AN OFFERING STATEMENT PURSUANT TO REGULATION A RELATING TO THESE SECURITIES HAS BEEN FILED WITH THE SECURITIES AND EXCHANGE COMMISSION. INFORMATION CONTAINED IN THIS PRELIMINARY OFFERING CIRCULAR IS SUBJECT TO COMPLETION OR AMENDMENT. THESE SECURITIES MAY NOT BE SOLD NOR MAY OFFERS TO BUY BE ACCEPTED BEFORE THE OFFERING STATEMENT FILED WITH THE COMMISSION IS QUALIFIED. THIS PRELIMINARY OFFERING CIRCULAR SHALL NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY NOR MAY THERE BE ANY SALES OF THESE SECURITIES IN ANY STATE IN WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE UNLAWFUL BEFORE REGISTRATION OR QUALIFICATION UNDER THE LAWS OF SUCH STATE. THE COMPANY MAY ELECT TO SATISFY ITS OBLIGATION TO DELIVER A FINAL OFFERING CIRCULAR BY SENDING YOU A NOTICE WITHIN TWO BUSINESS DAYS AFTER THE COMPLETION OF THE COMPANY’S SALE TO YOU THAT CONTAINS THE URL WHERE THE FINAL OFFERING CIRCULAR OR THE OFFERING STATEMENT IN WHICH SUCH FINAL OFFERING CIRCULAR WAS FILED MAY BE OBTAINED.

PRELIMINARY OFFERING CIRCULAR - DATED SEPTEMBER 15, 2025

SUBJECT TO COMPLETION

MIDORI GROUP INC.

Registrant’s principal address: # 5 Hazelton Ave. Suite 400, Toronto, Ontario Canada, M5R 2E1

Registrant’s telephone number, including area code: 289-242-5623

Registrant’s website: www.midori-bio.com

Midori Group Inc. (herein referred to as “Midori,” “we,” “us,” “our,” and the “Company”) is offering up to 20,000,000 shares of our common stock (the “Shares”) at $1.00 per share, for gross proceeds from the sale of Shares of up to $20,000,000 (“Maximum Offering Amount”). To offset some of the transactional expenses associated with this offering, we will charge investors a fee equal to 3% (“Investor Processing Fee”) of their subscription amounts (i.e. $3 for every $100 invested), effectively increasing the maximum offering amount by $600,000, to $20,600,000. The minimum investment established for each investor is $1,000 in Shares plus a $30 Investor Processing Fee. For more information on the securities offered hereby, please see the item titled “Securities Being Offered” on page 40.

Shares are being offered on a “best efforts” basis. The sale of Shares will commence within two days from the date this Offering Circular, as amended from time-to-time, is qualified by the Securities and Exchange Commission (“SEC”). This offering will terminate at the earlier to occur of: (i) all Shares offered hereby being sold, (ii) the date three years from the date this Offering Circular, as amended, is qualified with the SEC, or (iii) such earlier date as determined by the Company. Notwithstanding the foregoing, the Company believes that it may reasonably complete this offering within two years from this Offering Circular, as amended, being qualified.

| Price of common stock | Price to Public [1] | Underwriting Discount and Commissions [2] | Proceeds to Issuer [3] | |||||||||

| Per Share(4) | $ | 1.00 | 0.045 | 0.955 | ||||||||

| Investor Processing Fee(4) | $ | 0.03 | 0.00135 | 0.02865 | ||||||||

| Total Maximum(4) | $ 20,600,000 .00 | 1,362,000.00 | $ | 19,238,000 | ||||||||

| (1) | All amounts in this chart and circular are in U.S. dollars unless otherwise indicated. There is no minimum offering amount and no provision to escrow or return investor funds if any minimum number of Shares is not sold. All investor funds will be held in a Company processing account until the investor’s subscription is accepted by the Company, at which time such funds will become available for the Company’s use. We will conduct separate closings, which closings may be conducted on a rolling basis. Closings will be conducted promptly after receiving investor funds, but in no case any less frequently than every 30 days. |

| (2) | We have engaged DealMaker Securities LLC, referred to herein as the “Broker,” for administrative and compliance related services in connection with this Offering. The Broker is not purchasing any securities from the Company with a view to sell those for the Company as part of the distribution of the security. The Broker and its affiliates will receive one-time advances of accountable expenses of $65,000, monthly advances of accountable expenses of $10,000 totalling $30,000, a monthly account maintenance/management and advisory fee of $10,000 up to a maximum of $90,000, and prospective marketing budget fees of $250,000, which compensation is reflected as a total in the above table. The Broker will also receive up to four and 50/100th percent (4.5%) of the amount raised in this offering. The compensation due to Broker is capped at $1,362,000, assuming we raise the Maximum Offering Amount. Please see “Plan of Distribution” for additional information. |

| (3) | We expect to incur expenses relating to this offering in addition to the fees due to the Broker, including, but not limited to, legal, accounting, marketing, travel, and other miscellaneous expenses, which are not included in the foregoing table. See “Use of Proceeds” for more detail. |

(4) |

The Broker will also earn a commission on the Investor Processing Fees collected by the Company, subject to the above-described cap on commissions. The Investor Processing Fee will be applied towards the maximum amount the Company can raise under Regulation A and each unaccredited investor’s investment limits discussed herein. The Investor Processing Fee included in the above table presumes we sell the full $20,000,000 in Shares offered. |

Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

Our common stock is not now listed on any national securities exchange, quotation system or the Nasdaq stock market and there is no market for our securities. There is no guarantee, and it is unlikely, that an active trading market will develop in our securities. Investors should be prepared to hold our Shares indefinitely.

This offering is being made pursuant to Tier 2 of Regulation A, following the Form 1-A Offering Circular disclosure format.

This offering is highly speculative and these securities involve a high degree of risk and should be considered only by persons who can afford the loss of their entire investment. See “Risk Factors” on Page 5.

THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OF OR GIVE ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SOLICITATION MATERIALS. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION.

TABLE OF CONTENTS

| 2 |

This summary highlights some of the information in this Offering Circular. It is not complete and may not contain all of the information that you may want to consider. To understand this offering fully, you should carefully read the entire circular, including the section entitled “Risk Factors” and the exhibits included with the Offering Statement, before making a decision to invest in our securities. Unless otherwise noted or unless the context otherwise requires, the terms “we,” “us,” “our,” “Midori,” and the “Company” refer to Midori Group Inc. together with its wholly owned subsidiaries. In instances where we refer emphatically to “Midori Group Inc.” or where we refer to a specific subsidiary of ours by name, we are referring only to that specific legal entity. The term “Offering Circular” refers to this Offering Circular which comprises Part 2 of the Offering Statement (“Offering Statement”) filed with the SEC on Form 1-A, of which this Offering Circular is a part.

The Company

Midori Group Inc., a British Columbia corporation, was originally incorporated as 1284670 B.C. LTD in British Columbia, Canada under the British Columbia Business Corporations Act on January 19, 2021. It was renamed to Midori Group Inc. on June 29, 2022. Our wholly owned operating subsidiary, Midori-Bio Inc., an Ontario corporation, was incorporated in Ontario, Canada under the Canada Business Corporations Act on January 6, 2021, and acquired by the Company in August, 2021.

