Table of Contents

An offering statement pursuant to Regulation A relating to these securities has been filed with the Securities and Exchange Commission. Information contained in this Preliminary Offering Circular is subject to completion or amendment. These securities may not be sold nor may offers to buy be accepted before the offering statement filed with the Commission is qualified. This Preliminary Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy nor may there be any sales of these securities in any state in which such offer, solicitation, or sale would be unlawful before registration or qualification under the laws of any such state. We may elect to satisfy our obligation to deliver a Final Offering Circular by sending you a notice within two business days after the completion of our sale to you that contains the URL where the Final Offering Circular or the offering statement in which such Final Offering Circular was filed may be obtained.

Preliminary Offering Circular Subject to Completion, dated August 30, 2021

Amalgamated Specialty Group Holdings, Inc.

We are offering up to 3,060,000 shares of our common stock for sale at a price of $10.00 per share in connection with the conversion of Amalgamated Casualty Insurance Company, or ACIC, from the mutual to stock form of organization. Immediately following the conversion, we will acquire all of the newly issued shares of ACIC common stock. This is our initial public offering. For a description of our common stock, see “Description of Our Capital Stock.”

We are offering shares of our common stock in a subscription offering and a public offering. The subscription offering will be made in the following order of priority: (1) first, to eligible members of ACIC, who were the policyholders of ACIC as of February 3, 2021, which we refer to herein as “eligible members”; (2) second, to our employee stock ownership plan, which we refer to as our ESOP; and (3) third, to the trustees, officers, and employees of ACIC. The minimum number of shares that a person may subscribe to purchase is 50 shares. For information regarding limitations on the number of shares that may be purchased, see “The Conversion and Offering — Limitations on Purchases of Common Stock.”

Each eligible member will receive the right to purchase shares of our common stock. Eligible members that do not purchase any shares of stock in the offering will have such subscription right redeemed by us for $1,489.87 in cash. See “The Conversion and Offering — Redemption of Subscription Rights.”

The subscription offering will end at noon, Eastern Time, on [●], 2021. Concurrently with the subscription offering and subject to the prior right of subscribers in the subscription offering, shares will be offered in a public offering to the general public. This phase of the stock offering is referred to as the public offering. We refer to the subscription offering and the public offering as the offering.

Our ability to complete this offering is subject to two conditions. First, a minimum of 2,260,000 shares of common stock must be sold to complete this offering. Second, ACIC’s plan of conversion must be approved by the affirmative vote of at least a majority of the votes cast at the special meeting of members to be held on [●], 2021. Until such time as these conditions are satisfied, all funds submitted to purchase shares will be held in escrow with Computershare Trust Company, N.A. If the offering is terminated, purchasers will have their funds promptly returned without interest.

Shares purchased by the ESOP and by trustees, employees and officers of ACIC will be counted toward satisfaction of the minimum amount needed to complete this offering. If more orders are received than shares offered, shares will be allocated in the manner and priority described in this offering circular.

Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

Griffin Financial Group LLC will act as our placement agent and will use its best efforts to assist us in selling our common stock in this offering, but Griffin Financial is not obligated to purchase any shares of common stock that are being offered for sale. Any commissions paid in connection with the purchase of shares of common stock in this offering will be paid by us from the gross proceeds of the offering.

There is currently no public market for our common stock. We do not intend to apply for the listing of our common stock on any stock exchange. This will materially and adversely affect the liquidity of our stock. We intend to apply to have “buy” and “sell” quotes for shares of our common stock reported on the “OTC Pink” market by broker-dealers that agree to make a market in our common stock. See “Risk Factors — Risks Relating to Ownership of Our Common Stock — Our shares will not be listed on any stock exchange, and there will not be an active, liquid market for our common stock.”

Our principal executive offices are located at 8401 Connecticut Avenue, Suite 300, Chevy Chase, Maryland 20815, our phone number is (202) 547-8700 and our website address is asginsurance.com. This is a Regulation A+ Tier 2 offering. This offering circular is intended to provide the information required by the Offering Circular format of Part II of Form 1-A.

Investing in our common stock involves risks. For a discussion of the material risks that you should consider, see “Risk Factors” beginning on page 13 of this offering circular.

