AN OFFERING STATEMENT PURSUANT TO REGULATION A RELATING TO THESE SECURITIES HAS BEEN FILED WITH THE SECURITIES AND EXCHANGE COMMISSION. INFORMATION CONTAINED IN THIS PRELIMINARY OFFERING CIRCULAR IS SUBJECT TO COMPLETION OR AMENDMENT. THESE SECURITIES MAY NOT BE SOLD NOR MAY OFFERS TO BUY BE ACCEPTED BEFORE THE OFFERING STATEMENT FILED WITH THE COMMISSION IS QUALIFIED. THIS PRELIMINARY OFFERING CIRCULAR SHALL NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY NOR MAY THERE BE ANY SALES OF THESE SECURITIES IN ANY STATE IN WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE UNLAWFUL BEFORE REGISTRATION OR QUALIFICATION UNDER THE LAWS OF SUCH STATE. THE COMPANY MAY ELECT TO SATISFY ITS OBLIGATION TO DELIVER A FINAL OFFERING CIRCULAR BY SENDING YOU A NOTICE WITHIN TWO BUSINESS DAYS AFTER THE COMPLETION OF THE COMPANY’S SALE TO YOU THAT CONTAINS THE URL WHERE THE FINAL OFFERING CIRCULAR OR THE OFFERING STATEMENT IN WHICH SUCH FINAL OFFERING CIRCULAR WAS FILED MAY BE OBTAINED.

PRELIMINARY OFFERING CIRCULAR DATED MARCH 9, 2026

YSMD, LLC

(A DELAWARE SERIES LIMITED LIABILITY COMPANY)

745 5th Ave, Suite 500

New York, NY 10151

WWW.COLLABHOME.IO

| Series Interests Overview | ||||||||||||||||

| Price to Public | Underwriting Discounts and Commissions (1) | Proceeds to Issuer(2) | Proceeds to Other Persons | |||||||||||||

| Series A | Per Unit | $ | 5 | $ | 0.05 | $ | 4.95 | N/A | ||||||||

| Total Maximum | $ | 4,514,621 | $ | 45,146 | $ | 4,469,475 | N/A | |||||||||

| Series 2340 Hilgard | Per Unit | $ | 5 | $ | 0.05 | $ | 4.95 | N/A | ||||||||

| Total Maximum | $ | 2,402,400 | $ | 24,024 | $ | 2,378,376 | N/A | |||||||||

| Series Buttonwood 19-3 | Per Unit | $ | 5 | $ | 0.05 | $ | 4.95 | N/A | ||||||||

| Total Maximum | $ | 572,680 | $ | 5,727 | $ | 566,953 | N/A | |||||||||

| Series 33 Mine Street | Per Unit | $ | 5 | $ | 0.05 | $ | 4.95 | N/A | ||||||||

| Total Maximum | $ | 867,258 | $ | 8,673 | $ | 858,586 | N/A | |||||||||

| Series Buttonwood 21-2 | Per Unit | $ | 5 | $ | 0.05 | $ | 4.95 | N/A | ||||||||

| Total Maximum | $ | 559,091 | $ | 5,591 | $ | 553,500 | N/A | |||||||||

| (1) | The company has engaged Dalmore Group, LLC, member FINRA/SIPC (“Dalmore”), to perform administrative and compliance related functions in connection with this offering, but not for underwriting or placement agent services. This includes the 1% commission but it does not include the one-time expense allowance of $5,000, or consulting fees of $20,000 payable by the company to Dalmore. See “Plan of Distribution” for details. The company intends to distribute all offerings of Series Interests in any Series of the company through YSMD, LLC as described in greater detail under “Plan of Distribution.” |

| (2) | Because these are best efforts offerings, the actual public offering amounts, brokerage fees and proceeds to us are not presently determinable and may be substantially less than each total maximum offering set forth above. We will reimburse the Managing Member for Series offering expenses actually incurred in an amount up to 3% of gross proceeds, which we expect to allocate among all Series, including those created in the future, with commissions allocated directly to the Series Interests being sold in the offering. |

The minimum subscription per investor is 100 Series A Interests at $5.00 per Interest ($500), 20 Series 2340 Hilgard Interests at $5 per share ($100), 4 Series Buttonwood 19-3 Interests at $5.00 per Interest ($20), 60 Series 33 Mine Street Interests at $5.00 per share ($300) and 20 Series Buttonwood 21-2 Interests at $5.00 per share ($100).

Our company can offer up to $75 million within a rolling 12-month period pursuant to Regulation A. Our company intends to offer additional series within such limit and will file post qualification amendments for the offerings of such series with the U.S. Securities and Exchange Commission (the “Commission” or “SEC”). The offerings of such series will be made available to investors from the date such amendment is qualified by the Commission. There will be separate closings with respect to each offering. This offering will terminate at the earlier of (i) the date at which the maximum offering amount of all Series Interests has been sold, (ii) the date at which the offering is earlier terminated by the company, in our Managing Member’s sole discretion or (iii) the date that is three years from this offering being qualified by the SEC. Each Series Interests will be offered in an amount that, at the time the offering statement is qualified for such Series Interests, is reasonably expected to be offered and sold within two years from such initial qualification date.

At least every 12 months after this offering has been qualified by the SEC the company will file a post-qualification amendment to include the company’s recent financial statements. In addition, the company intends to periodically file a post-qualification amendment to include additional Series Interests to this offering. The company has engaged North Capital Private Securities Corporation as an escrow facilitator the “Escrow Facilitator” to hold funds tendered by investors.

THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OR GIVE ITS APPROVAL OF ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SOLICITATION MATERIALS. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION.

GENERALLY NO SALE MAY BE MADE TO YOU IN THIS OFFERING IF THE AGGREGATE PURCHASE PRICE YOU PAY IS MORE THAN 10% OF THE GREATER OF YOUR ANNUAL INCOME OR NET WORTH. DIFFERENT RULES APPLY TO ACCREDITED INVESTORS AND NON-NATURAL PERSONS. BEFORE MAKING ANY REPRESENTATION THAT YOUR INVESTMENT DOES NOT EXCEED APPLICABLE THRESHOLDS, THE COMPANY ENCOURAGES YOU TO REVIEW RULE 251(d)(2)(i)(C) OF REGULATION A. FOR GENERAL INFORMATION ON INVESTING, THE COMPANY ENCOURAGES YOU TO REFER TO www.investor.gov.

This offering is inherently risky. See “Risk Factors” on page 17.

The company is following the “Offering Circular” format of disclosure under Regulation A.

In the event that the company becomes a reporting company under the Securities Exchange Act of 1934, the company intends to take advantage of the provisions that relate to “Emerging Growth Companies” under the JOBS Act of 2012. See “Summary — Implications of Being an Emerging Growth Company.”

TABLE OF CONTENTS

2

In this Offering Circular, the terms “YSMD, LLC” “YSMD,” “we,” “us, “our,” the “company” and similar terms refer to YSMD, LLC, a Delaware Series Limited Liability Company; “Collab (USA) Capital LLC” and “Collab” refers to the Managing Member of YSMD, LLC.

