PART II – INFORMATION REQUIRED IN OFFERING CIRCULAR

Preliminary Offering Circular dated July 14, 2025

An Offering Statement pursuant to Regulation A relating to these securities has been filed with the Securities and Exchange Commission. Information contained in this Preliminary Offering Circular is subject to completion or amendment. These securities may not be sold nor may offers to buy be accepted before the Offering Statement filed with the Commission is qualified. This Preliminary Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy nor may there be any sales of these securities in any state in which such offer, solicitation or sale would be unlawful before registration or qualification under the laws of any such state. We may elect to satisfy our obligation to deliver a Final Offering Circular by sending you a notice within two business days after the completion of our sale to you that contains the URL where the Final Offering Circular or the Offering Statement in which such Final Offering Circular was filed may be obtained.

VOCODIA HOLDINGS CORP

30,000,000,000 Shares of Common Stock

Including 480,000,000 Shares of Common Stock

held by the Selling Shareholders

Vocodia Holdings Corp, a Wyoming corporation is offering up to 30,000,000,000 (Thirty Billion) shares of common stock, par value $0.0001 per share, of the Company (“Common Stock”), including 480,000,000 shares of Common Stock being offered by the Selling Shareholders, on a “best efforts” basis at an offering price between $.0001 and $.0005 per share.

Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

Shares offered by the Company will be sold through the Company’s executive officers and directors on a “best-efforts” basis. We may also engage sales agents licensed through the Financial Industry Regulatory Authority (“FINRA”) and pay such agents cash and/or stock-based compensation, which will be announced through a supplement to this Offering Circular. The sale of Shares will commence within two calendar days of the date the Offering Statement to which this Offering Circular relates is qualified by the Securities Exchange Commission (“SEC”) and continue for one year thereafter or until all shares have been sold, whichever occurs first. Notwithstanding, the Company may elect to extend this offering for an additional 90 days or cancel or terminate it at any time.

The per share public offering price of the shares to be sold by the Selling Shareholders will be fixed as the same price as the Shares to by the Company. The qualification of the Selling Shareholders’ shares of common stock does not mean that the Selling Shareholders will offer or sell any shares. We will not receive any proceeds from any sale or disposition of shares by the Selling Shareholders. In addition, we will pay all fees and expenses incident to the qualification of the resale of shares of common stock by the Selling Shareholders. The Selling Shareholders may offer their common stock from time to time directly or through one or more broker-dealers or agents. For additional information on the possible methods of sale that may be used by the Selling Shareholders, refer to the section of this offering circular entitled “Selling Shareholders -- Plan of Distribution”.

Investing in our Common Stock involves a high degree of risk. These are speculative securities. You should purchase these securities only if you can afford a complete loss of your investment. See “Risk Factors” starting on page 7 for a discussion of certain risks that you should consider in connection with an investment in our Common Stock.

| Price to Public | Underwriting discount and commissions (1) |

Proceeds to issuer (2) |

Proceeds to other persons (3) |

|||||||||||||

| Per share | Between $0.0001 and $.0005 | $ | 0.00 | $ | 0.0001 to $.0005 | $ | 0.0001 to $.0005 | |||||||||

| Total Maximum (5) | $ | 3,000,000 | $ | 0.00 | $ | 2,952,000 | $ | 48,000 | ||||||||

| (1) | The Company does not intend to engage a placement agent for this offering but may engage sales associates after this offering commences. Nonetheless, the Company as part of its convertible note with DebtFund LP, the Company has agreed that Alpine Securities Corporation to act as investment banker/placement agent and be entitled to placement agent compensation. If the investor or funder is a person introduced by Alpine, the placement agent fee shall be 10% of the amount raised; otherwise, the placement agent fee payable to Alpine shall equal 5% of the amount raised in the related Finance Transaction. |

| (2) | Does not include expenses of the offering or reflect the issuance of Bonus Shares; see “Plan of Distribution and Selling Stockholders.” |

| (3) | The proceeds represent amounts to be paid to the selling stockholders listed in this Offering Circular. See “Plan of Distribution and Selling Stockholders.” |

The company is seeking to raise up to $3,000,000 from the sale of Common Stock. All investors will be required to purchase securities pursuant to a subscription agreement which appears as an Exhibit to the Offering Statement of which this Offering Circular forms a part, and which is irrevocable. This contains exclusive forum and jury waiver provisions which are similarly irrevocable; see “Risk Factors,” “Securities Being Offered – Common Stock – Forum Selection Provision,” and “Plan of Distribution and Selling Stockholders – Jury Trial Waiver.”

This offering (the “Offering”) will terminate at the earlier of the date at which the maximum offering amount has been sold or one year from the date this Offering is qualified by the SEC, unless extended in the sole discretion of the Company. At least every 12 months after this offering has been qualified by the SEC, the Company will file a post-qualification amendment to include the company’s recent financial statements. The Offering covers a number of securities that we reasonably expect to offer and sell within one year, although the offering statement of which this offering circular forms a part may be used for up to three years and 180 days under certain conditions. The offering is being conducted on a best-efforts basis without any minimum target. Provided that an investor purchases shares in the amount of the minimum investment, $500, there is no minimum number of shares that needs to be sold in order for funds to be released to the Company and for this Offering to close, which may mean that the company does not receive sufficient funds to cover the cost of this Offering. The company may undertake one or more closings on a rolling basis. After each closing, funds tendered by investors will be made available to the company.

Each holder of Common Stock is entitled to one vote for each share on all matters submitted to a vote of the stockholders, except for certain matters for which only the holders of Preferred Stock vote and/or for which they are also entitled to vote as a single class. For matters where holders of Common Stock vote, they will vote together with the holders of Preferred Stock as a single class on all matters (including the election of directors) submitted to vote or for the consent of the stockholders of the company. See “Securities Being Offered”.

Certain holders of the Company’s Common Stock and Preferred Stock will continue to hold a majority of the voting power of all of the Company’s equity stock at the conclusion of this Offering and therefore control the board.

As of July 14, 2025, our Chief Executive Officer, Mr. Brian Podolak is entitled and our Chief Technology Officer, Mr. James Sposato, each have voting power equivalent to approximately 49% of our total outstanding shares. This percentage accounts for all of Mr. Podolak’s and Mr. Sposato’s common stock and Series A preferred stock, par value $0.0001 per share (the “Series A Preferred Stock”).

We intend to use the proceeds from this offering for acquisitions of websites, technologies, or other assets, building improved phone switch capabilities for our product, expanding our product offerings from other digital channels, sales and marketing, working capital and other general corporate purposes. Our phone switch capacity allows us to scale more calls simultaneously, which translates into our services being more readily available to handle the increased demands of current and future customers. See “Use of Proceeds.”

We are an “emerging growth company” and a “smaller reporting company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) and have elected to comply with certain reduced public company reporting requirements. See “Summary-Implications of Being an Emerging Growth Company and Smaller Reporting Company.”