Midori Group Inc. is currently incorporated and in good standing in British Columbia, Canada. Our principal executive offices are located at 5 Hazelton Avenue Suite 400, Toronto, ON M5R 2E1, and our telephone number 905-330-9113. Our website address is www.midori-bio.com. The information contained on our website is not incorporated by reference into this Offering Circular, and you should not consider any information contained on, or that can be accessed through, our website as part of this Offering Circular or in deciding whether to purchase our Shares.

Business

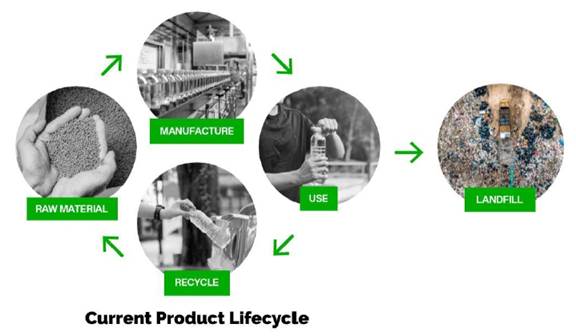

We are a distribution, sales and marketing company of a green, biodegradable plastic additive. We acquire our additive from a third-party supplier and market and resell the additive under our own private brand label “Midori Biosolutions.”

The Midori Biosolutions additive is non-toxic, with no heavy metals or starches, and free of BPA & Phosphates with extensive testing data available for customers. We believe the additive will provide consumer packaged goods (CPG) brands with an end-of-life biodegradable solution, without impeding normal recycle/composting plastics, and a practical and viable solution for reducing plastic waste from the world environment.

As a distributor, we do not own the intellectual property rights to the additive we sell. If our distribution agreement with our supplier were terminated, we would need to contract with one of the several other manufacturers of the additive of which the Company is aware. If we were not able to contract with another supplier or were forced to contract with another supplier on terms materially less favorable to the Company, our business would be materially negatively impacted. Notwithstanding the foregoing, the Company’s goal is to acquire intellectual property rights for its additive using proceeds from this offering; however, no formal negotiations for such acquisition have begun and are not expected to begin until we have raised sufficient funds from this offering.

We have trademarked “Advanced BioRecycle” in order to fit into the current government & industry primary desire to recycle. BioRecycle is part of the other two recycle processes including Mechanical and Chemical recycling; but with the advantage of no energy required to complete the recycle process in landfills and no microplastics as an end state of the plastic. The Midori Biosolutions additive is an innovative technology that aims to solve the major problem of the amount of time it takes for plastic to decompose, as it can otherwise take centuries to biodegrade. With this additive, we seek to accelerate the natural biodegradation process and reduce the timeframe to just a few years. We believe that the additive can help CPG brand owners alleviate the challenges associated with unrecycled plastics, supporting their industry and governmental plastic targets.

We are currently working with approximately 51 consumer and industrial brands across several industries. We have currently signed contracts with six of such brands and with each have completed initial integration testing where we tested to confirm that our products could be integrated into their plastics (e.g our pellet product can integrate and be used in their pellet products, our PET product can integrate and be used in their PET products, etc.). The testing is done internally by the Company and customer and is not certified over overseen by any neutral third party. The brands are now in the degradation testing phase where we test that after integration of our products into our customers’ products, such products will biodegrade as expected. This testing phase takes about three months, after which time the customers can move to products launch. While we assist customers with review of their messaging, we are not otherwise involved in the launch process nor do we control the timing of their product launches. As we onboard new clients, they will go through a similar process: testing to ensure our products can be added to their products in a matching form, test to ensure once added that the product degrades, and once internal processes are complete, launch new customer product with our additive included.

The Midori Biosolutions additive is considered a natural organic additive for plastic. Based on findings of independent third-party testing, the Midori Biosolutions additive is 100% organic and non-starch based with no heavy metals. The Midori-Biosolutions additive is sold by us in many formats to match each type of plastic format used by our customers, including, but not limited to, pellets, powder, polyethylene terephthalate (PET), polypropylene (PP), polystyrene (PS), nylon, and synthetic rubber (collectively, referred to herein as our “products”). We aim to provide an end-of-life solution for all plastics. The Company does not seek to interfere with current recycling efforts, and instead intends to compliment these efforts with our solutions. We believe that the Midori Biosolutions additive will provide brands and retailers with a possible solution for fossil fuel-based plastics.

Going Concern

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. Due to recurring losses from operations and the accumulated deficit the Company’s auditor has stated that substantial doubt exists about the Company’s ability to continue as a going concern.

The consolidated financial statements have been prepared on the assumption that the Company will continue as a going concern, meaning it will continue in operations for the foreseeable future and will be able to realize assets and discharge liabilities in the ordinary course of operations. The application of the going concern basis is dependent upon the Company achieving profitable operations to generate sufficient cash flows to fund continuing operations, or, in the absence of adequate cash flows from operations, obtaining additional financing to support operations for the foreseeable future.

Capitalization

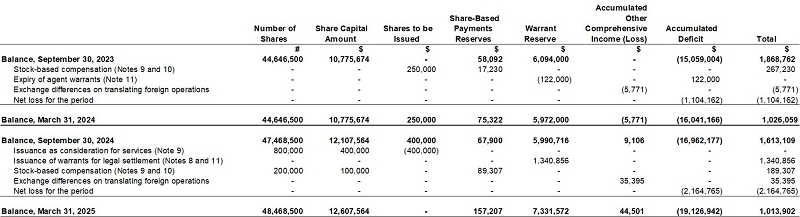

We are authorized to issue an unlimited amount of Common Shares with no par value per share. As of April 21, 2025, the Company had 48,168,500 Shares issued and outstanding. Following this offering, assuming all offered Shares are sold and no Shares outside of this offering are issued, we will have 68,168,500 Shares outstanding.

The Company has the following warrants and options issued and outstanding:

5,000,000 warrants, with a strike price of C$0.25 expiring 3 years from public listing

9,000,000 warrants expiring June 17, 2026, strike price of C$0.05

75,000 warrants, with a strike price of C$1.00, expiring May 14, 2027.

2,937,334 warrants with a strike price of C$0.05, expiring January 10, 2027

1,000,000 stock options at a strike price of C$0.50, expiring July 31, 2028

1,200,000 stock options at a strike price of C$0.50, expiring January 1, 2028

| 3 |

Use of Proceeds

In general, the Company will use net proceeds from the offering for operational working capital, marketing, capital expenditures and ongoing legal and accounting. See “Use of Proceeds” on page 26 for more detail.

The Offering

This Offering Circular relates to the sale of up to 20,000,000 Shares of our common stock at a price of $1.00 per Share.

To offset some of the transactional expenses associated with this offering, we will charge investors an Investor Processing Fee equal to 3% of their subscription amounts (i.e. $3 for every $100 invested). Thus, the minimum investment for any investor is $1,000 in Shares plus a $30 Investor Processing Fee. The Broker will earn its commission on the Investor Processing Fees collected by the Company, subject to the agreed cap on commissions. The Investor Processing Fee will be applied towards the maximum amount the Company can raise under Regulation A (effectively increasing the Maximum Offering Amount and price per Share by 3%) and each unaccredited investor’s investment limits discussed herein. No Shares will be issued in consideration for the Investor Processing Fee.