OFFERING SUMMARY

Price: $10.00 per share

| Minimum | Midpoint | Maximum | ||||||||||

| Number of shares offered |

2,260,000 | 2,660,000 | 3,060,000 | |||||||||

| Gross offering proceeds |

$ | 22,600,000 | $ | 26,600,000 | $ | 30,600,000 | ||||||

| Less: Proceeds from ESOP shares(1) |

$ | 2,237,400 | $ | 2,633,400 | $ | 3,029,400 | ||||||

| Estimated offering expenses |

$ | 2,020,000 | $ | 2,020,000 | $ | 2,020,000 | ||||||

| Commissions(2)(3) |

$ | 1,014,974 | $ | 1,231,314 | $ | 1,447,654 | ||||||

| Redemption of subscription rights(4) |

$ | 2,367,000 | $ | 2,367,000 | $ | 2,367,000 | ||||||

| Net proceeds |

$ | 14,960,626 | $ | 18,348,286 | $ | 21,735,946 | ||||||

| Net proceeds per share |

$ | 6.62 | $ | 6.90 | $ | 7.10 | ||||||

| (1) | The calculation of net proceeds from this offering does not include the shares being purchased by our ESOP because ACIC will loan a portion of the proceeds to the ESOP to fund the purchase of such shares. The ESOP is purchasing such number of shares as will equal 9.9% of the total number of shares sold in the offering. |

| (2) | Represents the amount to be paid to Griffin Financial, based on (i) 2.0% of the proceeds from shares sold in the offering to policyholders, trustees, officers, and employees of ACIC and the ESOP, and (ii) 6.25% of the proceeds from all other shares sold in the offering. See “The Conversion and Offering — Marketing Arrangements” for a description of the placement agent compensation. |

| (3) | Assumes that at the offering minimum, the offering midpoint, and at the offering maximum 1,324,645, 1,645,445, and 1,966,245 shares, respectively, are sold in the offerings to persons other than the policyholders, trustees, officers and employees and the ESOP. |

| (4) | Assumes that none of the policyholders exercise their right to purchase shares in the offering and their subscription rights are redeemed for cash. |

The District of Columbia Department of Insurance, Securities and Banking has not approved or disapproved of these securities or determined if this offering circular is accurate or complete.

The United States Securities and Exchange Commission does not pass upon the merits of or give its approval to any securities offered or the terms of the offering, nor does it pass upon the accuracy or completeness of any offering circular or other solicitation materials. These securities are offered pursuant to an exemption from registration with the Commission; however, the Commission has not made an independent determination that the securities offered are exempt from registration.

For assistance, please call the Stock Information Center at (610) 205-6005.

Griffin Financial Group LLC

The date of this Offering Circular is , 2021

Table of Contents

| 1 | ||||

| 13 | ||||

| 28 | ||||

| 29 | ||||

| 31 | ||||

| 32 | ||||

| 32 | ||||

| 33 | ||||

| 35 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

44 | |||

| 71 | ||||

| 89 | ||||

| 109 | ||||

| 113 | ||||

| 124 | ||||

| 125 | ||||

| 135 | ||||

| 135 | ||||

| 135 | ||||

| F-1 |

i

Table of Contents

CERTAIN IMPORTANT INFORMATION

This Offering Circular

You should rely only on the information contained in this offering circular. We have not, and Griffin Financial has not, authorized any other person to provide information that is different from that contained in this offering circular. If anyone provides you with different or inconsistent information, you should not rely on it. We and Griffin Financial are offering to sell and seeking offers to buy our common stock only in jurisdictions where such offers and sales are permitted. You should assume that the information contained in this offering circular is accurate only as of the date of this offering circular, regardless of the time of delivery of this offering circular or of any sale of our common stock. Our business, financial condition, results of operations, and prospects may have changed since that date. Information contained on our website, or any other website operated by us, is not part of this offering circular.

Frequently Used Terms

Unless the context otherwise requires, as used in this offering circular:

| • | “ACIC” refers to Amalgamated Casualty Insurance Company and its consolidated subsidiaries; |

| • | “the Company,” “we,” “us,” and “our” refer to Amalgamated Specialty Group Holdings, Inc. prior to the conversion as described in this offering circular, and to Amalgamated Specialty Group Holdings, Inc. and its consolidated subsidiaries after the conversion; |

| • | “conversion” refers to a series of transactions by which ACIC will convert from mutual to stock form and become a subsidiary of Amalgamated Specialty Group Holdings, Inc. under the terms of the plan of conversion adopted by the board of trustees of ACIC; |

| • | “Department” means the District of Columbia Department of Insurance, Securities and Banking; |