Investing in our securities is highly speculative and involves a high degree of risk. You should carefully consider the risks and uncertainties described under the heading “Risk Factors” beginning on page 7 of this prospectus before making a decision to purchase our securities.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THE SECURITIES OR PASSED UPON THE ACCURACY OR ADEQUACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

Table of Contents

i

The following summary highlights information contained elsewhere in this offering. This summary may not contain all of the information that may be important to you. You should read this entire prospectus carefully, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our Company’s historical financial statements and related notes included elsewhere in this prospectus. In this prospectus, unless otherwise noted, the terms “Company,” “Vocodia” “we,” “us,” and “our” refer to Vocodia Holdings Corp.

OVERVIEW

Company Overview

Vocodia Holdings Corp (“Vocodia” or “VHC”) was incorporated in the State of Wyoming on April 27, 2021 and is a conversational artificial intelligence (“AI”) technology provider. Our technology is designed to drive better sales and services for our customers. Clients turn to us for their product and service needs.

Business Summary

We are an AI software company that build practical AI functions and makes them easily obtainable for businesses on cloud-based platform solutions at low costs and scalable to multiagent vast enterprise solutions.

Our operations include one wholly owned subsidiary: Click Fish Media, Inc. (“CFM”), which was incorporated in the State of Florida on November 26, 2019 and is an IT services provider. CFM was formerly owned by James Sposato, who is an officer and director of the Company. CFM was acquired by us from Mr. Sposato per the Contribution Agreement, dated August 1, 2022 (the “Contribution Agreement”). In the Contribution Agreement, Mr. Sposato (“Contributor”), has contributed, assigned, transferred and delivered to us, the outstanding capital stock of CFM and we have accepted the contributed shares from the Contributor. As full consideration for the Contribution, we have paid the Contributor consideration in the amount of $10.

We aim to offer corporate clients scalable enterprise AI sales and customer service solutions intended to rapidly increase sales and service, while lowering employment costs.

We seek to enhance rapport and relationship building for customers, which is as necessary component to sales. We believe that there is a positive correlation between AI which sounds similar to a human voice over the phone and better customer rapport and customer service benefits. With our advanced AI, we believe that it will be difficult for customers to distinguish between speaking to a human sales representative and to an AI bot. We believe we can increase customer satisfaction and maximize potential service efficiency for our clients. Our goal is to provide quick training and deployment, potentially unlimited scalability, easy integration with existing corporate platforms and other benefits to our customers from AI’s efficiency. We strive to help our customers manage budgets and perform better than the high costs of existing sales and service personnel.

Our Mission

We are a conversational AI software developer and provider. Our mission is to maximize value in communications between organizations and their consumer bases from “hello” to “goodbye”. Our goal is to be the conversational leader in corporate and organizational, agenda driven communications, to drive convenience, scale, and empowerment, while reducing operational costs and risk.

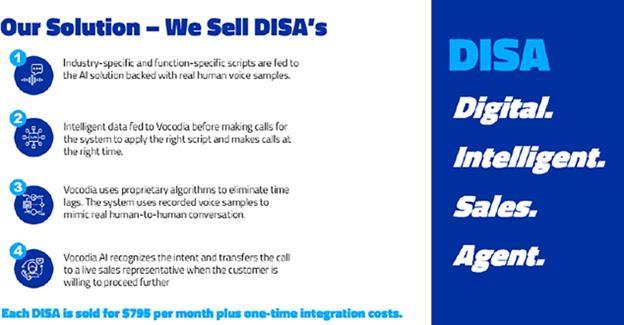

We offer our corporate clients scalable enterprise-level AI sales and customer service solutions which allow for AI sales representatives to reduce human labor costs and responsibilities while increasing the reach and efficacy of human-led, purposeful, agenda driven and conversational communications. We deliver our patent pending conversational AI software in the form of Digital Intelligent Sales Agents, which we refer to as DISAs® (the “DISAs”). The DISAs are built with AI software programmed for the DISAs to sound and feel human and to perform business tasks that require humans to converse with one another effectively, and thus to provide the best representation for each of our customers’ businesses.

1

Our DISAs have been programmed to provide the marketplace with an alternative to human sales representatives in the function of (1) sales; (2) customer service; (3) supportive agency; (4) intermediary communications; and (5) alerts with automated transfers and queuing. The DISAs are tailored to serve the specific requirements of each of our customers and are delivered via our proprietary platform.

We view our DISAs as the total solution for those in need of sales and customer service automation, which provides the marketplace alternative to a role that has primarily been serviced by humans in the sales and customer service departments, in part or in whole, to increase our clients’ revenues and lower costs, providing them with the ability to produce campaigns fast and scale them up or down as necessary.

Our AI software is intended to provide a solution for operational costs and efficiency deficits by improving business automation and reducing the inefficiencies caused by human limitations. Our motto is to “Go Beyond Human”, with AI alternative of human salespeople and customer service representatives. We aim to lower costs associated with sales campaigns that rely on humans and provide scalability of agent quantity, style, mission, and other personalization at varying levels for each organization’s needs.

Market Opportunity

AI Reduces Labor Spending

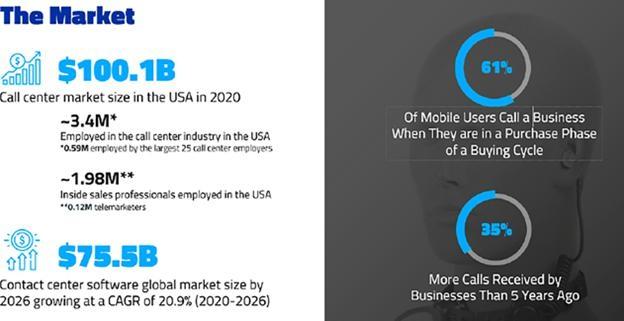

Growth for most businesses means increasing sales and services. However, growth is often limited by available resources, such as customers and employees. Planning, recruiting, training and retaining employees to focus on growth (sales), and retaining such employees (attrition), is typically expensive and costs can be prohibitive. Further, labor costs can be a considerable percentage of overall costs for running the business as they include, without limitation, employee wages, benefits, payroll or other related taxes. There may be no relief for businesses faced with the necessary employment costs of sales agents and customer service personnel.

Key Highlights

| ● | Voice Quality: We provide AI with high-level voice quality and seeks to deliver superior service in the marketplace. | |

| ● | Quality Sales: We use the following sales and marketing strategy: Prospects – Qualifies – Closes – Processes Orders – Upsells. Our DISAs are able to generate more leads and more transfers to clients so they can sell or upsell their new leads and transfers on their products. We believe that our customers can become more efficient by hiring DISA “fronters”, rather than traditional “fronters”. These traditional human “fronters” have served as the driving force in call centers making 150 or so calls daily to qualify potential clients. Once qualified, they then transfer the call to another department of the call center which handles the final transactional element of the sales call. The fronter position is the high turnover, low pay, very hard to hire, part for call centers that are the costliest and least productive. We automate this part of the process using AI to make these calls, instead of the human fronters. In addition, AI only has to be trained once, does not take vacation, can call 24/7, and could cost less than human fronters. Thereby, corporate clients can receive the same level of sales expected from their top 85% of employees. We deliver effective, dependable, scalable to the hour, low variance sales and customer service solutions. |

Our Strategy

Technology

We believe that we have built, and will continue to build, AI conversational systems that sound virtually the same as humans. Proprietary software and systems have been developed in-house from scratch with streamlined integration and a growing number of customer relationship managements (“CRMs”) and platforms all over the world. Our software uses Artificial Intelligence, Augmented Intelligence, Natural Language Processing and Machine Learning to provide a robust, continuously learning engine which can perform multiagent functions simultaneously. Our software is cloud-based, permitting easy API integration with most systems and platforms commonly used by businesses today.