THIS OFFERING CIRCULAR MAY CONTAIN FORWARD-LOOKING STATEMENTS AND INFORMATION RELATING TO, AMONG OTHER THINGS, THE COMPANY, ITS BUSINESS PLAN AND STRATEGY, AND ITS INDUSTRY. THESE FORWARD-LOOKING STATEMENTS ARE BASED ON THE BELIEFS OF, ASSUMPTIONS MADE BY, AND INFORMATION CURRENTLY AVAILABLE TO THE COMPANY’S MANAGEMENT. WHEN USED IN THE OFFERING MATERIALS, THE WORDS “ESTIMATE,” “PROJECT,” “BELIEVE,” “ANTICIPATE,” “INTEND,” “EXPECT” AND SIMILAR EXPRESSIONS ARE INTENDED TO IDENTIFY FORWARD-LOOKING STATEMENTS, WHICH CONSTITUTE FORWARD-LOOKING STATEMENTS. THESE STATEMENTS REFLECT MANAGEMENT’S CURRENT VIEWS WITH RESPECT TO FUTURE EVENTS AND ARE SUBJECT TO RISKS AND UNCERTAINTIES THAT COULD CAUSE THE COMPANY’S ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE CONTAINED IN THE FORWARD-LOOKING STATEMENTS. INVESTORS ARE CAUTIONED NOT TO PLACE UNDUE RELIANCE ON THESE FORWARD-LOOKING STATEMENTS, WHICH SPEAK ONLY AS OF THE DATE ON WHICH THEY ARE MADE. THE COMPANY DOES NOT UNDERTAKE ANY OBLIGATION TO REVISE OR UPDATE THESE FORWARD-LOOKING STATEMENTS TO REFLECT EVENTS OR CIRCUMSTANCES AFTER SUCH DATE OR TO REFLECT THE OCCURRENCE OF UNANTICIPATED EVENTS.

Implications of Being an Emerging Growth Company

The company is not subject to the ongoing reporting requirements of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) because the company is not registering its securities under the Exchange Act. Rather, the company will be subject to the more limited reporting requirements under Regulation A, including the obligation to electronically file:

| · | annual reports (including disclosure relating to our business operations for the preceding two fiscal years, or, if in existence for less than two years, since inception, related party transactions, beneficial ownership of the issuer’s securities, executive officers and directors and certain executive compensation information, management’s discussion and analysis (“MD&A”) of the issuer’s liquidity, capital resources, and results of operations, and two years of audited financial statements); |

| · | semiannual reports (including disclosure primarily relating to the issuer’s interim financial statements and MD&A); and |

| · | current reports for certain material events. |

In addition, at any time after completing reporting for the fiscal year in which the company’s offering statement was qualified, if the securities of each class to which this offering statement relates are held of record by fewer than 300 persons and offers or sales are not ongoing, the company may immediately suspend its ongoing reporting obligations under Regulation A.

3

If and when the company becomes subject to the ongoing reporting requirements of the Exchange Act, as an issuer with less than $1.07 billion in total annual gross revenues during its last fiscal year, it will qualify as an “emerging growth company” under the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) and this status will be significant. An emerging growth company may take advantage of certain reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies. In particular, as an emerging growth company, the company:

| · | will not be required to obtain an auditor attestation on its internal controls over financial reporting pursuant to the Sarbanes-Oxley Act of 2002; |

| · | will not be required to provide a detailed narrative disclosure discussing its compensation principles, objectives and elements and analyzing how those elements fit with its principles and objectives (commonly referred to as “compensation discussion and analysis”); |

| · | will not be required to obtain a non-binding advisory vote from its unit holders on executive compensation or golden parachute arrangements (commonly referred to as the “say-on-pay,” “say-on-frequency” and “say-on-golden-parachute” votes); |

| · | will be exempt from certain executive compensation disclosure provisions requiring a pay-for-performance graph and CEO pay ratio disclosure; |

| · | may present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations, or MD&A; and |

| · | will be eligible to claim longer phase-in periods for the adoption of new or revised financial accounting standards. |

The company intends to take advantage of all of these reduced reporting requirements and exemptions, including the longer phase-in periods for the adoption of new or revised financial accounting standards under Section 107 of the JOBS Act. The company’s election to use the phase-in periods may make it difficult to compare its financial statements to those of non-emerging growth companies and other emerging growth companies that have opted out of the phase-in periods under Section 107 of the JOBS Act.

Under the JOBS Act, the company may take advantage of the above-described reduced reporting requirements and exemptions for up to five years after its initial sale of common equity pursuant to a registration statement declared effective under the Securities Act of 1933, as amended, or such earlier time that the company no longer meets the definition of an emerging growth company. Note that this offering, while a public offering, is not a sale of common equity pursuant to a registration statement, since the offering is conducted pursuant to an exemption from the registration requirements. In this regard, the JOBS Act provides that the company would cease to be an “emerging growth company” if it has more than $1.07 billion in annual revenues, has more than $700 million in market value of its common stock held by non-affiliates, or issue more than $1 billion in principal amount of non-convertible debt over a three-year period.

Certain of these reduced reporting requirements and exemptions are also available to us due to the fact that the company may also qualify, once listed, as a “smaller reporting company” under the Commission’s rules. For instance, smaller reporting companies are not required to obtain an auditor attestation on their assessment of internal control over financial reporting; are not required to provide a compensation discussion and analysis; are not required to provide a pay-for-performance graph or CEO pay ratio disclosure; and may present only two years of audited financial statements and related MD&A disclosure.

4

The table below shows key information related to the offering of each Series, as of the date of this Offering Circular. Please also refer to “The Company’s Business – Property Overview” and “Use of Proceeds” for further details.

| Series Name | Underlying

Asset(s) | Offering

Price per Series Interest | Minimum Subscription per Investor | Maximum

Offering Size | Maximum

Series Interests (1) | Initial

Qualification Date (2) | Open

Date (3) | Closing

Date | Status | Number

of Securities Subscribed |

||||||||||||||||||

| Series A | 1742 Spruce Street, Berkeley, CA 94709 | $ | 5.00 | 100 Units ($500) | $ | 4,514,621 | 902,924 | [XX] | [XX] | [XX] | [XX] | [XX] | [XX] | |||||||||||||||

| Series 2340 Hilgard | 2340 Hilgard Ave, Berkeley, CA 94709 | $ | 5.00 | 20 Units ($100) | $ | 2,402,400 | 480,480 | [XX] | [XX] | [XX] | [XX] | [XX] | ||||||||||||||||

| Series Buttonwood 19-3 | 19 Buttonwood Street #3, Dorchester, MA 02125 | $ | 5.00 | 4 Units ($20) | $ | 572,680 | 114,536 | [XX] | [XX] | [XX] | [XX] | [XX] | ||||||||||||||||

| Series 33 Mine Street | 33 Mine Street, New Brunswick, NJ. 08901 | $ | 5.00 | 60 Units ($300) | $ | 867,258 | 173,452 | [XX] | [XX] | [XX] | [XX] | [XX] | ||||||||||||||||

| Series Buttonwood 21-2 | 21 Buttonwood Street #2, Dorchester, MA 02125 | $ | 5.00 | 20 Units ($100) | $ | 559,091 | 111,818 | [XX] | [XX] | [XX] | [XX] | [XX] | ||||||||||||||||

| (1) | For open offerings, each row states, with respect to the given offering, the minimum and maximum number of Series Interests offered. |

| (2) | For each offering, each row states, with respect to the given offering, the date on which the offering was initially qualified by the Commission. |

| (3) | For each offering, each row states, with respect to the given offering, the date on which offers and sales for such offering commenced. |

5

This summary highlights information contained elsewhere and does not contain all of the information that you should consider in making your investment decision. Before investing in the company’s Series Interests, you should carefully read this entire Offering Circular, including the company’s financial statements and related notes. You should also consider, among other information, the matters described under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

The Company

YSMD, LLC was organized as a series limited liability company in the State of Delaware on February 2, 2022. YSMD is an investment vehicle which intends to enable investors to own fractional ownership of a specific student housing rental property, but will also, under certain circumstances, consider multi-family and commercial real estate assets such as self-storage, warehouse and industrial, office, hospitality and retail properties. This lowers the cost-of-entry and minimizes the time commitment for real estate investing. An investment in the company entitles the investor to the potential economic and tax benefits normally associated with direct property ownership, while requiring no investor involvement in asset or property management. As of the date of this offering circular, no series of YSMD have been liquidated, and no prior program has been sponsored by YSMD resulting in any prior liquidation.

The company intends to establish separate Series for the holding of student housing rental properties to be acquired by the company. Notably, the debts, liabilities and obligations incurred, contracted for or otherwise existing with respect to a particular Series of the company will be enforceable against the assets of the applicable Series only, and not against the assets of the company. In addition, YSMD, through its manager, will manage all Underlying Assets related to the various Series including the sales of property, renting of the student housing rental property, maintenance and insurance.