| • | “ESOP” means our employee stock ownership plan; |

| • | “mutual form” refers to an insurance company organized as a mutual company, which is a form of organization in which the policyholders or members have certain membership rights in the mutual company, such as the right to vote with respect to the election of directors and approval of certain fundamental transactions, including the conversion from mutual to stock form; however, unlike shares held by shareholders, membership rights are not transferable and do not exist separately from the related insurance policy; |

| • | “stock form” is a form of organization in which the only rights that policyholders have are contractual rights under their insurance policies and in which voting rights reside with shareholders under state corporate law; |

| • | “subscription offering” refers to this offering of up to 3,060,000 shares of our common stock under the plan of conversion to eligible members, the ESOP, and trustees, officers, and employees of ACIC; |

| • | “public offering” refers to this offering of up to 3,060,000 shares of our common stock to the general public under the plan of conversion; |

| • | “offerings” refers to the subscription offering and the public offering; |

| • | “eligible member” refers to a person who was an owner of an insurance policy issued by ACIC and in-force on February 3, 2021, the date the plan of conversion was adopted by the board of trustees of ACIC; |

| • | “member” refers to a person who is the owner of an in-force insurance policy issued by ACIC; and |

| • | “ARM” refers to American Risk Management, Inc., a producer for ACIC under a nonexclusive agency agreement. |

ii

Table of Contents

Market and Industry Data

Market data and other statistical information used throughout this offering circular are based on independent industry publications, government publications, publicly available information, reports by market research firms, or other published independent sources. Independent industry publications, government publications, and other published independent sources generally indicate that the information included therein was obtained from sources believed to be reliable. Some data are based upon good faith estimates derived from our management’s review of the independent sources referenced herein and from experience with partners, licensees, and other contacts in the markets in which the Company operates.

iii

Table of Contents

This summary highlights information contained elsewhere in this offering circular. Before making a decision to purchase our common stock, you should read the entire offering circular carefully, including the “Risk Factors” and “Forward-Looking Statements” sections and our consolidated financial statements and the notes to those financial statements.

Overview

ACIC provides commercial automobile insurance products targeted to owners and operators of taxi cabs, passenger sedans, and other light transportation vehicles, including golf carts and school vans, in 13 states and the District of Columbia. ACIC strives to deliver to this market affordable insurance products through American Risk Management, Inc., its controlling producer (“ARM”), and 30 independent insurance agent sub-producers.

ACIC incurred losses in three of the last six years due to expansion into unprofitable products and underperforming states, which was exacerbated by the prolonged low interest rate environment which has depressed interest income. To address these shortcomings, ACIC has exited unprofitable non-core business segments and territories. ACIC has also implemented significant expense reductions. ACIC is also implementing an expansion plan focused on commercial auto insurance for vehicles used in a business such as contractors and other artisans instead of essentially being the business, such as taxis. See “— Our Market and Opportunities.”

For the year ended December 31, 2020, ACIC had total written premiums of $6.3 million, net premiums earned of $8.1 million, and comprehensive income of $4.4 million. As of December 31, 2020, ACIC had approximately 1,600 policyholders, total assets of $88.3 million, and equity of $42.2 million.

ACIC, a District of Columbia-domiciled mutual property and casualty insurance company, was incorporated in 1938. ACIC is rated B++ by A.M. Best. ACIC’s executive office is located in Chevy Chase, Maryland. After the completion of the conversion, ACIC intends to change its name to Forge Insurance Group.

Acquisition of American Risk Management, Inc.

We have entered into a stock purchase agreement with MCW Holdings, Inc. (“MCW”) to acquire all of the outstanding capital stock of American Risk Management, Inc. (“ARM”) concurrently with the completion of the conversion and the offerings. ARM is the controlling producer of ACIC. In connection with the acquisition of ARM, we will issue to MCW 550,000 shares of our Series A 8.5% cumulative convertible preferred stock (“Series A Preferred Stock”). For additional information regarding the acquisition of ARM, see “Business — Acquisition of American Risk Management, Inc.” Patrick J. Bracewell, the Chairman, President and Chief Executive Officer of the Company and ACIC, and his father Joseph Bracewell, a director of the Company and ACIC are significant shareholders of MCW. See “Certain Relationships and Related Transactions.” For a description of our Series A Preferred Stock, see “Description of our Capital Stock.”

Under a nonexclusive agency agreement between ARM and ACIC, ARM solicits commercial automobile and general liability insurance for ACIC directly with customers in the District of Columbia and Maryland and partners with 30 independent producers in other states to obtain commercial auto insurance business for ACIC. ARM receives a commission of 18.3% on substantially all premiums paid to ACIC on business solicited by ARM and ARM’s independent insurance agent sub-producers. ARM also shares space in ACIC’s offices at 8401 Connecticut Avenue, Chevy Chase, Maryland under a cost-sharing agreement with ACIC. See “Certain Relationships and Related Transactions.”

