Post-Qualification Offering Circular Amendment No. 4

SEC File No. 024-12060

POST EFFECTIVE AMENDMENT NO. 4

OFFERING CIRCULAR DATED May 15, 2025

WATER ON DEMAND, INC.

13575 58th Street North, Suite 200

Clearwater, FL 33760

https://www.waterondemand.net/

UNITS CONSISTING OF ONE SHARE OF COMMON STOCK AND TWO WARRANTS

MINIMUM INDIVIDUAL INVESTMENT: 200 UNITS ($ 500)

SEE “SECURITIES BEING OFFERED” AT PAGE 37

This Post-Qualification Offering Circular Amendment No. 4 amends the Offering Circular of Water On Demand, Inc., a Texas corporation (the “Company”), dated February 15, 2024, as qualified on February 17, 2024, as amended and as may be amended and supplemented from time to time, to: (a) extend the expiration date of this offering to May 15, 2026; and (b) revise the offered securities to 9,500,000 Units (consisting of one share of common stock and two warrants to purchase common stock) at $2.50 per Unit and 19,000,000 common shares upon the exercise of the warrants (collectively, the “Offered Securities”); (c) to add up to 950,000 bonus shares of common stock offered to certain purchasers and (d) to remove Castle Placement LLC as the placement agent with respect to the offering.

By this Offering Circular, the Company is offering for sale a maximum of 9,500,000 Units, which Units consist of one share of common stock and two warrants to purchase common stock (the “Offered Securities”), of which 4,400 shares have been sold for cash in the total amount of $11,000 at a fixed price of $2.50 per share, pursuant to Tier 2 of Regulation A of the United States Securities and Exchange Commission (the “SEC”). In addition, the Company is offering certain purchasers of the Units bonus shares (“Bonus Shares”) equal to ten percent (10%) pursuant to the bonus program (“Bonus Program”) based upon investment level. The maximum number of Bonus Shares issuable is 950,000. Investors participating in the Bonus Program may receive an effective discount of up to $0.25 per share or 10%.

A minimum purchase of $500 of the Offered Securities is required in this offering ($150 for subscription based). This offering is being conducted on a best-efforts basis, which means that there is no minimum number of Offered Shares that must be sold by us for this offering to close; thus, we may receive no or minimal proceeds from this offering. All proceeds from this offering will become immediately available to us and may be used as they are accepted. Purchasers of the Offered Shares will not be entitled to a refund and could lose their entire investments.

The Company expects that the amount of expenses of the offering (not including marketing to investors and commissions or state filing fees) will be approximately $100,000.

| Number

of or Primary Shares offered by the Company (2) | Per

Unit or Share (3) | Total Maximum | ||||||||||

| Units | 9,500,000 | (4) | $ | 2.50 | $ | 23,750,000 | (1)(6) | |||||

| Commissions(1)(6)(7) | $ | 0.00 | ||||||||||

| Proceeds to Company – Primary Units | $ | 2.50 | $ | 23,750,000 | ||||||||

| Bonus Shares | 950,000 | $ | 0.00 | (4) | $ | 0.00 | ||||||

| Commissions(7) | $ | 0.00 | ||||||||||

| Proceeds to Company-Bonus Shares | 0.00 | 0.00 | ||||||||||

| Total Proceeds to Company | $ | 23,750,000 | ||||||||||

| Warrants | Exercise Price per Warrant | |||||||||||

| Shares Underlying Warrants | 19,000,000 | (5) | $ | 2.50 | $ | 47,500,000 | ||||||

| Commissions (7) | $ | 0.00 | ||||||||||

| Proceeds to Company- Exercise of Warrants | $ | 47,500,000 | ||||||||||

| Proceeds to Company – From Units and the Exercise of Warrants | $ | 2.50 | $ | 71,250,000 | (8) |

| (1) | The Company previously engaged Castle Placement LLC to act as placement agent for this offering. However, effective June 26, 2024, the Company terminated Castle Placement LLC and is now selling the Units directly, using the services of the Manhattan Street Capital platform. No commissions will be paid to Manhattan Street Capital or any other party with respect to the sale of unites. |

| (2) | We are offering Units on a continuous basis. See “Distribution – Continuous Offering. The Units consist of one (1) share and two (2) warrants per Unit. |

| (3) | Our Board of Directors used its business judgment in setting a value of $2.50 per Unit to the Company as consideration for the stock to be issued under the Offering. The sales price per Unit bears no relationship to our book value or any other measure of our current value or worth. This is a “best efforts” offering. The proceeds of this offering will be placed into an escrow account. We will offer the Units on a best-efforts basis primarily through an online platform. As there is no minimum offering, upon the approval of any subscription to this Offering Circular, the Company shall immediately deposit said proceeds into the bank account of the Company and may dispose of the proceeds in accordance with the Use of Proceeds. See “How to Subscribe.” |

| (4) | No additional consideration will be received by the Company for the issuance of Bonus Shares and the Company will absorb the cost of the issuance of the Bonus Shares. If eligible for Bonus Shares, investors will receive the greater amount of Bonus Shares for which they are eligible and are not cumulative even if investors would qualify for multiple eligibility categories for receipt of Bonus Shares. See “Plan of Distribution” for further details. The Company will not receive any consideration for the additional 950,000 Bonus Shares. The Bonus Shares represent an effective discount of $0.25 or 10%. No fees or commissions will be paid with respect to sale of the Bonus Shares. |

| (5) | Includes Warrants to purchase 20,000,000 common shares issued in connection with the Units. |

| (6) | Excludes estimated total offering expenses of approximately $100,000. |

| (7) | The Company has not engaged the services of a broker-dealer for this Offering. This Offering is not being made in all states. |

| (8) | Although the Company will not receive any consideration for the Bonus Shares, the value of such Bonus Shares ($2,375,000) will be included towards the $75,000,000 maximum amount for any given year. |

The Company has engaged Enterprise Bank as an escrow agent (the “Escrow Agent”) to hold funds tendered by investors, and may hold a series of closings on a rolling basis at which we receive the funds from the escrow agent and issue the Securities to investors. The offering will terminate at the earlier of the date at which the maximum offering amount has been sold or the date at which the offering is earlier terminated by the Company in its sole discretion. After each closing, funds tendered by investors will be available to the Company.

THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OR GIVE ITS APPROVAL OF ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SOLICITATION MATERIALS. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION.

These securities may not be sold nor may offers to buy be accepted before the post effective amendment to the offering statement filed with the Commission is qualified. This post effective amendment to the offering circular shall not constitute an offer to sell or the solicitation of an offer to buy nor may there be any sales of these securities in any state in which such offer, solicitation or sale would be unlawful before registration or qualification under the laws of such state. The Company may elect to satisfy its obligation to deliver a final post effective amendment to the offering circular by sending you a notice within two business days after the completion of the Company’s sale to you that contains the URL where the final post effective amendment to the offering circular or the offering statement in which such final offering circular was filed may be obtained.

GENERALLY NO SALE MAY BE MADE TO YOU IN THIS OFFERING IF THE AGGREGATE PURCHASE PRICE YOU PAY IS MORE THAN 10% OF THE GREATER OF YOUR ANNUAL INCOME OR NET WORTH. DIFFERENT RULES APPLY TO ACCREDITED INVESTORS AND NON-NATURAL PERSONS. BEFORE MAKING ANY REPRESENTATION THAT YOUR INVESTMENT DOES NOT EXCEED APPLICABLE THRESHOLDS, WE ENCOURAGE YOU TO REVIEW RULE 251(d)(2)(i)(C) OF REGULATION A. FOR GENERAL INFORMATION ON INVESTING, WE ENCOURAGE YOU TO REFER TO www.investor.gov.

This offering is inherently risky. See “Risk Factors” on page 12.

Sales of these securities will commence on approximately November 24, 2025.

The Company is following the “Offering Circular” format of disclosure under Regulation A.

The date of this Post-Qualification Offering Circular Amendment No. 4 is November 24, 2025.