It is not anticipated that any Series would own any assets other than its respective real estate property and associated assets, the reason for which the applicable Series was created (the “Underlying Asset(s)”), plus cash reserves for maintenance, storage, insurance and other expenses pertaining to such Underlying Assets and amounts earned by each Series from the monetization of the Underlying Asset. It is intended that owners of a Series Interest in a Series will only have assets, liabilities, profits and losses pertaining to the specific Underlying Assets owned by that Series, which would include the allocated portion of shared fees, costs and expenses which our Managing Member has allocated to such Series as discussed under “The Company’s Business – Allocations of Expenses.”

For example, an investor who acquires Series Interests in Series 2340 Hilgard and in Series Buttonwood 19-3 will only have assets, liabilities, profits and losses pertaining to the properties located at 2340 Hilgard Ave, Berkeley, CA 94709 (“2340 Hilgard”) and 19 Buttonwood Street #3, Dorchester, MA 02125 (“Buttonwood 19-3”), respectively.

Collab (USA) Capital LLC will serve as the property manager responsible for managing each Series’ Underlying Assets (the “Property Manager”) as described in the Property Management Agreements between Collab and the respective Series. However, YSMD in its sole discretion, may engage other third-party property managers to manage a Series’ Underlying Assets.

Collab (USA) Capital LLC will also serve as the managing member (the “Managing Member”) responsible for the day-to-day management of the company and each Series. Each Series may purchase the property from a third party or from an affiliate of the Managing Member, such as is the case with Series 2340 Hilgard and Series Buttonwood 19-3.

6

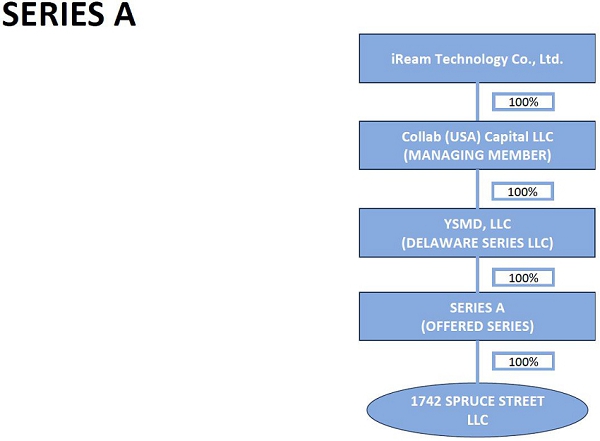

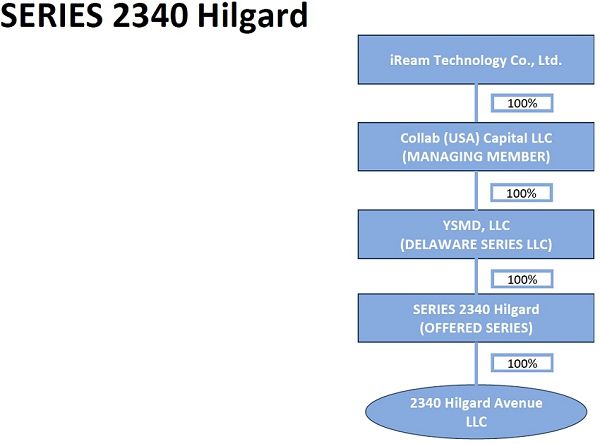

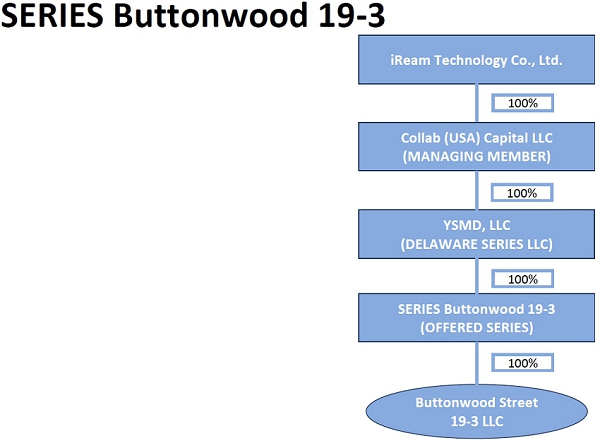

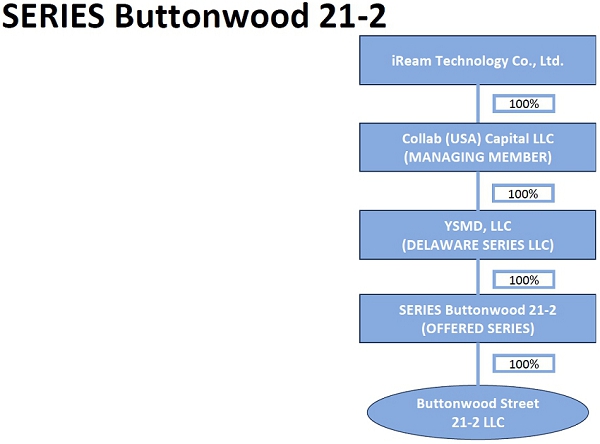

Our Series LLC Structure

Each property that we acquire will be owned by a separate series of our company that we will establish to acquire that property. As a Delaware series limited liability company, the debts, liabilities, obligations and expenses incurred, contracted for or otherwise existing with respect to a particular series are segregated and enforceable only against the assets of such series, as provided under Delaware law. This would include contractual obligations under the Property Management Agreement that each Series will enter into with respect to the management of the specific property. This would also include the portion of any shared fees, costs or expenses that have been allocated to the Series, as discussed above and under “The Company’s Business – Allocations of Expenses.”

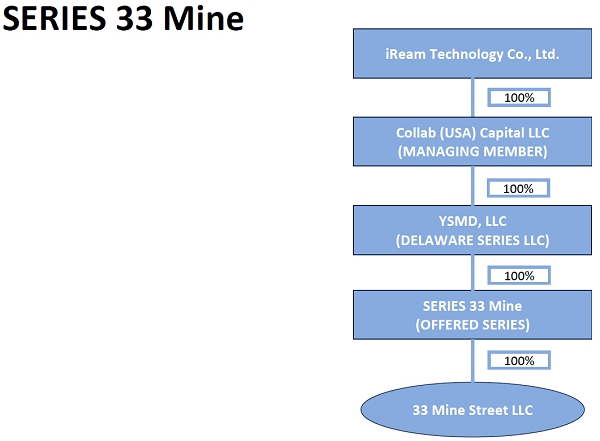

For ease of understanding the company’s business structure, we have included the organizational chart below:

7

8

1 iREAM Technology Co., Ltd. owns all of outstanding interests in Collab (USA) Capital LLC. Edrick Wang and Albert Wang, are the sons of Qian Wang, Collab’s CEO and Chairman, and indirectly own 64.67% of iREAM Technology Co., Ltd. (on a fully-diluted basis).

9

The company has been formed to invest in various real estate assets throughout the United States, with a focus on student housing. The Managing Member intends to initially search for properties located on the East and West coasts, but the company will not limit itself geographically. The company may invest in properties that are income producing in excess of their expenses; in other words, those properties that will produce positive cash flow immediately upon, or soon after, acquisition. The company may also invest in properties that need redevelopment, significant repositioning, or capital investments, known as value-add, and, thus, may not produce positive cash flow until the capital improvements are completed. It is expected that the company will focus on student housing and multi-family properties, but will also, under certain circumstances, consider commercial real estate assets such as self-storage, warehouse and industrial, office, hospitality, and retail properties.

Once the Managing Member identifies a property and agrees a price with the sellers, which may be an affiliate or the sole owner of the Managing Member, will enter into a purchase agreement for the property or the entity owning the property. Generally, YSMD expects to assign the contract to the relevant Series for the purchase of a specific property directly by the Series. However, there may be circumstances or timing considerations that result in YSMD or one of its wholly owned subsidiaries acquiring the property directly for further sale to the Series once sufficient funding has been obtained.

