As filed with the Securities and Exchange Commission on September 5, 2025

File No. 024-12633

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 1-A

(Amendment No. 2)

REGULATION A OFFERING CIRCULAR

UNDER THE SECURITIES ACT OF 1933

MASTERWORKS VAULT 6, LLC

(Exact name of issuer as specified in its charter)

Delaware

(State of other jurisdiction of incorporation or organization)

1 World Trade Center, 57th Floor

New York, New York 10007

Phone: (203) 518-5172

(Address, including zip code, and telephone number,

including area code of issuer’s principal executive office)

Joshua B. Goldstein

General Counsel and Secretary

Masterworks Vault 6, LLC

1 World Trade Center, 57th Floor

New York, New York 10007

Phone: (203) 518-5172

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

| 7380 | 39-2607186 | |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

EXPLANATORY NOTE

This Offering Circular contains certain terms and disclosures that are different from those in other offerings conducted or proposed to be conducted on the Masterworks Platform. Such changes will not apply to any Masterworks offering unless and until the offering statement of which this Offering Circular forms an integral part has been qualified by the Securities and Exchange Commission.

An offering statement pursuant to Regulation A relating to these securities has been filed with the Securities and Exchange Commission. Information contained in this preliminary offering circular is subject to completion or amendment. To the extent not already qualified under Regulation A, these securities may not be sold nor may offers to buy be accepted before the offering statement filed with the Securities and Exchange Commission is qualified. This preliminary offering circular shall not constitute an offer to sell or the solicitation of an offer to buy nor may there be any sales of these securities in any state in which such offer, solicitation or sale would be unlawful before registration or qualification under the laws of any such state. We may elect to satisfy our obligation to deliver a final offering circular by sending you a notice within two business days after the completion of our sale to you that contains the URL where the final offering circular or the offering statement in which such final offering circular was filed may be obtained.

MASTERWORKS VAULT 6, LLC

Preliminary Offering Circular

September 5, 2025

Subject to Completion

Offering of Series Class A ordinary shares

Representing Series Class A Limited Liability Company Interests

Masterworks Vault 6, LLC, which we refer to as “we,” “us,” “our,” “Masterworks Vault 6” or the “Company,” is a Delaware protected series limited liability company that has been formed to facilitate investment in individual works of art (“Artworks”) that will be beneficially owned by individual series of the Company. Each series will indirectly hold title to the specific Artwork that it acquires through a Cayman Islands subsidiary. We are offering Class A shares representing Class A limited liability company interests of each series of the Company reflected in the “Series Offering Table” beginning on page 1 of this Offering Circular. There is no minimum number of Class A shares or dollar amount that needs to be sold of a series as a condition of any closing of the offering of a series. Subscriptions, once received, are irrevocable by investors.

We believe that the Class A shares of a series represent an effective means for investors to gain economic exposure to the Artwork held by that series and an investment in multiple series can provide exposure to the broader Post-War and Contemporary collecting categories of the art market. The Class A shares of a series represent an investment solely in a particular series and, thus, indirectly in the Artwork owned by that series. Artwork will be held for an indefinite period and may be sold at any time following the final closing of the offering of such series.

Our series offerings are conducted as a continuous offering pursuant to Rule 251(d)(3) of Regulation A, meaning that while the offering of a particular series is continuous, active sales of series Class A shares may happen sporadically over the term of the offering.

There will be a separate closing, or closings, with respect to each series offering. An initial closing and each subsequent closing of a series offering will take place on the date subscriptions for the maximum number of series Class A shares have been accepted or an earlier date or dates determined by us in our sole discretion. The offering period for any series will not exceed 24 months from the qualification date of the offering statement that includes such series. We reserve the right to terminate a series offering for any reason at any time prior to the initial closing of such series offering. No securities are being offered by existing security-holders.

Each series offering is being conducted pursuant to Regulation A of Section 3(6) of the Securities Act of 1933, as amended (the “Securities Act”), for Tier 2 offerings.

Our affiliate Masterworks, LLC owns an online investment platform located at https://www.masterworks.com/ (the “Masterworks Platform”) that allows investors to acquire ownership of an interest in special purpose companies such as the Company that invest in distinct Artworks or a collection of Artworks. Once an investor establishes a user profile on the Masterworks Platform, they can browse and screen potential artwork investments, view details of an investment and sign contractual documents online.

We anticipate that Class A shares will be listed for trading on an alternative trading system operated by North Capital Private Securities Corporation, an SEC-registered broker-dealer (the “ATS”) approximately 90 days after the series offering is fully subscribed. Although the availability of secondary trading may provide a potential liquidity option for some investors, particularly in the U.S. and certain non-U.S. jurisdictions, there is no guarantee that an active market will develop or be sustained. Additionally, the price at which Class A shares trade on the ATS may not reflect their fair value or their net asset value, or “NAV”, which is the estimated value of the underlying Artwork represented by the Class A shares.

No sales of Class A shares of any series will occur prior to the qualification of the Offering Statement by the SEC or the qualification by the SEC of any post-qualification amendment to the Offering Statement which contains a description of such series. All Class A shares will be offered in all jurisdictions at the same price that is set forth in this offering circular.

| Series | Number of Shares | Price to Public | Underwriter Discounts and Commissions(1) | Proceeds, Before Expenses, to Issuer(2) | ||||||||||||

| (1) | The Company has not engaged underwriters in connection with any series offering. The Company intends to distribute the Class A shares through the Masterworks Platform. See the section entitled “Plan of Distribution” of this offering circular for additional information. |

| (2) | This amount does not include estimated offering expenses, all of which will be paid by Masterworks rather than from the net proceeds of the series offerings. |

The Class A shares of each series are to be offered primarily through the Masterworks Platform. Neither Masterworks, LLC nor any other affiliated entity involved in the offer and sale of the Class A shares of a series is currently a member firm of the Financial Industry Regulatory Authority, Inc. (“FINRA”) and no person associated with us will be deemed to be a broker solely by reason of his or her participation in the sale of the Class A shares of a series.

To invest in any series offering you must represent to us that the aggregate purchase price you pay for your investment is not more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov. We retain complete discretion to determine that subscribers are “qualified purchasers” (as defined in Regulation A under the Securities Act) in reliance on the information and representations provided to us regarding their financial situation.

An investment in the Class A shares of a series is subject to certain risks and should be made only by persons or entities able to bear the risk of and to withstand the total loss of their investment. Prospective investors should carefully consider and review the information under the heading “Risk Factors” beginning on page 8.

This offering is made pursuant to Regulation A, which is an exemption from the registration requirements of the Securities Act of 1933, as amended (the “Securities Act”). The SEC has not made an independent determination that the securities offered are exempt from registration or approved or disapproved of the merits of the securities offered, nor has it reviewed the accuracy or completeness of this offering circular. Regulation A allows us to offer investments in a streamlined, cost-effective way that may benefit investors, but it also means that investors should carefully review the offering circular and related materials to fully understand the terms and risks.

Periodically, we will provide an amendment or supplement to the offering circular that may add, update or change information contained in this offering circular. Any statement that we make in this offering circular will be modified or superseded by any inconsistent statement made by us in a subsequent amendment or supplement to the offering circular. The offering statement we filed with the SEC includes exhibits that provide more detailed descriptions of the matters discussed in this offering circular. You should read this offering circular and the related exhibits filed with the SEC and any amendment or supplement to the offering circular, together with additional information contained in our annual reports, semi-annual reports and other reports and information statements that we will file periodically with the SEC. See the section entitled “Where You Can Find More Information” below for more details.

Our principal office is located at 1 World Trade Center, 57th Floor, New York, New York 10007 and our phone number is (203) 518-5172. Our corporate website address is located at www.masterworks.com. Information contained on, or accessible through, the website is not a part of, and is not incorporated by reference into, this offering circular.