TABLE OF CONTENTS

In this Offering Circular, the term Water On Demand,” “we,” “us,” “our,” or “the Company” refers to Water On Demand, Inc.

THIS OFFERING CIRCULAR MAY CONTAIN FORWARD-LOOKING STATEMENTS AND INFORMATION RELATING TO, AMONG OTHER THINGS, THE COMPANY, ITS BUSINESS PLAN AND STRATEGY, AND ITS INDUSTRY. THESE FORWARD-LOOKING STATEMENTS ARE BASED ON THE BELIEFS OF, ASSUMPTIONS MADE BY, AND INFORMATION CURRENTLY AVAILABLE TO THE COMPANY’S MANAGEMENT. WHEN USED IN THE OFFERING MATERIALS, THE WORDS “ESTIMATE,” “PROJECT,” “BELIEVE,” “ANTICIPATE,” “INTEND,” “EXPECT, “ASSUME” AND SIMILAR EXPRESSIONS ARE INTENDED TO IDENTIFY FORWARD-LOOKING STATEMENTS, WHICH CONSTITUTE FORWARD LOOKING STATEMENTS. THESE STATEMENTS REFLECT MANAGEMENT’S CURRENT VIEWS WITH RESPECT TO FUTURE EVENTS AND ARE SUBJECT TO RISKS AND UNCERTAINTIES THAT COULD CAUSE THE COMPANY’S ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE CONTAINED IN THE FORWARD-LOOKING STATEMENTS. INVESTORS ARE CAUTIONED NOT TO PLACE UNDUE RELIANCE ON THESE FORWARD-LOOKING STATEMENTS, WHICH SPEAK ONLY AS OF THE DATE ON WHICH THEY ARE MADE. THE COMPANY DOES NOT UNDERTAKE ANY OBLIGATION TO REVISE OR UPDATE THESE FORWARD-LOOKING STATEMENTS TO REFLECT EVENTS OR CIRCUMSTANCES AFTER SUCH DATE OR TO REFLECT THE OCCURRENCE OF UNANTICIPATED EVENTS.

i

SUMMARY OF THE OFFERING (POST-QUALIFICATION AMENDMENT NO. 1)

Water on Demand, Inc. (“WODI”), a Texas corporation, is a subsidiary of OriginClear, Inc., a Nevada public corporation (“OCLN”). Through its subsidiary, Progressive Water Treatment, Inc. (“PWT”), an established designer and manufacturer of a complete line of water treatment systems for municipal, industrial and pure water applications, WODI deploys a wide range of technologies, including chemical injection, media filters, membrane, ion exchange and SCADA (supervisory control and data acquisition) technology in turnkey systems. Beyond the operations of PWT, WODI has stated its intention to evolve into a fintech focused company turning water systems into tax-leveraged assets, focusing entirely on developing and providing financing services, instead of competing with, water equipment companies.

OCLN acquired PWT in 2015. PWT has already established robust design and manufacturing offerings as well as maintenance and service offerings, and continued to do so under OCLN.

In September 2023, PWT merged with Water on Demand, Inc., a Nevada corporation (“WODI NV”), a water managed services company being developed at the time by OCLN. As a result of the merger, PWT changed its name to Water on Demand, Inc. (“WODI”), a Texas Company, in which OCLN continues to own a substantial equity stake.

In 2018, OCLN launched Modular Water Systems (MWS) to bring to market smaller, standardized water treatment systems. However, in, May 2025, WODI announced it intention to part ways with MWS and its inventor, Daniel M. Early, President and Chief Engineer of MWS, and transition out of MWS. Mr. Early agreed to assist in wrapping up all current projects and staying on as technical advisor to WODI. This transition will allow WODI to focus on its water infrastructure project financing and planned operations, including the planned launch of a Opportunity Zone Fund that will seek to raise up to $100 million.

Water On Demand

Water On Demand (“WOD”) aims to offer customers financing and solutions as a service for water self-sustainability - allowing them to pay on a per-gallon basis for managed wastewater treatment services rather than incurring significant upfront capital equipment acquisition costs. This approach, generally known as DBOO, provides an alternative to conventional on-site wastewater treatment solutions requiring substantial initial investments.

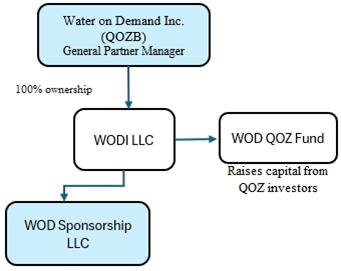

On April 17, 2025, WODI retained Eazy Do It, Inc., a platform for US Opportunity Zones (OZs) and a leading resource provider for the OZ ecosystem, to help develop the Water On Demand Opportunity Zone Fund. WODI intends to launch a series of such funds (“the Funds”).

1

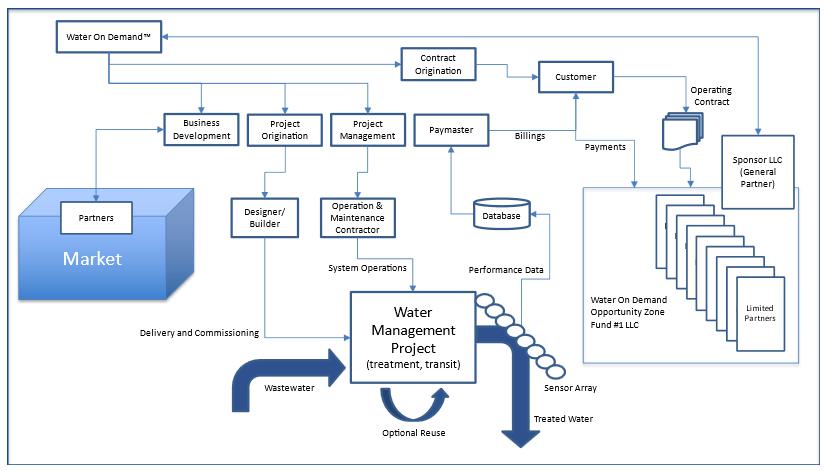

Under the new model, WODI intends act as General Partner of the Funds (the “Sponsorship”), in return for customary management fees, and as well as fees for business development, contract origination, project origination, project management and paymaster functions serving, as shown in the illustration below.

Figure 1: The Water On Demand Opportunity Zone Fund #1 Operating Lifecycle

The Company recently announced agreements with Enviromaintenance ®, a water services company, and Klir®, a utility network software provider, to support a WOD pilot program in the mobile home park sector.

As part of its role in support of the Funds, WODI intends to direct the building and operation of WOD-Financed systems to regional water companies under performance contracts, thus creating a network of partners that can enable rapid scaling and establish a competitive barrier to entry. On January 6, 2025 , WODI began its buildout of personnel, hiring veteran C-Level Executive, James Woloszyn as it Chief Operating Officer. The Company intends to scale as it expands by acquiring additional staff or independent resources. WODI currently obtains administrative support from OriginClear under a management services arrangement. All other members of WODI’s Board of Directors and executive officers are currently the same as those of OCLN, with the exception of Kenneth A. Berenger, who serves as co-chairman of WODI.

On March 26, 2024, the Company announced a Memorandum of Understanding with Enviromaintenance to collaborate on the planned WOD pilot program in the Greater Central Texas Region. On April 9, 2024, the Company announced that Klir, Inc. had been selected to support the WOD pilot, further bolstering the Company’s efforts to provide decentralized water management solutions on a pay-per-gallon basis, with anticipated financing provided by the Funds. Additional information regarding these developments is available in the Company’s publicly filed materials.

2

Water on Demand NV

In 2023, OCLN launched WODI NV to offer private businesses the opportunity to outsource and finance water treatment and purification services on a per-gallon basis while gaining independence from traditional, centralized private water infrastructure. WODI NV’s value proposition is that by outsourcing water treatment and purification, private businesses can gain the water security of a private, decentralized infrastructure while avoiding the capital, technological and administrative burden required to design, finance, build, operate and maintain a water treatment solution.

Following the creation of the merged company, WODI took over this function.