2

Products

We have developed and released its first software product and platform, which we refer to as “DISA”, a humanized conversational AI technology, that can complete each stage of the conversational aspect of the sales process, business-to-business (“B2B”) and business-to-consumer (“B2C”).

Our prospects for direct software sales are any enterprise clients who are in the phone and call center markets. The initial sales targets were call centers who needed to replace poor performing staff in the pre-Covid-19 era. Now, our sales targets have shifted to filling empty seats in the call centers. Our technology powers our virtual agent, the DISA. In the current marketplace, we consider any corporate client with a 50-seat call center at a telephony location a potential sales client. These potential clients span many industry verticals, including but not limited to, health, solar, employee retention credit, insurance, recruiting and real estate, automotive, cruise lines and hospitality and lodging.

Our AI sales agents not only sell and serve prospects and customers, but also gather and report robust intelligence from customers and the marketplace. Vocodia’s DISAs are programmed to instantly answer customer service calls and to upsell and provide personalized customer care.

Development Strategy

We plan three phases of development to become the largest and most profitable AI service provider, globally, in the next five years:

| ● | Integrate AI sales agents and customer service offerings directly into existing enterprises and then via CRM applications; |

| ● | Increase sales of AI-assisted workflow to more enterprises in a variety of functions and industries (e.g., food ordering, administration, accounting, bookkeeping and human resources). Grow revenue streams, including based upon market pricing where our DISAs can perform at advantageous margins such as notable efficiencies or less operational costs to achieve the same function to the satisfaction of the end customer (acquisitions may become a significant part of our growth strategy, but at this time we have not identified any specific candidates that meet our objectives); and |

| ● | Integrate personal AI assistants to individuals for overall life assistance, integrated with existing sales and other AI bots, to serve members of the community. |

Acquisition Strategy

Our strategy includes seeking to selectively pursue acquisitions, including companies with revenue streams where our DISAs can perform at advantageous margins with noticeable efficiency or less operational costs to achieve the same function. We will concentrate on several important priorities in evaluating potential acquisition candidates, including the key considerations and objectives we hope to achieve, which are listed below:

| ● | acquiring beneficial technology or use; | |

| ● | accelerating market share; | |

| ● | increasing revenue; | |

| ● | enhancing efficiencies in product and service delivery; | |

| ● | identifying and addressing possible threats to our organization; | |

| ● | acquiring access to targeted and specified client base; | |

| ● | reducing client acquisition costs by reducing our demands on resources and time (opportunity costs); | |

| ● | acquiring client bases from companies who have service relationships with consumers and acquisitions of companies with or without offerings of similar services; | |

| ● | reducing our client acquisition costs, preserving going rates of such services, and extending our wrapped services to such client base; and | |

| ● | maintaining our dynamic pricing thereby potentially creating greater value opportunities and allows us to minimize market price arbitrage to maximize profit potential. |

3

Management and Operating Strategy

Our management is market-receptive: as a new technology company, we seek to continuously identify new markets as well as industries where our services would be beneficial to potential customers. We believe that our technologies offer businesses and consumers significant advantages, but our technology is not yet generally recognized. We remain open to discovering new opportunities to offer our technology solutions.

We believe that we have an attractive operating model due to the scalability of our AI platform, the recurring nature of our revenue (Software-as-a Service (“SaaS”)) and the potentially high operating margins. We rely on conversions (sales) to generate increased free cash flow. Conversions happen for us when our clients use our services to sell their products/services to their customers. Our operational structure and AI focus allow us to convert enterprise clients in their call center environments (allowing us to rapidly convert clients in a cost-effective manner).

Given the fixed-cost nature of our technology, DISAs allow us to scale our solutions quickly with low marginal costs. These DISAs can pitch and close, as well as manage full customer service operations, in high data interactive demand-based industries, while providing a full human conversation experience to human customers. We offer our customers a contract term of 12 months, with a monthly fee of $1,495 per DISA per month. Additionally, we offer custom setup for a fee to begin building a DISA for a client (i.e., one-time setup fee for each client campaign). We believe that our recurring revenue, combined with our robust sales pipeline and enterprise customer base, will continue to contribute to our long-term growth and strong operating margins, giving us flexibility to allocate capital for our continued success.

Growth Strategy

We believe that we are well positioned for continued growth across the various markets in the call center space. Our strategy for achieving growth includes the following:

Build upon our extensive client relationships

We have a diversified pipeline of potential clients. Current clients include health insurance providers, health insurance recruiting new agents, employee retention credits, solar, real estate recruitment and real estate new clients. Through the development of our proprietary switch (as described below) and technical team, we have the ability to scale our DISAs over time. We also intend to scale our client base by strategically adding new sales development personnel and customer service and support team members. We believe that we are in the early stages of penetrating this expanding market with our DISA technology platform. Key elements of this strategy include:

| ● | widely commercializing this new humanized conversational AI platform in the marketplace; |

| ● | increasing the enterprise client usage by increasing the number of DISAs per client; |

| ● | adding multi-channel capabilities to our platform in the form of text message, voicemail, social media (such as LinkedIn), etc. to increase connection rates; and |

| ● | acquiring new strategic partners who bring enhanced complimentary technology and revenue to help us increase market share. |

Continue to innovate

We believe a significant opportunity exists to enhance our technology platform and analytics using our vast database. We intend to expand our technology services offerings to capitalize on the evolving call center and customer service environment. Our investments in human capital, technology and services capabilities position us to continue to pursue rapid innovation. Examples of our recent innovations include upgrading our own proprietary switch. Our platform depends on phone switch capability (generally voice over internet protocol switches) to generate the actual connection from AI to the customer on the outside. Thus, we are dependent on outside telecom switches and infrastructure to manage the speed of our connection pace. This dynamic creates operational risk, due to the reliance of each switch provider’s technology and infrastructure limits. The bulk of our challenges come from switch uncertainty. Therefore, our goal is to improve our own company-controlled switch, which is critical to our economic health, growth and can facilitate easier delivery of services provided in each software sale. We believe this development would provide us with switch independence, allowing us to obtain more control, efficiency and certainty of delivery while lowering internal costs and managing traffic to external, non-company managed switches. The benefits of building our own switch allows us to scale faster in the quantity of software licenses, the variety of industries and verticals served, the independent scale of service utilized by each individual software licensee (end user), and the quantity of connections made by the hour.

