required to register as an investment company under the Investment Company Act.

The Partnership intends to make investments that satisfy requirements that will exempt it from registration under the Investment Company Act and intends to monitor its compliance with applicable exemptions under the Investment Company Act on an ongoing basis. However, if at any time we may be deemed an “investment company,” we intend to rely on the exception set forth in Section 3(c)(5)(C) of the Investment Company Act, which excludes from the definition of investment company “any person who is not engaged in the business of issuing redeemable securities, face-amount certificates of the installment type or periodic payment plan certificates, and who is primarily engaged in one or more of the following businesses… (C) purchasing or otherwise acquiring mortgages and other liens on and interests in real estate.” The SEC Staff generally requires that, for the exception provided by Section 3(c)(5)(C) to be available, at least fifty-five percent (55%) of an entity’s assets be comprised of mortgages and other liens on and interests in real estate, also known as “qualifying interests,” and at least another twenty-five percent (25%) of the entity’s assets must be comprised of additional qualifying interests or real estate-type interests (with no more than twenty percent (20%) of the entity’s assets comprised of miscellaneous assets). We intend to acquire assets with the proceeds of this Offering in satisfaction of such SEC requirements to fall within the exception provided by Section 3(c)(5)(C) and limit our non-real estate assets in accordance with the foregoing. Notwithstanding, the staff of the SEC could possibly disagree with any of our determinations. If the staff of the SEC were to disagree with our analysis under the Investment Company Act, we would need to adjust our investment strategy. Any such adjustment in our strategy could have a material adverse effect on us. If we are deemed to be an investment company, we may be required to register as an investment company if we are unable to dispose of the disqualifying assets, which could have a material adverse effect on us, which may result in the Partnership not having, and not being able to acquire, the funds to repay the Bonds being issued in this Offering.

Registration under the Investment Company Act would require us to comply with a variety of substantive requirements that impose, among other things:

● limitations on capital structure;

● restrictions on specified investments;

● restrictions on leverage or senior securities;

● restrictions on unsecured borrowings;

● prohibitions on transactions with affiliates; and

● compliance with reporting, record keeping, voting, proxy disclosure and other rules and regulations that would significantly increase our operating expenses.

11

If we were required to register as an investment company but failed to do so, we could be prohibited from engaging in our business, and criminal and civil actions could be brought against us. Registration with the SEC as an investment company would be costly, would subject us to a host of complex regulations and would divert attention from the conduct of our business, which could materially and adversely affect us. In addition, we would no longer be eligible to offer our securities under Regulation D of the Securities Act of 1933, as amended if we were required to register as an investment company.

If we are required to register any Interests under the Exchange Act of 1934, as amended (the “Exchange Act”), it would result in significant expense and reporting requirements that would place a burden on the Partnership.

Subject to certain exceptions, Section 12(g) of the Exchange Act requires an issuer with more than $10 million in total assets to register a class of its equity securities with the Commission under the Exchange Act if the securities of such class are held of record at the end of its fiscal year by more than 2,000 persons or 500 persons who are not “accredited investors.” To the extent the Section 12(g) assets and holders limits are exceeded, we intend to rely upon a conditional exemption from registration under Section 12(g) of the Exchange Act contained in Rule 12g5-1(a)(7) under the Exchange Act (the “Reg. A+ Exemption”), which exemption generally requires that the issuer (i) be current in its Form 1-K, 1-SA and 1-U filings as of its most recently completed fiscal year end; (ii) engage a transfer agent that is registered under Section 17A(c) of the Exchange Act to perform transfer agent functions; and (iii) have a public float of less than $75 million as of the last business day of its most recently completed semi-annual period or, in the event the result of such public float calculation is zero, have annual revenues of less than $50 million as of its most recently completed fiscal year. If the number of record holders of any Securities exceeds either of the limits set forth in Section 12(g) of the Exchange Act and we fail to qualify for the Reg. A+ Exemption, we would be required to register such Securities with the Commission under the Exchange Act. If we are required to register any Securities under the Exchange Act, it would result in significant expense and reporting requirements that would place a financial burden on the Partnership and a time burden on our management.