Combined Companies

As of May 1, 2025, Water on Demand (formerly PWT), MWS and WODI NV have been consolidated under the Company, with OCLN being the largest single shareholder of the combined companies. The combined companies have complementary offerings that create meaningful synergies with the goal of allowing the Company to emerge as a leader in offering end-to-end outsourced water treatment services.

Products of Combined Company

| Division | Products | Customers | Geographic Region | Financing provided by WODI | ||||

| PWT | High-purity water systems, Reverse Osmosis (RO) Systems, Deionization Systems, Water Softening Solutions | Municipalities, Power Generation and Semiconductor. | North America | Not applicable | ||||

| WODI | Pay-as-you-go Project Financing of Turnkey Water Treatment Systems, Fund Management | Businesses, Municipalities, Industrial Clients |

North America | Through managed entities, WODI plans to provide financing options for water development projects helping clients manage upfront costs. These include structured financing plans that spread costs over time. |

Industry Background

Traditional Water Treatment Practices

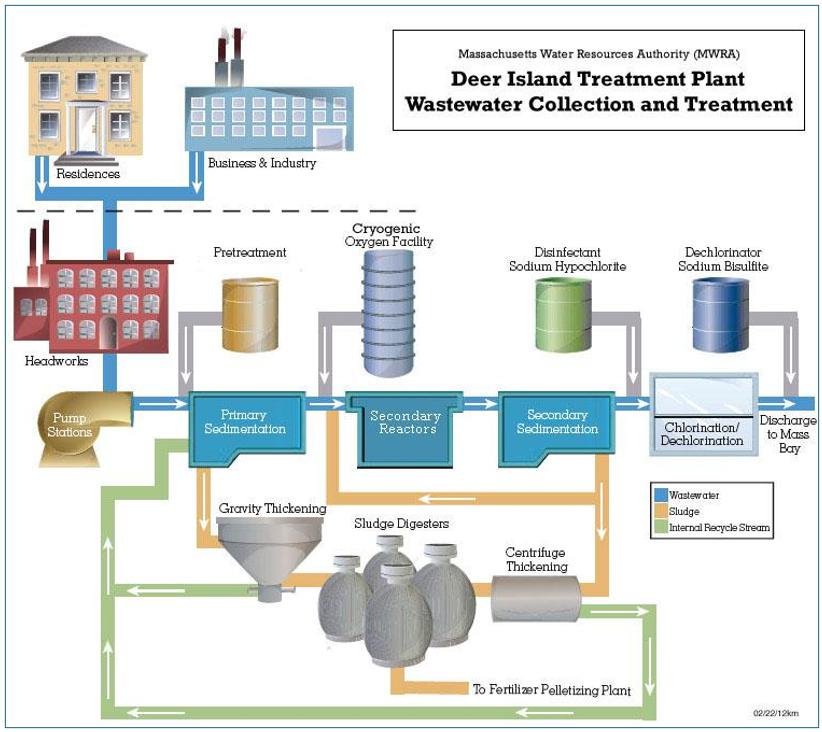

Public water utilities manage the collection, treatment, and distribution of water for residential, medical, and industrial use, as well as wastewater treatment. Globally, water treatment is centralized at large municipal facilities, benefiting from economies of scale. In the U.S, approximately 16,000 publicly owned wastewater treatment systems exist, however the largest 10% of these publicly owned plants process over 80% of all wastewater. Just 1.25% of facilities handle more than half of the nation’s wastewater.

Wastewater treatment plants receive ss wastewater from residential, commercial and ground runoff, through a network of storm drains and sewer lines. The wastewater is processed in three phases:

In preliminary treatment, large debris, sand, and mud settle in grit chamber, which is later disposed of in landfills for environmentally safe disposal. During primary treatment, wastewater enters settling tanks, where up to 60% of solids are separated as a sludge-water mixture. While this removes a majority of solid waste it does not remove toxic chemicals. In secondary treatment, oxygen is introduced through aeration, accelerating the growth of microorganisms which break down organic matter and reduce harmful gases. These microorganisms settle to the bottom of the secondary settling tanks. After secondary treatment, 80-90% of human waste, solids, and toxins have been removed from the wastewater.

3

During the final stage of secondary treatment, water is disinfected – typically with chlorine, which eliminates over 99% of bacteria. Before discharging the treated water into the environment, chlorine is neutralized to prevent ecological harm. As an alternative to chlorination and dichlorination, some facilities remove bacteria using ultraviolet light, carbon absorption, distillation and reverse osmosis.

Sludge from primary and secondary treatment undergoes further processing in digesters where it is mixed and heated t to reduce volume and eliminate disease-causing bacteria. The processed solids are then heat-dried in pelletizing plants and converted into fertilizer for use in agriculture, forestry, and land reclamation.

This three-phase process is the global standard for wastewater treatment. Given the industrial nature of the process and cost efficiencies achieved through economies of scale, treatment facilities are constructed on a massive scale with large facilities capable of processing over 1 billion gallons of water per day and construction costs billions of dollars.

Figure 2: A typical municipal sewer system (https://www.mwra.com/your-sewer-system)

4

Aging Infrastructure and Funding Gaps

Much of the U.S. water infrastructure was built in the 1970s and is nearing or beyond its intended service life. According to the American Society of Civil Engineers (ASCE), over 80% of facilities are at or near capacity. Despite federal legislation, such as the Infrastructure Investment and Jobs Act (2023), a funding shortfall of over $400 billion is projected by 2029. Regulatory compliance costs, such as for PFAS or lead removal, continue to rise.

The United States faces a significant funding shortfall for its water infrastructure, with estimates suggesting a deficit exceeding $1 trillion over the next 20 years to address critical needs in drinking water, wastewater, and stormwater systems. This gap stems from aging infrastructure, increasing demand, regulatory requirements, and insufficient investment. https://www.pewtrusts.org/en/research-and-analysis/articles/2024/09/05/water-system-upgrades-could-require-more-than-%241-trillion-over-next-20-years

Privatization and Decentralization Trends

Limited federal support, rising operational costs, and increased regulatory demands are pushing utilities to explore alternatives. Decentralized water treatment—where water is treated on-site—offers faster deployment, lower capital requirements, and operational flexibility, especially in rural or underserved areas. These systems reduce reliance on aging infrastructure and are increasingly favored by industrial users, developers, and small municipalities.

Emerging Drivers of Water Demand

Shifts such as climate change, migration, and reshoring of industrial activity are increasing pressure on local water systems. Decentralized solutions can adapt more quickly to changing demographics and site-specific needs, making them an essential part of modern water infrastructure strategy.

Climate Change

Prolonged droughts, shifting precipitation patterns, and rising temperatures are contributing to water scarcity. Groundwater levels in many areas are declining faster than can be replenished. As precipitation becomes more irregular, the global supply of usable freshwater is increasingly under pressure.

Migration

Shifting migration patterns and unpredictable population growth complicate long-term infrastructure planning. Traditional municipal wastewater plants require decades to plan and build, making them less responsive to demographic shifts. Decentralized water systems, in contrast, require less capital and can be deployed more quickly, offering greater flexibility.

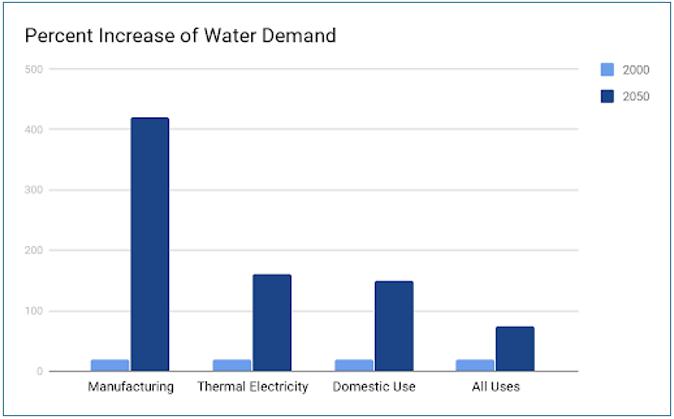

Reshoring of Manufacturing

The reshoring of industrial operations, driven by supply chain realignments and national policy, is increasing demand for water across the manufacturing sector. As domestic production expands, water-intensive operations are expected to place additional pressure on regional water supplies.