4

Expand portfolio through strategic acquisitions

We have developed an internal capability to source, evaluate and integrate acquisitions that have created value for our stockholders. We plan to target strategic acquisitions subsequent to the closing of this initial public offering, but we have not currently entered into any agreements for the acquisition of significant assets, businesses or companies. While there is no guarantee that any acquisition will be completed, successful acquisitions may bring a collection of complimentary technology and existing revenue to us. We also plan to continue to pursue strategic acquisitions to grow our platform and enhance our ability to provide more services to our clients. We also expect to seek favorable commercial opportunities, primarily in the areas of technological platforms, data suppliers and consulting services providers.

Going Concern

The consolidated financial statements which accompany this prospectus have been prepared assuming that the Company will continue as a going concern. As discussed in the report of the independent registered public accounting firm and the consolidated financial statements, we have suffered recurring losses from operations that raise substantial doubt about the Company’s ability to continue as a going concern.

Implications of being an Emerging Growth Company

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act of 1933, as amended (the “Securities Act”), as modified by the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). As such, we are eligible to take advantage of certain exemptions from various reporting requirements applicable to other public companies that are not “emerging growth companies” including, but not limited to:

| ● | being permitted to present only two years of audited financial statements and only two years of related disclosure in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus; |

| ● | being permitted to provide less extensive narrative disclosure than other public companies, including not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 and reduced disclosure obligations regarding executive compensation in our periodic reports, proxy statements and registration statements; | |

| ● | being permitted to utilize exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved; | |

| ● | being permitted to defer complying with certain changes in accounting standards; and |

| ● | being permitted to use test-the-waters communications with qualified institutional buyers and institutional accredited investors. |

We intend to take advantage of these and other exemptions available to “emerging growth companies.” We could remain an “emerging growth company” until the earliest of (i) the last day of our fiscal year following the fifth anniversary of the closing of this offering, (ii) the last day of the first fiscal year in which our annual gross revenues exceed $1.235 billion, (iii) the last day of our fiscal year in which we are deemed to be a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934 (the “Exchange Act”) (which would occur if the market value of our equity securities that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter), or (iv) the date on which we have issued more than $1 billion in nonconvertible debt during the preceding three-year period.

The JOBS Act permits an “emerging growth company” like us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. This means that an “emerging growth company” can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected to delay such adoption of new or revised accounting standards.

5

OFFERING SUMMARY

| Shares of Common Stock Offered by the Company | Up to 30,000,000,000 shares of our common stock, $0.001 par value (“Common Shares”) at an offering price between $.0001 and $.0005 per share. The offering price will remain fixed for the duration of the Offering. | |

| Shares of Common Stock Offered by the Selling Shareholders | Up to 30,000,000,000 shares. | |

| Shares of common stock outstanding before this offering | 1,677,460,730 shares. | |

| Shares of common stock outstanding after this offering(1): | 31,677,460,730 shares | |

| Maximum Offering Amount | $3,000,000. The Company will not receive any proceeds from sales of Common Stock by the Selling Shareholders. | |

| Use of proceeds: | We intend to use the net proceeds from this offering for acquisitions of websites, technologies, or other assets, building an improved switch, for expanding product offerings from other digital channels, sales and marketing, working capital and general other corporate purposes. See section entitled “Use of Proceeds” for a more complete description of the intended use of proceeds from this offering. |

| (1) | This includes 1,677,460,730 shares issued and outstanding, 29,520,000,000 shares to be issued by the Company pursuant to the offering, and 480,000,000 shares from conversion of notes held by the Selling Shareholder. |

6

Investing in our shares of common stock involves a high degree of risk. Prospective investors should carefully consider the risks described below, together with all of the other information included or referred to in this prospectus, before purchasing our shares of common stock. There are numerous and varied risks that may prevent us from achieving its goals. If any of these risks actually occur, our business, financial condition or results of operations may be materially adversely affected. In such case, the trading price of our common stock could decline and investors could lose all or part of their investment.

Risks Related to Our Business - General

We will need to raise additional capital to expand our business to meet our long-term business objectives. We have limited revenues and we cannot predict when we will achieve significant revenues and sustained profitability.

We have limited revenues and cannot definitively predict when we will achieve significant revenues and sustained profitability. We do not anticipate generating significant revenues until we successfully raise funds pursuant to this offering and execute our business strategy and operations, of which we can give no assurance. We are unable to determine when we will generate significant revenues from our operations. We cannot predict when we will achieve profitability, if ever. Our inability to become profitable may force us to sell certain of our websites, reduce operations or reduce our staff. Furthermore, we cannot assure you that profitability, if achieved, can be sustained on an ongoing or long-term basis.

We require additional capital to support our present business plans and our anticipated business growth, and such capital may not be available on acceptable terms, or at all, which would adversely affect our ability to operate.

We will require additional funds to further develop our business plan. Based on our current operating plans, we plan to use approximately $500,000 in capital to fund our acquisitions of websites, technologies or other assets (as of the date of this prospectus, we have no agreements in place to make any acquisitions), approximately $1,500,000 for research and development, and approximately $2,350,000 for sales and marketing, working capital and general corporate purposes. We may choose to raise additional capital beyond these amounts in order to expedite and propel growth more rapidly. We can give no assurance that we will be successful in raising any additional funds. Additionally, if we are unable to generate sufficient revenues from our sales and operating activities, we may need to raise additional funds, doing so through debt and equity offerings, in order to meet our expected future liquidity and capital requirements, including capital required for operations. Any such financing that we undertake will likely be dilutive to current stockholders.

We intend to continue to make investments to support our business growth, including acquiring additional assets. In addition, we may also need additional funds to respond to other business opportunities and challenges, including our ongoing operating expenses, protecting our intellectual property, and enhancing our operating infrastructure. While we may need to seek additional funding for such purposes, we may not be able to obtain financing on acceptable terms, or at all. In addition, the terms of our financings may be dilutive to, or otherwise adversely affect, holders of our common stock. We may also seek to raise additional funds through arrangements with collaborators or other third parties. We may not be able to negotiate any such arrangements on acceptable terms, if at all. If we are unable to obtain additional funding on a timely basis, we may be required to curtail or terminate some or all our business plans.

We cannot predict our future capital needs and we may not be able to secure additional financing.

We will need to raise additional funds in the future to fund our working capital needs and to fund further expansion of our business. We may require additional equity or debt financings, collaborative arrangements with corporate partners or funds from other sources for these purposes. No assurance can be given that necessary funds will be available for us to finance our development on acceptable terms, if at all. Furthermore, such additional financings may involve substantial dilution of our stockholders or may require that we relinquish rights to certain of our technologies or products. In addition, we may experience operational difficulties and delays due to working capital restrictions. If adequate funds are not available from operations or additional sources of financing, we may have to delay or scale back our growth plans.

7

Our independent auditors concurred with our management’s assessment that raises substantial doubt as to our ability to continue as a going concern.

Management has determined and has stated in the notes to the Company’s Unaudited Consolidated Financial Statements ended September 30, 2024 and 2023, respectively and Audited Consolidated Financial Statements ended December 31, 2023 and 2022, respectively that we have suffered recurring losses from operations that raise substantial doubt about our ability to continue as a going concern, which are still present. Our independent auditors concurred with our management’s assessment that raises substantial doubt as to our ability to continue as a going concern.