1

Table of Contents

Background and Reasons for the Conversion

ACIC believes that the state of the commercial auto specialty transportation insurance business in the United States currently presents it with the opportunity to extend its reach into its target market and provide affordable insurance products to this market. ACIC has examined various alternatives ranging from maintenance of the status quo, expansion or acquisition of other lines of business or companies, and various forms of demutualization of ACIC permitted by District of Columbia law. After careful study and consideration, ACIC has concluded that the subscription rights method of demutualization best suits ACIC’s circumstances. See “The Conversion and the Offering — Background and Reasons for the Conversion.”

Our Market and Opportunities

Market for Our Commercial Automobile Products

ACIC currently offers its specialty commercial auto insurance products in the District of Columbia and 13 states. Traditionally, ACIC’s customers have been primarily taxi cab and passenger sedan operators, with a majority of its business written in the Mid-Atlantic States. Commencing in 2016, ACIC expanded into the Midwest and Southeast, and in 2016 ACIC began to offer commercial auto coverage to non-emergency medical transportation providers. The non-emergency medical transportation product proved to be unprofitable, and ACIC discontinued that product in 2018. ACIC also stopped writing premium in certain states that it determined to be unprofitable in 2019, including Florida, Kentucky, Georgia, and Mississippi.

The taxi cab and passenger sedan insurance market, which accounts for substantially all of ACIC’s written premiums historically, has been under pressure for several years due to competition from ride-sharing services such as Uber and Lyft, and the reduction in demand resulting from COVID-19 has added additional stress to this market. ACIC intends to continue to offer taxi cab and passenger sedan products and is introducing commercial auto insurance to trade and service providers, including electricians, plumbers, and carpenters, that its research has indicated present lower loss risk.

Our Competitive Strengths

We believe that we are strategically positioned to take advantage of the following competitive strengths:

| • | Experienced Management Team. Our management team, led by Patrick Bracewell, has an average of 25 years of experience in the commercial automobile insurance business. We recently added two new executive officers who have significant experience in the commercial insurance industry. |

| • | Rich History and Strong Reputation for Service. We have been in business since 1938 and are widely recognized in the specialty commercial automobile insurance industry for our customer service. |

| • | Scalable Platform. We believe that we can significantly increase our policy volume without a significant increase in expense. We have the administrative capacity and information systems to process and service additional policy volumes without a significant increase in personnel, additional technology or infrastructure expenditures. |

Our Growth Strategies

We intend to use our competitive strengths and the capital from this offering to grow our business through the following strategies:

| • | Introduce New Insurance Products to Trade and Service Providers. We are developing a commercial auto insurance product that we intend to introduce to trade and service providers such as electricians, plumbers, carpenters, and other service providers that our research has indicated present lower loss risk. In this market, the vehicle is a tool used in the business and is typically driven significantly fewer miles than in the taxi cab and passenger sedan business where the vehicle is the business. |

2

Table of Contents

| • | Expand our Distribution Capacity by Increasing our Agent Force. We intend to significantly expand our small force of independent producers by recruiting a substantial number of additional producers over the next five years. We also intend to explore relationships with agency networks and insurers that offer insurance to trade and service providers but who do not have a commercial auto product. |

| • | Pursue Acquisitions of Insurance Companies and Related Businesses. We intend to use the additional capital provided by this offering to explore possible acquisitions of other insurance companies to grow our business and leverage our existing available administrative capacity. We will also explore opportunities to acquire related businesses, such as insurance agencies, that can expand our distribution network. |

| • | Focus on Profitability and Improve Operating Efficiency. We are committed to improving our profitability by continuously seeking efficiencies within our operations. The expanded use of technological resources will continue to allow us to improve our processes, scalability, and response times. |