Our Investor Services team is available to provide administrative assistance to prospective investors, including navigating the investment process and providing information included in this offering circular in response to inquiries regarding investments in current offerings. In addition, our team of dedicated investment adviser representatives provides advisory services related to previously qualified offerings sponsored by Masterworks. See “Plan of Distribution” and “Advisory Services” for further information. We encourage all prospective investors to reach out with questions at any time after the offering statement is qualified by the SEC at help@masterworks.com.

This offering circular is following the offering circular format described in Part II (a)(1)(i) of Form 1-A.

The date of this offering circular is ______, 2025.

TABLE OF CONTENTS

We have not authorized anyone to provide any information other than that contained or incorporated by reference in this offering circular prepared by us or to which we have referred you. We do not take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This offering circular is an offer to sell only the Class A shares of each series offered hereby but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this offering circular is current only as of its date, regardless of the time of delivery of this offering circular or any sale of Class A shares of a series.

For investors outside the United States: We have not done anything that would permit each series offering or possession or distribution of this offering circular in any jurisdiction where action for that purpose is required, other than the United States. You are required to inform yourselves about and to observe any restrictions relating to each series offering and the distribution of this offering circular.

| i |

Certain data included in this offering circular is derived from information provided by third-parties that we believe to be reliable. The discussions contained in this offering circular relating to the Artwork, the artist, the art market and the art industry are taken from third-party sources that the Company believes to be reliable and reasonable, and that the factual information is fair and accurate. Certain data is also based on our good faith estimates which are derived from management’s knowledge of the industry and independent sources. Industry publications, surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but there can be no assurance as to the accuracy or completeness of included information. While we believe the third-party data and estimates included in this offering circular to be reasonable, we have not independently verified their accuracy or the assumptions underlying them. The art market lacks uniform data standards, and statistics may vary across sources or become outdated. As such, we advise investors to view art market data as contextual rather than predictive. Insights and reports for the art market are regularly distributed by Masterworks to investors via the Masterworks Platform and through email and investment adviser representatives are available to investors for further support on the art market as further described under “Advisory Services” herein. The art market data presented in this offering circular involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such data. While we are not aware of any material misstatements regarding any market, industry or similar data presented herein, such data was derived from third party sources and reliance on such data involves risks and uncertainties.

We own or have applied for rights to trademarks or trade names that we use in connection with the operation of our business, including our corporate names, logos and website names. In addition, we own or have the rights to copyrights, trade secrets and other proprietary rights that protect our business. We do not own the copyright to the Artwork, as such term is defined below, acquired by a series. This offering circular may also contain trademarks, service marks and trade names of other companies, which are the property of their respective owners. Our use or display of third parties’ trademarks, service marks, trade names or products in this offering circular is not intended to, and should not be read to, imply a relationship with or endorsement or sponsorship of us. Solely for convenience, some of the copyrights, trade names and trademarks referred to in this offering circular are listed without their ©, ® and ™ symbols, but we will assert, to the fullest extent under applicable law, our rights to our copyrights, trade names and trademarks. All other trademarks are the property of their respective owners.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This offering circular contains certain forward-looking statements that are subject to various risks and uncertainties. Forward-looking statements are generally identifiable by use of forward-looking terminology such as “may,” “will,” “should,” “potential,” “plan,” “intend,” “expect,” “outlook,” “seek,” “anticipate,” “estimate,” “approximately,” “believe,” “could,” “project,” “predict,” or other similar words or expressions. Forward-looking statements are based on certain assumptions, discuss future expectations, describe future plans and strategies, or state other forward-looking information. Our ability to predict future events, actions, plans or strategies is inherently uncertain. Although we believe that the expectations reflected in our forward-looking statements are based on reasonable assumptions, actual outcomes could differ materially from those set forth or anticipated in our forward-looking statements. Factors that could cause our forward-looking statements to differ from actual outcomes include, but are not limited to, those described under the heading “Risk Factors.” Readers are cautioned not to place undue reliance on any of these forward-looking statements, which reflect our views as of the date of this offering circular. Furthermore, except as required by law, we are under no duty to, and do not intend to, update any of our forward-looking statements after the date of this offering circular, whether as a result of new information, future events or otherwise.

| ii |

STATE LAW EXEMPTION AND PURCHASE RESTRICTIONS

The Class A shares of each series are being offered and sold only to “qualified purchasers” (as defined in Regulation A under the Securities Act). As Tier 2 offerings pursuant to Regulation A under the Securities Act, the series offerings are exempt from state law “Blue Sky” review, subject to meeting certain state filing requirements and complying with certain anti-fraud provisions, to the extent that the Class A shares of each series offered hereby are offered and sold only to “qualified purchasers”. “Qualified purchasers” include: (i) “accredited investors” under Rule 501(a) of Regulation D and (ii) all other investors so long as their investment in any of the interests of the Company (in connection with any series offered under Regulation A) does not represent more than 10% of the greater of their annual income or net worth (for natural persons), or 10% of the greater of annual revenue or net assets at fiscal year-end (for non-natural persons). Accordingly, we reserve the right to reject any investor’s subscription in whole or in part for any reason, including if we determine in our sole and absolute discretion that such investor is not a “qualified purchaser” for purposes of Regulation A.

To determine whether a potential investor is an “accredited investor” for purposes of satisfying one of the tests in the “qualified purchaser” definition, the investor must be a natural person who:

| 1. | has a net worth, or joint net worth with the person’s spouse or spousal equivalent, that exceeds $1,000,000 at the time of the purchase, excluding the value of the primary residence of such person; or | |

| 2. | had earned income exceeding $200,000 in each of the two most recent years or joint income with a spouse or spousal equivalent exceeding $300,000 for those years and has a reasonable expectation of reaching the same income level in the current year; or | |

| 3. | is holding in good standing one or more professional certifications or designations or credentials from an accredited educational institution that the SEC has designated as qualifying an individual for accredited investor status; or | |

| 4. | is a “family client,” as defined by the Investment Advisers Act of 1940, of a family office meeting the requirements in Rule 501(a) of Regulation D and whose prospective investment in the issuer is directed by such family office pursuant to Rule 501(a) of Regulation D. |

For purposes of determining whether a potential investor is a “qualified purchaser,” annual income and net worth should be calculated as provided in the “accredited investor” definition under Rule 501 of Regulation D. In particular, net worth in all cases should be calculated excluding the value of an investor’s home, home furnishings and automobiles.

USE OF CERTAIN TERMS AND DEFINITIONS

In this offering circular, certain capitalized terms are used in the context of a particular series or offering and the same capitalized terms may be used in another context to refer generically to all series or offerings conducted by the Company. Accordingly, it is important to consider the context in which such capitalized terms are used. Unless the context indicates otherwise, the following terms have the following meaning:

| ● | “Artwork” or “Artworks” refers to any painting, sculpture or other artistic object owned by a series or generically to all such artistic objects owned by the Company. | |

| ● | “Board of Managers” refers to the board of managers of the Company. | |

| ● | “Class A share” or “Class A shares” refers to a Class A ordinary share or Class A ordinary shares collectively, representing membership interests of one or all series in the Company. | |

| ● | “Class B share” or “Class B shares” refers to a Class B ordinary share or Class B ordinary shares collectively, representing profits interests in one or all series of the Company. | |

| ● | “Class C share” refers to a Class C ordinary share, representing a special class of membership interests of one or all series in the Company, which have no economic rights or obligations and have no voting rights, but solely represents so-called “kick-out” rights, which means that the holder of a Class C share has the right to reconstitute, remove and or replace the Board of Managers of the Company pursuant to the Company’s operating agreement. | |

| ● | “Company” refers to Masterworks Vault 6, LLC, a Delaware series limited liability company. | |

