AN OFFERING STATEMENT PURSUANT TO REGULATION A RELATING TO THESE SECURITIES HAS BEEN FILED WITH THE SECURITIES AND EXCHANGE COMMISSION. INFORMATION CONTAINED IN THIS PRELIMINARY OFFERING CIRCULAR IS SUBJECT TO COMPLETION OR AMENDMENT. THESE SECURITIES MAY NOT BE SOLD NOR MAY OFFERS TO BUY BE ACCEPTED BEFORE THE OFFERING STATEMENT FILED WITH THE COMMISSION IS QUALIFIED. THIS PRELIMINARY OFFERING CIRCULAR SHALL NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY NOR MAY THERE BE ANY SALES OF THESE SECURITIES IN ANY STATE IN WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE UNLAWFUL BEFORE REGISTRATION OR QUALIFICATION UNDER THE LAWS OF SUCH STATE. THE COMPANY MAY ELECT TO SATISFY ITS OBLIGATION TO DELIVER A FINAL OFFERING CIRCULAR BY SENDING YOU A NOTICE WITHIN TWO BUSINESS DAYS AFTER THE COMPLETION OF THE COMPANY’S SALE TO YOU THAT CONTAINS THE URL WHERE THE FINAL OFFERING CIRCULAR OR THE OFFERING STATEMENT IN WHICH SUCH FINAL OFFERING CIRCULAR WAS FILED MAY BE OBTAINED.

PRELIMINARY OFFERING CIRCULAR

SUBJECT TO COMPLETION; DATED DECEMBER 22, 2025

Modern Mining Technology Corp.

Modern Mining Technology Corp.

1055 West Georgia Street, 1500 Royal Centre

Vancouver, British Columbia, V6E 4N7, Canada

Tel: +1 (984) 235-6778

www.modernmining.com

UP TO 7,058,823 COMMON SHARES

AGENT WARRANT FOR THE PURCHASE OF UP TO 211,764 COMMON SHARES

UP TO 211,764 COMMON SHARES UNDERLYING AGENT WARRANT

PRICE: $4.25 PER SHARE

The minimum investment in this offering is 200 Common Shares, or $850, unless waived by the Company in its sole discretion

| Price to Public | Commissions (1) | Proceeds to issuer (2) | Proceeds to other persons (4) | |||||||||||||

| Per share | $ | 4.25 | $ | 0.2975 | $ | 3.9525 | $ | 0.2543 | ||||||||

| Total Minimum of Public Offering (based on Minimum Quantitative Standards) | $ | 15,000,000 | $ | 1,050,000 | $ | 13,950,000 | $ | 1,795,000 | ||||||||

| Total Maximum of Public Offering | $ | 30,000,000 | $ | 2,100,000 | $ | 27,900,000 | $ | 1,795,000 | ||||||||

| Agent Warrant(3) | $ | 899,997 | $ | N/A | 1,124,996 | N/A | ||||||||||

| Per share of Common Shares underlying Agent Warrant (211,764 Shares) | $ | 5.3125 | $ | N/A | $ | 5.3125 | N/A | |||||||||

| Total Maximum | $ | 30,899,997 | $ | 2,100,000 | $ | 29,024,996 | $ | 1,795,000 | ||||||||

| (1) | We have engaged Digital Offering, LLC (“Digital Offering”) to act as lead selling agent (the “Lead Selling Agent”) to offer our common shares (the “Shares”) to prospective investors in this offering (the “Offering”) on a “best efforts” basis, which means that there is no guarantee that any minimum amount will be received by us in this Offering. In addition, the Selling Agent may engage one or more sub-agents or selected dealers to assist in its marketing efforts (Digital Offering, together with such sub-agents and/or dealers collectively, the “Selling Agents”). Digital Offering is not purchasing the Shares offered by us and is not required to sell any specific number or dollar amount of Shares in this Offering before a closing occurs. We will pay a cash commission of 7.0% to Digital Offering on sales of the Shares in this Offering and issue a warrant to Digital Offering to purchase a number of Shares equal to 2.5%of the total number of Shares sold in this Offering, exercisable for five years at an exercise price equal to 125% of the public offering price, subject to adjustments (the “Agent Warrant”). Digital Offering has agreed to remit .50% of this cash commission to the Company as a rebate to be applied towards the Company’s platform and marketing fees. See “Plan of Distribution” for details of compensation payable to the Selling Agent in connection with the Offering. |

| (2) | Does not account for the expenses of the Offering. See “Use of Proceeds” for estimated Offering expenses payable by the Company in connection with this offering. |

| (3) | The Agent Warrant is being issued as partial compensation to the Selling Agent. The value of the Agent Warrant set forth in the table above is based on the number of Shares underlying the Agent Warrant multiplied by the offering price of the Shares in this Offering of $4.25 per Share. The actual value of the Agent Warrant utilizing an options pricing model would be less than the amount indicated in the table. |

| (4) | We estimate that, in addition to the selling commission payable to the Lead Selling Agent, total expenses of the Offering will be approximately $1,795,000, assuming this Offering is fully subscribed. Includes (i) the $45,000 onboarding fee paid by the Company to Equifund Technologies LLC (“Equifund”), (ii) an estimated $500,000 in investor fees of $50 per investor payable by the Company to Equifund (assuming 10,000 investors in this Offering), (iii) payment processing fees payable by the Company to Equifund of approximately $650,000, and (iv) estimated expenses of the Offering (including the EDGARization, filing, printing, legal, marketing, accounting and other miscellaneous expenses) of approximately $600,000. See “Plan of Distribution” for further details. |

Modern Mining Technology Corp., a corporation formed under the laws of the Province of British Columbia (the “Company”, “we,” or “our”), is offering up to $30,000,000 or 7,058,823 Shares (the “Maximum Offering”) at a purchase price of $4.25 USD per share on a “best efforts” basis. Although the Company, may raise up to $30,000,000 in this offering, it may, in its sole discretion, decide to terminate the offering earlier, including after the Company reaches its internal target amount of $15,000,000. We are selling our Shares through a Tier 2 offering pursuant to Regulation A (Regulation A+) under the Securities Act of 1933, as amended (the “Securities Act”), and we intend to sell the Shares through the Selling Agent.

We intend to apply to have the Shares listed on Nasdaq Stock Exchange (the “Nasdaq”) under the symbol “MDRN.” To qualify for such listing, this Offering must meet the following minimum quantitative standards of the Nasdaq Capital Market: (i) 300 public holders of 100 Common Shares or more; (ii) 1,000,000 publicly held Common Shares; and (iii) an aggregate market value of publicly held Common Shares of $15.0 million (the “Minimum Quantitative Standards”). If approved, we intend to list the Shares on Nasdaq in the first quarter of 2026 following Nasdaq’s certification of our Form 8-A to be filed concurrently with qualification of, or a post-qualification amendment to, the Offering Statement of which this offering circular forms a part. If the Shares are not approved for listing on Nasdaq, we will not complete the Offering contemplated hereby. No assurance can be given that our application to list on Nasdaq will be approved or that an active trading market for the Shares will develop. The Shares are not currently listed or quoted on any exchange.

We will issue to the Selling Agent the Agent Warrant to purchase such number of Shares equal to 2.5% of the total number of Shares sold in this Offering, at a per Share price equal to 125% of the per Share price of the Shares offered hereby (subject to adjustments). The Offering Statement of which this Offering Circular forms a part also registers the issuance of the Shares issuable upon exercise of the Agent Warrant (although the Selling Agent has agreed not to sell the Agent Warrant or any of the shares issuable upon exercise of the Agent Warrant until six months after the commencement of the Offering). We do not intend to list the Agent Warrant on a national securities exchange or an over-the-counter quotation system. See “Plan of Distribution” for a description of these arrangements.