The Partnership will either rely on the exemption for insignificant participation by benefit plan investors or the real estate operating partnership exemption under ERISA.

The Plan Assets Regulation of the Employee Retirement Income Security Act of 1974 (“ERISA”) provides that the assets of an entity will not be deemed to be the assets of a benefits plan if equity participation in the entity by benefit plan investors, including benefit plans, is not significant. The Plan Assets Regulation provides that equity participation in the entity by benefit plan investors is “significant” if, at any time, twenty-five percent (25%) or more of the value of any class of equity interest is held by benefit plan investors. If we rely on this exemption, we will not accept investments from benefit plan investments of twenty-five percent (25%) or more of the value of any class of equity interest. If withdrawal or liquidation of Interests cause the Partnership to reach twenty-five percent (25%), we may liquidate Interests of benefit plan investors without their consent until we are under such twenty-five percent (25%) limit.

The subscription agreement has a dispute resolution provision that requires disputes to be resolved by binding arbitration pursuant to Florida law, regardless of convenience or cost to you, the investor.

As part of this investment, each Investor will be required to agree to the terms of the subscription agreement. In the agreement, investors agree to waive the right to trial by jury and agree to resolve disputes arising under the subscription agreement through binding arbitration. Waiving the right to a jury trial means agreeing to have your case decided by an arbitrator rather than a jury of peers. A jury trial allows ordinary citizens to assess evidence and witness testimony, which can sometimes bring empathy or a broader perspective. An arbitrator may be more neutral but also more focused on strict legal interpretations. In addition, arbitrators may have unconscious biases or be influenced by previous similar cases, and their decision-making is not as varied as a jury panel. Arbitrators often hear numerous cases, which can sometimes affect their perception of individual cases. Furthermore, in a jury trial, you may appeal based on claims like jury misconduct or flawed jury instructions.

With arbitration under the subscription agreement, if the amount in controversy exceeds $50,000.00, any party may appeal the arbitrator’s award to a three-arbitrator panel within thirty (30) days of the final award. This waiver may not apply to claims under the Securities Act or the Exchange Act. Section 27 of the Exchange Act creates exclusive federal jurisdiction over all suits brought to enforce any duty or liability created by the Exchange Act or the rules and regulations thereunder. As a result, the dispute resolution provision may not apply to suits brought to enforce any duty or liability created by the Exchange Act or any other claim for which the federal courts have exclusive jurisdiction. You will not be deemed to have waived the Partnership’s compliance with the federal securities laws and the rules and regulations thereunder. Although we believe the provision benefits the Partnership by providing increased consistency in the application of Florida law in the types of lawsuits to which

12

it applies and in limiting our litigation costs, if a court were to find the provision inapplicable to, or unenforceable

in an action, the Partnership may incur additional costs associated with resolving such matters in other jurisdictions, which could adversely

affect its business, financial condition or results of operations. Section 22 of the Securities Act creates concurrent jurisdiction for

federal and state courts over all suits brought to enforce any duty or liability created by the Securities Act or the rules and regulations

thereunder. The Partnership believes that the dispute resolution provision applies to claims arising under the Securities Act, but there

is uncertainty as to whether a court would enforce such a provision in this context.

The arbitration provision in the subscription agreement requires you to waive the right to resolve any dispute through a class action.

By agreeing to waive the right to file or participate in a class action lawsuit or to pursue arbitration on a class, collective, or representative basis, an investor accepts the risk that they may be required to bring any claims individually, at their own expense, and without the ability to pool resources with other investors who may have similar claims. This waiver could limit your ability to recover damages or obtain relief that might otherwise be available through a collective action, and it may result in inconsistent outcomes compared to other investors.

The Partnership intends to make multiple securities offerings which increases its risk of litigation.