If we fail to retain certain of our key personnel and attract and retain additional qualified personnel, we might not be able to pursue our growth strategy.

Our future success will depend upon the continued services of Brian Podolak, our Chief Executive Officer, James Sposato, our Chief Technology Officer, and our consultants. We especially consider Mr. Podolak to be critical to the management of our business and operations and the development of our strategic direction. Though no individual is indispensable, the loss of the services of these individuals could have a material adverse effect on our business, operations, revenues or prospects. We do not currently maintain key man life insurance on the lives of these individuals. Our future success will also depend on our ability to identify, hire, develop, motivate and retain highly skilled personnel. Competition in our industry for qualified employees is intense, and our compensation arrangements may not always be successful in attracting new employees and/or retaining and motivating our existing employees. Future acquisitions by us may also cause uncertainty among our current employees and employees of the acquired business, which could lead to the departure of key individuals. Such departures could have an adverse impact on the anticipated benefits of an acquisition.

We are anticipating a period of rapid growth in our headcount and operations, which may place, to the extent that we are able to sustain such growth, a significant strain on our management and our administrative, operational and financial reporting infrastructure.

Our success will depend in part on the ability of our senior management to manage this expected growth effectively. To do so, we believe we will need to continue to hire, train and manage new employees as needed. If our new hires perform poorly, or if we are unsuccessful in hiring, training, managing and integrating these new employees, or if we are not successful in retaining our existing employees, our business may be harmed. To manage the expected growth of our operations and personnel, we will need to continue to improve our operational and financial controls and update our reporting procedures and systems. The expected addition of new employees and the capital investments that we anticipate will be necessary to manage our anticipated growth and will increase our cost base, which may make it more difficult for us to offset any future revenue shortfalls by reducing expenses in the short term. If we fail to successfully manage our anticipated growth, then we will be unable to execute our business plan.

Negative publicity could adversely affect our reputation, our business, and our operating results.

Negative publicity about our Company (including, but not limited to the quality and reliability of our products and services, our privacy and security practices, and litigation involving or relating to us) could adversely affect our reputation which, in turn, could adversely affect our business, results of operations and financial condition. Because Vocodia is in a competitive industry where public perception is important, any harm to the Company’s reputation could be significant. Negative perception about the Company or its software and platform could harm sales and business prospects.

Natural disasters and other events beyond our control could materially adversely affect us.

Natural disasters or other catastrophic events may cause damage or disruption to our operations, international commerce and the global economy, and thus could have a strong negative effect on us. Our business operations are subject to interruption by natural disasters, fire, power shortages, pandemics and other events beyond our control. Such events could make it difficult or impossible for us to deliver our products and services to our customers and could decrease demand for our products and services.

8

Additionally, we depend on the efficient and uninterrupted operations of our third-party data centers and hardware systems. The data centers and hardware systems are vulnerable to damage from earthquakes, tornados, hurricanes, fire, floods, power loss, telecommunications failures and similar events. If any of these events results in damage to third-party data centers or systems, we may be unable to provide our clients with our products and services until the damage is repaired and may accordingly lose clients and revenues. In addition, subject to applicable insurance coverage, we may incur substantial costs in repairing any damage.

Political and economic factors may negatively affect our financial condition or results of operations.

Supply chain interruptions, regulatory changes, or political climate concerns could potentially adversely impact our relationships. Additionally, rising inflation could cause our product, marketing, and labor costs to rise beyond an acceptable level to us or cause us to increase our prices to a level not accepted by consumers. Furthermore, market volatility and macro-economic risks, including a slowdown or potential recession, could harm us and our business. We operate in the sales and customer service sector, and reductions in discretionary spending or consumer demand could have a significant negative impact on our operations and prospects. Any of the foregoing factors could negatively impact our financial condition or the results of our operations.

Market and economic conditions may negatively impact our business, financial condition and share price.

Concerns over inflation, energy costs, geopolitical issues, the U.S. mortgage market and unstable real estate market, unstable global credit markets and financial conditions, and volatile oil prices have led to periods of significant economic instability, diminished liquidity and credit availability, declines in consumer confidence and discretionary spending, diminished expectations for the global economy and expectations of slower global economic growth going forward, increased unemployment rates, and increased credit defaults in recent years. Our general business strategy may be adversely affected by any such economic downturns, volatile business environments and continued unstable or unpredictable economic and market conditions. If these conditions continue to deteriorate or do not improve, it may make any necessary debt or equity financing more difficult to complete, more costly, and more dilutive. Failure to secure any necessary financing in a timely manner and on favorable terms could have a material adverse effect on our growth strategy, financial performance, and overall plan of business.

We are authorized to issue preferred stock without stockholder approval, which could adversely impact the rights of holders of our securities.

Our articles of incorporation authorize us to issue up to 24,000,000 shares of Series A Preferred Stock, of which 4,000,000 shares are currently issued and outstanding respectively. Any shares or series of preferred stock that we issue in the future may rank ahead of our other securities in terms of dividend priority or liquidation premiums and may have greater voting rights than our common stock. In addition, we may issue preferred stock that could contain provisions allowing those shares to be converted into shares of common stock, which could dilute the value of our common stock to current stockholders and could adversely affect the market price, if any, of our common stock. In addition, the preferred stock could be utilized, under certain circumstances, as a method of discouraging, delaying or preventing a change in control of our Company.

Risks related to common stock and preferred stock voting rights.

Each share of our common stock is entitled to one vote per share, while our Series A Preferred Stock, par value $0.0001 is entitled to vote to 10,000 votes per share. As of the date of this Offering Circular, we have issued 4,000,000 shares of our Series A Preferred Stock: 2,000,000 shares of Series A Preferred Stock are owned by Mr. Podolak, our Chief Executive Officer and the remaining 2,000,000 shares of Series A Preferred Stock are owned by Mr. Sposato, our Chief Technology Officer. Although we have no present intention to issue any additional shares of authorized Series A Preferred Stock, there can be no assurance that we will not do so in the future.

9

Risks Related to Our Business – Operating Our Website

If we are unable to attract new customers and retain customers on a cost-effective basis, our business and results of operations will be adversely affected.

To succeed, we must attract and retain customers on a cost-effective basis. We rely on a variety of methods to attract new customers, such as paying providers of online services, search engines, directories and other websites to provide content, advertising banners and other links that direct customers to our website, direct sales and partner sales. If we are unable to use any of our current marketing initiatives or the cost of such initiatives were to significantly increase or such initiatives or our efforts to satisfy our existing customers are not successful, we may not be able to attract new customers or retain customers on a cost-effective basis and, as a result, our revenue and results of operations would be adversely affected.

Additionally, factors outside of our control, such as new terms, conditions, policies, or other changes made by the online services, search engines, directories and other websites that we rely upon to attract new customers could cause our websites to experience short- or long-term business disruptions, which could adversely affect our revenue and results of operations.

If we fail to develop our brands cost-effectively, our business may be adversely affected.