In cases where the Series purchases the property or the entity owning the property directly from a third party seller, it would use the proceeds of the offering for that Series to purchase the property or the entity owning the property and may finance a portion of the purchase price with mortgage or other third party financing. If the purchase agreement for the property or the entity owning the property does not include a financing condition, or the financing contingency has expired, and the closing for the property occurs prior to the closing of offering, YSMD or an affiliate may provide a loan to the Series, upon the terms described under “The Company’s Business – Intended Business Process” below, to finance all or part of the purchase price of the property or the entity owning the property that would be repaid with the proceeds of the offering. The remaining proceeds of the offering for a Series would be used by the Series first to fund any anticipated renovation costs and furnishing expenses for the property to prepare it for rent, if any, then to pay the sourcing fee to our Managing Member and the remainder held by the Series as operating reserves, depending on the amount raised in the offering for that Series.

10

If YSMD, one of its affiliates or sole owner of the Managing Member purchases the property directly, then, after the relevant Series has obtained sufficient financing, that Series would purchase the property or the entity owning the property for an amount equal to the original purchase price (including closing costs) plus holding costs, renovation costs and furnishing expenses actually incurred by YSMD prior to the sale to the Series. Any remaining proceeds from offering of such Series would be first allocated to pay the sourcing fee and any remaining proceeds of the offering for a Series would be used by the Series first to fund any anticipated renovation costs and furnishing expenses for the property to prepare it for rent, if any, then to pay the sourcing fee to our Managing Member and the remainder held by the Series as operating reserves, depending on the amount raised in the offering for that Series.

Distributions

We intend to distribute 100% of the Free Cash Flows of a Series, after reimbursing the Managing Member and the Property Manager for expenses incurred on behalf of a Series, plus accrued interest, and creating such reserves as the Managing Member deems necessary. A Series’ net income, and therefore, its Free Cash Flows, will be reduced by the expenses of that Series, including the following fees paid to our Managing Member and Property Manager, unless indicated in the relevant Series Designation or property management agreement:

| · | Property Management Fee: We generally seek to set these fees to be comparable to prevailing market rates for the management of student housing rental properties in the relevant geographic area. Currently these fees amount to 8% of the Gross Receipts of the Series. |

| · | Asset Management Fee: A quarterly fee of 0.5% (2% annually) of the Asset Value of the Series. |

| · | Sourcing Fee: Any portion of the sourcing fee for the Series that is not funded by the proceeds of the Series offering and that is booked as an expenses of the Series, at the company and Managing Member’s discretion. Please see “Use of Proceeds” for the sourcing fee applicable to each specific Series. |

We determined these fees internally without any independent assessment of comparable market fees. As a result, they may be higher than those available from unaffiliated third parties. After payment of all of the above fees, all other cash expenses and capital expenditures by the Series, it may not generate sufficient revenue to produce any Free Cash Flows or make distribution to investors.

Please see below and “Securities Being Offered – Distributions” for a more detailed discussion of the calculation of distributions to investors and the compensation paid to our Managing Member, as well as the defined terms used above.

No Series of YSMD has made any distributions to date.

Distribution Upon Liquidation of a Series

Subject to Article XI of the Operating Agreement and any Series Designation, any amounts available for distribution following the liquidation of a Series, net of any fees, costs and liabilities (as determined by the Managing Member in its sole discretion), shall be applied and distributed as follows:

| (a) | First, 100% to the Members (pro rata and which, for the avoidance of doubt, may include the Managing Member and its Affiliates if the Managing Member or any Affiliates acquired Interests or received Interests as a Sourcing Fee or otherwise) until the Members have received back 100% of their Capital Contribution; and |

11

| (b) | Second, 20% to the Managing Member and 80% to the Members (pro rata to their Interests and which, for the avoidance of doubt, may include the Managing Member and its Affiliates if the Managing Member or any Affiliates acquired Interests or received Interests as a Sourcing Fee or otherwise). |

No Series of YSMD has been liquidated to date.

Compensation Paid to our Managing Member

Each Series will pay the following fees:

Sourcing Fee: If a Series raises the maximum offering amount for that Series, a portion of the proceeds would be paid to our Managing Member as a sourcing fee, which is set forth in the Designation for the relevant Series and discussed under “Use of Proceeds” below. The sourcing fee represents a fee payable in connection with the search and negotiation of the property purchased. Our Managing Member determines this fee and sets the amount to equal up to 5% of the contractual purchase price of the relevant property acquired by the Series (but does not include capital expenditures or repair costs required to renovate and prepare the property for listing and rent, if any). To the extent that a Series raises less than the maximum offering amount resulting in insufficient funds to pay the sourcing fee, the company may choose to expense the balance of the sourcing fee, which would be deducted from revenues generated by the relevant property, or we may increase its investment in the relevant Series Interests to cover the balance of the sourcing fee.

Asset Management Fees: On a quarterly basis beginning on the first quarter end date following the initial closing date of the issuance of Series Interests, the Series shall pay the Managing Member an asset management fee, payable quarterly in arrears, equal to 0.5% (2% annualized) of Asset Value as of the last day of the immediately preceding quarter. “Asset Value” at any date means the fair market value of assets in a Series representing the purchase price that a willing buyer having all relevant knowledge would pay a willing seller for such assets in an arm’s length transaction, determined by the Managing Member in its sole discretion. We do not intend to obtain a third party valuation of the assets of each Series to determine “Asset Value.”

Property Management Fees: Each Series will pay, monthly, a property management fee to the Property Manager, who is initially is our Managing Member, equal to a percentage (as specified in the relevant Property Management Agreement) of the Gross Receipts received by the Series during the immediately preceding month. “Gross Receipts” means (i) receipts from the short-term or long-term rental of the Underlying Assets; (ii) receipts from rental escalations, late charges and/or cancellation fees (iii) receipts from tenants for reimbursable operating expenses; (iv) receipts from concessions granted or goods or services provided in connection with the Underlying Assets or to the tenants or prospective tenants; (v) other miscellaneous operating receipts; and (vi) proceeds from rent or business interruption insurance, excluding (A) tenants’ security or damage deposits until the same are forfeited by the person making such deposits; (B) property damage insurance proceeds; and (C) any award or payment made by any governmental authority in connection with the exercise of any right of eminent domain. See “The Company’s Business – Property Management Agreements.

Renovation Management Fees, If Any: If the Managing Member reasonably determines that capital improvements are required for a Series Property, then such Series will pay a renovation management fee, as applicable, to the Property Manager equal to 5.5% of the total capital improvement costs. Renovation management includes coordinating and facilitating the planning and the performance of the capital improvement projects.

Disposition Fees: Upon the disposition and sale of a Series Property, each Series will be charged a disposition fee equal to 2% of the disposition price. Disposition fees, include but are not limited to, property sale expenses such as brokerage commissions, and title, escrow and closing costs.

We and Collab determined these fees internally without any independent assessment of comparable market fees. As a result, they may be higher than those available from unaffiliated third parties.

12

Other Costs and Expenses

Each Series will bear all expenses of the applicable Underlying Asset, including fees, costs and expenses attributable to more than one Series and allocated among the relevant Series as discussed above. Because these are best efforts offerings, the actual public offering amounts, brokerage fees and proceeds to us are not presently determinable and may be substantially less than each total maximum offering set forth above. We will reimburse the Managing Member for Series offering expenses actually incurred in an amount up to 3% of gross proceeds.

Any fees, costs or expenses that are allocated among multiple Series will be equal, in the aggregate, to the amount actually incurred, without any mark-up. Once allocated, the portion of those fees, costs and expenses will become expenses and liabilities of the relevant Series and we would generally expect them to be paid out of the cash reserves or revenues of that Series in the ordinary course. If a Series does not have sufficient cash reserves and revenues to meet its operating expenses, YSMD, the Managing Member or one of their affiliates may loan funds to a Series to pay such expenses and charge a reasonable rate of interest. Under the Property Management Agreement of each Series, to the extent that the Property Manager of such Series incurs expenses on behalf of that Series, the Series will reimburse the Property Manager for any such expenses together with a reasonable rate of interest.