This is a continuous offering pursuant to Rule 251(d)(3)(i)(F) of Regulation A. We will commence this offering within two calendar days of the qualification by the SEC of the offering statement of which this offering circular forms a part and will continue to offer the Common Shares for an indefinite period of time (which may exceed 30 days from the date of qualification) until the offering is terminated. This Offering will terminate at the earliest of: (1) the date at which the Maximum Offering amount has been received by us, (2) one year from the date upon which the United States Securities and Exchange Commission (the “SEC” or “Commission”) qualifies the Offering Statement of which this Offering Circular forms a part, and (3) the date at which the Offering is earlier terminated by us in our sole discretion, including after the Company reaches its internal target amount raised of $15,000,000, and (4) May 31, 2026. This Offering is being conducted on a best-efforts basis. We intend to complete one closing in this Offering, and we will determine the closing date at our discretion based on our review of subscriptions received and in consultation with Digital Offering. While we intend to close the Offering as soon as possible following the qualification by the SEC of the offering statement of which this offering circular forms a part, we will not close the Offering until the Common Shares are approved for listing on Nasdaq. As a result, we will not close this Offering until we can establish that the Offering meets the Minimum Quantitative Standards. If we do not meet the Minimum Quantitative Standards by the Termination Date (as defined below), we will terminate this Offering and all funds tendered by investors with their subscriptions will be promptly returned to such investors in accordance with Rules 10b-9 and 15c2-4 under the Exchange Act. Once we have determined to close the Offering, we will inform investors of such closing date and the listing date via e-mail at least seven calendar days prior to the closing date, in accordance the terms of the subscription agreements executed by such investors. For more information regarding subscriptions and subscription agreements, see the section titled “Plan of Distribution-Procedures for Subscribing.” On the closing date, funds tendered by investors with their subscriptions will be made available to us and we will issue such investors their respective Common Shares.

INVESTING IN THE COMMON SHARES OF MODERN MINING TECHNOLOGY CORP. IS SPECULATIVE AND INVOLVES SUBSTANTIAL RISKS. YOU SHOULD PURCHASE THESE SECURITIES ONLY IF YOU CAN AFFORD A COMPLETE LOSS OF YOUR INVESTMENT. SEE “RISK FACTORS” BEGINNING ON PAGE 12 TO READ ABOUT THE MORE SIGNIFICANT RISKS YOU SHOULD CONSIDER BEFORE INVESTING IN THE COMMON SHARES OF THE COMPANY.

THE SEC DOES NOT PASS UPON THE MERITS OR GIVE ITS APPROVAL OF ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SOLICITATION MATERIALS. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION.

In particular, our securities have not been qualified for distribution by prospectus in Canada and may not be offered or sold in Canada during the course of their distribution hereunder except pursuant to a Canadian prospectus or prospectus exemption. The information in this OFFERING CIRCULAR is accurate only as of the date on its respective cover, regardless of the time of delivery of this OFFERING CIRCULAR or the time of any sale of our securities.

Sales of these securities will commence on approximately __________, 2025.

This Offering Circular follows the disclosure format of Part I of SEC Form S-1 pursuant to the general instructions of Part II(a)(1)(ii) of Form 1-A.

In the event that we become a reporting company under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), we intend to take advantage of the provisions that relate to “Emerging Growth Companies” under the JOBS Act of 2012. See “Implications of Being an Emerging Growth Company.”

TABLE OF CONTENTS

In this Offering Circular unless otherwise indicated or the context requires otherwise, the words “we,” “us,” “our,” the “Company,” or “our Company,” refer to Modern Mining Technology Corp., a Canadian corporation and its subsidiaries.

i

ABOUT THIS OFFERING CIRCULAR

As used in this Offering Circular, unless the context otherwise requires or otherwise states, references to “Modern Mining,” the “Company,” “we,” “us,” “our,” and similar references refer to Modern Mining Technology Corp., a corporation formed under the laws of the Province of British Columbia, Canada, and its subsidiaries.

Our functional currency is the Canadian dollar, the legal currency of Canada (“C$”) while the reporting currency is the U.S. dollar (“US$”). The functional and reporting currency of Urban Mining International Inc., our US wholly-owned subsidiary, is the U.S. dollar, the legal currency of the United States. Unless noted otherwise, all references to dollars herein are to US$.

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Our financial statements have been prepared in accordance with IFRS® Accounting Standards as issued by the International Accounting Standards Board (“IASB”) and interpretations issued by the International Financial Reporting Interpretations Committee (“IFRIC”). Our fiscal year ends on December 31 of each year as does our reporting year. Our most recent fiscal year ended on December 31, 2024. See Notes 2 and 3 to our audited consolidated financial statements for the years ended December 31, 2024 and 2023, included elsewhere in this Offering Circular, for a discussion of the basis of presentation, functional currency and summary of updated material accounting policies.

We have made rounding adjustments to some of the figures included in this Offering Circular. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that precede them.

ii

This summary highlights selected information contained elsewhere in this Offering Circular. This summary is not complete and does not contain all the information that you should consider before deciding whether to invest in our Shares. You should read this entire Offering Circular carefully, including the “Risk Factors” section, our historical consolidated financial statements and the notes thereto, each included elsewhere in this Offering Circular. Unless otherwise indicated or the context requires otherwise, the words “we,” “us,” “our,” the “Company,” or “our Company,” refer to Modern Mining Technology Corp., a Canadian corporation and its subsidiaries.

Our Company

Modern Mining Technology Corp. (formerly known as Urban Mining International Inc.) is a “landfill-to-commodity” focused business venture, offering a cleaner, safer, and lower-cost alternative compared to traditional mining operations. Our core business is aimed at processing and extracting strategic commodities from the vast, growing, and largely ignored global resource of electronic waste (“E-Waste”), and transforming these end-of-life landfill-bound materials into high-value resources. Value is captured by using our aqueous based processes to recover, process and refine commodity metals such as: gold, palladium, silver, copper and potentially 30 other metals.

Our Market

Our market consists of two parts — E-Waste feed supply and produced commodity sales.

E-Waste Feed Supply

The report, entitled Global E-Waste Monitor 2024 (the “Report”), provides that the world generated a staggering, and a record high, 62 million tonnes (Mt) of E-waste in 2022, representing billions of dollars worth of strategically-valuable resources dumped, squandered, and wasted. This is up 82% from 2010. In volume, this 62 million tonnes of E-waste would fill 1.55 million Semi Trucks, roughly enough pickup trucks to form a bumper-to-bumper line encircling the Earth’s equator. The Report also predicts global E-Waste will rise another 30% and reach 82 million tonnes annually by 2030 driven by increased technology use, shorter device life spans, and fewer repair options. The U.S. is the second largest generator of E-Waste in the world. The Report further indicates that in 2022 alone, approximately $62 billion worth of gold, silver, copper, platinum and other high-value, recoverable materials were wasted through landfill dumping or incineration burning, rather than being collected for treatment and reuse. It is Modern Mining’s business objective to address this situation and recover lost commodity materials from this E-Waste.

Commodity Sales

The Journal of Management Science and Engineering1 (the “Journal”) also produced findings that the cost to recycle E-Waste is significantly less than the cost of traditional mining. Lower production costs is a strategic advantage compared to traditional commodity producers. In addition to an increasing world demand for commodities, a number of large companies have announced their planned roadmaps to a more socially responsible supply chain. For example, in 2025, Apple announced that 24% of the materials it shipped in Apple products came from recycled or renewable sources, and it intends to use 100% renewable or recyclable materials in its products in the future, while Dell reemphasized its commitment to over 50% of product content being made from recycled, renewable or low emission materials by 2030. Also in 2025, Google announced that it used 20% recycled content in 2024 products with a goal to increase recycled materials usage. These are three examples of a growing trend of companies being more aware of their supply chains.