Figure 3: Visual representation of OECD

Environmental Outlook to 2050

www.bbc.com/future/story/20170412-is-the-world-running-out-of-fresh-water

5

Regulatory and Public Funding Risk

Water resource planning is becoming increasingly complex as freshwater supplies tighten and regulatory scrutiny intensifies. The Federal Reserve Bank of St. Louis has recommended more efficient allocation of water resources, while recent legal rulings—such as the 2021 U.S. Supreme Court decision on interstate groundwater rights—highlight growing disputes over access. In the western United States, limited coordination among states in the Colorado River Basin underscores the challenge of balancing declining supply with rising demand. These pressures elevate both financial and operational risks for municipalities and private water operators.

Industrial Centralization Risk

Large-scale, centralized water systems represent single points of failure that are increasingly vulnerable to disruption from natural disasters, financial constraints, and security threats. As infrastructure ages and environmental risks increase, these vulnerabilities become more acute. Decentralized water systems mitigate these risks by localizing treatment, offering greater resilience and control for communities, businesses, and institutions.

Water on Demand

WODI offers financing solutions that allow businesses and communities to develop water treatment systems without upfront capital investment. Through long-term service agreements, end-users pay only for the water they use. Projects are supported by experienced regional water providers and powered by standardized modular systems, ensuring efficiency and reliability. By leveraging proven technologies and a pay-per-use model, WODI reduces financial and operational risk while expanding access to advanced water treatment solutions.

Global Water Challenges

A 2021 study by Utrecht University and United Nations University found that nearly half of global wastewater is discharged untreated, while only 11% is reused. With the World Wildlife Fund projecting that two-thirds of the global population could face water shortages by 2025, increasing wastewater reuse is critical.

In North America, supply inefficiencies further strain resources—Stanford University estimates that 20–50% of water is lost through leaking infrastructure. In the U.S., the Environmental Integrity Project reports that nearly half of rivers, streams, and lakes are too polluted for swimming, fishing, or drinking. Public concern is growing, with a 2017 Gallup poll showing 63% of Americans worry about drinking water pollution and 57% about contamination of natural water bodies.

These challenges underscore the need for decentralized, resilient, and sustainable water solutions.

Decentralized Water Solutions

Businesses increasingly rely on onsite water treatment and recycling to address the limitations of centralized water utilities. Onsite systems provide tangible assets, improved water quality, and cost savings, especially when recycled water is used. WODI supports these efforts by helping business develop decentralized water treatment solutions tailored to their operational needs, enhancing resilience and reducing dependence on public infrastructure.

This trend aligns with ESG investing, which accounts for approximately 25% of all professionally managed assets worldwide. Effective water management is a key ESG metric, further emphasizing the importance of decentralized solutions.

6

Employees

As of the date of this filing, WODI employs approximately 27 full-time staff across engineering, manufacturing, sales, and administration. Operational and back-office support is provided through an administrative services agreement with OCLN.

The Company’s Competition

Competitive Analysis

PWT, while enjoying a great deal of prestige for its work on a variety of engineered solutions, especially in the power plant sector, is not uniquely differentiated.

However, the WOD plan to focus entirely on developing and providing financing services, instead of competing with water equipment companies is unique in its plan to seek to take advantage of tax benefits associated with investments in qualified opportunity zones.

Company management has addressed this unique factor in public statements:

“The water equipment business is historically very low-margin, with most such companies netting about 16% in net profits,” said Riggs Eckelberry, WODI CEO. “Meanwhile, the water-as-a-service business model is extremely profitable. Focusing only on that business will make us a resource for water companies and not a competitor.”

“Until recently, our ‘Water Like An Oil Well’ initiative lacked the tax benefits that other industries like oil and gas enjoy,” said Ken Berenger, EVP and co-chairman of WODI. “That’s now changed with the new water Opportunity Zone fund, which will be designed to provide favorable tax benefits.”

“When you think of it,” added Berenger, “we could take years to build a few more water companies… when there are already thousands out there. Or, we could help them address the looming trillion-dollar funding deficit with innovative financing for their clients, that happens to be very profitable for Water On Demand.”

7

Government Regulation

We are subject to various laws, regulations, and permitting requirements of federal, state, and local authorities, related to health and safety, anti-corruption and export controls. The foregoing may include the U.S. Foreign Corrupt Practices Act of 1977, the U.S. Export Administration Regulations, Money Laundering Control Act of 1986 and any other equivalent or comparable laws of other countries. We believe that we are in material compliance with all such laws, regulations, and permitting requirements.

Employees and Human Capital Resources

As of the filing date, the Company, together with its operating companies, had 25 full-time employees. The Company has an arrangement with OCLN whereby OCLN provides operational and administrative services for the Company.

Facilities

The Company’s corporate headquarters are located at 13575 58th Street North, Suite 200, Clearwater, Florida 33760. The Company leases a production facility at 5225 W Houston Sherman, Texas, under a non-cancelable operating lease classified in accordance with ASC 842, Leases. The lease commenced on July 1, 2024, with a 61-month term. Under a Triple Net (NNN) arrangement, the Company is responsible for property taxes, insurance and maintenance costs.

Legal Proceedings

The Company is not involved in any litigation, and its management is not aware of any pending or threatened legal actions relating to its intellectual property, conduct of business activities or otherwise. From time to time, we may be involved in pending or threatened claims relating to contract disputes, employment, intellectual property and other matters that arise in the normal course of our business, which we do not deem to be material to the business.

Patents

The Company does not currently hold any active patents. However, it continues to design and manufacture methods to deliver innovative, durable solutions for decentralized wastewater treatment.

Employees

As of the date of this filing, the Company had approximately 27 employees. The Company has an arrangement with OCLN whereby OCLN provides operational and administrative services for the Company. The Company recently implemented workforce reductions in connection with ongoing operational restructuring.

8

The Offering

| Securities offered | Units (1 share of Common Stock and 2 Warrants) Maximum of 9,500,000 Units at $2.50 per share(1). | |

| Warrants | 3-year term; $2.50 exercise price, eligible for cashless option | |

| Offering Amount | Total targeted proceeds is $71,250,000 from the sale of 9,500,000 Units at $2.50 per Unit and the exercise of 19,000,000 Units at $2.50 per share. | |

| Bonus Shares | Up to 9,500,000 bonus shares of common stock. | |

| Common Shares outstanding prior to this offering | 22,769,502 shares(2) | |

| Number of Common Shares issued previously in this offering | 4,400(3) | |

| Number of Common Shares following this offering Presuming all shares sold and all warrants issued. | 77,551,0514 | |

| Use of proceeds | The net proceeds of a fully subscribed offering, after estimated total offering expenses and commissions will be used for general corporate SG&A and business purposes including professional services fees, fees to OCLN for supporting administrative functions, IT infrastructure, acquisitions, hiring of personnel, sales and marketing expenses and general working capital, acquisitions, and to provide debt financing to one or more project specific subsidiaries of the Company. The details of our plans are set forth in “Use of Proceeds.” |

| (1) | Estimated pre-offering valuation of $66,000,000 based on the Fairness Opinion dated October 24, 2023, replacing Modular Water Systems forecasts with the new revenue model now in development with respect to Sponsorship and servicing functions related to the Funds. The Company may amend or withdraw this Offering in the future to reprice the Securities of Common Stock at any time as it deems necessary or appropriate. The Company reserves the rights to sell fractional units as necessary. |

| (2) | Non-diluted. Does not include the rights to receive up to 10,643,267 common shares related to certain restricted stock grant agreements. |

| (3) | Prior to this amendment, the Company issued 4,400 common shares. This amendment amends the securities being offered from common shares to Units (1 Common Share and 2 Warrants). |