| ● | “Masterworks” refers to Masterworks, LLC, and or its wholly owned subsidiaries, but does not include Masterworks Vault 6, LLC or Masterworks Advisers, LLC (“Masterworks Advisers”). | |

| ● | “Masterworks Cayman” refers to a Cayman Islands segregated portfolio company that will hold title to the Artwork acquired by each series in a segregated portfolio. | |

| ● | “Masterworks Platform” refers to the first online art investment platform located at https://www.masterworks.com/. The Masterworks Platform gives eligible investors the ability to: |

| ○ | Browse art investment offerings of each series in the Company; | |

| ○ | Transact entirely online, including review and execution of legal documentation, funds transfer and ownership recordation; | |

| ○ | Execute trades in shares issued by Masterworks issuers via the ATS; and | |

| ○ | Manage and track investments easily through an online portfolio management tool. |

| ● | “offering” or “offerings” refers to the offering of Class A shares of one or more series of the Company. | |

| ● | “series” refers to the series of the Company, individually and collectively. | |

| ● | “Shares” refers generically to the Class A shares and Class B shares of a series or all series collectively, of the Company. | |

| ● | “SPC Ordinary share” or “SPC Ordinary shares” refers to an ordinary share or ordinary shares collectively, representing ordinary equity interests in each segregated portfolio of Masterworks Cayman, which are issued by each segregated portfolio to each series upon acquisition of the Artwork. | |

| ● | “SPC Preferred share” or “SPC Preferred shares” refers to a preferred share or preferred shares collectively, representing preferred equity interests in each segregated portfolio of Masterworks Cayman, which are issued by each segregated portfolio to Masterworks in respect of management and administration services. | |

| ● | “SPC shares” refers generically to SPC Ordinary shares and SPC Preferred shares, collectively. | |

| ● | “we,” “our,” “ours,” or “us,” refer to Masterworks Vault 6, LLC, a Delaware series limited liability company, all series of the Company and the segregated portfolios of Masterworks Cayman that will hold title to the Artwork of each series, individually or collectively, as the context requires. |

Dollar amounts throughout this offering circular have been rounded to the nearest whole dollar and information such as auction sale prices, that were originally denominated in a currency other than the U.S. dollar have been converted into U.S. dollars at the prevailing exchange rate on the applicable date of such sale transaction per publicly available data.

| iii |

SERIES OFFERING TABLE

The table below shows key information related to the offering of each series that is either “Not Yet Open”, “Open” or “Closed”. When an offering has the status “Not Yet Open” the offering circular that describes the offering has not yet been qualified by the SEC. When an offering has the status “Open”, the offering circular that describes the offering has been qualified by the SEC and Class A shares in respect of such offering are available for investment. When an offering has the status “Closed”, all funds have been received by investors, all subscriptions have been accepted and all Class A shares offered have been issued. The offering price per Class A share of each series will be $20.00.

Series Name | Artist | Artwork | Offering Size | Class A shares | Opening Date | Status | ||||||||||||

| (1) | We expect that the approximate date of commencement of proposed sale to the public is promptly following qualification by the SEC of the Offering Statement which contains a description of this series, including information relating to the artist and artwork held by the series. |

This summary highlights selected information contained elsewhere in this offering circular. This summary does not contain all of the information you should consider before investing in the Class A shares. You should read this entire offering circular carefully, especially the risks of investing in the Class A shares discussed under “Risk Factors,” before making an investment decision.

Overview

Issuer

Masterworks Vault 6, LLC is a Delaware series limited liability company formed to facilitate investments in high-value artworks. The assets and liabilities of each series are legally segregated from the assets and liabilities of every other series, and the Class A shares of each series will represent an investment in a single Artwork for an indefinite period.

Series do not hold Artwork directly, but rather title to each Artwork is held through a subsidiary of each series which is a designated segregated portfolio of Masterworks Cayman, SPC, a segregated portfolio company organized under the laws of the Cayman Islands. Investors in a particular series will have an indirect investment interest in the Artwork beneficially owned by that particular series and will not have an interest in any other series or Artwork beneficially owned by the Company.

Masterworks

Masterworks, which was founded in 2017 to make art an investable asset class, operates the first and largest online art investment platform. As of March 31, 2025, Masterworks investment entities have securitized over 450 artworks totaling more than $1.2 billion in purchase price, making it a significant participant in the global art ecosystem. With a dedicated acquisitions team and proprietary artwork valuation models, Masterworks sources artworks through relationships with galleries, auction houses and collectors that would typically be inaccessible to individual investors. By fractionalizing beneficial ownership of these artworks through SEC-qualified offerings, Masterworks enables broader participation in a market traditionally available only to ultra-high-net-worth individuals and institutions.

Investment Highlights

The investment objective of each series is long-term capital appreciation. We may display and promote the Artworks to enhance their value and broaden their exposure to the art-viewing public, but the primary factors involved in achieving our investment objectives are driven by the art market and the market demand for a particular artist and artwork. No dividends or interim distributions are anticipated. Any distribution to Class A shareholders will occur only upon a successful sale of the Artwork, and only to the extent of net proceeds remaining after selling expenses and deduction of any preferences or profits interests payable to Masterworks.

We believe the characteristics of Post War & Contemporary Art present an attractive investment case as a potential risk diversifier. The following are our general observations about the Post-War & Contemporary Art category as an investment asset:

| ● | Sizable Asset Class. Since 2014, total estimated annual art sales have ranged from $50.1 billion to $68.2 billion, with Post-War & Contemporary representing the largest category. | |

| ● | Favorable Historical Price Trends. Price appreciation at an estimated annualized rate of 11.2% from 1995 through 2024, versus 10.1% for the S&P 500 Index (includes dividends reinvested) for the same period. | |

| ● | Low Correlation to Other Investment Assets. Correlation factor of (0.09) between Post-War & Contemporary Art and the S&P 500 Index based on annual price performance from 1995 through 2024. | |

| ● | Market Resilience. The Post-War & Contemporary segment has been resilient through periods of financial distress (e.g., 2001-2002, 2008-2009, 2020). |

The Art Market

The global art market consists of a large global network of auction houses, dealers, galleries, advisors, agents, individual collectors, museums, public institutions, and various experts and service providers engaged in the purchase and sale of unique and collectible works of art. Post-War and Contemporary art represents the largest segment of the fine art auction market, accounting for approximately 54% of the market by volume. In general, the global art market is influenced by the overall strength and stability of the global economy, geopolitical conditions, capital markets and world events, all of which may affect the willingness of potential buyers and sellers to purchase and sell art.

The public auction market, which is dominated by Christies and Sotheby’s, makes up slightly less than half of overall global transaction volume and is the source of virtually all publicly available art market data. A majority of art sales occur in privately negotiated transactions, which are arranged and executed through galleries and other intermediaries on behalf of collectors who often remain anonymous. Private art sales are typically subject to stringent confidentiality provisions, which makes it extremely difficult to discern transaction volume and trends in the private market, though market participants with transactional scale have clear informational advantages.

| 1 |

Management Services

Management services are provided pursuant to a management services agreement between us and Masterworks and incorporates a “unitary” expense and fee structure, which means that the Administrator will pay all of our ordinary ongoing operating costs and expenses and manage all management all of our activities, including, but not limited to, state and federal securities law filings, regulatory compliance, accounting, audit, tax, transfer agency services, governance, art market research, investor relations, artwork storage, appraisals and valuations, insurance, display, shipping and inspection. For these services and costs, the Administrator earns preferred equity interests at a rate of 1.5% of the total Class A shares outstanding per annum. Any extraordinary or non-routine services and costs (if any) are also managed and paid by the Administrator and any extraordinary or non-routine costs will be reimbursed upon the sale of an Artwork of a series or a sale of the Company, as applicable.