There is no minimum offering amount and no provision to escrow or return investor funds if any minimum number of shares is not sold. All funds raised by the Company from this offering will be immediately available for the Company’s use.

Shares are being offered on a “best efforts” basis. We have engaged Dealmaker Securities LLC to act as the Broker of record in connection with this offering, but not for underwriting or placement agent services. We have also engaged affiliates of the Broker to provide technology services.

In order to subscribe to purchase the shares, a prospective investor must complete a subscription agreement and send payment by wire transfer, ACH, or credit card through our subscription portal at www.__________.com. Investors must answer certain questions to determine compliance with the investment limitation set forth in Regulation A Rule 251(d)(2)(i)I under the Securities Act, which states that in offerings such as this one, where the securities will not be listed on a registered national securities exchange upon qualification, the aggregate purchase price to be paid by an investor who is a natural person for the securities cannot exceed 10% of the greater of the investor’s annual income or net worth, unless the purchaser is an accredited investor. In the case of an investor who is not a natural person, revenues or net assets for the investors’ most recently completed fiscal year are used instead.

This offering will terminate at the earlier to occur of: (i) all Shares offered hereby are sold, (ii) three years from the date this Offering Circular, as amended, is qualified with the SEC, or (iii) such earlier date as determined by the Company.

ABOUT THIS CIRCULAR

We have prepared this Offering Circular to be filed with the SEC for our offering of securities. The Offering Circular includes exhibits that provide more detailed descriptions of the matters discussed in this Offering Circular.

You should rely only on the information contained in this Offering Circular and its exhibits. We have not authorized any person to provide you with any information different from that contained in this Offering Circular. The information contained in this Offering Circular is complete and accurate only as of the date of this Offering Circular, regardless of the time of delivery of this Offering Circular or sale of our shares. This Offering Circular contains summaries of certain other documents, but reference is hereby made to the full text of the actual documents for complete information concerning the rights and obligations of the parties thereto. All documents relating to this offering and related documents and agreements, if readily available to us, will be made available to a prospective investor or its representatives upon request.

INDUSTRY AND MARKET DATA

The industry and market data used throughout this Offering Circular have been obtained from our own research, surveys or studies conducted by third parties and industry or general publications. Industry publications and surveys generally state that they have obtained information from sources believed to be reliable, but do not guarantee the accuracy and completeness of such information. We believe that each of these studies and publications is reliable. We have not engaged any person or entity to provide us with industry or market data.

TAX CONSIDERATIONS

No information contained herein, nor in any prior, contemporaneous or subsequent communication should be construed by a prospective investor as legal or tax advice. We are not providing any tax advice as to the acquisition, holding or disposition of the securities offered herein. In making an investment decision, investors are strongly encouraged to consult their own tax advisor to determine the U.S./CAN Federal, state and any applicable foreign tax consequences relating to their investment in our securities. This written communication is not intended to be “written advice,” as defined in Circular 230 published by the U.S. Treasury Department

| 4 |

PRESENTATION OF FINANCIAL INFORMATION

The financial information contained in this Offering Circular derives from (i) the audited financial statements of Midori Group Inc. (formerly known as 1284670 B.C. LTD), a British Columbian corporation, for the periods ended September 30, 2023 and September 30, 2024. Our audited financial statements are prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB. Our fiscal year ends on September 30 of each year, so all references to a particular fiscal year are to the applicable year ended September 30. References to “$,” “USD$” or “dollars” are to U.S. dollars, and all references to “CAD$” or “C$” are to the lawful currency of Canada. Except as otherwise indicated, our financial statements and other information are presented in Canadian dollars while offering terms are expressed in USD$.

SPECIAL INFORMATION REGARDING FORWARD LOOKING STATEMENTS

Some of the statements in this Offering Circular are “forward-looking statements.” These forward-looking statements involve certain known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by these forward-looking statements. These factors include, among others, the factors set forth above under “Risk Factors.” The words “believe,” “expect,” “anticipate,” “intend,” “plan,” and similar expressions identify forward-looking statements. We caution you not to place undue reliance on these forward-looking statements.

We undertake no obligation to update and revise any forward-looking statements or to publicly announce the result of any revisions to any of the forward-looking statements in this document to reflect any future or developments. However, the Private Securities Litigation Reform Act of 1995 is not available to us as a non-reporting issuer. Further, Section 27A(b)(2)(D) of the Securities Act and Section 21E(b)(2)(D) of the Exchange Act expressly state that the safe harbor for forward looking statements does not apply to statements made in connection with an initial public offering.

Any investment in our common stock involves a high degree of risk. Investors should carefully consider the risks described below and all of the information contained in this Offering Circular before deciding whether to purchase our common stock. Our business, financial condition or results of operations could be materially adversely affected by these risks if any of them actually occur. Some of these factors have affected our financial condition and operating results in the past or are currently affecting us. This Offering Circular also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the risks described below and elsewhere in this Offering Circular. In addition to the other information provided in this Offering Circular, you should carefully consider the following risk factors in evaluating our business and before purchasing any of our common stock. Material risks identified by the Company are discussed in this section; however, discussion may not include all risks applicable to an investment in Shares to the extent such risks have not been contemplated by the Company.

Risks Related to this Offering and our Common Stock

There is no current market for any shares of the Company’s stock.

There is no established trading market for our Shares and there may never be one. As a result, if you decide to sell these securities in the future, you may not be able to find a buyer. Investors should assume that they may not be able to liquidate their investment or be able to pledge their shares as collateral and should be prepared to hold this investment indefinitely.

Investors will hold minority interests in the Company.

While the common stock is entitled to vote on Company matters, investors in their individual capacities will represent a minority of the Company’s authorized voting stock. Accordingly, individual investors should anticipate little or no ability to direct the Company’s operations.

| 5 |

Using a credit card to purchase shares may impact the return on your investment as well as subject you to other risks inherent in this form of payment.

Investors in this offering may at some point have the option of paying for their investment with a credit card, which is not usual in the traditional investment markets. Transaction fees charged by your credit card company and interest charged on unpaid card balances (which can reach almost 30% in some states) add to the effective purchase price of the shares you buy. See “Plan of Distribution and Selling Shareholders.” The cost of using a credit card may also increase if you do not make the minimum monthly card payments and incur late fees. Using a credit card is a relatively new form of payment for securities and will subject you to other risks inherent in this form of payment, including that, if you fail to make credit card payments (e.g. minimum monthly payments), you risk damaging your credit score and payment by credit card may be more susceptible to abuse than other forms of payment. Moreover, where a third-party payment processor is used, your recovery options in the case of disputes may be limited. The increased costs due to transaction fees and interest may reduce the return on your investment.

The SEC’s Office of Investor Education and Advocacy issued an Investor Alert dated February 14, 2018 entitled Credit Cards and Investments – A Risky Combination, which explains these and other risks you may want to consider before using a credit card to pay for your investment.