Our Business, Our Products and Services

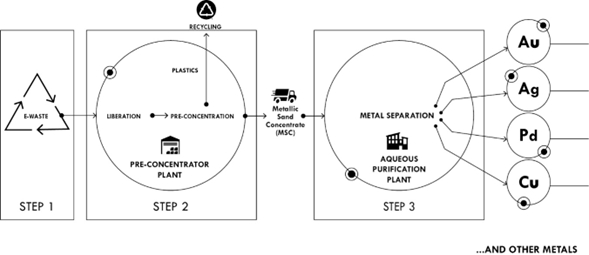

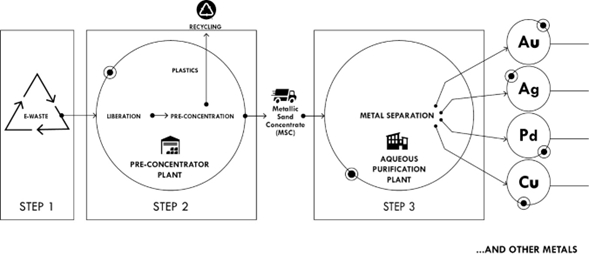

Our wholly-owned U.S. subsidiary, Urban Mining International Inc., largely focusing on research and development in the E-Waste sector, conducted internal and external bench scale and pilot plant testing from its former facilities in Raleigh, North Carolina to demonstrate proof of concept. The external tests were done to ensure that we would be able to liberate metals and separate them from the plastic in which they are imbedded. Metallic Sand Concentrate (“MSC”) was successfully created by this process. The internal tests were done to ensure that high-grade/upgraded E-waste feedstock would be able to undergo purification, which it was, and we were able to produce a doré bar. The test work was aimed at generating technical inputs needed for our proposed plan to design a commercial scale E-Waste processing facility using our proposed proprietary two-step Pre-Concentration Plant (“PCP”) and Aqueous Purification Plant (“APP”) process.

| 1 | See Comparing the Costs and Benefits of Virgin and Urban Mining; Zeng, Xia et al. |

1

To achieve our objectives, we have developed a two-step propriety process while our envisioned value-chain can be broken down into 3 main stages:

| 1) | We secure quality E-Waste feedstock from primary recyclers. |

| 2) | We separate the plastics from the metals using our proprietary pre-concentration methods. The plastics are then shipped to downstream third-party recyclers, suppliers, and certified waste handlers. |

| 3) | The concentrated metals streams can be sold as intermediate products, or treated though our proprietary aqueous purification process, and the purified metal products can then be sold into industrial supply chains. |

The following depicts the Company’s three main processing steps:

We plan to sell final products produced by the PCP and APP on the metal commodities markets into both domestic and international supply chains.

We have engaged a third-party process modelling and industrial optimization firm to assist in layout optimization, three dimensional (“3D”) modelling, and dynamic simulation studies on our first commercial scale PCP and APP. These plants will be co-located in our future commercial facility in North Carolina. Our current Greenville facility presently serves only as a pilot and demonstration plant that we intend to use to continue to optimize our processes that we ultimately plan to move to commercial scale production at a future location, or expand our current facility. In the long-term, we intend to secure a larger facility in the Raleigh or Greenville area of North Carolina to serve as our commercial-scale production facility although such future facility has yet to be identified as our current pilot plant facility still has significant capacity that we foresee being adequate in the short-term. The commercial PCP will be designed to treat approximately 8,000 tonnes of E-Waste per year and the commercial APP will be designed to be able to process concentrate from up to four PCPs.

After commercial start-up of our initial PCP and APP plants (expected to take approximately 18 months inclusive of a 6 month build-out, a 6-month commissioning program, and a 6 month ramp-up period), we believe that we can be a commercial producer of commodity materials, supplying both domestic and international supply chains with strategic metals. The processes we have developed for recycling E-Waste are environmentally beneficial compared to material going to landfill. Furthermore, we believe that the design of our proprietary processes (PCP and APP) will allow for the ability to scale and grow our business, and take advantage of a worldwide resource, E-Waste.

2

Our Competitive Strengths

| ● | Combining Four Core Market Trends |

Modern Mining anticipates benefiting from the overlap of four core market trends: (a) the growing global demand for commodity metals (examples — global push for electrification, growth in China, Ukraine rebuilding); (b) the importance of strengthening and developing transparent and socially responsible domestic supply chains, and onshoring the supply of critical materials; (c) the importance of developing sustainable and environmentally friendly driven solutions to support a ‘circular’ economy given the projected growth in global E-waste generation; and (d) the increasing importance of hedging against inflationary pressures.

| ● | Benefit from Proprietary Technology |

We have developed proprietary technologies that we believe set us apart from other E-Waste processors and from other commodity producers. We believe that our two-step approach of regional pre-concentration and centralized purification, combined with our modular and scalable design, will reduce capital and operating costs and will allow for a rapid expansion into other future potential major E-Waste generating locations.

| ● | Designed to Comply with Government Mandates |

Due to our anticipated high recovery rates and sustainable, environmentally friendly processes, and low/non-toxic controlled effluent, we believe we are well-positioned to comply with environmental guidelines around the world.

Our E-Waste recycling processes are environmentally friendly and do not generate any significant gaseous, liquid, or solids emissions only noise, air borne dust, and sewer discharges at this time. Our pre-concentration processes are purely water based with no chemical addition, and our purification methods utilize controlled aqueous based reagent blends in connection with our refined metal production. To that end, we have noise control and dust control systems in place and we currently use a closed-loop water recirculation system to manage effluent discharge. We envision that we will be well positioned to meet any environmental guidelines around the world when and if we expand our operations from our current facility in Greenville, North Carolina.

Global environmental guidelines that may be applicable to our operations include (a) the Basel Convention, which monitors the transboundary movements of hazardous and other wastes; (b) the UN Sustainable Development Goals encompassing E-Waste, such as SDG 6, which covers clean waste and sanitation, and SDG 12, which covers sustainable consumption and production patterns; (c) E-Waste legislation implemented around the world, such as Extended Producer Responsibility (EPR) programs to shift the burden of e-waste management from local municipalities to producers (d) U.S. Inflation Reduction Act; and (e) U.S. Senate hearings banning the export of E-waste (SEERA, June 20, 2023).

| ● | Superior to Current Standard E-Waste Recycling Processes |

We believe that our business plan sets us apart from others in the industry, in particular given our ability to be one of the low/non-carbon generating processors in the space with our proprietary aqueous based pre-concentration and purification technologies, versus the incineration-based methods of others in the industry. E-waste contains numerous toxic additives and hazardous substances that pose significant risk to human health and our environment if not disposed of and treated properly (examples — mercury, lead, heavy metals, brominated flame retardants, chlorofluorocarbons, hydrochlorofluorocarbons, dioxins). In China and other parts of the world, recycling of E-Waste can be a major hazard. Other locations include India and Ghana, Liberia, and Nigeria. Informal and primitive E-Waste recycling occurs regularly, where workers and others are exposed to dangerous chemicals with potentially long-term adverse health effects. Modern Mining plans to cleanly and safely process these substances, Incineration methods are extremely energy intensive methods2. The plastics are burned off resulting in major carbon dioxide and other hazardous emissions. Attempts to separate metals using pyrometallurgical methods result in significant metal losses as not all metals can be economically recovered. Modern Mining’s process, being aqueous-based, is largely carbon neutral, safer for both workers and for the environment, and allows for the recovery of a broader range of metals as separation and recovery is driven by physical methods and simple reagent addition, not complex pyrometallurgy.

| 2 | See Value-Added Products From Thermochemical Treatments of Contained E-Waste Plastics, Das, Gabriel, Tay and Lee. |

3

| ● | Decreased Risk Profile |

Traditional exploration and mining projects are inherently layered with significant risk as a consequence of having to deal with the earth’s crust and all of its natural variability. Major risks include: (a) exploration risk (the success rate of making a new discovery is low); (b) geological risk (the made grades of newly discovered deposits are generally decreasing); (c) engineering risk (the nature of newly discovered deposits is complex) and (d) geopolitical risk (various commodity resources are hosted in politically unstable and hostile jurisdictions).