Acquisitions and Sales of Artwork

Artwork is sourced through Masterworks’ dedicated acquisitions team, composed of individuals with significant transactional experience in the art market. This team, which is supported by Masterworks research function, appraisals team, and an extensive art market database, coordinates with an extensive global network of collectors and intermediaries to source high value artwork while maintaining price discipline based on proprietary analytics and research. In contrast to many other art market participants, we seek to acquire Artwork solely for its investment characteristics and we maintain a disciplined approach to pricing. If Masterworks and an artwork seller reach an agreement on a transaction, the acquisitions team conducts further due diligence to verify the condition and provenance of the Artwork, including performing a physical inspection of the object by a qualified Masterworks employee or an independent agent and performing a “know-you-customer” review of the artwork seller. Artwork we acquire for each series offering will be described in the section of this offering circular entitled “Description of Business - The Series.” Our acquisition of title to Artwork for each series will occur contemporaneously with or before the initial closing of the applicable series offering.

Masterworks has established a track record of sales that leverages its global network of collectors and institutions, as well its dedicated art sales team and gallery operations. As one of the largest participants in the global art market, opportunities for transactions are available through all possible sales channels. We may decide to sell the Artwork of a series at any time and in any manner in the sole discretion of our Board. We determine to sell Artwork based on a number of factors, including our perception of the fair value of the Artwork relative to its proposed selling price, our perspective on the current state and future direction of the applicable artist market and the art market more generally, the absolute net returns we can deliver to shareholders, the length of our holding period and other factors. Although we expect our holding period will typically be for three- to ten-years, our holding period is indefinite, although we may sell the Artwork of a series at any time due to market conditions and other factors. Prior to a sale of the Artwork of a series, investors in such series may seek to sell their shares through the secondary market. We may pay reasonable fees or commissions to art intermediaries in connection with the sale of artwork, including to affiliates of Masterworks, provided that any such amounts paid to affiliates of Masterworks shall be equal to or below the fees or commissions charged by unaffiliated third parties for similar services.

| 2 |

Organizational and Capital Structure

The Masterworks organizational and capital structure were developed to manage risks, align incentives, optimize tax efficiencies and safeguard investor interests. By leveraging this structure, we can provide a full-service platform that provides transparency and minimizes fees while providing meaningful protections such as:

| ● | Assets of each series are fully protected from the liabilities of other series; | |

| ● | Masterworks does not co-mingle capital between series or with its own funds; | |

| ● | Class A shares can be traded on an alternative trading platform; | |

| ● | Investors avoid double taxation that would result from a simpler structure; and | |

| ● | Investors in each series may be insulated from certain platform-level risks. |

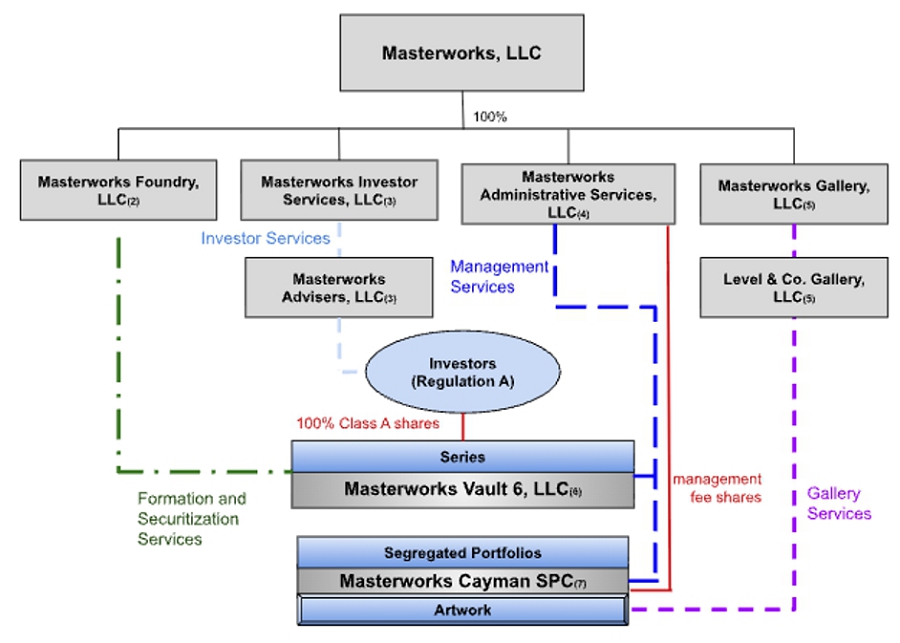

The following diagram reflects Masterworks organizational structure and the material commercial relationships between us and Masterworks that will exist following a series offering:

*All entities are Delaware limited liability companies, except the Company, which is a Delaware series limited liability company and Masterworks Cayman, SPC, which is a Cayman Islands segregated portfolio company.

| (1) | “Masterworks” refers to the Masterworks parent company which owns the Masterworks Platform. Scott W. Lynn, the founder and Chief Executive Officer of Masterworks, LLC, has effective control over Masterworks. |

| (2) | “Masterworks Foundry” forms Masterworks issuer entities, including the Company, and performs services relating to the formation of series and the securitization of Artwork for each series. Masterworks Foundry owns 100% of the membership interests, represented by Class B shares, of each series prior to giving effect to the series offerings. Masterworks Foundry may also advance us funds to acquire Artwork, though it has no obligation to do so. |

| (3) | “Masterworks Investor Services” conducts investor relations services and pays all fees and expenses of any registered investment adviser dedicated to advising with respect to Masterworks financial products. Masterworks Advisers, LLC is registered with the SEC as an investment adviser and investment advisor representatives of Masterworks Advisers, LLC provide advisory services in connection with offerings sponsored by Masterworks, including the series offerings. See the section entitled “Advisory Services” of this offering circular for additional information. |

| (4) | “Masterworks Administrative Services” or the “Administrator” will operate the Masterworks Platform and will perform administrative and management services for us pursuant to the management services agreement. |

| (5) | “Masterworks Gallery” and its subsidiaries perform gallery services, including Artwork acquisitions, sales and museum loans. Masterworks Gallery and its subsidiaries act as agents for each series of the Company in connection with Artwork transactions and provide financial guarantees to counterparties. |

| (6) | The Company intends to facilitate investment in Artwork by creating separate series, each of which will issue Class A shares in a series offering to facilitate investment in a single Artwork. |

| (7) | Masterworks Cayman, SPC is a Cayman Islands segregated portfolio company (“Masterworks Cayman”). The Artwork beneficially owned by each series will be the only asset of a segregated portfolio of Masterworks Cayman. A segregated portfolio company registered under the Cayman Islands Companies Law is a single legal entity which may establish internal segregated portfolios. Each portfolio’s assets and liabilities are legally separated from the assets and liabilities of the Masterworks Cayman ordinary account and are also separate from assets and liabilities attributed to Masterworks Cayman’s other segregated portfolios. This means that a creditor of Masterworks Cayman will only be entitled to recover against assets attributed and credited to the specific segregated portfolio to which the contract is also attributed. The segregated portfolios of Masterworks Cayman holding title to the Artwork of each series do not intend to enter into any contracts or incur any liabilities, except for the management services agreement and as may be necessary in connection with a sale of Artworks. |