13

The Current Offering

| Securities Being Offered: |

We are offering the number of Series Interests of each Series at a price per Series Interest set forth in the “Series Offering Table” section above. Our Managing Member intends to own a minimum of 5%, although such minimum threshold may be waived or modified by our Managing Member in its sole discretion. Our Managing Member may sell these Series Interests at any time after the applicable closing.

Each Series of Series Interests is intended to be a separate Series of our company for purposes of assets and liabilities. See “Securities Being Offered” for further details. The Series Interests will be non-voting except with respect to certain matters set forth in our Amended and Restated Series Limited Liability Company Agreement of YSMD dated August 12, 2022, as amended from time to time (the “Operating Agreement”) including the Series Designation applicable to the Series. The purchase of Series Interests in a Series is an investment only in that Series of our company and not an investment in our company as a whole. | |

| Minimum and maximum subscription: | The minimum subscription by an investor is 100 Series A Interests at $5.00 per Interest ($500), 20 Series 2340 Hilgard Interests at $5.00 per Interest ($100), 4 Series Buttonwood 19-3 Interests at $5.00 per Interest ($20), 60 Series 33 Mine Street Interests at $5.00 and 20 Series Buttonwood 21-2 Interests at $5.00, respectively. The maximum subscription by any investor is for Series Interests representing 19.9% of the total Series Interests of a particular Series, although such minimum and maximum thresholds may be waived or modified by our Managing Member in its sole discretion. See “Plan of Distribution” for additional information. | |

| Use of Proceeds: | Net proceeds from the sale of Series Interests will be used to purchase the relevant Underlying Assets set forth in the “Series Offering Table” above, pay a sourcing fee to Collab, pay the brokerage commission, and to create a maintenance reserve for the applicable Underlying Assets. Our Managing Member initially bears all offering expenses, other than brokerage commissions, on behalf of each Series. See “Use of Proceeds” for further details. |

14

Selected Risks

The company’s business is subject to a number of risks and uncertainties, including those highlighted in the section titled “Risk Factors” immediately following this summary. These risks include, but are not limited to, the following:

| · | An investment in an offering constitutes only an investment in that Series offered and not in the company as a whole or any Underlying Assets. |

| · | If the company’s series limited liability company structure is not respected, then investors may have to share any liabilities of the company with all investors and not just those who hold the same Series Interests as them. |

| · | If YSMD fails to attract and retain Mr. Qian Wang, CEO of YSMD and the Managing Member’s CEO, or its key personnel, the company may not be able to achieve its anticipated level of growth and its business could suffer. |

| · | There is competition for time among the various entities sharing the same management team. |

| · | Each Series will rely on its Property Manager, Collab, to manage each property. |

| · | If we fail to manage our growth, we may not have access sufficient personnel and other resources to operate our business and our results, financial condition and ability to make distributions to investors may suffer. |

| · | The company has limited operating history for investors to evaluate. |

| · | Possible changes in federal tax laws make it impossible to give certainty to the tax treatment of any Series Interests. |

| · | The company’s financial statements include a going concern opinion. |

| · | If the company does not successfully dispose of real estate assets, you may have to hold your investment for an indefinite period. |

| · | Competition with other parties for real estate investments may reduce the company’s profitability. |

| · | The company’s real estate and real estate-related assets will be subject to the risks typically associated with real estate. |

| · | We face possible risks associated with natural disasters and the physical effects of climate change, which may include more frequent or severe storms, hurricanes, flooding, rising sea levels, shortages of water, droughts and wildfires, any of which could have a material adverse effect on our business, results of operations, and financial condition. |

| · | The underlying value and performance of any real estate asset will fluctuate with general and local economic conditions. |

| · | Our results of operations are subject to an annual leasing cycle, short lease-up period, seasonal cash flows, changing university admission and housing policies and other risks inherent in the student housing industry. |

| · | Competition and any increased affordability of multi-family homes could limit our ability to lease our apartments or maintain or increase rents, which may materially and adversely affect us, including our financial condition, cash flows, results of operations and growth prospects. |

| · | We face significant competition from university-owned on-campus student housing, from other off-campus student housing properties and from traditional multi-family housing located within close proximity to universities. |

15

| · | A decline in general economic conditions in the markets in which each property is located or in the United States generally could lead to a decrease lower rental rates in those markets. |

| · | Lawsuits may arise between the company and its tenants resulting in lower cash distributions to investors. |

| · | The costs of defending against claims of environmental liability, of complying with environmental regulatory requirements, of remediating any contaminated property or of paying personal injury or other damage claims could reduce the amounts available for distribution to the company’s investors. |

| · | Costs associated with complying with the Americans with Disabilities Act may decrease cash available for distributions. |

| · | We may incur significant costs complying with other regulations. |

| · | Uninsured losses relating to real property or excessively expensive premiums for insurance coverage could reduce the company’s cash flows and the return on investment. |

| · | You may not receive Distributions on predictable schedule and may never receive any Distributions. |

| · | Rising expenses could reduce cash flow and funds available for future investments. |

| · | Due to economic conditions, local real estate conditions and competition for properties, the real estate we invest in may not appreciate or may decrease in value |

| · | Future pandemics, like what was experienced with the COVID-19 pandemic, and government restrictions adopted in response thereto, could significantly impact the ability of our tenants to pay rent, impede the performance of our properties, and harm our financial condition. |

| · | The company may not raise sufficient funds to achieve its business objectives. |

| · | The company’s management has full discretion as to the use of proceeds from the offering. |

| · | There is currently no trading market for the Series Interests. |

| · | The purchase price for the Series Interests has been arbitrarily determined. |

| · | The company’s Operating Agreement and Subscription Agreement each include a forum selection provision, which could result in less favorable outcomes to the plaintiff(s) in any action against the company. |

| · | Investors in this offering may not be entitled to a jury trial with respect to claims arising under the Subscription Agreement or Operating Agreement, which could result in less favorable outcomes to the plaintiff(s) in any action under these Agreements. |

16

The SEC requires the company to identify risks that are specific to its business and its financial condition. The company is still subject to all the same risks that all companies in its business, and all companies in the economy, are exposed to. These include risks relating to economic downturns, political and economic events and technological developments (such as cyber-attacks and the ability to prevent those attacks). Additionally, early-stage companies are inherently more risky than more developed companies. You should consider general risks as well as specific risks when deciding whether to invest.

Risks Relating to the Structure, Operation and Performance of the Company

An investment in an offering constitutes only an investment in that Series offered and not in the company as a whole or any Underlying Assets. A purchase of Series Interests in a Series does not constitute an investment in either the company as a whole or any Underlying Assets directly, or in any other Series Interest. This results in limited voting rights of the investor, which are solely related to a particular Series, and are further limited by the Operating Agreement, of the company, described further herein. Investors will have limited voting rights. Thus, the Managing Member and the Property Manager retain significant control over the management of the company and the Underlying Assets.

Furthermore, because the Series Interests in a Series do not constitute an investment in the company as a whole, holders of the Series Interests in a Series are not expected to receive any economic benefit from, or be subject to the liabilities of, the assets of any other Series. In addition, the economic interest of a holder in a Series will not be identical to owning a direct undivided interest in any Underlying Assets because, among other things, a Series will be required to pay corporate taxes before distributions are made to the holders, and the Property Manager will receive a fee in respect of its management of the Property.

Liability of investors between Series. The company is structured as a Delaware series limited liability company that issues separate Series Interests for specific properties. Each Series will merely be a separate Series and not a separate legal entity. Under the Delaware Limited Liability Company Act (the “LLC Act”), if certain conditions (as set forth in Section 18-215(b) of the LLC Act) are met, the liability of investors holding Series Interests in one Series is segregated from the liability of investors holding Series Interests in another Series and the assets of one Series are not available to satisfy the liabilities of other Series.