In contrast, E-Waste is a man-made engineered product. It contains a very prescriptive blend and known quantity of strategic metals. As a result, the processing of E-Waste carries negligible exploration, geological, and geopolitical risk. Furthermore, as industry standard payment terms for our feedstock E-Waste are linked to the proportions of metals recovered, the impact and risk of fluctuating commodity prices are reduced as well. We believe feedstock E-Waste can also deliver 100 times better3 grades than traditional mined ores and the processing of E-Waste can carry less than 1/70th the capital expenditures4 of a traditional gold mine. Modern Mining aims to provide our stakeholders with the potential upside value associated with commodities investments, all the while minimizing downside risk exposure common to conventional mining projects.

| ● | Availability of Supply |

The amount of E-Waste produced by the world in 2016 was approximately 50 million tonnes5. With 5% of that E-Waste being printed circuit boards (“PCBs’), that amounts to 2.5 million tonnes of potential feedstock, of which only 17.4% was being recycled. At our current plant design capacity of approximately 8,000 tonnes per PCP, capturing “wasted” E-Waste would require over 250 concentrator plants. It is envisioned that 1 tonne of PCBs is equivalent in volume to three gaylord pallet boxes.

We currently have non-binding letters of intent to secure two times the quantity of feedstock needed to operate our initial PCP at 100% capacity, however, there are no guaranteed obligations for such suppliers to provide any amount of such feedstock to us.

| ● | Positioned to Benefit from Raising Commodity Prices |

We further believe we are positioned to benefit from any rise in commodity metal prices for our recovered metals: Gold, Silver, Copper, Platinum and Palladium.

| ● | Continuous Process Research and Development Plans |

We plan to have a continuing research and development program. This program will have two main goals. The first goal will be to optimize our proprietary processes to increase recoveries and reduce costs. The second goal will be to expand our core technology to be able to recover additional metals and to be able to process additional types of E-Waste feedstock.

| 3 | See S&P Capital IQ data publicly available which reports grade and tonnage values for the reserves and resources of every active primary gold mine currently in production across the world up to the date September 5, 2025. The average gold grade of global reserves and resources is approximately 1.24 g/t Au. We anticipate the average grade of our feedstock to be approximately136 g/t Au, which represents a grade 100 times better than traditional mined ores like gold. |

| 4 | See S&P Capital IQ data publicly available. The average capital expenditure for every operating and/or feasibility complete primary gold project in North America between August 2020 and August 2025 is approximately $700 million. Our estimated capital expenditure costs are anticipated to be approximately 10 million, yielding a figure of 1/70th the capital expenditure of traditional ore mines. |

| 5 | See Waste Printed Circuit Board Recycling: Conventional and Emerging Technology Approach, Muammer Kaya. |

4

Our Growth Strategy

The Company intends to expand its footprint to other locations around the United States and internationally (target of 1 PCP per year over 4 years), so that multiple concentrator plants are strategically located geographically near major third-party, primary recycling facilities, significantly reducing raw material transportation costs. Our plan is that the first additional PCPs will feed into the initial APP in North Carolina. Expansion of our aqueous purification capacity will be undertaken as material supply and economics dictate.

Our North Carolina Plant

In September 2022, we secured a facility lease containing approximately 10,000 square feet of effective working space in nearby Greenville, North Carolina to serve as our pilot plant and demonstration facility.

It is anticipated that this facility will allow us to operate at approximately up to 5% (avg. plant capacity of 1 tonne per day in short term ramp-up) of the processing capacity envisioned for our future planned commercial-scale plant. We intend to use this facility to house both our pilot PCP and APP equipment. We intend to operate our pilot and demonstration plant as needed for the following business purposes:

| ● | To demonstrate the operability and scalability of our full end-to-end process; |

| ● | To generate additional operating data for detailed engineering and scale-up studies for our commercial plant; |

| ● | To conduct process expansion studies; |

| ● | To optimize the performance objectives of our technology; and |

| ● | To serve as an operations training platform to help streamline the commissioning and start-up activities of our commercial plant. |

We elected to make North Carolina our U.S. processing home as a logical extension of our past local research efforts, favorable incentives, proximity to major logistics networks, and direct access to some of the world’s largest supplies of E-Waste through proximity to the densely populated eastern U.S. seaboard.

In the long-term, we intend to secure a larger facility in the Raleigh or Greenville area of North Carolina to serve as our commercial-scale production facility although such future facility has yet to be identified as our current pilot plant and demonstration facility still has significant capacity that we foresee being adequate in the short-term.

Company Information

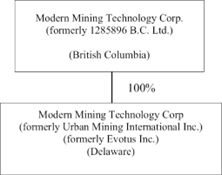

The Company was incorporated under the laws of the Province of British Columbia, Canada, as 1285896 B.C. Ltd, on January 26, 2021. In connection with the completion of the Merger (as defined below), the Company changed its name to its current name, “Modern Mining Technology Corp.”, on September 1, 2021.

Urban Mining International Inc. (“UMI”), our US wholly-owned subsidiary, was formed under the laws of the State of Delaware. UMI was first incorporated on August 8, 2017, under the name “Evotus Inc.” UMI changed its name from “Evotus Inc.” to “Urban Mining International Inc.” on October 14, 2020. On December 8, 2021, UMI changed its name from “Urban Mining International Inc.” to “Modern Mining Technology Corp.”

Our principal executive office and mailing address is located at 1055 West Georgia Street, 1500 Royal Centre, Vancouver, British Columbia, Canada V6E 4N7, and our telephone number is +1 (984) 235 6778. Our website is www.modernmining.com. The information contained on our website or accessible through our website is not incorporated into this Offering Circular.

5

Implications of Being an Emerging Growth Company and a Foreign Private Issuer

As an issuer with (i) less than $1.235 billion in total annual gross revenues during our last fiscal year, (ii) $700 million in market value of our capital stock held by non-affiliates and (iii) $1.07 billion in non-convertible debt over a three-year period, we will qualify as an “emerging growth company” under the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) and this status will be significant if and when we become subject to the ongoing reporting requirements of the Exchange Act upon filing a Form 8-A. An emerging growth company may take advantage of certain reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies. In particular, as an emerging growth company we:

| ● | will not be required to obtain an auditor attestation on our internal controls over financial reporting pursuant to the Sarbanes-Oxley Act of 2002, as amended; |

| ● | will not be required to provide a detailed narrative disclosure discussing our compensation principles, objectives and elements and analyzing how those elements fit with our principles and objectives (commonly referred to as “compensation discussion and analysis”); |

| ● | will not be required to obtain a non-binding advisory vote from our members on executive compensation or golden parachute arrangements (commonly referred to as the “say-on-pay,” “say-on-frequency” and “say-on-golden-parachute” votes); |

| ● | will be exempt from certain executive compensation disclosure provisions requiring a pay-for-performance graph and CEO pay ratio disclosure; |

| ● | may present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations, or MD&A; and |

| ● | will be eligible to claim longer phase-in periods for the adoption of new or revised financial accounting standards. |

We intend to take advantage of all of these reduced reporting requirements and exemptions, including the longer phase-in periods for the adoption of new or revised financial accounting standards, and hereby elect to do so. Our election to use the phase-in periods may make it difficult to compare our financial statements to those of non-emerging growth companies and other emerging growth companies that have opted out of the phase-in periods under Section 107 of the JOBS Act.

Under the JOBS Act, we may take advantage of the above-described reduced reporting requirements and exemptions for up to five years after our initial sale of common equity pursuant to a registration statement declared effective under the Securities Act of 1933, as amended (the “Securities Act”), or such earlier time that we no longer meet the definition of an emerging growth company. Note that this Offering, while a public offering, is not a sale of common equity pursuant to a registration statement, since the Offering is conducted pursuant to an exemption from the registration requirements. In this regard, the JOBS Act provides that we would cease to be an “emerging growth company” if we have more than $1.235 billion in annual revenues, have more than $700 million in market value of our capital stock held by non-affiliates, or issue more than $1.07 billion in principal amount of non-convertible debt over a three-year period.