| 3 |

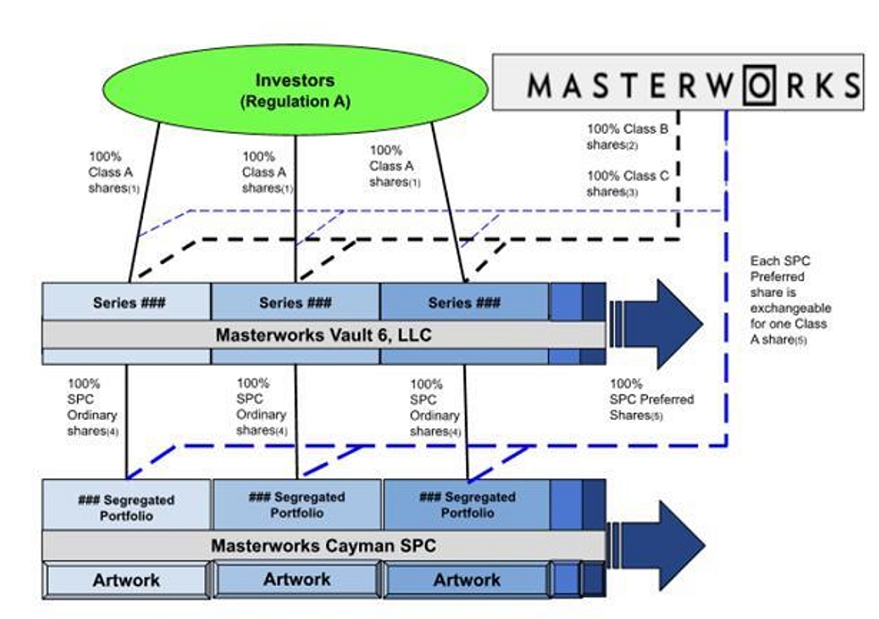

The following diagram reflects the capital structure that will exist following a series offering:

| (1) | Each series will issue Class A shares representing ordinary membership interests in such series upon each closing of the series offering. Immediately following the consummation of the series offering, investors participating in such series offering will own 100% of the outstanding Class A shares issued by such series. |

| (2) | Upon formation of a series, Masterworks will be issued 1,000 Class B shares, which represent the right to receive 20% of the positive difference, if any, between the amount available for distribution to Class A shareholders in connection with a liquidation after a sale of the Artwork and $20.00. Class B shares can be converted into Class A shares based on the relative fair market values of the Class B shares and the Class A shares. Masterworks has also agreed to lock-up provisions in our operating agreement, that will prohibit it from selling any Class B shares prior to the one-year anniversary of the relevant offering, though it is permitted to pledge all of its shares to unaffiliated third-party lenders and such lenders shall not be subject to the lock-up if they obtain ownership of the profits interest in connection with a default by Masterworks on its indebtedness. |

| (3) | Class C shares have no economic or voting rights, other than so-called “kick-out” rights, meaning the holder has the right to remove, replace or reconstitute the Company’s Board of Managers. The Class C shares can only be issued to, transferred to, or, held by, a Masterworks affiliate and there can only be one holder of Class C shares of all series of the Company at any point in time. |

| (4) | When a segregated portfolio of Masterworks Cayman acquires title to an Artwork, the segregated portfolio will issue the applicable series the same number of SPC Ordinary shares in the segregated portfolio as the number of Class A shares offered to investors in the series offering, and such SPC Ordinary shares shall initially represent 100% of the outstanding equity interests in such segregated portfolio. In the event any additional Class A shares are issued following the closing of a series offering upon a conversion of Class B shares or exchange of SPC Preferred shares, additional SPC Ordinary shares will be issued to the applicable series, such that at all relevant times the number of outstanding SPC Ordinary shares held by a series shall equal the number of outstanding Class A shares for such series. |

| (5) | Masterworks will earn SPC preferred shares of each applicable segregated portfolio pursuant to the management services agreement at a rate of 1.5% of the total SPC Shares (i.e. SPC Ordinary shares and SPC Preferred shares) offered, after giving effect to such issuance, per annum, commencing on the earliest closing date on which the applicable series offering is fully subscribed and at least 95% of the subscription proceeds for such offering have been received by the Company. There is no overall limit to the number of SPC Preferred shares that may be issued to pay these fees. SPC Preferred shares have no voting rights, but have a $20.00 per share liquidation preference over SPC Ordinary shares which are held by each series. This preference means that Masterworks management fees will be paid in priority to any payments made to Class A shareholders. Once earned, SPC Preferred shares can be exchanged for Class A shares of the applicable series. |

| 4 |

The following table further describes the economic rights of each share class of a series and segregated portfolio company following the completion of each series offering:

| Share Class | Summary of Economic Rights |

| Series of the Company | ||||

| Class A shares | ● | 100% of members’ capital. | ||

| ● | 80% of net profits, after deduction of all management fees and other expenses. | |||

| Class B shares | ● | 0% of members’ capital. | ||

| ● | 20% of net profits, after deduction of all management fees and other expenses. |

| Class C share | None. |

| Cayman Segregated Portfolio | ||||

| SPC Ordinary shares | ● | 100% economic interest in the segregated portfolio, after deduction of preference amounts payable in respect of the SPC Preferred shares, if any. | ||

| SPC Preferred shares | ● | $20.00 per share liquidation preference over SPC Ordinary shares. | ||

| ● | Exchangeable into Class A shares of the series of which the segregated portfolio holds the Artwork at an exchange rate of 1 for 1. | |||

| ● | If there is a sale of Artwork resulting in a net loss (i.e. holders of Class A shares in a series on a fully-diluted basis would receive a liquidating distribution of less than $20 per Class A share), Masterworks, as the holder of the SPC Preferred shares, would effectively receive up to $20 per SPC Preferred share in preference to any distribution made to Class A shareholders. If the Artwork sale results in a net profit (i.e. holders of Class A shares in a series on a fully-diluted basis would receive a liquidating distribution of more than $20 per Class A share), Masterworks would convert its SPC Preferred shares into Class A shares prior to the liquidating distribution and would receive the same economics per Class A share as other Class A shareholders. | |||

Summary of Risks

An investment in the Class A shares of any series includes a number of risks and uncertainties which are described in the “Risk Factors” section of this offering circular, including the following:

| ● | Risks Related to Our Business Model. The timing and outcome of any Artwork sale cannot be guaranteed, and will depend on a number of external factors, including market demand, the artist’s market trajectory and broader economic conditions. Our business is highly dependent on conditions prevailing in the art market and the market for specific artists and therefore our ability to execute a profitable sale will hinge, to a large extent, on factors that are beyond our control. |

| ● | Risks Associated with an Investment in Art. Artwork may decline in value or may not appreciate sufficiently to exceed carrying costs, including management fees. Artists often go through periods of rising and shrinking popularity, which can result in material changes in the value and marketability of their work. There are a variety of other risks to art investing, including, without limitation, the risk of claims that the artwork is not authentic, physical damage and market risks for any particular artist or work. |

| ● | Risks Relating to Our Relationship with Masterworks and Conflicts of Interest. We are totally reliant on Masterworks to administer our Company and the Artwork held by each series. If Masterworks were to cease operations for any reason we would likely be required to sell the Artwork of each series and dissolve the Company. In addition, Masterworks may have economic interests that diverge from your interests. Masterworks compensates investment advisory representatives to provide investment advice to persons interested in investing in the series offerings and therefore such representatives have inherent conflicts of interest. In addition, Masterworks will perform internal appraisals of the fair market value of each Artwork and such appraisals may not reflect the same values as appraisals performed by an independent third party. Also, Masterworks has significant discretion to sell Artwork and Masterworks may have economic interests that differ from those of Class A shareholders, a majority of our Board of Managers are Masterworks officers and Masterworks has the right to remove and replace our Board of Managers. Conflicts of interest may not be resolved in favor of our Class A shareholders. |

| ● | Risks Related to Illiquidity. Artwork and an investment in the Class A shares are inherently illiquid. Unlike publicly traded securities, there is no active daily market, and it may take time to identify a suitable buyer or favorable market conditions for sale. As such, Masterworks is not obligated to sell any Artwork on a set timeline, and investors should be prepared to hold their shares for an extended period. While we intend to facilitate secondary sales of Class A shares on an alternative trading system, or “ATS”, such system has limitations, including restricted availability in certain jurisdictions, an absence of market-makers, limited trading volume and uncertain pricing dynamics. For these reasons, attempting to sell shares on the ATS may not result in a sale or may result in a sale below the net asset value, or “NAV”, of the Class A shares. Investors must be prepared to hold their investment for an extended and indefinite period of time. An investment in Class A shares is not appropriate for investors who may need a liquidity event in a prescribed time frame. |

| 5 |

| Securities being Offered: |

We are offering the maximum number of Class A shares of each series referenced in the “Series Offering Table.”