The subscription agreement has a forum selection provision that requires disputes be resolved in state or federal courts in the state of British Columbia, regardless of convenience or cost to you, the investor.

As part of this investment, each investor will be required to agree to the terms of the subscription agreement included as Exhibit 4.1 to the Offering Statement of which this Offering Circular is part. In the agreement, investors agree to resolve disputes arising under the subscription agreement in state or federal courts located in the province of British Columbia, Canada, for the purpose of any suit, action or other proceeding arising out of or based upon the agreement. Section 22 of the Securities Act creates concurrent jurisdiction for federal and state courts over all suits brought to enforce any duty or liability created by the Securities Act or the rules and regulations thereunder. The Company believes that the exclusive forum provision applies to claims arising under the Securities Act, but there is uncertainty as to whether a court would enforce such a provision in this context. Section 27 of the Exchange Act creates exclusive federal jurisdiction over all suits brought to enforce any duty or liability created by the Exchange Act or the rules and regulations thereunder. As a result, the exclusive forum provision will not apply to suits brought to enforce any duty or liability created by the Exchange Act or any other claim for which the federal courts have exclusive jurisdiction. You will not be deemed to have waived the Company’s compliance with the U.S. federal securities laws and the rules and regulations thereunder. This forum selection provision may limit your ability to obtain a favorable judicial forum for disputes with us. Although we believe the provision benefits us by providing increased consistency in the application of British Columbia law in the types of lawsuits to which it applies and in limiting our litigation costs, to the extent it is enforceable, the forum selection provision may limit investors’ ability to bring claims in judicial forums that they find favorable to such disputes, may increase investors’ costs of bringing suit and may discourage lawsuits with respect to such claims. Alternatively, if a court were to find the provision inapplicable to, or unenforceable in an action, the Company may incur additional costs associated with resolving such matters in other jurisdictions, which could adversely affect its business, financial condition or results of operations.

We do not anticipate paying any cash dividends.

We presently do not anticipate that we will pay any dividends on any of our common stock in the foreseeable future. The payment of dividends, if any, would be contingent upon our revenues and earnings, if any, capital requirements, and general financial condition. The payment of any dividends will be within the discretion of our Board of Directors (the “Board”). We presently intend to retain all earnings to implement our business plan; accordingly, we do not anticipate the declaration of any dividends in the foreseeable future.

We may need additional capital, and the sale of additional Shares or other equity securities could result in additional dilution to our stockholders.

We may require additional capital for the development and commercialization of our products and may require additional cash resources due to changed business conditions or other future developments, including any investments or acquisitions we may decide to pursue. If our resources are insufficient to satisfy our cash requirements, we may seek to sell additional equity or debt securities or obtain a credit facility. We may sell an unlimited number of Shares. The sale of additional equity securities could result in additional dilution to our stockholders, in an amount that cannot be determined at this time. The incurrence of additional indebtedness would result in increased debt service obligations and could result in operating and financing covenants that would restrict our operations. We cannot assure you that financing will be available in amounts or on terms acceptable to us, if at all.

| 6 |

Our principal stockholders and management own a significant percentage of our stock and will be able to exert significant control over matters subject to stockholder approval.

Our Chief Executive Officer and President each beneficially own approximately 21.98% of the Company’s common stock. Accordingly, they will collectively have significant influence over our affairs due to their substantial ownership coupled with their positions on our board and management team. For example, they may be able to significantly influence elections of directors, amendments of our organizational documents, or approval of any merger, sale of assets, or other major corporate transaction. This concentration of ownership may prevent or discourage unsolicited acquisition proposals or offers for our common stock that some of our stockholders may believe is in their best interest.

Because our management will have broad discretion and flexibility in how the net proceeds from this offering are used, we may use the net proceeds in ways in which you disagree.

The intended use of proceeds from this offering is more particularly described in the Section titled “Use of Proceeds,” however, such description is not binding and the actual use of proceeds may differ from the description contained therein. Accordingly, our management will have significant discretion and flexibility in applying the net proceeds of this offering. You will be relying on the judgment of our management with regard to the use of these net proceeds, and you will not have the opportunity, as part of your investment decision, to assess whether the net proceeds are being used appropriately. It is possible that the net proceeds will be invested in a way that does not yield a favorable, or any, return for us. The failure of our management to use such funds effectively could have a material adverse effect on our business, financial condition, operating results and cash flow.

The offering price of our Shares from the Company has been arbitrarily determined.

Our management has determined the Shares offered by the Company. The price of the Shares we are offering was arbitrarily determined based upon the illiquidity and volatility of our common stock, our current financial condition and the prospects for our future cash flows and earnings, and market and economic conditions at the time of the offering. The offering price for the common stock sold in this offering may be more or less than the fair market value for our common stock.

The best-efforts structure of this offering may yield insufficient gross proceeds to fully execute our business plan.

Shares are being offered on a best-efforts basis. We are not required to sell any specific number or dollar amount of common stock, but will use our best efforts to sell the Shares offered by us. As a “best efforts” offering, there can be no assurance that the offering contemplated by this Offering Circular will result in any proceeds being made available to us.

We may not register or qualify our securities with any state agency pursuant to blue sky regulations.

The holders of our shares of common stock and persons who desire to purchase them in the future should be aware that there may be significant state law restrictions upon the ability of investors to resell our shares. We currently do not intend to and may not be able to qualify securities for resale in states which require shares to be qualified before they can be resold by our shareholders.

We are relying on the exemption for insignificant participation by benefit plan investors under ERISA.

The Plan Assets Regulation of the Employee Retirement Income Security Act of 1974 (“ERISA”) provides that the assets of an entity will not be deemed to be the assets of a benefits plan if equity participation in the entity by benefit plan investors, including benefit plans, is not significant. The Plan Assets Regulation provides that equity participation in the entity by benefit plan investors is “significant” if, at any time, 25% or more of the value of any class of equity interest is held by benefit plan investors. Because we are relying on this exemption, we will not accept investments from benefit plan investments of 25% or more of the value of any class of equity interest. If repurchases of shares reach 25%, we may repurchase shares of benefit plan investors without their consent until we are under such 25% limit. See the section of this offering circular captioned “ERISA Considerations” for additional information regarding the Plan Assets Regulation.

| 7 |

Shares are being offered under an offering exemption under Regulation A and, if it were later determined that such exemption was not available, U.S. purchasers would be entitled to rescind their purchase agreements.

Shares are being offered to prospective investors pursuant to Tier 2 of Regulation A under the Securities Act. Unless the sale of Shares should qualify for such exemption the U.S. investors might have the right to rescind their purchase of Shares. Since compliance with these exemptions is highly technical, it is possible that if an investor were to seek rescission, such investor would succeed. A similar situation prevails under state law in those states where Shares may be offered without registration. If a number of investors were to be successful in seeking rescission, the Company would face severe financial demands that could adversely affect the Company and, thus, the non-rescinding investors. Inasmuch as the basis for relying on exemptions is factual, depending on the Company’s conduct and the conduct of persons contacting prospective investors and making the offering, the Company will not receive a legal opinion to the effect that this offering is exempt from registration under any federal or state law. Instead, the Company will rely on the operative facts as documented as the Company’s basis for such exemptions.