Successful promotion of our Company’s brands will depend largely on the effectiveness of our marketing efforts and on our ability to provide reliable and useful products and services at competitive prices. Brand promotion activities may not yield increased revenue, and even if they do, any increased revenue may not offset the expenses we incur in building our brands. If we fail to successfully promote and maintain our brands or incur substantial expenses in an unsuccessful attempt to promote and maintain our brands, we may fail to attract enough new customers or retain existing customers to the extent necessary to realize a sufficient return on our brand-building efforts, and our business and results of operations could suffer.

The market in which we participate is competitive and, if we do not compete effectively, our operating results could be harmed.

The market for our clients, goods and services is competitive and rapidly changing, and the barriers to entry are relatively low. With the influx of new entrants to the market, we expect competition to persist and intensify in the future, which could harm our ability to increase sales, limit customer attrition and maintain our prices. Competition could result in reduced sales, reduced margins or the failure of our products and services to achieve or maintain more widespread market acceptance, any of which could harm our business. We compete with large established companies possessing large, existing customer bases, substantial financial resources and established distribution channels, as well as smaller less established businesses. If either of these types of competitors decide to develop, market or resell competitive services, acquire one of our existing competitors or form a strategic alliance with one of our competitors, our ability to compete effectively could be significantly compromised and our operating results could be harmed. Our current and potential competitors may have significantly more financial, technical, marketing and other resources than we do and may be able to devote greater resources to the development, promotion, sale and support of their products and services. Our current and potential competitors have more extensive customer bases and broader customer relationships than we have. If we are unable to compete with such companies, the demand for our products could substantially decline.

Risks Related to Information Technology Systems, Intellectual Property and Privacy Laws

We are reliant upon information technology to operate our business and maintain our competitiveness.

Our ability to leverage our technology and data scale is critical to our long-term strategy. Our business increasingly depends upon the use of sophisticated information technologies and systems, including technology and systems (cloud solutions, mobile and otherwise) utilized for communications, marketing, productivity tools, training, lead generation, records of transactions, business records (employment, accounting, tax, etc.), procurement and administrative systems. The operation of these technologies and systems is dependent upon third-party technologies, systems and services, for which there are no assurances of continued or uninterrupted availability and support by the applicable third-party vendors on commercially reasonable terms. We also cannot assure that we will be able to continue to effectively operate and maintain our information technologies and systems. In addition, our information technologies and systems are expected to require refinements and enhancements on an ongoing basis, and we expect that advanced new technologies and systems will continue to be introduced. We may not be able to obtain such new technologies and systems, or to replace or introduce new technologies and systems as quickly as our competitors or in a cost-effective manner. Also, we may not achieve the benefits anticipated or required from any new technology or system, and we may not be able to devote financial resources to new technologies and systems in the future.

10

Any significant disruption in service on our website or in our computer systems, or in our customer support services, could reduce the attractiveness of our services and result in a loss of customers.

The satisfactory performance, reliability and availability of our services are critical to our operations, level of customer service, reputation and ability to attract new customers and retain customers. Most of our computing hardware is co-located in third-party hosting facilities. None of the companies who host our systems guarantee that our customers’ access to our products will be uninterrupted, error-free or secure. Our operations depend on their ability to protect their and our systems in their facilities against damage or interruption from natural disasters, power or telecommunications failures, air quality, temperature, humidity and other environmental concerns, computer viruses or other attempts to harm our systems, criminal acts and similar events. If our arrangements with third-party data centers are terminated, or there is a lapse of service or damage to their facilities, we could experience interruptions in our service as well as delays and additional expense in arranging new facilities. Any interruptions or delays in access to our services, whether as a result of a third-party error, our own error, natural disasters or security breaches, whether accidental or willful, could harm our relationships with customers and our reputation. These factors could damage our brand and reputation, divert our employees’ attention, reduce our revenue, subject us to liability and cause customers to cancel their accounts, any of which could adversely affect our business, financial condition and results of operations.

We do not have a disaster recovery system, which could lead to service interruptions and result in a loss of customers.

Although we have all of our data backed up with multiple services, we do not have any disaster recovery systems. In the event of a disaster in which our software or hardware are irreparably damaged or destroyed, we would experience interruptions in access to our services. Any or all these events could cause our customers to lose access to our services.

If a third party asserts that we are infringing its intellectual property, whether successful or not, it could subject us to costly and time-consuming litigation or require us to obtain expensive licenses, and our business may be adversely affected.

Our industry is characterized by the existence of a large number of patents, trademarks and copyrights and by frequent litigation based on allegations of infringement or other violations of intellectual property rights. Third parties may assert patent and other intellectual property infringement claims against us in the form of lawsuits, letters or other forms of communication. These claims, whether or not successful, could:

| ● | divert management’s attention; |

| ● | result in costly and time-consuming litigation; |

| ● | require us to enter into royalty or licensing agreements, which may not be available on acceptable terms, or at all; |

| ● | in the case of any open source software-related claims, require us to release our software code under the terms of an open source license; or |

| ● | require us to redesign our software and services to avoid infringement. |

As a result, any third-party intellectual property claims against us could increase our expenses and adversely affect our business. Even if we have not infringed any third parties’ intellectual property rights, we cannot be sure our legal defenses will be successful, and even if we are successful in defending against such claims, our legal defense could require significant financial resources and management time. Finally, if a third party successfully asserts a claim that our products infringe its proprietary rights, royalty or licensing agreements might not be available on terms we find acceptable or at all, and we may be required to pay significant monetary damages to such third party.

11

If the security of our customers’ confidential information stored in our systems is breached or otherwise subjected to unauthorized access, our reputation may be severely harmed, we may be exposed to liability and we may lose the ability to offer our customers a credit card payment option.

Our system stores our customers’ proprietary email distribution lists, credit card information and other critical data. Any accidental or willful security breaches or other unauthorized access could expose us to liability for the loss of such information, adverse regulatory action by federal and state governments, time-consuming and expensive litigation and other possible liabilities as well as negative publicity, which could severely damage our reputation. If security measures are breached because of third-party action, employee error, malfeasance or otherwise, or if design flaws in our software are exposed and exploited, and, as a result, a third party obtains unauthorized access to any of our customers’ data, our relationships with our customers will be severely damaged, and we could incur significant liability. Because techniques used to obtain unauthorized access or to sabotage systems change frequently and generally are not recognized until they are launched against a target, we and our third-party hosting facilities may be unable to anticipate these techniques or to implement adequate preventative measures. In addition, many states have enacted laws requiring companies to notify individuals of data security breaches involving their personal data. These mandatory disclosures regarding a security breach often lead to widespread negative publicity, which may cause our customers to lose confidence in the effectiveness of our data security measures. Any security breach, whether actual or perceived, would harm our reputation, and we could lose customers and fail to acquire new customers.

If we fail to maintain our compliance with the data protection policy documentation standards adopted by the major credit card issuers, we could lose our ability to offer our customers a credit card payment option. Any loss of our ability to offer our customers a credit card payment option would make our products less attractive to many small organizations by negatively impacting our customer experience and significantly increasing our administrative costs related to customer payment processing.