In addition, upon the consummation of this Offering, we will report in accordance with the rules and regulations applicable to a “foreign private issuer.” As a foreign private issuer, we will take advantage of certain provisions under the rules that allow us to follow the applicable laws of the Province of British Columbia for certain corporate governance matters. Even when we no longer qualify as an emerging growth company, as long as we continue to qualify as a foreign private issuer under the Exchange Act, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

| ● | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations with respect to a security registered under the Exchange Act; |

| ● | the rules under the Exchange Act requiring the filing with the SEC of quarterly reports on Form 10-Q containing unaudited financial and other specified information, and current reports on Form 8-K upon the occurrence of specified significant events; and |

| ● | Regulation Fair Disclosure (“Regulation FD”), which regulates selective disclosures of material information by issuers. |

6

As a foreign private issuer, we will have four months after the end of each fiscal year to file our annual report on Form 20-F with the SEC. In addition, our executive officers, directors, and principal shareholders will be exempt from the requirements to report transactions in our equity securities and from the short-swing profit liability provisions contained in Section 16 of the Exchange Act.

Foreign private issuers, like emerging growth companies, are exempt from certain more stringent executive compensation disclosure rules. As such, even when we no longer qualify as an emerging growth company, as long as we continue to qualify as a foreign private issuer under the Exchange Act, we will continue to be exempt from the more stringent compensation disclosures required of public companies that are not foreign private issuers.

We may take advantage of these exemptions until such time as we are no longer a foreign private issuer. We are required to determine our status as a foreign private issuer on an annual basis at the end of our second fiscal quarter. We would cease to be a foreign private issuer at such time as more than 50% of our outstanding voting securities are held by U.S. residents and any of the following three circumstances applies:

| (i) | the majority of our executive officers or directors are U.S. citizens or residents; |

| (ii) | more than 50% of our assets are located in the United States; or |

| (iii) | our business is administered principally in the United States. |

In this Offering Circular, we have taken advantage of certain of the reduced reporting requirements as a result of being an emerging growth company and a foreign private issuer. Accordingly, the information that we provide in this Offering Circular may be different than the information you may receive from other public companies in which you hold equity interests. If some investors find our securities less attractive as a result, there may be a less active trading market for our securities and the prices of our securities may be more volatile.

7

RISK FACTORS SUMMARY

Risks Related to Our Business and Industry

| ● | we are an early-stage company with limited operating history and may never become profitable; |

| ● | our revenue depends on maintaining and increasing feedstock of E-Waste supply commitments as well as securing new customers and off-take agreements; |

| ● | in addition to commodity prices, our revenues will be primarily driven by the volume and composition of E-Waste feedstock materials to be processed at our future facilities and changes in the volume or composition of E-Waste feedstock processed could significantly impact our revenues and results of operations; |

| ● | our success will depend on our ability to economically source, extract and recover E-Waste, and to meet the market demand for sustainable and environmentally driven solutions for E-Waste processing; |

| ● | we may not be able to successfully implement our growth strategy, on a timely basis or at all; |

| ● | the development of our Greenville, North Carolina facility, and any future projects are subject to risks, including with respect to engineering, permitting, procurement, construction, commissioning and ramp-up, and we cannot guarantee that these projects will be completed in a timely manner, that our costs will not be significantly higher than estimated, or that the completed projects will meet expectations with respect to their productivity or the specifications of their and products, among others; |

| ● | we may be unable to manage future growth effectively; |

| ● | failure to materially increase recycling capacity and efficiency could have a material adverse effect on our business, results of operations or financial condition; |

| ● | future acquisitions and strategic investments could be difficult to integrate, divert the attention of key management personnel, disrupt our business, dilute shareholder value, and harm our results of operations and financial conditions; and |

| ● | expanding internationally involves risks that could delay our expansion plans and/or prohibit us from entering markets in certain jurisdictions, which could have a material adverse effect on our results of operations. |

| ● | Using a credit card to purchase Shares may impact the return on your investment as well as subject you to other risks inherent in this form of payment. |

Risks Related to our Regulatory Framework

| ● | We may not be able to obtain or maintain the necessary permits, licenses, or regulatory approvals required to operate or expand our business, which could curtail our operations. |

| ● | Changes in laws, regulations, or their enforcement could require costly operational changes or result in material liabilities. |

Risks Related to our Shares and this Offering

| ● | Significant shareholders, including holders of Investor Rights Warrants and Convertible Debentures, may exert substantial control over the company, potentially leading to conflicts of interest with other shareholders. |

| ● | As a foreign private issuer, we are subject to less stringent U.S. reporting and governance requirements, which may reduce transparency and shareholder protections compared to U.S. domestic companies. |

| ● | Listing on the Nasdaq will increase our regulatory burden and compliance costs, and failure to meet listing requirements could result in delisting and reduced liquidity for our shares. |

| ● | We may issue additional shares or equity securities without shareholder approval, diluting existing shareholders’ ownership and potentially depressing our share price. |

| ● | We are likely to be treated as a U.S. corporation for federal tax purposes, potentially resulting in double taxation and complex tax compliance obligations. |

| ● | Using a credit card to purchase shares may increase investment costs and expose investors to additional financial risks. |

8

THE OFFERING

| Securities Offered: | Maximum of 7,058,823 Shares. | |

| Offering Price per Share | $4.25 per Share. | |

| Minimum Investment | The minimum subscription is $850, or 200 Shares. However, the Company may waive the minimum subscription amount in its sole discretion. | |

| Best Efforts Offering | We may raise up to $30,000,000 in this offering. We may, in our sole discretion, decide to terminate the offering earlier, including after we reach our internal target amount of $15,000,000. | |

| Number of Shares outstanding immediately before the Offering | 5,082,200 Shares. | |

| Number of Shares outstanding after the Offering | 12,141,023 Shares, assuming the Company sells the Maximum Offering amount of Shares in the Offering, excluding the automatic conversion of the Debentures and the SAFE Notes, and automatic exercise of the Investor Rights Warrants on completion of the Offering (as each are defined herein). | |

| Use of Proceeds | If we raise the maximum amount contemplated in this Offering (excluding any exercise of the Agent Warrant), we estimate our net proceeds, after deducting estimated Offering expenses (including commissions) of approximately $3,895,000, will be approximately $26,105,000. We intend to use the proceeds from this Offering for (i) capital expenditures (45%), (ii) working capital and general corporate purposes, which may include repayment of one or more of certain interest bearing promissory notes that are payable on demand, in the event we do not have any other available capital (35%), (iii) marketing expenditures (15%) and (iv) research and development expenses (5%). See the “Use of Proceeds” section of this Offering Circular for details on our intended use of proceeds from this Offering. | |

| Risk Factors | Investing in our securities is highly speculative and involves a high degree of risk. You should carefully consider the information set forth in the “Risk Factors” section beginning on page 12 before deciding to invest in our securities. | |

| Selling Agent | We have engaged Digital Offering to serve as the Lead Selling Agent to assist in the placement of our Shares in this Offering on a “best efforts” basis. In addition, Digital Offering may engage one or more sub-agents or selected dealers to assist in its marketing efforts. See “Plan of Distribution” for further details. |