The Partnership is offering its securities concurrently through an offering exempt from registration under Regulation D, Rule 506(c). The rise in litigation tied to multiple security offerings is a growing trend, fuelled by increased regulatory scrutiny, complex financial structures, and the push for transparency in financial markets. When companies offer securities in multiple offerings, the complexity of managing these offerings can lead to potential oversights and misrepresentations, which, in turn, can result in legal challenges. Investors often claim that they were misled or inadequately informed about the risks or terms associated with particular offerings. This increased legal risk is particularly prevalent in sectors with intricate financial products or where companies are rapidly expanding, as the lack of detailed disclosures or inconsistencies in documentation can lead to allegations of securities fraud. As a result, companies must remain diligent in their disclosures and compliance practices, ensuring that each security offering adheres to strict standards to mitigate the potential for costly litigation.

Handling multiple security offerings can significantly strain management’s time and resources, diverting attention from core business operations and strategic initiatives.

Each securities offering requires extensive planning, regulatory compliance, and clear communication with investors. The need to prepare detailed disclosures, manage legal considerations, and coordinate with financial advisors and underwriters creates a complex landscape for management to navigate. Additionally, the ongoing reporting and oversight required for multiple securities demand dedicated resources to ensure accuracy and transparency, particularly to meet regulatory standards and avoid potential litigation. This extensive process often monopolizes management’s time and attention, limiting their capacity to focus on long-term growth strategies, operational efficiency, and product or service innovation. Consequently, while multiple offerings can attract diverse investment pools, they can also restrict management’s agility and reduce the resources available to drive the business forward.

There may be deficiencies with our internal controls that require improvements, and if we are unable to adequately evaluate internal controls, we may be subject to sanctions.

As a Tier 2 issuer, we will not need to provide a report on the effectiveness of our internal controls over financial reporting, and we will be exempt from the auditor attestation requirements concerning any such report so long as we are a Tier 2 issuer. We are in the process of evaluating whether our internal control procedures are effective and therefore there is a greater likelihood of undiscovered errors in our internal controls or reported financial statements as compared to issuers that have conducted such evaluations.

We will be subject to ongoing public reporting requirements that are less rigorous than rules for more mature public partnerships, and our investors receive less information.

We are required to report on an ongoing basis under the reporting rules set forth in Regulation A for Tier 2 issuers. The ongoing reporting requirements under Regulation A are more relaxed than for public partnerships reporting under the Exchange Act. The differences include, but are not limited to, being required to file only annual and semi-annual reports, rather than annual and quarterly reports. Annual reports are due within 120 calendar days after the end of our fiscal year, and semi-annual reports are due within 90 calendar days after the end of the first six months of our fiscal year.

13

We also may elect to become a public reporting partnership under the Exchange Act. If we elect or are required to do so, we will be required to publicly report on an ongoing basis as an emerging growth partnership, as defined in the JOBS Act, under the reporting rules set forth under the Exchange Act. For so long as we remain an emerging growth partnership, we may take advantage of certain exemptions from various reporting requirements that are applicable to other Exchange Act reporting partnerships that are not emerging growth partnerships, including, but not limited to:

● not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act;

● being permitted to comply with reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements; and

● being exempt from the requirement to hold a non-binding advisory vote on executive compensation and member approval of any golden parachute payments not previously approved.

In either case, we will be subject to ongoing public reporting requirements that are less rigorous than Exchange Act rules for partnerships that are not emerging growth partnerships, and investors could receive less information than they might expect to receive from more mature public partnerships.

Risks related to the partnership’s ability to continue as a going concern.

The Partnership’s consolidated financial statements have been prepared on a going concern basis, which assumes that the Partnership will be able to realize its assets and satisfy its liabilities in the normal course of business. However, the Partnership has not yet generated sufficient revenues to fund its ongoing operations and requires additional capital to execute its business plan and meet its obligations as they become due. The Partnership’s ability to continue as a going concern is dependent upon its ability to raise additional capital and to achieve profitable operations.

Management intends to seek additional financing through this Regulation A offering and is pursuing additional capital through a Regulation D, and may seek other debt or equity financings. There can be no assurance that any such financing will be available on acceptable terms, in sufficient amounts, or at all. The failure to obtain additional financing, delays in raising capital, or an inability to achieve profitable operations could materially and adversely affect the Partnership’s liquidity, financial condition, and ability to continue operations. These conditions and uncertainties raise substantial doubt about the Partnership’s ability to continue as a going concern. If the Partnership is unable to continue as a going concern, investors may lose some or all of their investment, and the Partnership may be required to significantly curtail, delay, or cease operations, sell assets at unfavorable prices, or seek protection under applicable insolvency laws. The consolidated financial statements do not include any adjustments that might result from the outcome of these uncertainties.