Investors in our securities could experience immediate and substantial dilution after this offering.

The public offering price of our Shares is higher than the pro forma net tangible book value per share of the outstanding Common Shares immediately after this offering. As a result of this dilution, investors purchasing Shares in this offering could receive significantly less than the full purchase price that they paid for the Shares purchased in this offering in the event of a liquidation. Further, we have outstanding warrants and options with strike prices less than the price per Share in this offering. Consequently, if these securities are exercised, there could be further dilution to the purchasers of our Shares.

We may experience investment delays.

There may be a delay between the time an investor’s subscription is accepted by the Company and the time the proceeds of this offering are deployed. During these periods (after an investor’s closing but before the Company has deployed the funds), the Company may invest these proceeds in short-term certificates of deposit, money-market funds, or other liquid assets with FDIC-insured and/or NCUA-insured banking institutions, which may not yield a return as high as if deployed towards operations.

There may be deficiencies with our internal controls that require improvements.

As a Tier 2 issuer, we will not need to provide a report on the effectiveness of our internal controls over financial reporting, and we will be exempt from the auditor attestation requirements concerning any such report. We do not know whether our internal control procedures are effective and therefore there is a greater likelihood of undiscovered errors in our internal controls or reported financial statements as compared to issuers that have conducted such evaluations.

Investors in this offering may not be entitled to a jury trial with respect to claims arising under the Subscription Agreement, which could result in less favorable outcomes to the plaintiff(s) in any action under these Agreements.

Investors in this offering will be bound by the Subscription Agreement, which includes a provision under which investors waive the right to a jury trial of any claim, other than claims arising under federal securities laws, that they may have against the Company arising out of or relating to these agreements. By signing the Subscription Agreement, the investor warrants that the investor has reviewed this waiver with his or her legal counsel, and knowingly and voluntarily waives the investor’s jury trial rights following consultation with the investor’s legal counsel.

If you bring a claim against the Company in connection with matters arising under the Subscription Agreement, other than claims under the federal securities laws, you may not be entitled to a jury trial with respect to those claims, which may have the effect of limiting and discouraging lawsuits against the Company. If a lawsuit is brought against the Company, it may be heard only by a judge or justice of the applicable trial court, which would be conducted according to different civil procedures and may result in different outcomes than a trial by jury would have had, including results that could be less favorable to the plaintiff(s) in such an action.

We will be subject to ongoing public reporting requirements that are less rigorous than rules for more mature public companies, and our investors receive less information.

We are required to report on an ongoing basis under the reporting rules set forth in Regulation A for Tier 2 issuers. The ongoing reporting requirements under Regulation A are more relaxed than for public companies reporting under the Exchange Act. The differences include, but are not limited to, being required to file only annual and semiannual reports, rather than annual and quarterly reports. Annual reports are due within 120 calendar days after the end of our fiscal year, and semiannual reports are due within 90 calendar days after the end of the first six months of our fiscal year.

| 8 |

We also may elect to become a public reporting company under the Exchange Act. If we elect or are required to do so, we will be required to publicly report on an ongoing basis as an emerging growth company, as defined in the JOBS Act, under the reporting rules set forth under the Exchange Act. For so long as we remain an emerging growth company, we may take advantage of certain exemptions from various reporting requirements that are applicable to other Exchange Act reporting companies that are not emerging growth companies. Alternatively, in the event we become a public reporting company under the Exchange Act, we may qualify for reduced reporting obligations as a Foreign Private Issuer.

In any case, we will be subject to ongoing public reporting requirements that are less rigorous than Exchange Act rules for companies that are not Foreign Private Issuers or emerging growth companies, and investors could receive less information than they might expect to receive from more mature public companies.

If we are required to register any Shares under the Exchange Act, it would result in significant expense and reporting requirements that would place a burden on the Company.

Subject to certain exceptions, Section 12(g) of the Exchange Act requires an issuer with more than $10 million in total assets to register a class of its equity securities with the Commission under the Exchange Act if the securities of such class are held of record at the end of its fiscal year by more than 2,000 persons or 500 persons who are not “accredited investors.” To the extent the Section 12(g) assets and holders limits are exceeded, we intend to rely upon a conditional exemption from registration under Section 12(g) of the Exchange Act contained in Rule 12g5-1(a)(7) under the Exchange Act (the “Reg. A+ Exemption”), which exemption generally requires that the issuer (i) be current in its Form 1-K, 1-SA and 1-U filings as of its most recently completed fiscal year end; (ii) engage a transfer agent that is registered under Section 17A(c) of the Exchange Act to perform transfer agent functions; and (iii) have a public float of less than $75 million as of the last business day of its most recently completed semi-annual period or, in the event the result of such public float calculation is zero, have annual revenues of less than $50 million as of its most recently completed fiscal year. Alternatively, we may qualify for a conditional exemption for certain Foreign Private Issuers contained in Rule 12g3-2 under the Exchange Act under limited circumstances. If the number of record holders of any Series of Interests exceeds either of the limits set forth in Section 12(g) of the Exchange Act and we fail to qualify for the Reg. A+ Exemption or the Foreign Private Issuer exemption, we would be required to register such Series with the Commission under the Exchange Act. If we are required to register any securities under the Exchange Act, it would result in significant expense and reporting requirements that would place a financial burden on the Company and a time burden on our management.

Our management team has limited experience managing a publicly reporting company.

Most members of our management team have limited experience managing a publicly reporting company, interacting with public investors, and complying with the increasingly complex laws pertaining to Regulation A reporting companies. Our management team may not successfully or efficiently manage our transition to being a publicly reporting company that is subject to significant regulatory oversight and reporting obligations under the federal securities laws and the continuous scrutiny of securities analysts and investors. These new obligations and constituents will require significant attention from our senior management and could divert their attention away from the day-to-day management of our business, which could harm our business, financial condition, and results of operations.

There are inherent uncertainties involved in estimates, judgments and assumptions used in the preparation of financial statements in accordance with IFRS. Any changes in these estimates, judgments or assumptions, including any changes as a result of changes in accounting principles and guidance, or their interpretation, could result in unfavorable accounting charges or effects.

The preparation of financial statements in accordance with IFRS as issued by IASB requires management and the Board to make judgments, estimates and assumptions that affect the application of policies and the reported amounts of assets and liabilities, income and expenses. Estimates, judgments and assumptions are inherently subject to change in the future, and any such changes, including any changes as a result of changes in accounting principles and guidance, or their interpretation, could result in corresponding changes to the amounts of assets and liabilities, income and expenses.

| 9 |

Risks Related to our Business

Since we have a limited operating history, it is difficult for potential investors to evaluate our business.

Our short operating history may hinder our ability to successfully meet our objectives and makes it difficult for potential investors to evaluate our business or prospective operations. As an early-stage company, we are subject to all the risks inherent in the financing, expenditures, operations, complications and delays inherent in a newer business. Accordingly, our business and success face risks from uncertainties faced by developing companies in a competitive environment. There can be no assurance that our efforts will be successful or that we will ultimately be able to attain profitability.