9

| Selling Agent Warrant | We have agreed to issue to Digital Offering warrants to purchase such number of Shares equal to 2.5% of the total number of Shares sold in this Offering at an exercise price equal to 125% of the public offering price of the Shares sold in this Offering (subject to adjustments). The Agent Warrant will be exercisable at any time, and from time to time, in whole or in part, commencing from the date of issuance and expiring on the fifth anniversary of the commencement date of sales in this Offering. The Agent Warrant will have a cashless exercise provision and will provide for registration rights with respect to the registration of the Shares underlying the Agent Warrant. | |

| Pooling Agreements | The holders of the Investor Rights Warrants and the Convertible Debentures, with Kuljit Basi acting as their representative, have entered into pooling agreements with the Company dated September 11, 2025 (together, the “Pooling Agreements”). The Pooling Agreements impose contractual resale restrictions on “pooled securities,” defined to include all Investor Rights Warrants, all Convertible Debentures, and all securities underlying the Investor Rights Warrants and Convertible Debentures held by the participating securityholders. The Pooling Agreement restrictions prohibit securityholders from selling, transferring, pledging, or otherwise disposing of any legal or beneficial interest in their pooled securities for a period of 180 days following the Company’s listing on the Nasdaq, subject to certain exceptions for earlier release of up to a maximum of 50% of the pooled securities in the event certain trading price and volume thresholds are achieved over certain time periods. See “Plan of Distribution” for further details. The holders of Shares issued in exchange for shares of common stock of UMI pursuant to the Merger Agreement (as defined herein) are subject to contractual lock-up which prohibits the holder from selling, transferring, pledging, or otherwise disposing of any legal or beneficial interest in their Shares for a period of 12 months following the Company’s listing on the Nasdaq. 20% of such shares will be released on the date that is 12 months following the listing date, and 20% will be released on the date that is each of 4, 8, 12 and 16 months following such date. | |

| Lock-Up Agreements | Except as described below, our officers, directors and certain of our stockholders have agreed, or will agree, with Digital Offering, subject to certain exceptions, that, without the prior written consent of Digital Offering, they will not, directly or indirectly, during the period of six months following the closing of this Offering, offer, pledge, sell, contract to sell, sell any option or contract to purchase, purchase any option or contract to sell, grant any option, right or warrant for the sale of, or otherwise dispose of or transfer any Common Shares or any securities convertible into or exchangeable or exercisable for Common Shares, whether now owned or hereafter acquired by them or with respect to which they have or hereafter acquire the power of disposition; or enter into any swap or any other agreement or any transaction that transfers, in whole or in part, the economic consequence of ownership of the Common Shares, whether any such swap or transaction is to be settled by delivery of the Common Shares or other securities, in cash or otherwise | |

| Termination of the Offering | This Offering will terminate at the earlier of: (1) the date on which the Maximum Offering amount has been sold, (2) the date which is one year after this Offering has been qualified by the Commission (3) the date on which this Offering is earlier terminated by us in our sole discretion, including after the Company reaches its internal target amount raised of $15,000,000, and (4) May 31, 2026. | |

| Continuous Offering; Termination of the Offering | This is a continuous offering pursuant to Rule 251(d)(3)(i)(F) of Regulation A. We will commence this Offering within two calendar days of the qualification by the SEC of the offering statement of which this offering circular forms a part and will continue to offer the Common Shares for an indefinite period of time (which may exceed 30 days from the date of qualification) until the Offering is terminated. This Offering will terminate at the earliest of: (a) the date at which the maximum offering amount has been received by us, (b) one year from the date upon which the SEC qualifies the offering statement of which this Offering Circular forms a part, and (c) the date at which the offering is earlier terminated by us in our sole discretion. | |

| Closing of the Offering | We intend to complete one closing for this Offering and will determine the closing date at our discretion based on our review of subscriptions received and in consultation with Digital Offering. While we intend to close the offering as soon as possible following the qualification by the SEC of the offering statement of which this offering circular forms a part, we will not close the offering until the Common Shares are approved for listing on Nasdaq. As a result, we will not close this offering until we can establish that the offering meets the Minimum Quantitative Standards. If we do not meet the Minimum Quantitative Standards by the Termination Date, we will terminate this Offering and all funds tendered by investors with their subscriptions will be promptly returned to such investors in accordance with Rules 10b-9 and 15c2-4 under the Exchange Act. Once we have determined to close the offering, we will inform investors of such closing date and the listing date via e-mail at least seven calendar days prior to the closing date, in accordance with the terms of the subscription agreements executed by such investors. On the closing date, funds tendered by investors with their subscriptions will be made available to us and we will issue such investors their respective Common Shares. | |

| Proposed Listing | We intend to apply to have our Shares listed on the Nasdaq under the symbol “MDRN.” If our Shares are not approved for listing on Nasdaq, we will not complete the Offering contemplated hereby. |

10

Summary Financial Data

The following tables summarize our unaudited consolidated financial data for our business for each of the six months ended June 30, 2025 and 2024, and audited consolidated financial data for our business for each of the financial years ended December 31, 2024 and 2023 and should be read in conjunction with our audited financial statements and related notes contained elsewhere in this Offering Circular and the information under “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Our financial statements have been prepared in accordance with IFRS® Accounting Standards as issued by the International Accounting Standards Board (“IASB”) and interpretations issued by the International Financial Reporting Interpretations Committee (“IFRIC”). Our historical results are not necessarily indicative of our future results.

Balance Sheet Data

| June

30, 2025 | December 31, 2024 | December 31, 2023 | ||||||||||

| Assets | ||||||||||||

| Total current assets | $ | 436,897 | $ | 206,420 | $ | 75,230 | ||||||

| Total assets | $ | 478,367 | $ | 330,832 | $ | 392,670 | ||||||

| Liabilities and stockholders’ Equity | ||||||||||||

| Total current liabilities | $ | 5,496,815 | $ | 8,038,773 | $ | 2,971,096 | ||||||

| Total liabilities | 9,477,226 | 8,133,419 | 6,595,633 | |||||||||

| Total stockholders’ equity | (8,998,859 | ) | (7,802,587 | ) | (6,202,963 | ) | ||||||

| Total liabilities and stockholders’ equity | $ | 478,367 | $ | 330,832 | $ | 392,670 | ||||||

Statement of Operations Data

| For

the six months ended June 30, | ||||||||

| 2025 | 2024 | |||||||

| Revenue | $ | - | $ | - | ||||

| Total operating expenses | (568.560 | ) | (1,157,761 | ) | ||||

| Loss from operations | (568,560 | ) | (1,157,761 | ) | ||||

| Interest and other income | 546 | 11,488 | ||||||

| Interest and accretion expense | (173,360 | ) | (149,174 | ) | ||||

| Unrealized gain (loss) on warrant liability | 331,242 | |||||||

| Net loss for the period | (741,374 | ) | (964,205 | ) | ||||

| Foreign currency translation adjustment | (454,898 | ) | 303,286 | |||||

| Comprehensive loss for the period | $ | (1,196,272 | ) | $ | (660,919 | ) | ||

| For

the years ended December 31, | ||||||||

| 2024 | 2023 | |||||||

| Revenue | $ | - | $ | - | ||||

| Total operating expenses | (2,350,891 | ) | (2,259,124 | ) | ||||

| Loss from operations | (2,350,891 | ) | (2,259,124 | ) | ||||

| Interest and other income | 24,915 | 15,212 | ||||||

| Interest and accretion expense | (307,757 | ) | (271,630 | ) | ||||

| Unrealized gain (loss) on warrant liability | 328,512 | (186,508 | ) | |||||

| Net loss for the year | (2,305,221 | ) | (2,702,050 | ) | ||||

| Foreign currency translation adjustment | 705,597 | (133,447 | ) | |||||

| Comprehensive loss for the year | $ | (1,599,624 | ) | $ | (2,835,497 | ) | ||

11

An investment in our Shares involves a high degree of risk. The SEC requires that we identify risks that are specific to our business and our financial condition. You should carefully consider the following risk factors and the other information in this Offering Circular before investing in our securities. Our business and results of operations could be seriously harmed by any of the following risks. The risks set out below are not the only risks we face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially adversely affect our business, financial condition and/or operating results. If any of the following risks actually occur, our business, reputation, financial condition, results of operations, revenue and future prospects could be materially adversely affected and you could lose all or part of your investment in the Shares. In such case, the value of our securities could decline, and you may lose all or part of your investment.