The Partnership was recently formed, has a limited track record and minimal operating history from which you can evaluate the Partnership or this investment.

The Partnership was recently formed and has not generated any significant revenues and has limited operating history upon which prospective investors may evaluate their performance. No guarantee can be given that the Partnership will achieve its investment objectives or the underlying assets to be acquired will be successfully monetized.

Given our start-up nature, investors may not be interested in making an investment and we may not be able to raise all of the capital we seek, which could have a material adverse effect upon the Partnership and the value of your Interests.

There can be no guarantee that we will reach our funding target from potential investors. In the event we do not raise sufficient funds through this Offering, we may not be able to achieve our investment objectives and may seek capital elsewhere, which could be on different terms than those hereby offered.

14

Because our management will have broad discretion and flexibility in how the net proceeds from this Offering are used, we may use the net proceeds in ways in which you disagree.

The intended use of proceeds from this offering is more particularly described in the Section titled “Use of Proceeds” on page 36 however, such description is not binding, and the actual use of proceeds may differ from the description contained therein. Accordingly, our management will have significant discretion and flexibility in applying the net proceeds of this offering. You will be relying on the judgment of our management with regard to the use of these net proceeds, and you will not have the opportunity, as part of your investment decision, to assess whether the net proceeds are being used appropriately. It is possible that the net proceeds will be invested in a way that does not yield a favourable, or any, return for us. The failure of our management to use such funds effectively could have a material adverse effect on our business, financial condition, operating results and cash flow.

Our success depends in large part upon our General Partner and its ability to execute our business plan.

The successful operation of the Partnership is dependent on the ability of our General Partner to source, acquire and manage our assets. As our General Partner was formed recently, and is an early-stage startup partnership, it has no operating history which evidences its ability to source, acquire, manage and utilize our intended assets. The success of the Partnership will be highly dependent on the expertise and performance of our General Partner and its team to source, acquire and manage the underlying assets. There can be no assurance that these individuals will continue to be associated with our General Partner. The loss of the services of one or more of these individuals could have a material adverse effect on our investments and/or operations.

You will not have the opportunity to evaluate our investments before we make them, which makes your investment more speculative.

You will be unable to evaluate the economic merit of our investments before we invest in them and will be entirely relying on the ability of our General Partner to select our investments. Furthermore, our General Partner will have broad discretion in implementing policies regarding tenant or mortgagor creditworthiness, and you will not have the opportunity to evaluate potential tenants, managers or borrowers. These factors increase the risk that your investment may not generate returns comparable to our competitors.

We may need additional capital, which may be on terms more or less favourable than those offered in this offering.

We may require additional capital and may require additional cash resources due to changed business conditions or other future developments. If our resources are insufficient to satisfy our cash requirements, we may seek to sell additional equity or debt securities or incur debt. The sale of additional equity securities could result in additional dilution to our members. The incurrence of additional indebtedness would result in increased debt service obligations and could result in operating and financing covenants that would restrict our operations. We cannot assure you that financing will be available in amounts or on terms acceptable to us, if at all, or that the terms provided won’t be more or less favourable than those hereby offered.

Limited Partners have limited voting rights.

Investors have limited voting rights. Our General Partner will have most of the control over the Partnership. Limited Partners will only be able to vote in limited circumstances. Investors may not necessarily agree with the decisions of the General Partner or decisions may not be in the best interests of all the investors but only a limited number, and investors may not have an ability to influence these decisions. See “Securities Being Offered” on page 69 for a description of matters on which Limited Partners may vote.

We may experience liability for alleged or actual harm to third parties and costs of litigation.