The Class A shares of each series will be non-voting except in limited circumstances with respect to certain matters set forth in our operating agreement, including to remove and replace the Administrator, to remove a member of the Board of Managers for “cause” and to approve certain acts as described in our operating agreement, including certain proposed amendments to the operating agreement or the management services agreement. See “Description of Shares - Summary of Operating Agreement” for more information on voting rights. The purchase of Class A shares in a particular series is an investment only in that series and not an investment in the Company as a whole or Masterworks. |

|

| Offering Price per Class A Share of a series: | $20.00. | |

| Number of Shares Outstanding Before the Offering | Prior to giving effect to each series offering, 100% of the membership interests of each series are held by Masterworks in the form of 1,000 Class B shares of such series. | |

| Shares Outstanding After the Series Offerings: | ||

|

Class A shares

|

Each series shall have Class A shares issued and outstanding immediately following a series offering equal to the number of Class A shares offered which will be set forth in the “Series Offering Table” section in the forepart of this Offering Circular. |

|

|

Class B shares |

Each series shall have 1,000 Class B shares issued and outstanding. |

|

|

Class C share

|

Each series shall have one Class C share issued and outstanding entitling a Masterworks affiliate to effectively control the company by granting it the right to remove and replace members of the Board of Managers. |

|

|

SPC Ordinary shares

|

Immediately following the series offering, the applicable series will own 100% of the equity interests of the segregated portfolio of Masterworks Cayman that holds title to the Artwork and at all relevant times the number of outstanding SPC Ordinary shares held by a series equals the number of outstanding Class A shares for such series. |

|

|

SPC Preferred shares

|

Following the series offering, Masterworks will earn SPC Preferred shares pursuant to the management services agreement in the applicable segregated portfolio of Masterworks Cayman at the rate of 1.5% per annum in respect of management and administrative services and costs. These issuances will be dilutive to Class A shareholders, which means the beneficial ownership percentage of the Artwork represented by the Class A shares will decline by 1.5% per annum following the series offering. |

|

| Minimum and Maximum Investment Amount | The maximum investment amount per investor in any series is $250,000 (12,500 Class A shares) and the minimum investment amount per investor in any series is $15,000 (750 Class A shares) for investors that have not invested in offerings via the Masterworks Platform and $500 (25 Class A shares) for investors that have invested in other offerings on the Masterworks Platform . We reserve the right to reject any subscription, waive or increase the maximum purchase restriction or waive or decrease the minimum purchase restriction in our sole and absolute discretion and we routinely grant such waivers, increases or reductions for categories of investors or on a case-by-case basis. Accordingly, investors should not assume that the stated minimum investment restriction will be applied uniformly to all investors. Subscriptions, once received, are irrevocable by the investors. Further, pursuant to the terms of the Company’s operating agreement, an investor, other than an affiliate of Masterworks, generally cannot own, or be deemed to beneficially own, as “beneficial ownership” is determined pursuant to Section 13(d) and 13(g) of the Securities Act, more than 24.99% of the total number of Class A shares of a series outstanding, provided that we may waive such limit on a case-by-case basis in our sole discretion. | |

| Subscribing Online | Investors can subscribe for Class A shares via the Masterworks Platform located at https://www.masterworks.com/, as well as browse and screen potential artwork investments, view details of an investment and sign contractual documents online. For additional information, see “Plan of Distribution – Procedures for Subscribing.” | |

| Investment Amount Restrictions | To invest in any series offering, you must represent to us that the aggregate purchase price you pay for your investment is not more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, you are encouraged to review Rule 251(d)(2)(i)(c) of Regulation A. For general information on investing, you are encouraged to refer to www.investor.gov. |

| 6 |

| Use of Proceeds | Masterworks will pay all expenses of each series offering and therefore the gross proceeds from each series offering will equal the net proceeds. The net proceeds will be used to acquire the Artwork and to pay Masterworks the Expense Allocation as described in the section entitled “Management Compensation.” |

| Offering Period | The series offerings are being conducted as a continuous offering pursuant to Rule 251(d)(3) of Regulation A, meaning that while the offering of a particular series is continuous, active sales of series interests may take place sporadically over the term of the series offering.

There will be a separate closing, or closings, with respect to each series offering. An initial closing and each subsequent closing of a series offering will take place on the date subscriptions for the maximum number of series Class A shares have been accepted or an earlier date or dates determined by us in our sole discretion. The offering period for any series will not exceed 24 months from the qualification date of the offering statement that includes such series. We reserve the right to terminate a series offering for any reason at any time prior to the initial closing of such series offering. | |

| Closings | The Company may close an entire series offering at one time or may have multiple closings. Throughout this Offering Circular, we have assumed multiple closings and refer to the “initial closing” as the first such closing and the “final closing” as the last such closing. The Artwork held by a series will be acquired by the Company on or prior to the initial closing of the respective series offering. Subscriptions will be accepted on a rolling basis. | |

| Termination of a Series Offering | We reserve the right to terminate any series offering for any reason at any time prior to the initial closing. |

| Transfer Restrictions | The Class A shares of a series may only be transferred by operation of law or with the consent of the Company: |

| ● | To an immediate family member or an affiliate of the owner of the Class A shares of a series, | |

| ● | To a trust or other entity for estate or tax planning purposes, | |

| ● | As a charitable gift, | |

| ● | On a trading platform approved by Masterworks, such as the ATS, or | |

| ● | In a transaction otherwise approved by Masterworks. |

Transfer Agent and Registrar |

The transfer agent and registrar for the Class A shares of any series is Equity Stock Transfer, LLC. The transfer agent’s address is 237 West 37th Street, Suite 602, New York, New York 10018. The transfer agent’s telephone number is (212) 575-5757. We can remove the transfer agent at any time and in the absence of a replacement transfer agent, the Company will maintain the share register. | |

| NAV Reporting | Masterworks performs appraisals at the end of each calendar quarter and provides Class A shareholders with quarterly estimates of the net asset value, or “NAV” of their Class A shares. NAV is determined by performing a fair value appraisal of the Artwork and dividing the appraised value by the fully diluted Class A shares outstanding, with appropriate reductions for Class B profit share interests and liquidation preferences, as applicable. NAV per Class A share represents Masterworks’ best estimate of the then current fair value of the Artwork represented by a Class A share. Such value would only be recognized upon a sale of the Artwork and NAV is not reflective of the value that a shareholder might receive for a Class A share traded on the ATS. The Class A shares are highly illiquid and therefore they may trade at a significant discount to NAV.

| |

| SEC Reporting | The Company intends to continue to file reports with the SEC pursuant to Regulation A for the foreseeable future. These reports include annual reports on Form 1-K, which include audited financial statements, semiannual reports on Form 1-S/A which include unaudited interim financial statements and special reports on Form 1-U, which are filed periodically and include other material information.

| |

| Tax Matters | For U.S. federal income tax purposes, we expect that each series will be treated as a separate partnership. As a result, any taxable gains or losses from that series, such as from the sale of the Artwork, will flow through to you directly and be reported on a Schedule K-1. This structure allows tax items to pass through without double taxation at the entity level. For more information, see the section entitled MATERIAL U.S. FEDERAL TAX CONSIDERATIONS. We recommend consulting your tax advisor for details based on your personal tax situation. Masterworks will provide all necessary tax documents annually. |

Series

Company Information

We are a manager-managed series limited liability company, managed by the Board of Managers. Our principal office is located at 1 World Trade Center, 57th Floor, New York, New York 10007 and our phone number is (203) 518-5172. Our corporate website address is the website address of Masterworks at www.masterworks.com. Information contained on, or accessible through, the website is not a part of, and is not incorporated by reference into, this offering circular.