Our Challenges and Risks

Our company and our business are subject to numerous risks as more fully described in the section of this offering circular entitled “Risk Factors.” As part of your evaluation of our business, you should consider the challenges and risks we face in implementing our business strategies:

| • | Low Interest Rate Environment. Although the Federal Reserve raised key short term interest rates multiple times from the end of 2015 until the first quarter of 2020, the Federal Reserve cut short term rates in response to the economic downturn resulting from the COVID-19 pandemic. As a result, interest rates remain historically low. The prolonged period of low interest rates that began in 2008 has significantly reduced the returns on our investment portfolio. |

| • | History of Losses. ACIC experienced losses in three of the last six years primarily due to our expansion into new insurance products and new territories. Although ACIC has begun to target a new niche market of customers that it believes present a lower loss risk, acceptance of ACIC’s insurance products by these customers will take time and we may not achieve the market penetration that we project. Our B++ A.M. Best rating may also limit our ability to grow our business, which impairs our ability to leverage our operating expenses over a larger premium base. |

| • | Lack of Marketing Resources. We are small in relation to many of the insurance companies with which we compete. Larger insurance companies have a substantial advantage with respect to the resources that they can devote to advertising, marketing, and agent recruitment. Furthermore, their larger surplus permits them to maintain a larger book of business and spread their administrative expenses over a larger revenue base. In addition, we will need to develop and implement new marketing strategies in connection with the introduction of our new insurance products. |

| • | Lack of Multiple Distribution Channels. We rely primarily on ARM and ARM’s limited number of independent agents to distribute our insurance products. Growth in our written premiums will depend on our ability to recruit a number of new independent agents to distribute our insurance products. Much of the competition for talent involves agent recruitment. If our competitors have higher A.M. Best ratings, provide the agents with better technology, or pay higher commissions, our ability to attract and retain agents may be impaired, which could have a material and adverse effect on our ability to grow our business. |

| • | Intense Competition for Policyholders. We face intense competition for policyholders and compete with much larger insurance companies, many of which seek to sell commercial automobile insurance products to the same markets that we target. Most of these companies devote substantial resources to advertising and marketing to potential policyholders as well as to agent recruitment. Many of these |

3

Table of Contents

| companies have multiple distribution channels for their products and some employ in-house agents, which reduces their commission expense. In addition, several of these companies have well established Internet sales capabilities. |

Business Segments

We manage our business through two segments: insurance and commercial real estate investments. ACIC engages in the principal business line of commercial automobile insurance.

Our Companies

The Company is a newly created Pennsylvania business corporation organized to be the stock holding company for ACIC following the conversion. We formed the Company so that it could acquire all of the capital stock of ACIC as part of the conversion and acquire ARM. Prior to the conversion, the Company has not engaged and will not engage in any significant operations and does not have any assets or liabilities. After the conversion, our primary assets will be the outstanding capital stock of ACIC, the outstanding capital stock of ARM, and a portion of the net proceeds of the offerings.

ACIC has three indirect subsidiaries that hold investments in real estate in Washington, D.C.

In connection with the conversion, the Company has entered into an agreement with MCW pursuant to which upon completion of the conversion the Company will purchase all of the outstanding capital stock of American Risk Management, Inc. in exchange for 550,000 shares of convertible preferred stock of the Company. Completion of the purchase of ARM is contingent upon completion of the conversion and the offerings. See “Business — American Risk Management, Inc.”

Our executive offices are located at 8401 Connecticut Avenue, Suite 300, Chevy Chase, Maryland, 20815, and our phone number is (202) 547-8700. Our website address is www.asginsurance.com. Information contained on our website is not incorporated by reference into this offering circular, and such information should not be considered to be part of this offering circular.

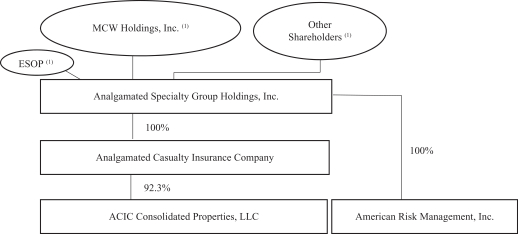

Our Structure Prior to the Conversion

Our current corporate structure is shown in the following chart:

Prior to the conversion, the Company has not engaged in any significant operations and does not have any assets or liabilities.

Our Structure Following the Conversion

Immediately upon the conversion of ACIC, all of the authorized capital stock of the converted ACIC will be issued to the Company, and the issued and outstanding shares of our capital stock will consist of the shares of

4

Table of Contents

common stock sold in the offerings, shares of preferred stock issued in connection with the acquisition of ARM, and any shares of our common stock that become subject to restricted stock awards granted under our stock based incentive plan.