We are subject to the risk of lawsuits filed by tenants, borrowers, past and present employees, contractors, competitors, business partners, and others in the ordinary course of business. As with all legal proceedings, no assurance can be provided as to the outcome of these matters, and legal proceedings can be expensive and time consuming. The Partnership may not be successful in the defense or prosecution of these lawsuits, which could result in settlements or damages that could result in substantial losses to the Partnership. Even if the Partnership is successful, there may be substantial costs associated with the legal proceeding, and our General Partner may be delayed or prevented from implementing the business plan of the Partnership.

15

Risks Related to Potential Conflicts of Interest

The Partnership expects to acquire Mortgage loans from BW Capital, an affiliate of the General Partner, which creates inherent conflicts of interest.

Because the General Partner and its affiliates may be involved on both sides of transactions between the Partnership and BW Capital, the negotiation, pricing, underwriting assumptions, structure, and timing of such acquisitions may not reflect terms that would be obtained through arm’s-length negotiations or competitive market processes. The General Partner may have financial or strategic incentives to cause the Partnership to purchase loans originated or held by affiliates, including loans that generate origination, servicing, or other fee income for affiliates, even where alternative investments may be available. The Partnership may rely on information or underwriting analyses prepared by affiliates, which may limit the independence of the diligence process. As a result, loans acquired from affiliates may differ in credit quality, liquidity, collateral characteristics, or expected performance compared to loans sourced from unaffiliated market participants, and investors must rely on the General Partner’s good faith judgment to manage these conflicts.

We are significantly dependent on BW Capital (“Lender”), an affiliate of our General Partner. The loss of Lender or its services would have an adverse effect on our business, operations and prospects in that we may not be able to obtain new Lender services under the same financial arrangements, which could result in a loss of your investment.

Our business plan is significantly dependent upon the Lender. It would be difficult to replace the Lender at such an early stage of development of the Partnership. While we could possibly find an unrelated third party who would offer the Partnership better terms and services, we believe that the loss of the Lender’s services would have an adverse effect on our business, operations and prospects, and could result in the loss of one’s investment. There can be no assurance that we would be able to locate or replace the Lender, should their services be discontinued. In the event that we are unable to replace Lender, we would be required to cease pursuing our business plan, which could result in a loss of your investment.

BW Capital and other affiliates may receive origination fees, servicing fees, processing fees, and other compensation in connection with loans acquired by the Partnership, which may create incentives that are not aligned with investor returns.

Affiliates may earn compensation at multiple stages of a loan’s lifecycle, including origination, servicing, administration, and restructuring activities. Because certain fees may be based on loan balances or servicing activity, affiliates may have incentives to originate larger loans, maintain higher balances, or pursue loan modifications that preserve fee streams. These layered compensation arrangements may reduce net returns to investors and may influence decisions regarding loan selection, structure, timing of transfers, or workout strategies. Certain affiliate compensation may be earned regardless of loan performance, which may further diverge affiliate incentives from investors seeking long-term capital preservation and income.

Affiliates receiving servicing or related fees may have incentives to approve loan modifications or extensions that preserve fee income rather than maximizing immediate recoveries.

Because servicing compensation may be tied to outstanding loan balances or servicing duration, affiliates may benefit economically from extending loans or maintaining borrower relationships rather than pursuing prompt enforcement or liquidation. Decisions regarding amendments, restructurings, foreclosures, or loan sales may therefore involve competing considerations, including reputational or economic interests of affiliated platforms. As a result, the Partnership may pursue strategies that differ from those that might be selected by an independent third-party servicer.

Investors will have limited ability to approve or challenge transactions between the Partnership and affiliates of the General Partner.

The Partnership may enter into affiliate transactions, including acquiring, servicing, administering, or disposing of Mortgage loans involving BW Capital, without independent investor approval. The General Partner may therefore have broad discretion in determining the terms and timing of affiliate transactions. Because investors will not participate in day-to-day management decisions and may have limited voting rights, they may have little practical ability to prevent or modify transactions that present conflicts of interest. Investors must rely on the General Partner’s interpretation of its fiduciary and contractual duties, which may not eliminate all potential conflicts.