DETERMINATION OF OFFERING PRICE

The aggregate offering size of a series equals the sum of (a) the estimated purchase price that Masterworks anticipates paying for the Artwork plus (b) approximately 11% of such amount (approximately 10% of the maximum aggregate offering amount), as an upfront payment, or “Expense Allocation” payable to Masterworks. The initial offering price of $20.00 per Class A share of each series was arbitrarily determined by Masterworks.

We believe that based on the arms-length ultimate purchase price of each Artwork of a series, historical appreciation rates of similar artworks by the same artist of such Artwork and other factors, the per share offering price of each series will constitute a reasonable estimate at or below the fair value of the Class A shares of such series as of the date such series is added to the Offering Circular.

| 7 |

We do not anticipate making distributions in the foreseeable future on any Class A shares, unless and until the Artwork held by such series is sold, at which point we will pay any expenses for which we are responsible and make a distribution to the holders of the Class A shares of such series in accordance with our operating agreement. There can be no assurance as to the timing of a distribution or that we will pay a distribution at all. There are no contractual restrictions on the ability of a series to make distributions.

The purchase of the Class A shares of a series offered hereby involves risk. Each prospective investor should consult his, her or its own counsel, accountant and other advisors as to legal, tax, business, financial and related aspects of an investment in the securities offered hereby. Prospective investors should carefully consider the following specific risk factors, in addition to the other information set forth in this offering circular, before purchasing Class A shares.

Risks Related to our Business Model

Whether or not we will deliver capital appreciation to investors is largely dependent on the art market, which we cannot control.

We cannot make any assurance that our business model will be successful. Our operations will be dedicated to acquiring and maintaining Artworks held by our series and facilitating the ultimate sale of Artworks. The ability of any series to deliver capital appreciation will depend to a large extent on economic conditions, the art market in general and the market for works produced by the specific artist, which are factors that are beyond our control. Aggregate returns realized by investors are expected to correlate to the change in value of the Artwork of a series, which may not correlate to changes in the overall art market or any segment of the art market. The value of an Artwork may decline over time or may not appreciate sufficiently to cover expenses, either of which would have a direct adverse effect on the value of the Class A shares.

Each series will hold an interest in a single Artwork, a non-diversified investment.

Each series will own a single Artwork and not invest in any other artwork or assets or conduct any other operations that could generate income. This structure allows investors to target exposure to specific artists or artworks but also introduces concentration risk. An investment in the Class A shares of a single series may be riskier than an investment in a diversified pool of assets or multiple series. However, because multiple offerings are available on the Masterworks Platform, investors have the opportunity to build diversified exposure across different artists, price points and market dynamics over time. In addition, because each series holds a single Artwork and does not generate cash flow, investors will only realize a return if the Artwork is ultimately sold for a price that exceeds its acquisition cost and all associated costs, fees and expenses. Distributions to Class A shareholders will only occur if sufficient net proceeds are available following such a sale.

| 8 |

Artwork may be sold at a loss or at a price that results in a distribution that is below the purchase price of the Class A shares.

Any sale of Artwork may be subject to market timing, economic conditions or other circumstances that would result in a distribution of cash that is less than the price paid by investors to purchase the Class A shares of the applicable series. While we aim to sell Artwork opportunistically based on favorable market conditions, we may sell earlier or at a loss if doing so aligns with our fiduciary duty to protect shareholder value, or if external events, such as legal, regulatory, or platform-level developments, necessitate an earlier sale. Additionally, there is no guarantee that the Class A shares of any series can be resold at a specific price, or that the Artwork of a series will be sold at a time or price that results in a distribution of more than $20.00 per share.

There can be no assurance that the Class A shares of such series can ever be resold or that the Artwork of a series can ever be sold or that any sale would occur at a price that would result in a distribution of more than $20.00 per Class A share of a series.

The timing and potential price of a sale of Artwork are inherently uncertain, so investors should be prepared to hold their Class A shares for an extended or even indefinite period.

While we aim to pursue liquidity events that maximize value, the art market is non-linear and sale timing is subject to external market dynamics, artist-specific factors and buyer readiness. Masterworks maintains an active network of institutional and ultra-high-net-worth collectors, dealers, and platforms, including a private sales channel operated by Masterworks, through which we may evaluate potential opportunities for sale. We intend to hold Artwork for an indefinite period, although the Artwork will be perpetually available for sale following the series offering and we will evaluate any reasonable third party offers to acquire the Artwork of such series. Accordingly, a risk of investing in the Class A shares is the unpredictability of the timing of a sale of the Artwork and the unpredictability of funds being available for cash distribution and investors should be prepared for both the possibility that they will not receive a cash distribution for many years, if ever, and the contrary possibility that they may receive a cash distribution at any time following the completion of the series offering. An investment in Class A shares is unsuitable for investors that are not prepared to hold their Class A shares for an indefinite period of time, as there can be no assurance that the Class A shares can ever be resold or that the Artwork can be sold within any specific timeframe or at all.

Art investment involves carrying costs and our securitization of artwork adds additional costs for which Masterworks is compensated and reimbursed through the issuance of equity which will have a dilutive effect on Class A shareholders.

Pursuant to a management services agreement among us, Masterworks Cayman and the Administrator to be entered into prior to the initial closing of the initial series offerings, the Administrator will manage all entity-level and asset management services relating to our business and the maintenance of the Artwork of each series. The Administrator will pay all ordinary and necessary costs and expenses associated with the administration of our business and maintenance of the Artwork of each series. In exchange for these services and incurring these costs and expenses, the Administrator will receive equity interests that effectively dilute Class A shareholders at a rate of 1.5% per annum. These equity interests also have a $20.00 per share liquidation preference, which means Masterworks’ management fees will be paid at the same value ascribed to Class A shares in this offering in priority to distributions to Class A shareholders. These equity interests issued to Masterworks will continue indefinitely for as long as the Artwork is managed by Masterworks.

| 9 |

Risks Associated with an Investment in the Artwork

There is no assurance of appreciation of the Artwork of a series or sufficient cash distributions resulting from the ultimate sale of the Artwork of a series.

While we acquire Artwork through a deliberate and research-driven process, there is no guarantee that a specific artwork will appreciate, maintain its present value or be sold at a profit. The art market is affected by many external variables, including macroeconomic conditions, changing collector preferences, and artist-specific developments, all of which may impact the resale market.

Masterworks mitigates some of these uncertainties through scale and specialization. We maintain one of the most active acquisitions teams in the Post-War and Contemporary art market and regularly engage with auction houses, galleries, and institutional buyers to evaluate sale opportunities. Despite this infrastructure, investments in artwork remain illiquid, and there may be periods in which no ready market exists for resale.

Even in cases where appreciation occurs, the realized return will be reduced by management costs and expenses. Investors should therefore view investments in Class A shares as long-term, illiquid, and subject to a wide range of market outcomes.