Although this limitation of liability is recognized by the courts of Delaware, there is no guarantee that if challenged in the courts of another U.S. State or a foreign jurisdiction, such courts will uphold a similar interpretation of Delaware corporation law, and in the past certain jurisdictions have not honored such interpretation.

If the company’s series limited liability company structure is not respected, then investors may have to share any liabilities of the company with all investors and not just those who hold the same Series Interests as them and account for them separately and otherwise meet the requirements of the LLC Act, it is possible a court could conclude that the methods used did not satisfy Section 18-215(b) of the LLC Act and thus potentially expose the assets of a Series to the liabilities of another Series. The consequence of this is that investors may have to bear higher than anticipated expenses which would adversely affect the value of their Series Interests or the likelihood of any distributions being made by a particular Series to its investors.

In addition, the company is not aware of any court case that has tested the limitations on inter-series liability provided by Section 18-215(b) in federal bankruptcy courts and it is possible that a bankruptcy court could determine that the assets of one Series should be applied to meet the liabilities of the other Series or the liabilities of the company generally where the assets of such other Series or of the company generally are insufficient to meet its liabilities.

If any fees, costs and expenses of the company are not allocable to a specific Series, they will be borne proportionately across all of the Series (which may include future Series to be issued). Although the Managing Member will allocate fees, costs and expenses acting reasonably and in accordance with its allocation policy (see “Description of the Business – Allocations of Expenses” section), there may be situations where it is difficult to allocate fees, costs and expenses to a specific Series and therefore, there is a risk that a Series may bear a proportion of the fees, costs and expenses for a service or product for which another Series received a disproportionately high benefit.

17

If Collab (USA) Capital LLC, our Managing Member fails to attract and retain Mr. Qian Wang, CEO of YSMD and our Managing Member’s CEO, or its key personnel, the company may not be able to achieve its anticipated level of growth and its business could suffer. The Managing Member’s and the company’s future depends, in part, on Collab’s ability to attract and retain key personnel. Its future also depends on the continued contributions of Mr. Wang. Mr. Wang implemented the company’s strategy to identify and invest in multi-family properties. Mr. Wang is critical to the management of the Managing Member’s and the company’s business and operations and the development of its strategic direction. The loss of the services of Mr. Wang’s would involve significant time and expense and may significantly delay or prevent the achievement of the company’s business objectives.

There is competition for time among the various entities sharing the same management team. Currently, Collab (USA) Capital LLC is the Managing Member of YSMD and each Series and is the Property Manager for this Series. YSMD expects to create more Series in the future as additional attractive student rental properties are identified. It is foreseeable that at certain times the various Series will be competing for time from the management team.

Each Series will rely on its Property Manager to manage each property. Following the acquisition of any property, the property may be managed by Collab Capital (USA) LLC. In addition, any Property Manager will be entitled to certain fees in exchange for its day-to-day operations of each property. Any compensation arrangements if Collab Capital (USA) LLC serves as the Property Manager, will be determined by YSMD sitting on both sides of the table and will not be an arm’s length transaction.

If we fail to manage our growth, we may not have access sufficient personnel and other resources to operate our business and our results, financial condition and ability to make distributions to investors may suffer. We intend to establish additional Series and acquire additional student rental properties in the future. As we do so, we will be increasingly reliant on the resources of YSMD and the Property Manager to manage our properties and our company. Currently, the company has no staff and the Managing Member operates with a small staff of three full time employees and three part time employees and may need to hire additional staff. If its resources are not adequate to manage our properties effectively, our results, financial condition and ability to make distributions to investors may suffer.

You will have limited control over changes in our policies and operations, which increases the uncertainty and risks you face as a Member. Our Managing Member determines our major policies, including our policies regarding financing, growth and debt capitalization. Our Managing Member may amend or revise these and other policies without a vote of the Members. Our Managing Member’s broad discretion in setting policies and our Members’ inability to exert control over those policies increases the uncertainty and risks you face as a Member.

Our ability to make distributions to our Members is subject to fluctuations in our financial performance, operating results and capital improvement requirements. Currently, our strategy includes paying a distribution at least monthly to investors in the event of positive Free Cash Flow from operation of the Property. In the event of downturns in our operating results, unanticipated capital improvements to the Property, or other factors, we may be unable, or may decide not to pay distributions to our Members. The timing and amount of distributions are the sole discretion of our Managing Member who will consider, among other factors, our financial performance, any debt service obligations, any debt covenants, and capital expenditure requirements. We cannot assure you that we will generate sufficient cash in order to pay distributions.

The company has limited operating history for investors to evaluate. The company and this Series were recently formed and have not generated any revenues and have no operating history upon which prospective investors may evaluate their performance. No guarantee can be given that the company or any Series will achieve their investment objectives, the value of any properties will increase or that any Properties will be successfully monetized.

18

Possible changes in federal tax laws make it impossible to give certainty to the tax treatment of any Series Interests. The Internal Revenue Code (the “Code”) is subject to change by Congress, and interpretations of the Code may be modified or affected by judicial decisions, by the Treasury Department through changes in regulations and by the Internal Revenue Service through its audit policy, announcements, and published and private rulings. Although significant changes to the tax laws historically have been given prospective application, no assurance can be given that any changes made in that law affecting an investment in any Series of the company would be limited to prospective effect.

For instance, prior to effectiveness of the Tax Cuts and Jobs Act of 2017, an exchange of the Series Interests of one Series for another might have been a non-taxable ‘like-kind exchange’ transaction, while transactions would only qualify for that treatment with respect to real property. Accordingly, the ultimate effect on an investor’s tax situation may be governed by laws, regulations or interpretations of laws or regulations which have not yet been proposed, passed or made, as the case may be.

The company’s financial statements include a going concern opinion. Our financial statements have been prepared assuming the company will continue as a going concern. We are newly formed and have not generated revenue from operations. We will require additional capital until revenue from operations are sufficient to cover operational costs. There are no assurances that we will be able to raise capital on acceptable terms. If we are unable to obtain sufficient amounts of additional capital, we may be required to reduce the scope of our planned development and operations, which could harm our business, financial condition and operating results. Therefore, there is substantial doubt about the ability of the company to continue as a going concern.

If the company does not successfully dispose of real estate assets, you may have to hold your investment for an indefinite period. The determination of whether to dispose of the Property is entirely at the discretion of the company. Even if the company decides to dispose of such real estate assets, the company cannot guarantee that it will be able to dispose of them at a favorable price to investors.

Competition with other parties for real estate investments may reduce the company’s profitability. The company will compete with other entities engaged in real estate investment for the acquisition or sale of properties, including financial institutions, many of which have greater resources than the company. Larger entities may enjoy significant competitive advantages that result from, among other things, a lower cost of capital. Such competition could make it more difficult for the company to obtain future funding, which could affect the company’s growth.

Risks Related to the Real Estate Industry

Our performance and value are subject to risks associated with real estate assets and with the real estate industry.

Our ability to satisfy our financial obligations and make expected distributions to our Members depends on our ability to generate cash revenues in excess of expenses and capital expenditure requirements. Events and conditions generally applicable to owners and operators of real property that are beyond our control may decrease cash available for distribution and the value of the Property. These events include:

| · | general economic conditions; |

| · | rising level of interest rates; |

| · | local oversupply, increased competition or reduction in demand for student housing; |

| · | inability to collect rent from tenants; |

| · | vacancies or our inability to rent beds on favorable terms; |

| · | inability to finance property development on favorable terms; |

| · | increased operating costs, including insurance premiums, utilities, and real estate taxes; |

| · | costs of complying with changes in governmental regulations; |

| · | decreases in student enrollment at particular colleges and universities; |

| · | changes in university policies related to admissions and housing; and |

| · | changing student demographics. |

In addition, periods of economic slowdown or recession, rising interest rates or declining demand for real estate, or the public perception that any of these events may occur, could result in a general decline in rents or an increased incidence of defaults under existing leases, which would adversely affect us.