16

The purchase price and valuation of loans acquired from affiliates may be determined or influenced by the General Partner, which may affect reported performance and Net Asset Value (“NAV”).

Loans purchased from BW Capital may be priced using internal models or affiliate-provided information and may not be subject to competitive bidding, independent appraisals, or third-party fairness opinions. Because valuations directly impact NAV, investor reporting, and potentially the calculation of fees or distributions, the General Partner’s involvement in valuation methodologies may create incentives that are not fully aligned with investor interests. Investors must rely on the General Partner’s good faith judgment in determining fair value, and actual realized values may differ materially from reported valuations.

The executive officer and sole director of the General Partner also serves as an officer of BW Capital and other affiliated entities, which may result in competing fiduciary duties and allocation conflicts.

This individual may allocate management time, investment opportunities, or resources among multiple affiliated entities, including those engaged in similar lending activities. Conflicts may arise with respect to the allocation of new investments, the timing and terms of loan acquisitions, and compensation arrangements with affiliates. These competing responsibilities may result in actions or inactions that are detrimental to the Partnership or its investment objectives.

The General Partner and its affiliates may sponsor or manage other investment vehicles that pursue similar strategies, which may compete with the Partnership for investment opportunities and management attention.

To the extent the General Partner and its affiliates devote time to other business activities, they may have reduced availability to monitor the Partnership’s operations or investment portfolio, which could adversely affect performance.

The General Partner, certain Partners, and their affiliates will receive compensation from the Partnership that has not been negotiated at arm’s length.

Fees for management, asset management, servicing, administrative, or other operational services may be more favorable to affiliates than terms that might be obtained from unaffiliated service providers. Because certain compensation may be earned regardless of the Partnership’s performance, affiliates may have incentives to increase transaction activity or assets under management, which may reduce net returns to investors. See “Management Compensation, Fees, and Expenses” for additional information.

Attorneys, accountants, and other professionals representing the Partnership may also represent the General Partner or its affiliates, which may create conflicts of interest.

These professionals may not have separate counsel exclusively representing investor interests, and in the event of conflicts, such professionals may withdraw from representing one or more parties. Multiple representation may limit the independence of advice provided to the Partnership.

We do not have a conflict-of-interest policy.

Our General Partner and its affiliates will try to balance our interests with their own. However, to the extent that such parties take actions that are more favourable to other people or entities than the Partnership, these actions could have a negative impact on our financial performance and, consequently, on distributions to investors and the value of our assets. We have not adopted, and do not intend to adopt in the future, either a conflicts of interest policy or a conflicts resolution policy.

Conflicts may result in the use of certain service providers over others.

Our General Partner and our operators will engage with, on behalf of the Partnership, a number of brokers, asset sellers, insurance partnerships, and maintenance providers and other service providers and thus may receive in-kind discounts. In such circumstances, it is likely that these in-kind discounts may be retained for the benefit of our General Partner or operators and not the Partnership. Our General Partner or operators may be incentivized to choose a service provider or seller based on the benefits they are to receive.

17

There may be conflicting interests of investors.

Our General Partner will determine whether or not to acquire or liquidate our assets. When determining to acquire or liquidate an investment, our General Partner will do so considering all of the circumstances at the time, which may include obtaining or paying a price for an underlying asset that is in the best interests of some but not all of the investors.

Conflicts may exist between service providers, the Partnership, our General Partner and its affiliates.

Our service providers may provide services to our General Partner and its affiliates. Because such providers may represent both the Partnership and such other parties, certain conflicts of interest exist and may arise. To the extent that an irreconcilable conflict develops between us and any of the other parties, providers may represent such other parties and not the Partnership. Providers may, in the future, render services to us or other related parties with respect to activities relating to the Partnership as well as other unrelated activities. Legal counsel is not representing any prospective investors in connection with this offering and will not be representing interest holders of the Partnership. Prospective investors are advised to consult their own independent counsel with respect to the other legal and tax implications of an investment in our Interests.

Risks Related to our Business

The Partnership will experience those risks associated with an investment in and ownership of Interests in a newly formed limited Partnership.