Following the completion of these actions, our corporate structure will be as shown in the following chart:

| (1) | Following completion of the conversion and the offerings, the respective ownership and voting percentages of the number of shares of the Company’s outstanding capital stock owned by MCW Holdings, Inc., the ESOP, and all other shareholders of the Company are as follows, assuming that 2,660,000 shares are sold in the offering, which is the midpoint of the offering range, and that all of the shares of Series A Preferred Stock have been converted to shares of common stock: |

| Ownership Percentage | Voting Percentage | |||||||

| MCW Holdings, Inc |

14.7 | % | 14.7 | % | ||||

| ESOP |

8.4 | % | 8.4 | % | ||||

| All other shareholders |

76.9 | % | 76.9 | % | ||||

The Conversion of ACIC from Mutual to Stock Form

ACIC is a District of Columbia mutual insurance company. As a mutual company, it has no shareholders but it does have members. A member of ACIC is the owner of an in force individual policy issued by ACIC.

Like shareholders, the members have certain rights with respect to ACIC, such as voting rights with respect to the election of members of the board of trustees and approval of certain fundamental transactions, including the conversion of ACIC from mutual to stock form. However, unlike shares held by shareholders, the memberships in ACIC are not transferable and do not exist separately from the related insurance policy issued by ACIC. Therefore, these membership rights are extinguished when a member’s policy with ACIC is terminated by surrender, lapse, nonrenewal, or cancellation. Those membership interests will also be extinguished upon conversion of ACIC from mutual to stock form in accordance with District of Columbia law and the plan of conversion.

The board of trustees of ACIC adopted a plan of conversion on February 3, 2021, under which ACIC will convert from a mutual insurance company to a stock insurance company. Following the conversion, ACIC will become a wholly-owned subsidiary of the Company. A special meeting of the members of ACIC eligible to vote (those persons who were members of ACIC as of the close of business on February 3, 2021) will be held on [●],

5

Table of Contents

2021 (special meeting date), to approve the plan of conversion. To become effective, the plan must be approved by the affirmative vote of at least a majority of the votes cast at the special meeting.

The sale of sufficient shares to meet the offering minimum of 2,260,000 shares does not indicate that sales have been made to investors who have no financial or other interest in the offering, and the sale of 2,260,000 shares in the offering should not be viewed as an indication of the merits of the offering.

The Subscription Offering

We are offering shares of our common stock in a subscription offering. The subscription offering will end at noon, Eastern Time, on [●], 2021. In the subscription offering, 3,060,000 shares of common stock are being offered in the following order of priority: first, to the policyholders of ACIC as of the close of business on February 3, 2021, whom we refer to as eligible members, second, to our ESOP, and third, to the trustees, officers, and employees of ACIC.

The number of shares of common stock issued in the offerings will not exceed 3,060,000 shares. Shares purchased by the ESOP and by the trustees, officers, and employees of ACIC will be purchased for investment and not for resale and will be counted toward satisfaction of the minimum amount needed to complete this offering.

Except for any shares of restricted stock that will be granted to officers and directors of the Company upon completion of the offerings, and which will be subject to the satisfaction of certain conditions of vesting, the shares issued in the offerings will constitute all of the outstanding shares of the Company’s common stock after completion of the offerings.

The Public Offering

If less than 2,260,000 shares are subscribed for in the subscription offering, we will offer the remaining shares to the general public. The public offering will end at noon, Eastern Time, on [●], 2021.

The following table shows those persons that are eligible to purchase shares in the various phases of the offering and the shares available for purchase in each phase of the offering. We expect to conduct the subscription offering and the public offering simultaneously.

| Offering |

Eligible Purchasers |

Shares Available for Purchase | ||

| Subscription Offering | Policyholders of ACIC at February3, 2021; | 3,060,000 shares | ||

| The ESOP; and | 302,940 shares | |||

| Officers, trustees and employees of ACIC. | 3,060,000 shares, less shares subscribed for by eligible members and the ESOP | |||

| Public Offering | The general public. | 3,060,000 shares, less shares subscribed for in the subscription offering |

Redemption of Subscription Rights

Under the plan of conversion, each eligible member was granted the right to cause the Company to redeem such member’s right to purchase shares in the subscription offering, provided such member does not exercise his or her right by purchasing shares in the offering. Each eligible member may either:

| • | Exercise his or her subscription right by purchasing shares in the offering at the offering price of $10.00 per share; or |

| • | Elect, either affirmatively or by failing to purchase any shares in the offering, to have the Company redeem for cash such eligible member’s subscription right. Each eligible member who does not purchase any shares in the offering will receive cash in the amount of $1,489.87. |

6

Table of Contents

The redemption price for the subscription rights was determined by Boenning & Scattergood, Inc. (“Boenning”) in accordance with the valuation parameters specified in ACIC’s plan of conversion, including, but not limited to, the use of the Black-Scholes option pricing methodology. An eligible member would be able to purchase approximately 149 shares of the Company’s common stock in the subscription offering with the amount of cash that such member will receive as the redemption price for his subscription rights if the member elects not to purchase shares in the offering.