Risks Related to our Business and Industry

We are an early-stage company with limited operating history and may never become profitable.

We are a development stage company with no meaningful commercial revenues and only net losses. For the six months ended June 30, 2025, our revenue was $Nil and we recorded a net loss of $741,374 and for the year ended December 31, 2024, our revenue was $Nil and we recorded a net loss of $2,305,221. For the six months ended June 30, 2024, our revenue was $Nil and we recorded a net loss of $964,205 and for the year ended December 31, 2023, our revenue was $Nil and we recorded a net loss of $2,702,050. Our primary sources of liquidity are currently the funds raised from the issuance of the offering of the Urban Mining International, Inc. UMI Warrants, our common shares, the 2022 Debenture Offering, the 2024 Debenture Offering, the funds borrowed from Blue Bird Capital Enterprises, LLC, the funds borrowed from certain other shareholders and the funds borrowed from former directors and officers. We expect both our capital and operating expenditures will increase significantly in connection with our ongoing activities.

We expect to require adequate proceeds generated from this Offering and additional funding to expand our operations and develop our sales and distribution channels. However, there can be no assurance that additional funding will be available to us for the development of our business, which will require the commitment of substantial resources. Accordingly, you should consider our prospects in light of the costs, uncertainties, delays and difficulties frequently encountered by companies in the early stages of development. Potential investors should carefully consider the risks and uncertainties that an early-stage company with a very limited operating history will face. In particular, potential investors should consider that we may be unable to:

| ● | successfully implement or execute our business plan if our business plan is not sound or for other reasons; |

| ● | obtain sufficient and affordable quantities of high quality feedstock; |

| ● | effectively process the E-Waste we obtain to produce sufficient quantities of commercially saleable commodities; |

| ● | develop our proposed facilities; |

| ● | effectively pursue business opportunities, including potential acquisitions; |

| ● | adjust to changing conditions or keep pace with increased demand; |

| ● | attract and retain an experienced management team; or |

| ● | raise sufficient funds in the capital markets to effectuate our business plan, including building production capacity. |

We believe that our performance and future success is dependent on multiple factors that present significant opportunities for us to increase revenues, but also pose risks and challenges. If we cannot successfully develop, manufacture and distribute our products, or if we experience difficulties in the development process, such as capacity constraints, quality control problems or other disruptions, we may not be able to develop or offer market-ready commercial products at acceptable costs, which would adversely affect our ability to effectively enter the market or expand our market share. A failure by us to achieve a low-cost structure through economies of scale or improvements in cultivation, manufacturing or distribution processes would have a material adverse effect on our commercialization plans and our business, prospects, results of operations and financial condition.

12

Our revenue depends on obtaining, maintaining and increasing feedstock of E-Waste supply commitments as well as securing new customers and off-take agreements.

We must obtain, maintain and grow our E-Waste feedstock supply commitments as well as new customers (including through entry into off-take agreements for our concentrates and products) in order to generate revenue. As of the date of this Offering Circular, we have no firm commitments for the supply of E-Waste feedstock to our operating facility, and only have non-binding letters of intent from numerous suppliers. Such suppliers have no contractual obligation to provide us any E-waste feedstock for our current operations. Going forward, we may be unable to secure contracts with such E-Waste feedstock vendors and even if we do secure such contracts, E-Waste feedstock suppliers may change or delay supply contracts for any number of reasons, such as force majeure or government approval factors that are unrelated to Modern Mining. Likewise, we do not currently have any off-take agreements for the sale of our products. Even if we do secure such off-take contracts, suppliers may fail to perform under their contracts for similar reasons outlined above.

As a result, in order to operate our business, we must develop and obtain feedstock supply and product off-take agreements. However, it is difficult to predict whether and when we will secure such commitments and/or contracts due to competition for suppliers and the lengthy process of negotiating supplier agreements as well as buyer contracts, all of which may be affected by factors that we do not control, such as market and economic conditions, financing arrangements, commodity prices, environmental issues and government approvals.

In addition to commodity prices, our revenues will be primarily driven by the volume and composition of E-Waste feedstock materials to be processed at our future facilities and changes in the volume or composition of E-Waste feedstock processed could significantly impact our revenues and results of operations.

Our future revenues depend on processing high volumes of E-Waste feedstock, and our revenues will be directly impacted by the chemistry of the feedstock processed, particularly as market chemistries shift. Certain feedstock chemistries produce raw materials for which we receive higher prices than others. A decline in overall volume of E-Waste feedstock processed, or a decline in volume of chemistries with higher priced content relative to other chemistries, could result in a significant decline in our revenues, which in turn would have a material impact on our results of operations.

Our success will depend on our ability to economically source, extract, and recover E-Waste, and to meet the market demand for sustainable and environmentally driven solutions for E-Waste processing.

Our future business depends in large part on our ability to economically and effectively process and recover strategic metals and materials from E-Waste, and to meet the market demand for sustainable and environmentally driven solutions for E-Waste processing. Although we have conducted research and development (“R&D”) and testing of our proprietary two-step PCP and APP process, we will need to scale our processing capacity in order to successfully implement our growth strategy and plan to do so in the future by, among other things, successfully building and developing our first commercial facility in Greenville, North Carolina. Although we have experience in processing E-Waste materials in our previous facilities, such operations were conducted on a limited scale, and we have not yet developed or operated a facility on a commercial scale to produce and sell end products. We do not know whether we will be able to develop efficient and low-cost processing capabilities, or whether we will be able to secure reliable sources of supply, in each case that will enable us to meet the production standards, costs and volumes required to successfully process E-Waste and meet our business objectives and customer needs. Even if we are successful in high-volume recycling and processing in our future facilities, we do not know whether we will be able to do so in a manner that avoids significant delays and cost overruns, including as a result of factors beyond our control, such as problems with suppliers, or in time to meet the commercialization schedules of future recycling needs or to satisfy the requirements of our customers. Our ability to effectively reduce our cost structure over time is limited by the fixed nature of many of our planned expenses in the near-term, and our ability to reduce long-term expenses is constrained by our need to continue investment in our growth strategy. Any failure to develop and scale such manufacturing processes and capabilities within our projected costs and timelines could have a material adverse effect on our business, results of operations or financial condition.

13

We may not be able to successfully implement our growth strategy, on a timely basis or at all.

Our future growth, results of operations and financial condition depend upon our ability to successfully implement our growth strategy, which, in turn, is dependent upon a number of factors, some of which are beyond our control, including our ability to:

| ● | economically process E-Waste and recover strategic metals and materials and meet customers’ business needs; |

| ● | effectively introduce methods for higher extraction and higher recovery rates of strategic metals, including metals recovery from R&D initiatives; |

| ● | complete the construction of our future facilities, including the Greenville, North Carolina facility, at a reasonable cost and on a timely basis; |

| ● | effectively ramp-up our facilities to expected performance targets; |

| ● | invest and keep pace in technology, research and development efforts, and the expansion into additional commodities recovery beyond gold, silver, copper, and palladium; |

| ● | secure and maintain required strategic supply arrangements, and obtain appropriate operating environmental and industrial quality certifications; |

| ● | effectively compete in the markets in which we operate; and |

| ● | attract and retain management or other employees who possess specialized knowledge and technical skills. |

There can be no assurance that we can successfully achieve any or all of the above initiatives in the manner or time period that we expect. Further, achieving these objectives will require investments that may result in both short-term and long-term costs without generating any current revenue and therefore may be dilutive to earnings. We cannot provide any assurance that we will realize, in full or in part, the anticipated benefits we expect to generate from our growth strategy. Failure to realize those benefits could have a material adverse effect on our business, results of operations or financial condition.