9

Selected Risks Associated with Our Business

Our business is subject to a number of risks and uncertainties, including those highlighted in the section titled “Risk Factors” immediately following this summary. These risks include, but are not limited to, the following:

| ● | We are an early-stage company and have not yet generated any profits or significant revenues. |

| ● | We may not be able to continue to operate the business if we are not successful in securing significant additional fundraising in a short timeframe and, as a result, we may not be able to continue as a going concern. |

| ● | The Company relies on rolling closes of equity infusions for its financings which may pose a risk to having sufficient capital on hand at any point in time. |

| ● | The Company has a limited operating history by which performance can be gauged. |

| ● | The Company is subject to potential fluctuations in operating results. |

| ● | The Company’s future operating results are difficult to predict and may be affected by a number of factors, many of which are outside of the Company’s control. |

| ● | Unanticipated obstacles may hinder the execution of the Company’s business plan. |

| ● | We have limited market acceptance of our services. |

| ● | We cannot assure you that we will effectively manage our growth. |

| ● | Our costs may grow more quickly than our revenues, harming our business and profitability. |

| ● | We expect to raise additional capital through equity and/or debt offerings and to provide our employees with equity incentives. Therefore, your ownership interest in the Company is likely to continue to be diluted and subordinated. |

| ● | The loss of one or more of our key personnel, or our failure to attract and retain other highly qualified personnel in the future, could harm our business. |

| ● | If we are unable to protect our intellectual property, the value of our brand and other intangible assets may be diminished and our business may be adversely affected. |

10

| ● | Our financial results will fluctuate in the future, which makes them difficult to predict. |

| ● | We may face additional competition. |

| ● | In connection with the audit of our financial statements for the period from inception to August 31, 2022, our independent auditor identified material weaknesses in our internal control over financial reporting related to certain corporate finance and accounting oversight, which were primarily the result of the lack of sufficient and competent accounting and finance resources. Our failure to implement and maintain effective internal control over financial reporting may in the future result in material misstatements in our financial statements, which has and could in the future require us to restate financial statements, cause investors to lose confidence in our reported financial information and could have an adverse effect on our ability to fundraise. |

| ● | We realized a gross and net loss for each period since our inception to date, and there can be no assurances that the Company will become profitable in the future. |

| ● | The Company is controlled by its OriginClear, Inc. (OCLN), which also provides all funding, sales and administrative resources. |

| ● | Actual or threatened epidemics, pandemics, outbreaks, or other public health crises may adversely affect our business, including pandemics similar to the novel COVID-19 outbreak. |

| ● | The offering price for the Securities has been determined by the Company rather than any of the investors. |

| ● | An investment in the Securities is not a diversified investment. |

| ● | Subsequent offerings or potential recapitalizations of the Company’s capital stock below the offering price or on terms better than the Securities may adversely affect the market price of the Company’s capital stock and may make it difficult for the Company to continue to sell Units or other equity or debt securities. |

| ● | The Company may apply the proceeds of this offering to uses for which you may disagree. |

| ● | Investors in this offering may not be entitled to a jury trial with respect to claims arising under the subscription agreement, which could result in less favorable outcomes to the plaintiff(s) in any action under the agreement. |

| ● | There is no current market for any of our shares of stock. |

11

The Commission requires the Company to identify risks that are specific to its business and its financial condition. The Company is still subject to all the same risks that all companies in its business, and all companies in the economy, are exposed to. These include risks relating to economic downturns, political and economic events and technological developments (such as hacking and the ability to prevent hacking). Additionally, early-stage companies are inherently riskier than more developed companies. You should consider general risks as well as specific risks when deciding whether to invest.

This investment has a high degree of risk. Before you invest you should carefully consider the risks and uncertainties described below and the other information in this prospectus. If any of the following risks actually occur, our business, operating results and financial condition could be harmed and the value of our stock could go down. This means you could lose all or a part of your investment.

We have a limited operating history upon which you can evaluate our performance, and accordingly, our prospects must be considered in light of the risks that any new company encounters.

The Company is still in an early phase and we are just beginning to implement our business plan. There can be no assurance that we will ever operate profitably. The likelihood of our success should be considered in light of the problems, expenses, difficulties, complications and delays usually encountered by early-stage companies. The Company may not be successful in attaining the objectives necessary for it to overcome these risks and uncertainties.

The amount of capital the Company is attempting to raise in this Offering may not be enough to sustain the Company’s current business plan.

In order to achieve the Company’s near and long-term goals, the Company may need to procure funds in addition to the amount raised in the Offering. There is no guarantee the Company will be able to raise such funds on acceptable terms or at all. If we are not able to raise sufficient capital in the future, we may not be able to execute our business plan, our continued operations will be in jeopardy and we may be forced to cease operations and sell or otherwise transfer all or substantially all of our remaining assets, which could cause an Investor to lose all or a portion of their investment.

We may face potential difficulties in obtaining capital.

We may have difficulty raising needed capital in the future as a result of, among other factors, our lack of revenues from sales, as well as the inherent business risks associated with our Company and present and future market conditions. Future sources of revenue may not be sufficient to meet our future capital requirements. We will require additional funds to execute our business strategy and conduct our operations. If adequate funds are unavailable, we may be required to delay, reduce the scope of or eliminate one or more of our research, development or commercialization programs, product launches or marketing efforts, any of which may materially harm our business, financial condition and results of operations.

We may implement new lines of business or offer new products and services within existing lines of business.

As an early-stage company, we may implement new lines of business at any time. There are substantial risks and uncertainties associated with these efforts, particularly in instances where the markets are not fully developed. In developing and marketing new lines of business and/or new products and services, we may invest significant time and resources. Initial timetables for the introduction and development of new lines of business and/or new products or services may not be achieved, and price and profitability targets may not prove feasible. We may not be successful in introducing new products and services in response to industry trends or developments in technology, or those new products may not achieve market acceptance. As a result, we could lose business, be forced to price products and services on less advantageous terms to retain or attract clients or be subject to cost increases. As a result, our business, financial condition or results of operations may be adversely affected.

In order to satisfy the Company’s obligations as a public company, we will need to hire qualified accounting and financial personnel with appropriate public company experience.

As a public company, we will need to establish and maintain effective disclosure and financial controls and make changes in its corporate governance practices. We may need to hire additional accounting and financial personnel with appropriate public company experience and technical accounting knowledge, and it may be difficult to recruit and retain such personnel. Even if the Company is able to hire appropriate personnel, its existing operating expenses and operations will be impacted by the direct costs of their employment and the indirect consequences related to the diversion of management resources from research and development efforts.

12

The commercial and credit environment may adversely affect the Company’s access to capital.

We will need to continue to raise capital in order to execute our business plan. the Company’s ability to issue debt or enter into other financing arrangements on acceptable terms could be adversely affected if there is a material decline in the demand for its products or in the solvency of its customers or suppliers or if there are other significantly unfavorable changes in economic conditions. Volatility in the world financial markets could increase borrowing costs or affect the Company’s ability to access the capital markets. Capital raised by us may have a dilutive impact on existing stockholders and if the Company is unable to raise additional capital on favorable terms, or at all, we may be unable to maintain its research and development activities or may be unable to grow its business, which could impact the Company’s operating results and gross margin adversely.

Wage increases and pressure in certain geographies may prevent us from sustaining the Company’s competitive advantage and may reduce its profit margin.

Measures are being taken in the United States and globally to increase minimum wages, and there is a shortage of skilled labor in certain locations leading to increased wage pressure. Similarly, with an increased global focus on environmental, social and corporate-governance concerns and sustainability, input costs have been steadily rising. Accordingly, we may need to increase the levels of labor compensation more rapidly than in the past to remain competitive in attracting and retaining the quality and amount of labor that its business requires. To the extent that the Company is not able to control or share wage increases, wage increases may reduce its margins and cash flows, which could adversely affect its business.

The loss of one or more key members of the Company’s management team or personnel, or its failure to attract, integrate and retain additional personnel in the future, could harm its business and negatively affect its ability to successfully grow its business.