We may not be able to raise capital when needed, if at all, which would force us to delay, reduce or eliminate our product development programs or commercialization efforts and could cause our business to fail.

We anticipate needing additional funding to pursue additional product development and launch and commercialize our products. There are no assurances that future funding will be available on favorable terms or at all. If additional funding is not obtained, we may need to reduce, defer or cancel additional product development or overhead expenditures to the extent necessary. The failure to fund our operating and capital requirements could have a material adverse effect on our business, financial condition and results of operations.

If we are unable to raise capital when needed or on attractive terms, we could be forced to delay future expansion and/or commercialization efforts. Any of these events could significantly harm our business, financial condition and prospects.

Our financial situation creates doubt whether we will continue as a going concern.

During the year ended September 30, 2024, the Company incurred a net loss of $2,025,173 (2023 – $2,195,748), and as of that date, the Company’s accumulated deficit was $16,962,177 (September 30, 2023 – accumulated deficit of $15,059,004). Our ability to continue as a going concern is dependent upon obtaining additional equity financing or other capital, attaining further operating efficiencies, reducing expenditures, and, ultimately, generating more revenue. The doubt regarding our potential ability to continue as a going concern may adversely affect our ability to obtain new financing on reasonable terms or at all. Additionally, if we are unable to continue as a going concern, our stockholders may lose some or all of their investment in the Company.

We depend heavily on key personnel, and turnover of key senior management could harm our business.

Our future business and results of operations depend in significant part upon the continued contributions of our senior management personnel. If we lose their services or if they fail to perform in their current positions, or if we are not able to attract and retain skilled personnel as needed, our business could suffer. Significant turnover in our senior management could significantly deplete our institutional knowledge held by our existing senior management team. We depend on the skills and abilities of these key personnel in managing the product acquisition, marketing and sales aspects of our business, any part of which could be harmed by turnover in the future. We do not have any key person insurance.

We have substantial capital requirements that, if not met, may hinder our operations.

We anticipate that we will make substantial capital expenditures for research and product development work and expansion. If we cannot raise sufficient capital, we may have limited ability to expend the capital necessary to undertake or complete research and product development work and acquisitions. There can be no assurance that debt or equity financing will be available or sufficient to meet these requirements or for other corporate purposes, or if debt or equity financing is available, that it will be on terms acceptable to us. Moreover, future activities may require us to alter our capitalization significantly. Our inability to access sufficient capital for our operations could have a material adverse effect on our financial condition, results of operations or prospects.

| 10 |

Terms of subsequent financings may adversely impact your investment.

We will likely need to engage in common equity, debt, or preferred stock financings in the future, which may reduce the value of your investment in the Common Stock. Interest on debt securities could increase costs and negatively impact operating results. Preferred stock could be issued in series from time to time with such designation, rights, preferences, and limitations as needed to raise capital. The terms of preferred stock could be more advantageous to those investors than to the holders of Common Stock. In addition, if we need to raise more equity capital from the sale of Common Stock, institutional or other investors may negotiate terms that are likely to be more favorable than the terms of your investment, and possibly a lower purchase price per share.

Current global financial conditions have been characterized by increased volatility which could negatively impact our business, prospects, liquidity and financial condition.

Current global financial conditions and recent market events have been characterized by increased volatility and the resulting tightening of the credit and capital markets has reduced the amount of available liquidity and overall economic activity. We cannot guaranty that debt or equity financing, the ability to borrow funds or cash generated by operations will be available or sufficient to meet or satisfy our initiatives, objectives or requirements. Our inability to access sufficient amounts of capital on terms acceptable to us for our operations will negatively impact our business, prospects, liquidity and financial condition.

We intend to grow the size of our organization, and we may experience difficulties in managing any growth we may achieve.

As our development and commercialization plans and strategies develop, we expect to need additional research, development, managerial, operational, sales, marketing, financial, accounting, legal, and other resources. Future growth would impose significant added responsibilities on members of management. Our management may not be able to accommodate those added responsibilities, and our failure to do so could prevent us from effectively managing future growth, if any, and successfully growing our company.

We may expend our limited resources to pursue a particular product and may fail to capitalize on products that may be more profitable or for which there is a greater likelihood of success.

Because we have limited financial and managerial resources, we have focused our efforts on particular products. As a result, we may forego or delay pursuit of opportunities with other products that later prove to have greater commercial potential. Our resource allocation decisions may cause us to fail to capitalize on viable commercial products or profitable market opportunities. Any failure to improperly assess potential products could result in missed opportunities and/or our focus on products with low market potential, which would harm our business and financial condition.

We engage in transactions with related parties and such transactions present possible conflicts of interest that could have an adverse effect on us.

We have entered, and may continue to enter, into transactions with related parties for financing, corporate, business development and operational services, as detailed herein. Such transactions may not have been entered into on an arm’s-length basis, and we may have achieved more or less favorable terms because such transactions were entered into with our related parties. Such conflicts could cause an individual in our management to seek to advance his or her economic interests or the economic interests of certain related parties above ours. Further, the appearance of conflicts of interest created by related party transactions could impair the confidence of our investors, which could have a material adverse effect on our liquidity, results of operations and financial condition.

Any inability to protect our intellectual property rights could reduce the value of our technologies and brands, which could adversely affect our financial condition, results of operations and business.

Our business is dependent upon our trademarks, trade secrets, copyrights and other intellectual property rights. There is a risk of certain valuable trade secrets being exposed to potential infringers. In addition, we do not own the formula for our product and third parties may purchase our product from our supplier or may counterfeit our products. The efforts we have taken to protect our proprietary rights may not be sufficient or effective. Any significant impairment of our intellectual property rights could harm our business reputation or our ability to compete. In addition, protecting our intellectual property rights is costly and time consuming. There is a risk that we may have insufficient resources to counter adequately such infringements through negotiation or the use of legal remedies. It may not be practicable or cost effective for us to fully protect our intellectual property rights in some countries or jurisdictions. If we are unable to successfully identify and stop unauthorized use of our intellectual property and/or counterfeiting of our products, we could lose potential revenue, experience diminished brand reputation, and experience increased operational and enforcement costs, which could adversely affect our financial condition, results of operations and business.

| 11 |

If we fail to comply with government laws and regulations it could have a materially adverse effect on our business.

We are subject to extensive foreign, federal, state and local laws and regulations that are extremely complex. We exercise care in structuring our operations to comply in all material respects with applicable laws to the extent possible. We will also take such laws into account when planning future operations and acquisitions. The laws, rules and regulations described above are complex and subject to interpretation. In the event of a determination that we are in violation of such laws, rules or regulations, or if further changes in the regulatory framework occur, any such determination or changes could have a material adverse effect on our business. There can be no assurance however that we will not be found in noncompliance in any particular situation.

We may not maintain sufficient insurance coverage for the risks associated with our business operations.

Risks associated with our business and operations include, but are not limited to, claims for wrongful acts committed by our officers, directors, and other representatives, the loss of intellectual property rights, the loss of key personnel, risks posed by natural disasters, risks of lawsuits from our employees, and risks of lawsuits from customers who are injured from or dissatisfied with our products. Any of these risks may result in significant losses. We cannot provide any assurance that our insurance coverage is sufficient to cover any losses that we may sustain, or that we will be able to successfully claim our losses under our insurance policies on a timely basis or at all. If we incur any loss not covered by our insurance policies, or the compensated amount is significantly less than our actual loss or is not timely paid, our business, financial condition and results of operations could be materially and adversely affected.