The development of our Greenville, North Carolina facility, and future projects, if any, are subject to risks, including with respect to engineering, permitting, procurement, construction, commissioning and ramp-up, and we cannot guarantee that these projects will be completed in a timely manner, that our costs will not be significantly higher than estimated, or that the completed projects will meet expectations with respect to their productivity or the specifications of their end products, among others.

Our Greenville, North Carolina facility (herein, the “Facility”), and future projects, if any, are subject to development risks, including with respect to engineering, permitting, procurement, construction, commissioning and ramp-up. Because of the uncertainties inherent in estimating construction and labor costs and the potential for the scope of a project to change, it is relatively difficult to evaluate accurately the total funds that will be required to complete the Facility, or future projects. Further, our estimate of the amount of time it will take to complete the Facility, or future projects, are based on assumptions about the timing of engineering studies, permitting, procurement, construction, commissioning and ramp-up, all of which can vary significantly from the time an estimate is made to the time of completion. We cannot guarantee that the costs of the Facility, or future projects, will not be higher than estimated, or that we will have sufficient capital to cover any increased costs, or that we will be able to complete the Facility, or future projects, within expected timeframes. Any such cost increases or delays could negatively affect our results of operations and ability to continue to grow, particularly if the Facility, or any future project, cannot be completed. Further, there can be no assurance that the Facility will perform at the expected production rates or unit costs, or that the end products will meet the intended specifications.

We may be unable to manage future growth effectively.

Even if we can successfully implement our growth strategy, any failure to manage our growth effectively could materially and adversely affect our business, results of operations and financial condition. We intend to expand our operations around the United States, and internationally in the long-term, which will require us to hire and train new employees; accurately forecast supply and demand, production and revenue; control expenses and investments in anticipation of expanded operations; establish new or expand current design, production, and sales and service facilities; and implement and enhance administrative infrastructure, systems and processes. Future growth may also be tied to acquisitions, and we cannot guarantee that we will be able to effectively acquire other businesses or integrate businesses that we acquire. Failure to efficiently manage any of the above could have a material adverse effect on our business, results of operations or financial condition.

14

Failure to materially increase recycling capacity and efficiency could have a material adverse effect on our business, results of operations or financial condition.

Although our future commercial facility in North Carolina is expected to have an annual total processing capacity of approximately 8,000 tonnes of E-Waste, the future success of our business depends in part on our ability to significantly increase our recycling capacity and efficiency. We may be unable to expand our business, satisfy demand from customers, maintain our competitive position and achieve profitability if we are unable to build and operate any future facilities. The construction of future facilities will require significant cash investments and management resources and may not meet our expectations with respect to increasing capacity and efficiency. For example, if there are delays in any future planned facilities, or if our facilities do not meet expected performance standards or are not able to produce materials that meet the quality standards we expect, we may not meet our target for adding capacity, which would limit our ability to increase sales and result in lower-than-expected sales and higher than expected costs and expenses. Failure to drastically increase recycling and processing capacity or otherwise satisfy customers’ demands may result in a loss of market share to competitors, damage our relationships with our key customers, a loss of business opportunities or otherwise materially adversely affect our business, results of operations or financial condition.

We have not yet demonstrated commercial-scale metal recoveries from E-Waste, and actual operating results may differ materially from our laboratory and pilot-plant projections.

Although our proprietary PCP and APP processes have produced encouraging bench-scale and pilot-scale results, we have no experience operating these processes at the throughput rates, metal concentrations and continuous-run durations contemplated for our first commercial facility. Scale-up frequently introduces unanticipated engineering challenges, lower recoveries, higher reagent consumption, fouling, wear, downtime and maintenance costs. Should recoveries or unit costs deviate adversely from our current projections, we may be unable to meet offtake specifications, satisfy lender covenants or achieve positive operating margins, any of which would have a material adverse effect on our business.

Future acquisitions and strategic investments could be difficult to integrate, divert the attention of key management personnel, disrupt our business, dilute shareholder value, and harm our results of operations and financial condition.

We may in the future seek to acquire or invest in, businesses, products, or technologies that we believe could complement our operations or expand our breadth, enhance our capabilities, or otherwise offer growth opportunities. While our growth strategy includes broadening our product offerings, implementing an aggressive marketing plan and employing product diversification, there can be no assurance that our systems, procedures and controls will be adequate to support our operations as they expand. We cannot assure you that our personnel, systems, procedures or controls will be adequate to support our operations in the future or that we will be able to successfully implement appropriate measures consistent with our growth strategy. As part of our planned growth and diversified product offerings, we may have to implement new operational and financial systems, procedures and controls to expand, train and manage our employee base, and maintain close coordination among our staff. We cannot guarantee that we will be able to do so, or that if we are able to do so, we will be able to effectively integrate them into our existing staff and systems.

Additionally, the integration of our acquisitions and pursuit of potential future acquisitions may divert the attention of management and cause us to incur various expenses in identifying, investigating, and pursuing suitable acquisitions, whether or not they are consummated. Any acquisition, investment or business relationship may result in unforeseen operating difficulties and expenditures. In addition, we have limited experience in acquiring other businesses. Specifically, we may not successfully evaluate or utilize the acquired products, assets or personnel, or accurately forecast the financial impact of an acquisition transaction, including accounting charges. Moreover, the anticipated benefits of any acquisition, investment, or business relationship may not be realized, or we may be exposed to unknown risks or liabilities associated with our acquisitions.

15

We may not be able to find and identify desirable acquisition targets or we may not be successful in entering into an agreement with any one target. Acquisitions could also result in dilutive issuances of equity securities or the incurrence of debt, which could harm our results of operations. In addition, if an acquired business fails to meet our expectations, our business, results of operations, and financial condition may suffer. In some cases, minority shareholders may exist in certain of our non-wholly-owned acquisitions and may retain minority shareholder rights which could make a future change of control or necessary corporate approvals for actions more difficult to achieve and/or more costly.

We may also make strategic investments in early-stage companies developing products or technologies that we believe could complement our business or expand our breadth, enhance our technical capabilities, or otherwise offer growth opportunities. These investments may be in early-stage private companies for restricted shares. Such investments are generally illiquid and may never generate value. Further, the companies in which we invest may not succeed, and our investments could lose their value.

Expanding internationally involves risks that could delay our expansion plans and/or prohibit us from entering markets in certain jurisdictions, which could have a material adverse effect on our results of operations.

At present, we have no immediate intention to expand our operations outside of North America. If we were to expand more broadly and pursue international operations, those operations would be subject to certain risks inherent in doing business abroad, including:

| ● | political, civil and economic instability; |

| ● | corruption risks; |

| ● | trade, customs and tax risks; |

| ● | currency exchange rates and currency controls; |

| ● | limitations on the repatriation of funds; |

| ● | insufficient infrastructure; |

| ● | restrictions on exports, imports and foreign investment; |

| ● | increases in working capital requirements related to long supply chains; |

| ● | changes in labor laws and regimes and disagreements with the labor force; |

| ● | difficulty in protecting intellectual property rights and complying with data privacy and protection laws and regulations; and |

| ● | different and less established legal systems. |

We will be dependent on our facilities. If one or more of our facilities become inoperative, capacity constrained or if operations are disrupted, our business, results of operations or financial condition could be materially adversely affected.

Our revenue will be dependent on the continued operations of our facilities, including our Greenville, North Carolina head office/processing facility and any other facilities we may develop in the future. To the extent that we experience any operational risk including, among other things, fire and explosions, severe weather and natural disasters (such as floods and hurricanes), failures in water supply, major power failures, equipment failures (including any failure of our information technology, air conditioning, and cooling and compressor systems), a cyber-attack or other incident, failures to comply with applicable regulations and standards, labor force and work stoppages, including those resulting from local or global pandemics or otherwise, or if our current or future facilities become capacity constrained, we may be required to make capital expenditures even though we may not have sufficient available resources at such time.

16