Any eligible member who has his or her subscription right redeemed will not be permitted to purchase shares of Company common stock in the offering. See “The Conversion and the Offering — Redemption of Subscription Rights for Cash.”

The following table presents a summary of selected pricing ratios for the peer group companies, and the resulting pricing ratios for the Company as converted. Compared to the average as converted pricing ratios of the peer group, the Company’s pro forma fully converted pricing ratios at the midpoint of the offering range indicated a discount of 51.4% on an as converted price-to-earnings basis, a discount of 33.2% on an as converted price-to-book value basis and a discount of 28.2% on an as converted price-to-tangible book value basis.

| As Converted Pro Forma Price-to-Earnings Multiple(1) |

As Converted Pro Forma Price-to-Book Value Ratio(1) |

As Converted Pro Forma Price-to- Tangible Book Value Ratio(1) |

||||||||||

| Amalgamated |

||||||||||||

| Maximum |

7.8 | 51.2 | % | 55.2 | % | |||||||

| Midpoint |

6.7 | 47.8 | % | 51.6 | % | |||||||

| Minimum |

5.6 | 43.9 | % | 47.7 | % | |||||||

| Valuation of peer group companies as of December 29, 2020(2) |

||||||||||||

| Averages |

16.2 | 81.9 | % | 83.6 | % | |||||||

| Medians |

13.8 | 71.6 | % | 71.9 | % | |||||||

| (1) | See the footnotes to the table at “Pro Forma Information — Additional Pro Forma Information” for the assumptions underlying the pro forma data. |

| (2) | Information for the peer group companies is based upon actual earnings for the twelve months ended September 30, 2020, and information for the Company is based upon actual earnings for the twelve months ended December 31, 2020. |

The fully converted pro forma calculations for the Company are based on the following assumptions:

| • | A number of shares equal to 9.9% of the shares sold in the conversion are purchased by the employee stock ownership plan, with the expense to be amortized over 10 years; and |

| • | no effect is given to any shares that may be issued pursuant to restricted stock awards and stock options that will be granted to directors and officers of the Company and ACIC upon the closing of the offering. |

The independent appraisal does not indicate trading market value. Do not assume or expect that our valuation as indicated in the appraisal means that after the offering the shares of our common stock will trade at or above the $10.00 per share price. Furthermore, Boenning used the pricing ratios presented in the appraisal to estimate our pro forma appraised value for regulatory purposes and not to compare the relative value of shares of our common stock with the value of the capital stock of the peer group. The value of the capital stock of a particular company may be affected by a number of factors such as financial performance, asset size and market location.

7

Table of Contents

For a more complete discussion of the amount of common stock we are offering for sale and the independent appraisal, see “The Conversion and Offering — The Appraisal.”

Conditions to Completion of the Conversion and this Offering

Before we can complete this offering and issue our common stock, the members of ACIC eligible to vote must approve the plan of conversion and we must sell at least the minimum number of shares offered in the offerings. No funds will be released from the escrow account until all of these conditions have been satisfied.

In 2011, MCW received approval from the Department to be the ultimate controlling party of ACIC in its mutual form. As detailed in the conversion application, which was approved on [●], 2021, MCW will have a controlling interest in our stock.

Termination of this Offering

We have the right to cancel this offering at any time. In addition, the completion of this offering is subject to market conditions and other factors beyond our control. If this offering is not completed, all funds received will be promptly returned to purchasers without interest.

Stock Pricing and Number of Shares to be Issued

The plan of conversion requires that the number of shares to be issued in connection with the conversion must be based on the range of valuation of our estimated consolidated pro forma market value. Under the plan of conversion, the valuation must be in the form of a range consisting of a midpoint valuation, a valuation fifteen percent (15%) above the midpoint valuation, and a valuation fifteen percent (15%) below the midpoint valuation. We retained Boenning to determine the valuation range for this offering. Boenning has determined that, as of December 30, 2020, the estimated consolidated pro forma market value of ACIC is $26.6 million at the midpoint, and the range of value of the total number of shares of common stock to be issued in the offering is between a minimum value of $22.6 million and a maximum value of $30.6 million. We plan to issue between 2,260,000 and 3,060,000 shares of our common stock in this offering. This range was determined by dividing the $10.00 price per share into the range of Boenning’s valuation. Shares purchased by the ESOP and the trustees, officers, and employees of ACIC will be purchased for investment and not for resale and will be counted toward satisfaction of the minimum amount needed to complete this offering.