There are significant restrictions placed on the Partnership via the Partnership Agreement, including, but not limited to, restrictions on transfer of Interests, voting, distributions, withdrawal, management, dissolution, and dispute resolution.

There are significant risk factors relating to our business generally.

Our business, operating results and financial condition could be adversely affected by any of the following specific risks. In addition to the risks described below, we may encounter risks that are not currently known to us or that we currently deem immaterial, which may also impair our business operations.

We have no established investment criteria limiting the geographic concentration of our investments in Mortgage Loans.

Our Mortgage Loans may be concentrated in a limited number of geographic locations, and certain Mortgage Loans in which we invest may be secured by a single property or properties in a limited number of geographic locations. We plan to have our investment activities take place in the United States. Any weakness of economic conditions in the areas where we have a geographic concentration of Mortgage loans may have a material adverse effect on our financial condition.

Our Mortgage Loans may carry the risks associated with significant geographical concentration. Therefore, it is likely that we will establish a plan in the future to limit our exposure to geographical concentration risk. If our loans are overly concentrated in certain geographic areas and become exposed to significant declines in general economic conditions in those areas, caused by inflation, overbuilding of commercial properties, recession, relocations of businesses outside the area, acts of terrorism, outbreak of hostilities or other international or domestic occurrences, unemployment, changes in securities markets or other factors could impact these local economic conditions. A deterioration of economic conditions in the geographic area in which our Mortgage Loans may be concentrated could have an adverse effect on our business, including limited the ability of tenants to pay rent, reducing the demand for new financings, limiting the ability of customers to pay financed amounts and reducing the value of our Properties and the value of the collateral securing our Mortgage Loans.

We need a substantial amount of liquidity to operate our business.

We may not be able to obtain sufficient funding for our future operations from internally generated cash flows and sales of debt, in addition to, possible funding from commercial banks, or other sources. We are a newly formed entity and our access to the capital markets and commercial bank financing may be impaired due to a lack of operating history and established earnings. As a consequence, our results of operations, financial condition and cash flows will be materially and adversely affected by our general and administrative expenses.

18

We require a substantial amount of cash liquidity to operate our business. Among other things, we use such cash liquidity to:

● Acquire real property loans; satisfy working capital requirements and pay operating expenses;

● pay taxes; and

● pay interest expense

We will attempt to match the maturities of our funding obligations with the estimated holding periods of our investments. There can be no assurance that we will be successful in being able to fund our Mortgage Loans with match maturity funding.

We will have fewer funds available for investments and our profitability will be reduced if we pay distributions to Limited Partners from sources other than our cash flow from operations.

We may pay distributions to Limited Partners from any source, including Offering proceeds, borrowings, or sales of assets. We have not placed a cap on the use of proceeds to fund distribution payments. We intend to pay distributions to Limited Partners from cash flow from our operations. Until the proceeds from this Offering are fully invested and from time to time during the operational stage, however, we may not generate sufficient cash flow from operations to pay distributions. If we pay distributions from sources other than our cash flow from operations, we will have fewer funds available for investments, and our profitability may be reduced.

Payment of fees, distributions and expense reimbursements to the General Partner and its affiliates will reduce cash available for investment and for distribution to our Limited Partners.

The General Partner and its affiliates perform services for us in connection with the offer and sale of our Interests, the management and servicing of our investments, and administrative and other services. These fees, distributions and expense reimbursements are substantial and reduce the amount of cash available for investment and distribution to our Limited Partners.

Our Results of Operations May Be Impaired if we fail to comply with regulations.

Failure to materially comply with all laws and regulations applicable to us could materially and adversely affect our ability to operate our business. Our business is subject to numerous federal and state laws and regulations, which are, among other things:

● require disclosures to our customers;

● define our rights to foreclose and sell real estate; and

● maintain safeguards designed to protect the security and confidentiality of customer information.

We believe that we are in compliance in all material respects with all such laws and regulations, and such laws and regulations have had no material adverse effect on our ability to operate our business. However, we may be materially and adversely affected if we fail to comply with:

● applicable laws and regulations;

● changes in existing laws or regulations;

● changes in the interpretation of existing laws or regulations; or