19

We face possible risks associated with natural disasters and the physical effects of climate change, which may include more frequent or severe storms, hurricanes, flooding, rising sea levels, shortages of water, droughts and wildfires, any of which could have a material adverse effect on our business, results of operations, and financial condition. To the extent climate change causes changes in weather patterns, our coastal destinations could experience increases in storm intensity and rising sea-levels causing damage to our properties and result in reduced rentals at these properties. Climate change may also affect our business by increasing the cost of, or making unavailable, property insurance on terms we find acceptable in areas most vulnerable to such events, increasing operating costs, including the cost of water or energy, and requiring us to expend funds to repair and protect our properties in connection with such events. Any of the foregoing could have a material adverse effect on our business, results of operations, and financial condition.

The underlying value and performance of any real estate asset will fluctuate with general and local economic conditions. The successful operation of any real estate asset is significantly related to general and local economic conditions. Periods of economic slowdown or recession, significantly rising interest rates, declining employment levels, decreasing demand for student rentals, declining real estate values, or the public perception that any of these events may occur, can result in reductions in the underlying value of any asset and result in poor economic performance. In such cases, investors may lose the full value of their investment, or may not experience any distributions from the real estate asset.

Our results of operations are subject to an annual leasing cycle, short lease-up period, seasonal cash flows, changing university admission and housing policies and other risks inherent in the student housing industry. We generally lease our owned properties under 12-month leases, and in certain cases, under nine-month or shorter-term semester leases. As a result, we may experience significantly reduced cash flows during the summer months at properties with lease terms shorter than 12 months. Furthermore, all of our properties must be entirely re-leased each year during a limited leasing season that usually begins in January and ends in August of each year. We are therefore highly dependent on the effectiveness of our marketing and leasing efforts and personnel during this season, exposing us to significant leasing risk.

Changes in university admission policies could adversely affect us. For example, if a university reduces the number of student admissions or requires that a certain class of students, such as freshman, live in a university-owned facility, the demand for beds at our properties may be reduced and our occupancy rates may decline. While we may engage in marketing efforts to compensate for such change in admission policy, we may not be able to effect such marketing efforts prior to the commencement of the annual lease-up period or our additional marketing efforts may not be successful.

Competition and any increased affordability of multi-family homes could limit our ability to lease our apartments or maintain or increase rents, which may materially and adversely affect us, including our financial condition, cash flows, results of operations and growth prospects. The multi-family industry is highly competitive, and we face competition from many sources, including from other multi-family apartment communities both in the immediate vicinity and the geographic market where our properties are and will be located. This could increase the number of apartments units available and may decrease occupancy and unit rental rates. Furthermore, multi-family apartment communities we invest in compete, or will compete, with numerous housing alternative in attracting residents, including owner occupied single and multi-family homes available to rent or purchase. The number of competitive properties and/or condominiums in a particular area, or any increased affordability of owner occupied single and multi-family homes caused by declining housing prices, mortgage interest rates and government programs to promote home ownership, could adversely affect our ability to retain our residents, lease apartment units and maintain or increase rental rates. These factors could materially and adversely affect us.

20

We face significant competition from university-owned on-campus student housing, from other off-campus student housing properties and from traditional multi-family housing located within close proximity to universities. On-campus student housing has certain inherent advantages over off-campus student housing in terms of physical proximity to the university campus and integration of on-campus facilities into the academic community. Colleges and universities can generally avoid real estate taxes and borrow funds at lower interest rates than us and other private sector operators. We also compete with national and regional owner-operators of off-campus student housing in a number of markets as well as with smaller local owner-operators.

Currently, the industry is fragmented with no participant holding a significant market share. There are a number of student housing complexes that are located near or in the same general vicinity of the Property and that compete directly with us. Such competing student housing complexes may be newer than our properties, located closer to campus, charge less rent, possess more attractive amenities or offer more services or shorter term or more flexible leases.

Rental income at a particular property could also be affected by a number of other factors, including the construction of new on-campus and off- campus residences, increases or decreases in the general levels of rents for housing in competing communities, increases or decreases in the number of students enrolled at one or more of the colleges or universities in the market of the property and other general economic conditions.

We believe that a number of other companies with substantial financial and marketing resources may be potential entrants in the student housing business. The entry of one or more of these companies could increase competition for students and for the acquisition, development and management of other student housing properties.

A decline in general economic conditions in the markets in which each property is located or in the United States generally could lead to a lower rental rates in those markets. As a result of this trend, the company may reduce revenue, potentially resulting in losses and lower resale value of properties, which may reduce your return.

Lawsuits may arise between the company and its tenants resulting in lower cash distributions to investors. Disputes between landlords and tenants are common. These disputes may escalate into legal action from time to time. In the event a lawsuit arises between the company and a tenant it is likely that the company will see an increase in costs. Accordingly, cash distributions to investors may be affected.

The costs of defending against claims of environmental liability, of complying with environmental regulatory requirements, of remediating any contaminated property or of paying personal injury or other damage claims could reduce the amounts available for distribution to the company’s investors. Under various federal, state and local environmental laws, ordinances and regulations, a current or previous real property owner or operator may be liable for the cost of removing or remediating hazardous or toxic substances on, under or in such property. These costs could be substantial. Such laws often impose liability whether or not the owner or operator knew of, or was responsible for, the presence of such hazardous or toxic substances. Environmental laws also may impose liens on property or restrictions on the manner in which property may be used or businesses may be operated, and these restrictions may require substantial expenditures or prevent us renting the property. Environmental laws provide for sanctions for noncompliance and may be enforced by governmental agencies or, in certain circumstances, by private parties. Certain environmental laws and common law principles could be used to impose liability for the release of and exposure to hazardous substances, including asbestos-containing materials and lead-based paint. Third parties may seek recovery from real property owners or operators for personal injury or property damage associated with exposure to released hazardous substances and governments may seek recovery for natural resource damage. The costs of defending against claims of environmental liability, of complying with environmental regulatory requirements, of remediating any contaminated property, or of paying personal injury, property damage or natural resource damage claims could reduce or eliminate the amounts available for distribution to Members.

Costs associated with complying with the Americans with Disabilities Act may decrease cash available for distributions. Each Property may be subject to the Americans with Disabilities Act of 1990, as amended, or the ADA. Under the ADA, all places of public accommodation are required to comply with federal requirements related to access and use by disabled persons. The ADA has separate compliance requirements for “public accommodations” and “commercial facilities” that generally require that buildings and services be made accessible and available to people with disabilities. The ADA’s requirements could require removal of access barriers and could result in the imposition of injunctive relief, monetary penalties or, in some cases, an award of damages. Any funds used for ADA compliance will reduce the company’s net income and the amount of cash available for distributions to investors.

We may incur significant costs complying with other regulations. Each Property is subject to various federal, state and local regulatory requirements, such as state and local fire and life safety requirements. If we fail to comply with these various requirements, we might incur governmental fines or private damage awards. Furthermore, existing requirements could change and require us to make significant unanticipated expenditures that would materially and adversely affect us.

21

Uninsured losses relating to real property or excessively expensive premiums for insurance coverage could reduce the company’s cash flows and the return on investment. There are types of losses, generally catastrophic in nature, such as losses due to wars, acts of terrorism, earthquakes, floods, hurricanes, pollution or environmental matters, that are uninsurable or not economically insurable, or may be insured subject to limitations, such as large deductibles or co-payments. Insurance risks associated with potential acts of terrorism could sharply increase the premiums the company pays for coverage against property and casualty claims. Additionally, to the extent the company finances the acquisition of a Property, mortgage lenders in some cases insist that property owners purchase coverage against flooding as a condition for providing mortgage loans. Such insurance policies may not be available at reasonable costs, which could inhibit the company’s ability to finance or refinance its properties if so required. In such instances, the company may be required to provide other financial support, either through financial assurances or self-insurance, to cover potential losses. The company may not have adequate coverage for such losses. If any of the properties incur a casualty loss that is not fully insured, the value of the assets will be reduced by any such uninsured loss, which may reduce the value of investor interests. In addition, other than any working capital reserve or other reserves the company may establish, the company has no additional sources of funding to repair or reconstruct any uninsured property. Also, to the extent the company must pay unexpectedly large amounts for insurance, it could suffer reduced earnings that would result in lower distributions to investors.