The Company is highly dependent upon the continued service and performance of the key members of the Company’s management team and other personnel. The loss of any of these individuals, each of whom is “at will” and may terminate his or her employment relationship with us at any time, could disrupt its operations and significantly delay or prevent the achievement of its business objectives. We believe that its future success will also depend in part on its continued ability to identify, hire, train and motivate qualified personnel. High demand exists for senior management and other key personnel (including technical, engineering, product, finance and sales personnel) in the infrastructure and manufacturing industry. A possible shortage of qualified individuals in the regions where we operate might require us to pay increased compensation to attract and retain key employees, thereby increasing its costs. In addition, we face intense competition for qualified individuals from numerous companies, many of whom have substantially greater financial and other resources and name recognition than us. We may be unable to attract and retain suitably qualified individuals who are capable of meeting its growing operational, managerial and other requirements, or we may be required to pay increased compensation in order to do so. For example, the Company’s failure to attract and retain shop floor employees may inhibit its ability to fulfill production orders for its customers. the Company’s failure to attract, hire, integrate and retain qualified personnel could impair its ability to achieve its business objectives.

All of the Company’s employees (which includes full time and part time employees and consultants) are at-will employees, meaning that they may terminate their employment relationship with us at any time, and their knowledge of its business and industry would be extremely difficult to replace. We generally enter into non-competition agreements with its employees and certain consultants. These agreements prohibit the Company’s employees and applicable consultants from competing directly with us or working for its competitors or customers while they work for us, and in some cases, for a limited period after they cease working for us. We may be unable to enforce these agreements under the laws of the jurisdictions in which its employees and applicable consultants work and it may be difficult for us to restrict the Company’s competitors from benefiting from the expertise that the Company’s former employees or consultants developed while working for us. If we cannot demonstrate that its legally protectable interests will be harmed, we may be unable to prevent its competitors from benefiting from the expertise of its former employees or consultants and its ability to remain competitive may be diminished.

13

Risks Related to Government Regulations

Our business is subject to various laws and regulations and changes in such laws and regulations, or failure to comply with existing or future laws and regulations, could adversely affect our business.

Our business is subject to numerous and frequently changing federal, state and local laws and regulations. We routinely incur significant costs in complying with these regulations. The complexity of the regulatory environment in which we operate and the related cost of compliance are increasing due to additional legal and regulatory requirements, our expanding operation and increased enforcement efforts. Further, uncertainties exist regarding the future application of certain of these legal requirements to our business. New or existing laws, regulations and policies, liabilities arising thereunder and the related interpretations and enforcement practices, particularly those dealing with environmental protection and compliance, taxation, zoning and land use, workplace safety, public health, recurring debit and credit card charges, information security, consumer protection, and privacy and labor and employment, among others, or changes in existing laws, regulations, policies and the related interpretations and enforcement practices, particularly those governing the sale of products and consumer protection, may result in significant added expenses or may require extensive system and operating changes that may be difficult to implement and/or could materially increase our cost of doing business. For example, we have to comply with recent new laws in some of the states in which we operate regarding recycling, waste, minimum wages, and sick time. In addition, we are subject to environmental laws pursuant to which we could be strictly liable for any contamination at our current or former locations, or at third-party waste disposal sites, regardless of our knowledge of or responsibility for such contamination.

Our operations are subject to certain environmental laws and regulations.

Our current and former operations are governed by federal, state and local laws and regulations, including environmental regulations. Certain business activities involve the handling, storage, transportation, import/export, recycling, or disposing of various new and used products and generate solid and hazardous wastes. These business activities are subject to stringent federal, regional, state and local laws, by-laws and regulations governing the storage and disposal of these products and wastes, the release of materials into the environment or otherwise relating to environmental protection. These laws and regulations may impose numerous obligations upon our locations’ operations, including the acquisition of permits to conduct regulated activities, the imposition of restrictions on where or how to store and how to handle new products and to manage or dispose of used products and wastes, the incurrence of capital expenditures to limit or prevent releases of such material, the imposition of substantial liabilities for pollution resulting from our locations’ operations, and costs associated with workers’ compensation and similar health claims from employees.

Environmental laws and regulations have generally imposed further restrictions on our operations over time, which may result in significant additional costs to our business. Failure to comply with these laws, regulations, and permits may result in the assessment of administrative, civil, and criminal penalties, the imposition of remedial and corrective action obligations, and the issuance of injunctions limiting or preventing operation of our locations. Any adverse environmental impact on our locations, including, without limitation, the imposition of a penalty or injunction, or increased claims from employees, could materially and adversely affect our business and the results of our operations.

Environmental laws also impose liability for damages from and the costs of investigating and cleaning up sites of spills, disposals or other releases of hazardous materials. Such liability may be imposed, jointly and severally, on the current or former owners or operators of properties or parties that sent wastes to third-party disposal facilities, in each case without regard to fault or whether such persons knew of or caused the release. Moreover, neighboring landowners and other third parties may file claims for nuisance (including complaints involving noise and light), personal injury and property or natural resource damage allegedly caused by our operations and the release of petroleum hydrocarbons, hazardous substances or wastes into the environment. Although we are not presently aware of any such material liability related to our current or former locations or business operations, such liability could arise in the future and could materially and adversely affect our business and the results of our operations.

14

Government regulations, weather conditions and natural hazards may affect our business.

Climate change, drought, overuse of sources of water, the protection of threatened species or habitats or other factors may limit the availability of ground and surface water. Climate change and seasonal drought conditions may impact our access to water supplies, and drought conditions currently exist in several areas of the United States. Governmental restrictions on water use may also result in decreased access to water supplies, which may adversely affect our financial condition and results of operations. Water service interruptions due to severe weather events are also possible. These include winter storms and freezing conditions in colder climate locations, high wind conditions in areas known to experience tornados, earthquakes in areas known to experience seismic activity, high water conditions in areas located in or near designated flood plains, hurricanes and severe electrical storms also have the potential to impact our access to water.

Any interruption in our ability to access water could materially and adversely affect our financial condition and results of operations. Furthermore, losses from business interruptions or damage to our facilities might not be covered by our insurance policies and such losses may make it difficult for us to secure insurance in the future at acceptable rates.

Failure to protect or enforce our intellectual property could reduce or eliminate any competitive advantage and reduce our potential sales and profitability and the cost of protecting or enforcing our intellectual property may be significant.

Our long-term success depends on our ability to market innovative competitive products. We own a number of patents, trade secrets, copyrights, trademarks, trade names and other forms of intellectual property related to our products and services throughout the world and the operation of our business, which we rely on to distinguish our services and solutions from those of our competitors. Patents have a limited life and, in some cases, have expired or will expire in the near future. We also have non-exclusive rights to intellectual property owned by others in certain of our markets. For example, some of our products may include components that are manufactured by our competitors. Our intellectual property may be challenged, invalidated, stolen, circumvented, infringed or otherwise violated upon by third parties or we may be unable to maintain, renew or enter into new license agreements with third-party owners of intellectual property on reasonable terms, or at all. In addition, the global nature of our business increases the risk that our intellectual property may be subject to infringement, theft or other unauthorized use or disclosure by others. Our ability to protect and enforce intellectual property rights, including through litigation or other legal proceedings, also varies across jurisdictions and in some cases, our ability to protect our intellectual property rights by legal recourse or otherwise may be limited, particularly in countries where laws or enforcement practices are less protective than those in the United States. Our inability to obtain sufficient protection for our intellectual property, or to effectively maintain or enforce our intellectual property rights, could lead to reputational harm and/or adversely impact our competitive position, business, financial condition or results of operations.

Competitors and others may also initiate litigation or other proceedings to challenge the scope, validity or enforceability of our intellectual property or allege that we infringed, misappropriated or otherwise violated their intellectual property. Any litigation or proceedings to defend ourselves against allegations of infringement, misappropriation, or other violations of intellectual property rights, regardless of merit, could be costly, divert attention of management and may not ultimately be resolved in our favor. If we are unable to successfully defend against claims that we have infringed the intellectual property rights of others, we may be prevented from using certain intellectual property or offering certain products, or may be liable for substantial damages, which in turn could materially adversely affect our business, financial condition or results of operations. We may also be required to develop an alternative, non-infringing product that could be costly, time-consuming or impossible, or seek a license from a third party, which may not be available on terms that are favorable to us, or at all. Any of the foregoing could have a material adverse effect on our business, financial condition and results of operations.