We rely on third parties to provide services essential to the success of our business.

We rely on third parties to provide a variety of essential business functions for us, including manufacturing, shipping, accounting, legal work, public relations, advertising, retailing, and distribution. It is possible that some of these third parties will fail to perform their services or will perform them in an unacceptable manner. It is possible that we will experience delays, defects, errors, or other problems with their work that will materially impact our operations and we may have little or no recourse to recover damages for these losses. A disruption in these key or other suppliers operations could materially and adversely affect our business. As a result, your investment could be adversely impacted by our reliance on third parties and their performance.

The Company is vulnerable to cyber-security risks.

We may be vulnerable to hackers who may access the data of our investors and customers. Any disruptions of services due to cyber attacks could harm our reputation and materially negatively impact our financial condition and business.

We are a holding company with no operations and rely on our operating subsidiary (Midori-Bio Inc.) to provide us with funds necessary to meet our financial obligations and to pay taxes, expenses and dividends. The subsidiary’s ability to make such distributions and payments to us may be subject to various limitations and restrictions.

We are a holding company with no direct operations that will hold as our principal asset a 100% ownership interest in Midori-Bio Inc. (our wholly owned operating subsidiary) and will rely on the subsidiary to provide us with funds necessary to meet any financial obligations. As such, we will have no independent means of generating revenue. We intend to cause the subsidiary to make distributions or, in the case of certain expenses, payments in an amount sufficient to allow us to pay our taxes and operating expenses. However, the subsidiary’s ability to pay dividends or make other distributions and payments to us may be subject to various limitations and restrictions, including, but not limited to, the operating results, cash requirements and financial condition of the subsidiary, the applicable provisions of Ontario law that may limit the amount of funds available for distribution to the shareholders of the subsidiary, compliance by the subsidiary with restrictions, covenants and financial ratios related to future indebtedness, and other agreements entered into by the subsidiary with third parties. If we do not have sufficient funds to pay tax or other liabilities or to fund our operations (i.e., as a result of the subsidiary’s inability to make distributions due to various limitations and restrictions), we may have to borrow funds, and thus our liquidity and financial condition could be materially and adversely affected.

| 12 |

The commercial success of our business depends on the widespread market acceptance of plastics manufactured with the Midori Biosolutions additive, which we believe accelerates the biodegradability of plastic products to just a few years, by third-parties and if we are unable to generate interest in plastic products produced with the Midori Biosolutions additive, we will be unable to generate sales and we will be forced to cease operations.

The market for biodegradable plastics produced with the Midori Biosolutions additive is still developing. Our success will depend on consumer acceptance of plastics produced with Midori Biosolutions by third parties. At present, it is difficult to assess or predict with any assurance the potential size, timing and viability of market opportunities for our product in the plastics market. The standard plastics market sector is well established with entrenched and well-capitalized competitors with whom we must compete. Achieving widespread market acceptance for these products will require substantial marketing efforts and the expenditure of sufficient resources to create brand recognition and customer demand and to cause potential customers to consider the potential benefits of the Company’s products as against the traditional products to which they have long been accustomed. Moreover, we have limited marketing capabilities and resources. To date, substantially all of our marketing activities have been conducted by members of management. The prospects for our product line will be largely dependent upon our ability to achieve market penetration for such products. Achieving market penetration will require sufficient efforts by the Company to create awareness of and demand for our products. The Company’s ability to build its customer base will depend in part on our ability to locate, hire and retain sufficient qualified marketing personnel and to fund marketing efforts, including advertising. There can be no assurance that our products will achieve widespread market acceptance or that our marketing efforts will result in profitable operations.

Currently, we distribute, sell and market a single private brand labeled additive (Midori Biosolutions), which is currently produced and supplied to us by a third party. We could lose the right to distribute the product if we do not meet the required sales goals under our distribution agreement, or otherwise breach the distribution agreement, which could materially negatively impact our business.

Currently, we distribute, sell and market a single private brand labeled additive which is currently produced and supplied by a third-party. We could lose the right to distribute the product if we do not meet the required sales goals or otherwise breach the Distributor Agreement. In the event of the termination of the Distributor Agreement, by termination by a party or expiration, we could no longer purchase and resell the additive to our clients. While we are aware of a number of other suppliers of similar additive products, there is no assurance that we be able to contract with any such supplier on terms favorable to the Company. The loss of our relationship with our current supplier could have a material adverse effect on our business, financial condition and results of operations. Further, transitioning to a new supplier for our product would be time consuming and expensive, may result in interruptions in our operations, could affect the performance specifications of our product or could require that we revalidate the materials. There can be no assurance that we will be able to secure alternative materials, and bring such materials on line and revalidate them without experiencing interruptions in our workflow. If we should encounter delays or difficulties in securing, reconfiguring or revalidating the materials required for our product, our business related to these products and our financial condition, results of operations and reputation could be adversely affected.

| 13 |

Although we seek to diversity our client base, we have historically depended on, and expect to continue to depend on, a limited number of customers for a high percentage of our revenues.

The loss of, or a significant reduction in orders from, any of these customers, including following any termination or failure to renew a long-term supply contract, would significantly reduce our revenues and harm our results of operations. If a large customer purchases fewer of our products, defers orders or fails to place additional orders with us for any other reason, including for business continuity purposes, our revenue could decline, and our operating results may not meet market expectations. In addition, if those customers order our products, but fail to pay on time or at all, our liquidity and operating results could be materially and adversely affected. Furthermore, if any of our current or future products compete with those of any of our largest customers, these customers may place fewer orders with us or cease placing orders with us, which would negatively affect our revenues and operating results.

We do not own the intellectual property rights to the additive constituting Midori Biosolutions.

We do not own the intellectual property rights to the additive constituting Midori Biosolutions. Our intellectual property currently only consists of a trademark for our private brand label “Midori Biosolutions.” Although we hope to acquire intellectual property rights with a portion of the proceeds in the offering so we may manufacture or have third parties manufacture the additive for us, we do not have a binding agreement relating to the acquisition of any such intellectual property and may not be able to enter into such an agreement on terms favorable to the Company.

Confidentiality agreements with employees and others may not adequately prevent disclosure of trade secrets and other proprietary information.

To protect our proprietary technologies and processes, we rely on trade secret protection. Although we have taken security measures to protect our trade secrets and other proprietary information, these measures may not provide adequate protection for such information. Our policy is to execute confidentiality and proprietary information agreements with each of our employees and consultants upon the commencement of an employment or consulting arrangement with us. These agreements generally require that all confidential information developed by the individual or made known to the individual by us during the course of the individual’s relationship with us be kept confidential and not be disclosed to third parties. These agreements also generally provide that technology conceived by the individual in the course of rendering services to us shall be our exclusive property. Even though these agreements are in place there can be no assurances that that trade secrets and proprietary information will not be disclosed, that others will not independently develop substantially equivalent proprietary information and techniques or otherwise gain access to our trade secrets, or that we can fully protect our trade secrets and proprietary information. Violations by others of our confidentiality agreements and the loss of employees who have specialized knowledge and expertise could harm our competitive position and cause our sales and operating results to decline as a result of increased competition. Costly and time-consuming litigation might be necessary to enforce and determine the scope of our proprietary rights, and failure to obtain or maintain trade secret protection might adversely affect our ability to continue our research or bring products to market.