Risks Related to Our Properties, Our Markets and Our Business

We are a newly formed company organized on February 2, 2022 and have not yet acquired properties or commenced our principal operations, which makes an evaluation of us extremely difficult. At this stage of our business operations, even with our good faith efforts, we may never become profitable or generate any significant amount of revenues, thus potential investors have a possibility of losing their investment. We were organized on February 2, 2022 and have not yet started operations. As a result of our start-up status we (i) have generated no revenues, (ii) will accumulate deficits due to organizational and start-up activities, business plan development, and professional fees since we organized. There is nothing at this time on which to base an assumption that our business operations will prove to be successful or that we will ever be able to operate profitably. Our future operating results will depend on many factors, including our ability to raise adequate working capital, availability of properties for purchase, the level of our competition and our ability to attract and maintain key management and employees.

You may not receive Distributions on predictable schedule and may never receive any Distributions. Distributions will only be available to the extent there is cash flow from rentals and other operations of the properties and other investments in excess of Company expenses. Therefore, there can be no assurance as to when or whether there will be any Cash Distributions from the Company to the Members.

The profitability of the properties is uncertain. We intend to invest in properties selectively. Investment in properties entails risks that investments will fail to perform in accordance with expectations. In undertaking these investments, we will incur certain risks, including the expenditure of funds on, and the devotion of management’s time to, transactions that may not come to fruition. Additional risks inherent in investments include risks that the properties will not achieve anticipated rents or occupancy levels and that estimated operating expenses may prove inaccurate.

Rising expenses could reduce cash flow and funds available for future investments. Our properties will be subject to increases in real estate tax rates, utility costs, operating expenses, insurance costs, repairs and maintenance, administrative and other expenses. If we are unable to increase rents at an equal or higher rate or lease properties on a basis requiring the tenants to pay all or some of the expenses, we would be required to pay those costs, which could adversely affect funds available for future distributions to Members.

22

Due to economic conditions, local real estate conditions and competition for properties, the real estate we invest in may not appreciate or may decrease in value. A multi-family or commercial property's income and value may be adversely affected by national and regional economic conditions, local real estate conditions such as an oversupply of properties or a reduction in demand for properties, competition from other similar properties, our ability to provide adequate maintenance, insurance and management services, increased operating costs (including real estate taxes), the attractiveness and location of the property and changes in market rental rates. Our income will be adversely affected if a significant number of tenants are unable to pay rent or if our properties cannot be rented on favorable terms. Our performance is linked to economic conditions in the regions where the Property is located and in the market for multi-family space generally. Therefore, to the extent that there are adverse economic conditions in those regions, and in these markets generally, that impact the applicable market rents, such conditions could result in a reduction of our income and cash available for distributions and thus affect the amount of distributions we can make to Members.

We may be unable to renew, repay or refinance our outstanding debt. We are subject to the risk that our indebtedness will not be able to be renewed, repaid or refinanced when due or that the terms of any renewal or refinancing will not be as favorable as the existing terms of such indebtedness. If we were unable to refinance our indebtedness on acceptable terms, or at all, we might be forced to dispose of the Property on disadvantageous terms, which might result in losses to us. Such losses could have a material adverse effect on us and our ability to make distributions to our equity holders and pay amounts due on our debt.

Changes in laws could affect our business. We are generally not able to pass through to our residents under existing leases real estate taxes, income taxes or other taxes. Consequently, any such tax increases may adversely affect our financial condition and limit our ability to satisfy our financial obligations and make distributions to security holders. Changes that increase our potential liability under environmental laws or our expenditures on environmental compliance could have the same impact.

A cybersecurity incident and other technology disruptions could negatively impact our business, our relationships and our reputation. We use computers in substantially all aspects of our business operations. We also use mobile devices, social networking and other online activities to connect with our employees, suppliers and our residents. Such uses give rise to cybersecurity risks, including security breach, espionage, system disruption, theft and inadvertent release of information. Our business involves the storage and transmission of numerous classes of sensitive and/or confidential information and intellectual property, including residents' personal information, private information about employees, and financial and strategic information about us. As our reliance on technology increases, so have the risks posed to our systems, both internal and those we have outsourced to third party service providers. In addition, information security risks have generally increased in recent years due to the rise in new technologies and the increased sophistication and activities of perpetrators of cyberattacks. The theft, destruction, loss, misappropriation or release of sensitive and/or confidential information or intellectual property, or interference with our information technology systems or the technology systems of third-parties on which we rely, could result in business disruption, negative publicity, brand damage, violation of privacy laws, loss of residents, potential liability and competitive disadvantage, any of which could result in a material adverse effect on financial condition or results of operations.

Pandemics, like the COVID-19 pandemic, and government restrictions adopted in response thereto, could significantly impact the ability of our tenants to pay rent, impede the performance of our properties, and harm our financial condition. The United States, like the rest of the world, was adversely affected by the breakout of the COVID-19 virus, and the occurrence of future pandemics cannot be predicted. In the event of a future pandemic, the United States government, many states, and cities may institute "shelter in place" orders and adopt other restrictions which may cause the shuttering of many businesses and multiple layoffs, which may affect the income and, ultimately, the ability of tenants to pay rent. In addition, property owners may become subject of certain restrictions, such as a temporary moratorium on evictions, which may limit the company’s ability to respond to tenant defaults. These factors, and any other responses to a pandemic, may impede the operations of our properties and could significantly harm our financial condition and operating results.

Risks Related to the Offering

The company may not raise sufficient funds to achieve its business objectives. As identified in the Series Offering Table, for certain Series of the company, there is no minimum amount required to be raised before the company can accept your subscription for the Series Interests, and it can access the funds immediately. The company may not raise an amount sufficient for it to meet all of its objectives, including acquiring the Property. Once the company accepts your investment funds, there will be no obligation to return your funds. Even if other Series Interests are sold, there may be insufficient funds raised through this offering to cover the expenses associated with the offering or complete the purchase of the Property and the development and implementation of the company’s operations. The lack of sufficient funds to pay expenses and for working capital will negatively impact the company’s ability to implement and complete its planned use of proceeds.

23

The company’s management has full discretion as to the use of proceeds from the offering. The company presently anticipates that the net proceeds from the offering will be used by us to purchase the Property and as general working capital. The company reserves the right, however, to use the funds from the offering for other purposes not presently contemplated herein but which are related directly to growing its current business. As a result of the foregoing, purchasers of the Series Interests hereby will be entrusting their funds to the company’s management, upon whose judgment and discretion the investors must depend, with only limited information concerning management’s specific intentions.

An investment in the Interests is highly illiquid. You may never be able to sell or otherwise dispose of your Series Interests. Since there is no public trading market for our Interests, you may never be able to liquidate your investment or otherwise dispose of your Series Interests. Potential investors should note that the Operating Agreement does not compel the Managing Member to sell all the properties, and thus, there is a risk that an investor may remain in the company indefinitely. Therefore, you should expect to keep your investment in Series Interests indefinitely.

There is no current market for the Series Interests. There is no formal marketplace for the resale of the Series Interests. These Series Interests are illiquid and there will not be an official current price for them, as there would be if the company were a publicly-traded company with a listing on a stock exchange. Investors should assume that they may not be able to liquidate their investment or be able to pledge their Series Interests as collateral. Since the company has not established a trading forum for the Series Interests, there will be no easy way to know what the Series Interests are worth at any time.

The purchase price for the Series Interests has been arbitrarily determined. The purchase price for the Series Interests has been arbitrarily determined by the company and bears no relationship to the company’s assets, book value, earnings or other generally accepted criteria of value. In determining pricing, the company considered factors such as the purchase and holding costs of the Property, the company’s limited financial resources, the nature of its assets, estimates of its business potential, the degree of equity or control desired to be retained by Managing Member and general economic conditions.