We may be the subject of intentional cyber disruptions and attacks.

We expect to be an ongoing target of attacks specifically designed to impede the performance of our products and services. Experienced computer programmers, or hackers, may attempt to penetrate our network security or the security of our data centers and IT environments. These hackers, or others, which may include our employees or vendors, may cause interruptions of our services. Although we continually seek to improve our countermeasures to prevent and detect such incidents, if these efforts are not successful, our business operations, and those of our customers, could be adversely affected, losses or theft of data could occur, our reputation and future sales could be harmed, governmental regulatory action or litigation could be commenced against us and our business, financial condition, operating results and cash flow could be materially adversely affected.

We may not be able to adequately protect our proprietary technology, and our competitors may be able to offer similar products and services which would harm our competitive position.

Our success, in part, depends upon our proprietary technology. We have various forms of intellectual property including copyright, trademark, confidentiality procedures and contractual provisions to establish and protect our proprietary rights. Despite these precautions, third parties could copy or otherwise obtain and use our technology without authorization, or develop similar technology independently. We also pursue the registration of our domain names, trademarks, and service marks in the United States. If we file patent applications, we cannot assure you that any of the patent applications that we file will ultimately result in an issued patent or, if issued, that they will provide sufficient protections for our technology against competitors. We cannot assure you that the protection of our proprietary rights will be adequate or that our competitors will not independently develop similar technology, duplicate our products and services or design around any intellectual property rights we hold.

We could be harmed by improper disclosure or loss of sensitive or confidential data.

Our business operations require us to process and transmit data. Unauthorized disclosure or loss of sensitive or confidential data may occur through a variety of methods. These include, but are not limited to, systems failure, employee negligence, fraud or misappropriation, or unauthorized access to or through our information systems, whether by our employees or third parties, including a cyberattack by computer programmers, hackers, members of organized crime and/or state-sponsored organizations, who may develop and deploy viruses, worms or other malicious software programs.

12

Such disclosure, loss or breach could harm our reputation and subject us to government sanctions and liability under laws and regulations that protect sensitive or personal data and confidential information, resulting in increased costs or loss of revenues. It is possible that security controls over sensitive or confidential data and other practices we and our third-party vendors follow may not prevent the improper access to, disclosure of, or loss of such information. The potential risk of security breaches and cyberattacks may increase as we acquire additional business and introduce new services and offerings. Further, data privacy is subject to frequently changing rules and regulations, which sometimes conflict among the various jurisdictions in which our websites operate. Any failure or perceived failure to successfully manage the collection, use, disclosure, or security of personal information or other privacy related matters, or any failure to comply with changing regulatory requirements in this area, could result in legal liability or impairment to our reputation in the marketplace.

Unauthorized breaches or failures in cybersecurity measures adopted by us and/or included in our products and services could have a material adverse effect on our business.

Information security risks have generally increased in recent years, in part because of the proliferation of new technologies and the use of the Internet, and the increased sophistication and activity of organized crime, hackers, terrorists, activists, cybercriminals and other external parties, some of which may be linked to terrorist organizations or hostile foreign governments. Cybersecurity attacks are becoming more sophisticated and include malicious attempts to gain unauthorized access to data and other electronic security breaches that could lead to disruptions in critical systems, unauthorized release of confidential or otherwise protected information and corruption of data, substantially damaging our reputation. Our security systems are designed to maintain the security of our users’ confidential information, as well as our own proprietary information. Accidental or willful security breaches or other unauthorized access by third parties or our employees, our information systems or the systems of our third-party providers, or the existence of computer viruses or malware in our or their data or software could expose us to risks of information loss and misappropriation of proprietary and confidential information, including information relating to our products or customers and the personal information of our employees.

In addition, we could become subject to unauthorized network intrusions and malware on our own IT networks. Any theft or misuse of confidential, personal or proprietary information as a result of such activities or failure to prevent security breaches could result in, among other things, unfavorable publicity, damage to our reputation, loss of our trade secrets and other competitive information, difficulty in marketing our products, allegations by our customers that we have not performed our contractual obligations, litigation by affected parties and possible financial obligations for liabilities and damages related to the theft or misuse of such information, as well as fines and other sanctions resulting from any related breaches of data privacy regulations, any of which could have a material adverse effect on our reputation, business, profitability and financial condition. Furthermore, the techniques used to obtain unauthorized access or to sabotage systems change frequently and are often not recognized until launched against a target, and we may be unable to anticipate these techniques or to implement adequate preventative measures.

We may be subject to stringent and changing laws, regulations, standards, and contractual obligations related to privacy, data protection, and data security. Our actual or perceived failure to comply with such obligations could adversely affect our business.

We receive, collect, store, and process certain personally identifiable information about individuals and other data relating to our customers. We have legal and contractual obligations regarding the protection of confidentiality and appropriate use of certain data, including personally identifiable and other potentially sensitive information about individuals. We may be subject to numerous federal, state, local, and international laws, directives, and regulations regarding privacy, data protection, and data security and the collection, storing, sharing, use, processing, transfer, disclosure, disposal and protection of information about individuals and other data, the scope of which are changing, subject to differing interpretations, and may be inconsistent among jurisdictions or conflict with other legal and regulatory requirements. We strive to comply with our applicable data privacy and security policies, regulations, contractual obligations, and other legal obligations relating to privacy, data protection, and data security. However, the regulatory framework for privacy, data protection and data security worldwide is, and is likely to remain for the foreseeable future, uncertain and complex, and it is possible that these or other actual or alleged obligations may be interpreted and applied in a manner that we do not anticipate or that is inconsistent from one jurisdiction to another and may conflict with other legal obligations or our practices. Further, any significant change to applicable laws, regulations or industry practices regarding the collection, use, retention, security, processing, transfer or disclosure of data, or their interpretation, or any changes regarding the manner in which the consent of users or other data subjects for the collection, use, retention, security, processing, transfer or disclosure of such data must be obtained, could increase our costs and require us to modify our services and features, possibly in a material manner, which we may be unable to complete, and may limit our ability to receive, collect, store, process, transfer, and otherwise use user data or develop new services and features.

13

If we are found in violation of any applicable laws or regulations relating to privacy, data protection, or security, our business may be materially and adversely affected and we would likely have to change our business practices and potentially the services and features, integrations or other capabilities of websites. In addition, these laws and regulations could impose significant costs on us and could constrain our ability to use and process data in a commercially desirable manner. In addition, if a breach of data security were to occur or be alleged to have occurred, if any violation of laws and regulations relating to privacy, data protection or data security were to be alleged, or if we were to discover any actual or alleged defect in our safeguards or practices relating to privacy, data protection, or data security, our business websites may be perceived as less desirable and our business, financial condition, results of operations and growth prospects could be materially and adversely affected.

Online applications are subject to various laws and regulations relating to children’s privacy and protection, which if violated, could subject us to an increased risk of litigation and regulatory actions.