15

We rely on a limited number of suppliers for certain raw materials and supplied components. We may not be able to obtain sufficient raw materials or supplied components to meet our manufacturing and operating needs, or obtain such materials on favorable terms, which could impair our ability to fulfill our orders in a timely manner or increase our costs of production.

Our ability to manufacture and deliver water treatment systems is dependent upon the availability of raw materials and supplied components, which we source from a limited number of suppliers. Our reliance on these suppliers exposes us to volatility in pricing and availability. If we are unable to obtain sufficient quantities of required materials or components on favorable terms, in may result in delays in manufacturing schedules or i increased production costs.

Additionally, the imposition of tariffs or other trade restrictions on such raw materials or components could negatively affect our operations. Prolonged disruptions in the supply chain, challenges in qualifying new sources of supply, or volatility in material pricing could significantly impair our ability to manufacture cost-effectively on time, and may lead to order cancelations, or reduced margins – any of which could materially impact our business, financial condition and results of operations.

Although dependent on certain key personnel, the Company does not have any key person life insurance policies on any such people.

We are dependent on certain key personnel in order to conduct our operations and execute our business plan, however, the Company has not purchased any insurance policies with respect to those individuals in the event of their death or disability. Therefore, if any of these personnel die or become disabled, the Company will not receive any compensation to assist with such person’s absence. The loss of such person could negatively affect the Company and our operations. We have no way to guarantee key personnel will stay with the Company, as many states do not enforce non-competition agreements, and therefore acquiring key man insurance will not ameliorate all of the risk of relying on key personnel.

Potential Risks Associated with Global Pandemics

COVID-19. On March 11, 2020, the World Health Organization declared the current outbreak of a novel coronavirus disease 2019 (“COVID-19”) to be a global pandemic. The COVID-19 outbreak led to disruptions in the global economy, including extreme volatility in the stock market and capital markets and severe disruptions in the global supply chain, capital markets and economies. Future outbreaks of similar pandemics could have a significant affect upon the Company, its business and its ability to continue as a going concern.

Financial projections require caution

Prospective investors are urged to consider that any financial projections which might be discussed by the Company or its officers, employees, etc. should not be understood as any guarantee or assurance made on behalf of the Company. Projections based on past performance data or mathematical models are subject to externalities and risks of which the compiler may not or could not be aware. Such projections would not and should not be construed as indications or guarantees of future financial performance, nor should they be understood as such by prospective investors. Prospective investors should be aware of the inherent inaccuracies of forecasting. Although the Company has a reasonable basis for projections it might make and provide them herewith in good faith, prospective investors may wish to consult independent market professionals about the Company’s potential future performance.

Damage to our reputation could negatively impact our business, financial condition and results of operations

Our reputation and the quality of our brand are critical to our business and success in existing markets and will be critical to our success as we enter new markets. Any incident that erodes consumer loyalty for our brand could significantly reduce its value and damage our business. We may be adversely affected by any negative publicity, regardless of its accuracy. Also, there has been a marked increase in the use of social media platforms and similar devices, including blogs, social media websites and other forms of internet-based communications that provide individuals with access to a broad audience of consumers and other interested persons. The availability of information on social media platforms is virtually immediate as is it’s impact. Information posted may be adverse to our interests or may be inaccurate, each of which may harm our performance, prospects or business. The harm may be immediate and may disseminate rapidly and broadly, without affording us an opportunity for redress or correction.

16

Risks associated with the increased use of AI Technologies.

While the use of AI technologies is in the early stages of widespread adoption and continues to rapidly evolve, companies are increasingly considering the extent to which AI will be used in their operations. Risks related to AI include operational risks such as the potential for errors or inaccuracies in work product developed with AI; privacy-related risks, such as compliance with required privacy notices or receipt of consents; risks related to intellectual property rights with respect to both the inputs to the program (including leakage of confidential or proprietary information or infringement) and the program outputs (including infringement by and ownership rights to AI work product); risks related to AI’s impact on the workforce; content related risks for public AI generated outputs; and ethical risks related to the potential for inherent biases in the algorithm or programming, among others. The complexity of, and lack of transparency into, many AI models and the speed of technological advancements may make it difficult for companies to understand and assess their proper operation and fully recognize the related risks.

Cybersecurity-related issues are also a significant risk for AI.

In addition, the legal and regulatory environment relating to AI is uncertain and rapidly evolving, both in the US and internationally, and includes new regulations targeted specifically at AI as well as updates to or developments in intellectual property, privacy, consumer protection, employment, and other laws regarding the use of AI. These laws and regulations could require changes in the Company’s implementation of AI technology, increase compliance costs and/or increase the risk of non-compliance. Any of these risks could expose a company to liability or adverse legal or regulatory consequences and reputational harm. There is also the risk of AI-related competition and threats to current business models, as evolving AI technologies may increase competition, alter consumer demand or render existing technologies obsolete. In assessing whether and to what extent AI should be addressed in risk factors, companies should consider their disclosure on AI across their annual report, website, press releases and other public statements in light of their operations and industry, and determine whether risks related to AI pose a material risk to their businesses and prospects.

Risk Factor Considerations on Cybersecurity

Cybersecurity incidents, data misuse, and ransomware attacks continue to be top of mind for both companies and investors, particularly in light of evolving technologies such as AI. Unauthorized access and data breaches pose threats of theft, misuse, or loss of sensitive data, including personal, financial, and proprietary information which can result in operational disruptions, impact a company’s reputation, customer trust, and financial condition, and lead to legal liabilities, regulatory fines, and costly remediation efforts. Reliance on third-party vendors can introduce additional vulnerabilities. Further, timely detection, identification, and response to evolving cyber threats remain challenging, requiring significant resources for cybersecurity measures, technology upgrades, training, and incident response. Cybersecurity insurance may offer some protection, but it may not fully cover all losses or liabilities.

Climate

Recent extreme weather events, including the wildfires in Los Angeles and devastating hurricanes, flooding and heat waves experienced in 2024, underscore the physical, financial, and operational risks associated with severe weather and climate issues. Weather events can disrupt operations and supply chains, create shortages of raw materials, impact workforce availability and cause damage to business infrastructure. It is important that companies carefully consider and disclose any such risks that could materially impact their business, results of operations or financial condition.

Risk Factor Disclosure Related to Political Changes in the US:

US trade policies and practices:

President Trump has implementing a 10-20% tariff on US imports, a 25% tariff on imports from Mexico and Canada, and increasing the tariff on Chinese products. Whether and to what extent these tariffs will be imposed remains to be seen, but as a result of tariffs, materials and goods that US companies import may face higher prices, which could lead to reduced margins or increased prices that could cause decreased consumer demand. President Trump has discussed pursuing an agenda that focuses on deregulation, particularly with respect to environmental and climate change-related regulations. While this could be a boon to companies in the traditional energy sectors, such policies could be detrimental to more sustainable-focused energy companies or industries.

Immigration:

One clear focus of the Trump administration is the to reduce or eliminate illegal immigration, which could have an impact on businesses, particularly agriculture, construction, hospitality, home health care and child/elder care.

Changes to regulatory agencies:

The Trump administration has instituted significant changes to certain regulatory agencies and through the “Department of Government Efficiency,” or “DOGE,” has made significant changes to eliminate regulations, cut expenditures, and restructure federal agencies, some of which could impact public companies. For example, the administration has attempted to make several changes to the reach and oversight of the agencies which has had a significant effect on these agencies and those charged with carrying out their responsibilities. Similarly, there have been discussions of “reigning in” regulatory agencies such as the Federal Trade Commission, the Federal Communications Commission and the Federal Energy Regulatory Commission, all of which could impact how companies do business and could pose risks related to business operations and financial outlook.