Valuation of artwork by artists that have fewer auction sales is more difficult than artists with larger auction markets

Certain artists such as Andy Warhol and Pablo Picasso have a relatively large global collector base and a well-established track record of auction sales over a lengthy period. These artists were also extremely prolific during their careers, so their artwork is frequently bought and sold at auction. This relatively large volume of data makes estimates of historical pricing trends and fair value ranges for artwork produced by these artists more reliable. By contrast, valuation of works by other artists who have a smaller collector base and or a shorter track record of auction sales is comparatively more difficult and such assessments are generally prone to wider margins of error. When assessing the historical auction performance of artwork by a particular artist, investors are urged to consider the volume of public auction data available. As a general matter, historical pricing trends and fair value estimates are more likely to be more meaningful and predictive for artists with higher volumes of prior auction sales than pricing trends and estimates for artists that have fewer historical auction sales. Accordingly, there is a higher risk that we may overpay for, or misprice, artwork by artists with fewer auction sales than those with higher volumes of prior auction sales.

| 10 |

Our appraisal of the fair value of Artwork and determination of estimated net asset value, or NAV, per share may not be reflective of the realizable value of the Class A shares.

We, together with Masterworks, will estimate the fair value of Artwork on a quarterly basis, including for purposes of preparing our annual and semi-annual financial statements in accordance with generally accepted accounting principles in the United States and reporting the estimated NAV per share to Class A shareholders. For the reasons set forth elsewhere in this “Risk Factors” section, any such appraisal is inherently subjective and may not represent the actual realizable value of the Artwork. In addition, the estimated NAV per share may have little or no correlation with the value a Class A shareholder would receive in a sale of Class A shares on the automated trading system, or ATS. The ATS is a highly illiquid market with no market-makers and, as such, offers very limited price discovery. In addition, NAV per share is an estimate of the amount a holder of a Class A share would receive in a liquidating distribution if the Artwork were sold at such time, but this amount is not the same as the fair market value of the Class A shares. Unless a liquidation happens to be occurring at the time NAV is published, the “fair market value” of the Class A shares represents not just the fractional beneficial ownership of the Artwork, but also the other attributes of ownership of a security, such as the economic aspects of the ongoing management services agreement, as well as each series tax and governance structure, coupled with subjective expectations about the future direction of the artist’s market, which will influence the future value of the Artwork and the timing of a sale of the Artwork, which are unknown.

Our appraisal of the fair market value of an Artwork may differ from the appraisal that would be issued by an independent third-party and you are cautioned not to place undue reliance on any appraisal or estimated NAV per share issued by Masterworks.

Masterworks performs appraisals of artwork in conformity with the 2024-2025 Uniform Standards of Professional Appraisal Practice (USPAP) developed by the Appraisal Standards Board of the Appraisal Foundation, although conflicts of interest may call into question standards related to appraiser independence. Appraisals are performed by employees of the Administrator and, therefore, Masterworks has conflicts of interest in performing appraisals. For example, Masterworks sells its management fee shares at prices that are determined based on the appraised value of the underlying artwork. Masterworks has implemented policies designed to mitigate conflicts, such as requiring that all draft appraisals are reviewed for reasonableness prior to finalization by an unaffiliated third-party appraiser, however we cannot provide assurance that our policies are adequate or that our appraisal of the fair market value of an Artwork would not differ from the appraisal that would be issued by an independent third party and you are cautioned not to place undue reliance on any appraisal or the estimated NAV per share issued by Masterworks.

Calculation of the Masterworks Artist Market Index includes a degree of subjectivity, which inherently makes it less precise and less reliable than a purely mathematical metric.

The Masterworks Artist Market Index metric seeks to determine how an overall artist market has performed historically and relies in part on categorizing various unique artworks produced by an artist based on quality assessments made by members of the Masterworks appraisals team. Quality, as used in this context, refers to the unique attributes and characteristics of an artwork that make it more or less valuable in the market, such as image, size, creation year, subject matter, coloration and historical sale data. Although some of these factors are objective in nature, the ultimate assessment of how the combination of such factors affect the quality and value of an artwork is subjective. Accordingly, there is a degree of subjectivity employed in the calculation of the Masterworks Artist Market Index, which means that if different people were involved in the categorization process they might have different opinions which would lead to different resulting calculations. In addition, as the Masterworks Artist Market Index is a customized mathematical model with no singular or universally accepted method of computation, there were subjective decisions made by the Masterworks research team in developing the model and categorizing the relevant data. These subjective aspects of the Masterworks Artist Market Index inherently make it prone to variability and may make it less reliable than other metrics that are purely mathematical.

In addition, the art professionals making subjective determinations that impact the calculation of the Masterworks Artist Market Index are employees of Masterworks and therefore may have potential conflicts of interest. We do not believe that these art professionals would have a basis to know how their categorization decisions would impact the overall mathematical calculation of the Masterworks Artist Market Index, though we cannot guarantee that their decisions are free from bias or that the categorization decisions would not be different if they were conducted by unaffiliated third parties.

The Masterworks Artist Market Index also leverages the use of machine learning technology for predictive rankings of subject artworks by quality features which, although reviewed by the Masterworks appraisals team for accuracy, may have potential for error or inaccuracies. While the Masterworks Artist Market Index reflects our best available tool to assess an artist’s overall historical auction market performance, you should not place undue reliance on the Masterworks Artist Market Index and it should not be viewed in isolation or as a substitute for the other important information included in this Offering Circular.

| 11 |

An investment in Artwork is subject to various risks, any of which could materially affect the value of the Artwork and the market value of the Class A shares.

Although Masterworks conducts due diligence prior to acquisition and seeks to mitigate the following risks through its sourcing process, no amount of diligence can eliminate them entirely. The most material risks include:

| ● | Authenticity. Claims with respect to the authenticity of a work may result from incorrect attribution, uncertain attribution, lack of certification proving the authenticity of the artwork, forgery of a work of art, or falsification of the artist’s signature. We generally obtain representations of authenticity from sellers, but these representations may not effectively eliminate the risk. | |

| ● | Provenance. The ownership history of a work, or “provenance,” may be disputed or incomplete. Claims can arise around gaps in the chain of title, contested prior ownership, or historical events such as wartime looting. Additionally, frequent changes in ownership, including resale by Masterworks, may impact buyer perception and, therefore, market value. | |

| ● | Condition. The physical condition of an artwork over time is dependent on technical aspects of artistic workmanship, including the materials used, the manner and skill of application, handling and storage and other factors. | |

| ● | Physical Risks. Artwork is subject to potential damage, destruction, devastation, vandalism or loss as a result of natural disasters (flood, fire, hurricane), crime, theft, illegal exportation abroad, etc. | |

| ● | Legal and Title Risks. Artwork ownership is prone to a variety of legal challenges, including challenges to title, nationalization, purchase of work of art from an unauthorized person, risk of cheating, money laundering, violation of legal regulations and restitution issues. Purchasing from major auction houses and reputable galleries can reduce, but not eliminate, these risks. | |

| ● | Market Risks. The art market is prone to change due to a variety of factors, including changes in transaction costs, substantial changes in fees, tax law changes, export licenses etc., changes in legal regulations, changes in attitudes toward art as an investment, changes in tastes, trends (fashion) and changes in supply, such as the liquidation of a major collection. These risks can be specific to certain geographies. | |

| ● | Economic Risks. Art values and demand are affected by economic confidence among ultra-high-net-worth individuals. | |

| ● | Informational Risk. The art market is unregulated, opaque and available information is often limited to transactions that occur in public auctions, which excludes private transactions that represent a majority of the overall market. |

| 12 |

If any of these risks materialize, the value of the Artwork of such series may decline, and the value of the Class A shares of such series would be adversely affected.

We may not be able to find a buyer for the Artwork at an attractive price.

Art is a highly illiquid asset and a meaningful percentage of works offered at public auction may fail to sell, particularly if reserve prices are not met or if market conditions are unfavorable. While we intend to pursue strategic sale opportunities through private channels or auctions, there is no guarantee that a buyer will be available or willing to pay at any reasonable price.

We continuously monitor market signals, artist momentum and buyer interest to position each Artwork for potential sale. Even in the event that we attempt to sell the Artwork of a series, we cannot guarantee that there will be a buyer at any reasonable price.