A variety of laws and regulations have been adopted in recent years aimed at protecting children using the internet such as the U.S. Federal Trade Commission’s Children’s Online Privacy Protection Rule (the “COPPA”) and Article 8 of the European Union’s General Data Protection Regulation (the “GDPR”). We implement certain precautions to ensure that we do not knowingly collect personal information from children under the age of 13 through our websites. Despite our efforts, no assurances can be given that such measures will be sufficient to completely avoid allegations of COPPA violations, any of which could expose us to significant liability, penalties, reputational harm and loss of revenue, among other things. Additionally, new regulations are being considered in various jurisdictions to require the monitoring of user content or the verification of users’ identities and age. Such new regulations, or changes to existing regulations, could increase the cost of our operations.

Risks Related to Our Business – Our Acquisition Plans

As part of our business plan, we intend to acquire or make investments in other companies, or engage in business relationships with other companies, which will divert our management’s attention, result in dilution to our stockholders, consume resources that may be necessary to sustain our business and could otherwise disrupt our operations and adversely affect our operating results.

As part of our business plan, we will plan to acquire or invest in websites, applications and services or technologies that we believe could offer growth opportunities or complement or expand our business or otherwise. The pursuit of target companies will divert the attention of management and cause us to incur various expenses in identifying, investigating and pursuing suitable acquisitions, whether or not they are consummated.

As we acquire additional companies, we may not be able to integrate the acquired personnel, operations and technologies successfully, or effectively manage the combined business following the acquisition. We also may not achieve the anticipated benefits from the acquired business or investments in other companies, due to a number of factors, including:

| ● | inability to integrate or benefit from acquired technologies or services in a profitable manner; |

| ● | unanticipated costs or liabilities associated with the acquisition; |

14

| ● | difficulty integrating the accounting systems, operations and personnel of the acquired business; |

| ● | difficulty converting the customers of the acquired business onto our platform and contract terms, including disparities in the revenue, licensing, support or professional services model of the acquired company; |

| ● | adverse effects to our existing business relationships with business partners and customers as a result of the acquisition; and |

| ● | use of substantial portions of our available cash to consummate the acquisition. |

In addition, a significant portion of the purchase price of companies we acquire may be allocated to acquired goodwill and other intangible assets, which must be assessed for impairment at least annually. If future acquisitions do not yield expected returns, we may be required to take charges to our operating results based on this impairment assessment process and this could adversely affect our results of operations.

Acquisitions could also result in dilutive issuances of equity securities or the incurrence of debt, which could adversely affect our operating results. In addition, if an acquired business fails to meet our expectations, our operating results, business and financial position may suffer. As of the date of this prospectus, we have no agreements in place to make any acquisitions.

Pursuant to our long-term investment strategy, we may pursue future acquisitions or business relationships, or make business dispositions that may not be in the best interests of common stockholders in the near term or at all.

As part of our long-term investment strategy, we will plan to acquire or invest in websites, applications and services or technologies that we believe could complement or expand our services or otherwise offer growth opportunities in the long run. We may incur indebtedness for future acquisitions, which would be senior to our common shares. Future acquisitions may also reduce our cash available for distribution to our stockholders, including holders of common shares, following such acquisitions. To the extent such acquisitions do not perform as expected, such risk may be particularly heightened. As of the date of this prospectus, we have no agreements in place to make any acquisitions.

In addition to acquiring businesses, we may sell those companies that we own from time to time when attractive opportunities arise that outweigh the future growth and value that we believe we will be able to bring to such companies consistent with our long-term business and investment strategy. As such, our decision to sell a business will be based on our belief that doing so will increase stockholder value to a greater extent than through our continued ownership of that business. Future dispositions of companies may reduce our cash flows from operations. We cannot assure you that we will use the proceeds from any future dispositions in a manner with which you agree. You will generally not be entitled to vote with respect to our future acquisitions or dispositions, and we may pursue future acquisitions or dispositions with which you do not agree.

Because of our limited resources and the significant competition for acquisition opportunities, it may be more difficult for us to acquire target companies that meet our acquisition criteria.

We expect to encounter competition from other companies having a business plan similar to ours, including private investors (which may be individuals or investment partnerships), blank check companies and other entities, domestic and international, competing for the types of companies we intend to acquire. Many of these individuals and entities are well-established and have extensive experience in identifying and effecting, directly or indirectly, acquisitions of companies operating in or providing services to various industries. Many of these competitors possess similar or greater technical, human and other resources to ours or more local industry knowledge than we do and our financial resources will be relatively limited when contrasted with those of many of these competitors. While we believe there are numerous target businesses we could potentially acquire with the net proceeds of this offering, our ability to compete with respect to the acquisition of certain target companies that are attractive to us will be limited by our available financial resources. This inherent competitive limitation gives others an advantage in pursuing the acquisition of certain companies. As of the date of this prospectus, we have no agreements in place to make any acquisitions.

15

Subsequent to the acquisition of any target business, we may be required to take write-downs or incur write-offs, restructuring and impairment or other charges that could have a significant negative effect on our financial condition, results of operations and the price of our securities.

Even if we conduct extensive due diligence on target companies that we acquire, we cannot assure you that this diligence will identify all material issues that may be present with a particular target business, that it would be possible to uncover all material issues through a customary amount of due diligence, or that factors outside of the target business and outside of our control will not later arise. As a result of these factors, we may be forced to later write-down or write-off assets or incur impairment or other charges that could result in our reporting losses. Even if our due diligence successfully identifies certain risks, unexpected risks may arise and previously known risks may materialize in a manner not consistent with our preliminary risk analysis. Even though these charges may be non-cash items and not have an immediate impact on our liquidity, the fact that we report charges of this nature could contribute to negative market perceptions about us or our shares of common stock. In addition, charges of this nature may cause us to violate net worth or other covenants to which we may be subject as a result of assuming pre-existing debt held by a target business or by virtue of our obtaining debt financing to partially finance the acquisition transaction or thereafter. Accordingly, we could experience a significant negative effect on our financial condition, results of operations and the price of our securities. As of the date of this prospectus, we have no agreements to make any acquisitions.

We will likely not obtain an opinion from an independent accounting or investment banking firm in connection with the acquisition of a target business.

We will likely not obtain an opinion from an independent accounting firm or independent investment banking firm that the price we are paying for a target business is fair to our stockholders. If no opinion is obtained, our stockholders will be relying on the judgment of our Board, who will determine fair market value based on standards generally accepted by the financial community.

Our resources could be wasted by acquisition transactions that are not completed.

We anticipate that the investigation of each target business and the negotiation, drafting and execution of relevant agreements, disclosure documents and other instruments will require management time and attention and costs for accountants, attorneys and others. If we decide not to complete a specific acquisition transaction, the costs incurred up to that point for the proposed transaction likely would not be recoverable. Furthermore, if we reach an agreement relating to a specific target business, we may fail to complete our acquisition transaction for any number of reasons including those beyond our control. Any such event will result in a loss to us of the related costs incurred. As of the date of this prospectus, we have no agreements in place to make any acquisitions.

The officers and directors of a target business may resign upon completion of our acquisition. The loss of a target business key personnel could negatively impact the operations and profitability of the target business post-acquisition.