International Geopolitics

Ongoing conflicts across the globe, such as in Russia-Ukraine and the Middle East, international tensions such as between the US and China and political turmoil in Europe, may add to the current economic uncertainty.

17

Risks Related to the Securities

The Securities will not be freely tradable under the Securities Act until one year from the initial purchase date. Although the Securities may be tradable under federal securities law, state securities regulations may apply, and each Investor should consult with their attorney.

You should be aware of the long-term nature of this investment. Because the Securities have not been registered under the Securities Act or under the securities laws of any state or foreign jurisdiction, the Securities have transfer restrictions and cannot be resold in the United States except pursuant to an applicable securities exemption. Although the Company is party to the Business Combination Agreement, there is no guarantee that the Business Combination will ever be completed and that the Company’s shares will be registered. Limitations on the transfer of the Securities may also adversely affect the price that you might be able to obtain for the Securities in a private sale. Investors should be aware of the long-term nature of their investment in the Company. Each Investor in this Offering will be required to represent that they are purchasing the Securities for their own account, for investment purposes and not with a view to resale or distribution thereof exchange.

This Offering is not Registered.

The offerings of the Securities will not be registered with the SEC under the Securities Act or with the securities authorities of any state. The Securities are being offered in reliance on exemptions from the registration provisions of Regulation A of the Securities Act and state securities laws applicable to offers and sales to prospective Investors meeting the prospective investor suitability requirements set forth herein. If the Board or the Company fail to comply with the requirements of such exemptions, prospective purchasers may have the right to rescind their purchase of the Securities, as applicable.

There is no guarantee of a return on an Investor’s investment.

There is no assurance that an Investor will realize a return on their investment or that they will not lose their entire investment. For this reason, each Investor should read this Memorandum and all exhibits carefully and should consult with their attorney and business advisor prior to making any investment decision.

There is currently no public market for our Securities. Failure to develop or maintain a trading market could negatively affect the value of our Securities and make it difficult or impossible for you to sell your Securities.

Prior to this Offering, there has been no public market for our Securities and a public market for our Securities may not develop after completion of this offering. There is no guarantee that the Business Combination will be completed or that there will ever be a public market for the Securities. There can be no assurance as to the liquidity of any markets that may develop for our Securities, the ability of holders of Securities to sell their Securities, or the prices at which holders may be able to sell Securities.

Your percentage ownership in the Company may be diluted in the future.

Stockholders’ percentage ownership in the Company may be diluted in the future because of equity issuances for acquisitions, capital market transactions or otherwise, including equity awards that the Combined Company will be granting to directors, officers and other employees. The Board has adopted an equity incentive plan subject to stockholder approval, for the benefit of certain of our current and future employees, service providers and non-employee directors.

From time-to-time, the Company may opportunistically evaluate and pursue acquisition opportunities, including acquisitions for which the consideration thereof may consist partially or entirely of newly-issued shares of Company common stock and, therefore, such transactions, if consummated, would dilute the voting power and/or reduce the value of our common stock.

An active, liquid trading market for the Company’s common stock may not develop, which may limit your ability to sell your shares.

The Company is currently a private company. An active trading market for the Company’s shares of common stock may never develop or be sustained following the consummation of the Business Combination. A public trading market having the desirable characteristics of depth, liquidity and orderliness depends upon the existence of willing buyers and sellers at any given time, such existence being dependent upon the individual decisions of buyers and sellers over which neither the Company nor any market maker has control. The failure of an active and liquid trading market to develop and continue would likely have a material adverse effect on the value of the Company’s common stock. An inactive market may also impair the Company’s ability to raise capital to continue to fund operations by issuing shares and may impair the Company’s ability to acquire other companies or technologies by using the Company’s shares as consideration.

18

The issuance of additional shares of common stock, preferred stock or convertible securities will likely dilute your ownership and could adversely affect the stock price.

From time to time in the future, the Company will likely issue additional shares of common stock, preferred stock or securities convertible into common stock pursuant to a variety of transactions, including acquisitions. Additional shares of common stock may also be issued upon exercise of outstanding stock options and warrants to purchase common stock. The issuance by us of additional shares of common stock or securities convertible into common stock would dilute your ownership of the Company and the sale of a significant amount of such shares in the public market could adversely affect prevailing market prices of our common stock. Subject to the satisfaction of vesting conditions and the expiration of lockup agreements, shares issuable upon exercise of options will be available for resale immediately in the public market without restriction.

Issuing additional shares of the Company’s capital stock, other equity securities, or securities convertible into equity would dilute the economic and voting rights of our existing stockholders, could reduce the market price of our common stock, or both. Debt securities convertible into equity could be subject to adjustments in the conversion ratio pursuant to which certain events may increase the number of equity securities issuable upon conversion. Preferred stock, if issued, could have a preference with respect to liquidating distributions or a preference with respect to dividend payments that could limit our ability to pay dividends to the holders of our common stock. The Company’s decision to issue securities in any future offering will depend on market conditions and other factors beyond our control, which may adversely affect the amount, timing, or nature of our future offerings. As a result, holders of the Company’s common stock bear the risk that the Company’s future offerings may reduce the market price of the Company’s common stock and dilute their percentage ownership.

We are offering Bonus Shares in our Regulation A Offering, which is effectively a discount on our stock price, to some investors who purchase Units in this Offering.

Certain investors who purchase Units in this Offering are entitled to receive additional shares of common stock (the “Bonus Shares”) that effectively provide a discount on price based on the amount invested. The number of Bonus Shares will be determined by the amount of money they invest in this Offering. These categories for Bonus Shares are non-cumulative and an investor will only be eligible for the category that offers the greatest number of Bonus Shares. Bonus Shares will effectively act as a discount to the price at which the Company is offering its stock. The maximum amount of Bonus Shares an investor may qualify for is 10%. For more details, including all of the Bonus Shares being offered, see Plan of Distribution. Consequently, the value of shares of investors who pay the full price or are entitled to a smaller amount of Bonus Shares in this Offering will be immediately diluted by investments made by investors entitled to the discount, who will pay less for their stake in the Company.

There is a risk of a loss of your investments.

There is no assurance that the Company’s activities will be profitable or that your investment in the Preferred Securities will be profitable. You may lose all of your investment.

There is an absence of a merit review of this offering.

No state or federal authority has reviewed the accuracy or adequacy of the information contained herein nor has any regulatory authority made a merit review of the offering or the terms of the Securities. Therefore, you must judge for yourself the adequacies of the disclosures, the pricing and fairness of the terms of the offering. This offering is being made in reliance on an exemption from registration contained in the Act and the rules and regulations thereunder, and on similar exemptions from the qualification provisions of applicable state securities laws. You must also recognize that they do not necessarily have any of the protections afforded by applicable federal and state securities laws as may be provided in registered and/or qualified offerings and therefore must judge the fairness of the terms of this Subscription and the adequacy and accuracy of the Memorandum without the benefit of prior review by any regulatory agency.

No Representation of Investors.

Each of the Investors acknowledges and agrees that counsel for the Company does not represent and shall not be deemed under the applicable codes of professional responsibility to have represented or to be representing any or all of the Investors in any respect.

19

No Broker Dealer.

Currently the Board has not engaged the services of a broker dealer and it is uncertain whether a broker dealer will be used for this Offering. Under federal securities laws, an independent broker-dealer is expected to take steps to ensure that the information contained in this Offering Circular is accurate and complete. The steps are typically taken by the “Managing Underwriter” or “Managing Dealer” who participates in the preparation of an offering memorandum. In addition, the Managing Dealer has certain duties related to an offering, including a duty to a prospective investor to ensure that an investment in a security is suitable for that prospective investor, a duty to conduct adequate due diligence with respect to the offering and a duty to comply with federal and state securities laws.

Although the Company has not engaged a Managing Dealer for this Offering, Clarity Partners, a business consulting firm and not a registered broker dealer, has performed an independent review and analysis of this Offering Circular. This offering will be conducted without a broker-dealer.

Forward-Looking Statements