Established product manufacturers could improve their ability to recycle their existing products or develop new environmentally preferable products which could render our technology less competitive.

Several plastic disposable packaging manufacturers and converters and others have made efforts to increase the recycling of their products. Increased recycling of plastic products could lessen their harmful environmental impact, one major basis upon which we compete.

We face competition from numerous competitors, many of whom have far greater resources than we have currently, which may make it more difficult for us to achieve significant market penetration.

The biodegradable product market is intensely competitive, subject to rapid change and significantly affected by new product introductions and other market activities of industry participants.

Many of our competitors are large, well-capitalized companies with significantly more market share and resources than we have. As a consequence, they are able to spend more aggressively on product development, marketing, sales and other product initiatives than we can. Many of these competitors have, among other things:

| ● | significantly greater name recognition; | |

| ● | larger and more established distribution networks; | |

| ● | additional lines of products and the ability to bundle products to offer higher discounts or other incentives to gain a competitive advantage; |

| 14 |

Our current competitors or other companies may at any time develop additional products that compete with our products. If any company develops products that compete with or are superior to our products, our revenue may decline. In addition, some of our competitors may compete by lowering the price of their products. If prices were to fall, we may not be able to improve our gross margins or sales growth sufficiently to maintain and grow our profitability.

Given our limited resources, we may not effectively manage our growth.

Our growth and expansion plan, which includes targeting high-growth segments with commercial products and working with third-party manufacturers and converters of biodegradable plastic products in the adoption of the Midori Biosolutions additive to enlarge our customer base, commencing and expanding our manufacturing capabilities of our product (assuming we acquire the intellectual property rights to the additive), strengthening our product leadership by developing new formulations in conjunction with customer demands and pursuing strategic alliances, requires significant management time and operational and financial resources. There is no assurance that we have the necessary operational and financial resources to manage our growth. This is especially true as we expand facilities and manufacture our organic additive on a larger commercial scale. In addition, rapid growth in our headcount and operations may place a significant strain on our management, administrative, operational and financial infrastructure. Failure to adequately manage our growth could have a material and adverse effect on our business, results of operations, financial condition and the quoted price of our Common Shares.

Disruptions in world financial markets could impede our ability to raise capital necessary to continue our operations and could have a material adverse impact on our future results of operations, financial condition or cash flows, and/or could cause the market price of our Common Shares to decline.

We face risks attendant to changes in economic environments, changes in interest rates, and instability in securities and capital markets, around the world, among other factors. Major market disruptions and the current adverse changes in market conditions and the regulatory climate in the United States and worldwide may impair our ability to raise capital under any future financial arrangements. We cannot predict how long the current market conditions will last. However, these recent and developing economic and governmental factors may impede our ability to raise the capital necessary to continue our operations, and may have a material adverse effect on future results of operations, financial condition or cash flows and could cause the price of our Common Shares to decline significantly.

Fluctuations in the costs of our raw materials and competitive products could have an adverse effect on our results of operations and financial condition.

Our results of operations are directly affected by the cost of our raw materials. Our product, the Midori Biosolutions additive, is based in large part on resin futures costing, for our carrier/backbone ingredient. Our additive is included in a masterbatch resin. If we are working with a Polyethylene terephthalate (“PET”) product, which is a type of plastic, we provide our additive in a PET masterbatch resin, if we are working with a Polypropylene (“PP”) product, which is also a type of plastic, then we provide our additive in a PP masterbatch resin. Our ability to offset the effect of raw material prices by increasing sales prices is uncertain. A further increase in the price differential between 10 to 25% based raw materials relative to petroleum-based plastics could have a negative impact on our results of operations and financial position.

Our operations in the U.S. are subject to regulation by the U.S. Food and Drug Administration to the extent the additive is a component of food and beverage containers.

The manufacture, sale and use of organic additives are subject to regulation by the U.S. Food and Drug Administration (the “FDA”). The FDA’s regulations are concerned with substances used in food packaging materials, not with specific finished food packaging products. Thus, food and beverage containers are in compliance with FDA regulations if the components used in the food and beverage containers: (i) are approved by the FDA as indirect food additives for their intended uses and comply with the applicable FDA indirect food additive regulations; or (ii) are generally recognized as safe for their intended uses and are of suitable purity for those intended uses.

| 15 |

The Midori Biosolutions additive has been cleared for use in food-contact applications by the FDA. Therefore, we believe that the Midori Biosolutions additive is in compliance with all FDA requirements. However, failure to comply with FDA regulations could subject us to administrative, civil or criminal penalties.

Regulatory changes applicable to us, or the products in our end-use markets, could adversely affect our financial condition and results of operations.

We and many of the applications for the products in the end-use markets in which we sell our products are regulated by various national and local regulations. Changes in those regulations could result in additional compliance costs, seizures, confiscations, recall or monetary fines, any of which could prevent or inhibit the development, distribution and sale of our products.

We may be liable for damages based on product liability claims brought against our customers in our end-use markets.

Many of our products may provide critical performance attributes to our customers’ products that will be sold to end users who could potentially bring product liability suits in which we could be named as a defendant. The sale of these products involves the risk of product liability claims. If a person were to bring a product liability suit against one of our customers, this customer may attempt to seek contribution from us. A person may also bring a product liability claim directly against us. A successful product liability claim or series of claims against us in excess of our insurance coverage for payments, for which we are not otherwise indemnified, could have a material adverse effect on our financial condition and results of operations.

If our products do not perform as expected or the reliability of the technology on which our product is based is questioned, we could experience lost revenue, delayed or reduced market acceptance of our product, increased costs and damage to our reputation.

The Midori Biosolutions additive we manufacture is incorporated into biodegradable plastic products that are sold by other companies and we have no control over the manufacture and production of those products. Our success depends on the market’s confidence that we can provide a reliable, high-quality organic additive product that can accelerate the speed of decomposer of biodegradable plastic products. Our reputation and the public image of our product and technologies may be impaired if our product fails to perform as expected. In the future, if our products experience, or are perceived to experience, a material defect or error, this could result in loss or delay of revenues, delayed market acceptance, damaged reputation, diversion of development resources, legal claims, increased insurance costs or increased service and warranty costs, any of which could harm our business. Such defects or errors could also narrow the scope of the use of our products, which could hinder our success in the market. Even after any underlying concerns or problems are resolved, any lingering concerns in our target market regarding our technology or any manufacturing defects or performance errors in our products could continue to result in lost revenue, delayed market acceptance, damaged reputation, increased service and warranty costs and claims against us.

| 16 |

If our supplier is unable to manufacture our product in sufficient quantities and in a timely manner, our operating results will be harmed, our ability to generate revenue could be diminished and our gross margin may be negatively impacted.