We determined to offer the common stock in the subscription offering at the price of $10.00 per share to ensure a sufficient number of shares are available for purchase by eligible members. In addition, Griffin Financial Group, LLC. (“Griffin”) advised us that the $10.00 per share offering price is commonly used in mutual-to-stock conversions of other insurance companies and savings banks and savings associations that use the subscription rights conversion model. These were the only factors considered by our board of trustees in determining to offer shares of common stock at $10.00 per share.

How Do I Buy Stock in this Offering?

If you wish to purchase shares of common stock in the subscription offering, you must sign and complete the stock order form that accompanies this offering circular and send it to us with your payment such that your order is received before the offering deadline. You may submit your order to us by overnight delivery to the address indicated for this purpose on the top of the stock order form or by mail using the stock order reply envelope provided. Payment by personal check, cashier’s check or money order must accompany the stock order form. No cash or third party checks will be accepted. All checks or money orders must be made payable to “Computershare Trust Company, N.A., escrow agent, on behalf of Amalgamated Specialty Group Holdings, Inc.” We may permit certain persons who submit orders in the public offering to make payment by a wire transfer to the escrow agent of the purchase price for any shares that they seek to purchase.

8

Table of Contents

The completed stock order form and payment in full for the shares ordered must be received (not postmarked) no later than noon, Eastern Time, on [●], 2021. Once submitted, your order is irrevocable without our consent unless we terminate this offering. Our consent to any modification or withdrawal request may or may not be given in our sole discretion. We may reject a stock order form if it is incomplete, improperly completed, or not timely received.

How Do I Elect to Have My Subscription Right Redeemed by the Company?

Each eligible member is granted the right under the plan of conversion to purchase shares in the subscription offering. Eligible members may elect to have their subscription right redeemed by the Company for cash equal to $1,489.87 per eligible member. You may elect to have your subscription right redeemed by making such election on the stock order form that accompanies this offering circular and signing and returning it in the envelope provided. Any eligible member that does not purchase shares in the offering will be deemed to have elected to have such subscription right redeemed for cash. See “The Conversion and the Offering — Redemption of Subscription Right for Cash.”

Offering Deadline

All subscription rights will expire at noon, Eastern Time, on [●], 2021. Subscription rights not exercised prior to the termination date of this offering will be void, whether or not we have been able to locate each person entitled to receive subscription rights.

Limits on Your Purchase of Common Stock

The plan of conversion and District of Columbia law establish the following minimum and maximum purchase limitations for participants (including such participants’ associates or a group acting in concert) in the subscription offering:

| • | No person may purchase fewer than 50 shares in this offering. |

| • | No person other than the ESOP may purchase more than 100,000 shares in the subscription offering. |

| • | A person who is not an “accredited investor” as defined in Rule 501 of SEC Regulation D cannot purchase shares with an aggregate purchase price in excess of the greater of (x) 10% of their annual net income or net worth, as calculated in accordance with Rule 501 of Regulation D and (y) if the person is not a natural person, 10% of such person’s net assets or revenue for the most recently completed fiscal year. See “The Conversion and Offering — Limitations on Purchases of Common Stock.” |

| • | Subject to the prior right of each eligible member to subscribe for up to 100,000 shares in this offering, in no event may any person purchase more than 5% of the total number of shares sold in the subscription and public offerings without the prior approval of the Commissioner. |

| • | In addition to the limitations set forth above, no person may acquire, directly or indirectly, in this offering or any public offering, more than 5% of the capital stock of the Company for a period of five years from the effective date of the conversion without the approval of the Department. |

For purposes of the limitations described above, an associate of a person includes:

| • | any relative or spouse of such person, or any relative of such person’s spouse, who shares the same home as such person; |

| • | any corporation or other organization (other than the Company or a majority owned subsidiary of the Company) of which such person is an officer, director, or partner, or of which such person is, directly or indirectly, a beneficial owner of 10% or more of any class of equity securities; |

9

Table of Contents

| • | any trust or other estate in which such person has a substantial beneficial interest or as to which such person serves as trustee or in a similar fiduciary capacity (exclusive of any employee stock benefit plan of the Company, such as the ESOP); and |

| • | any person acting in concert with any of the persons or entities listed above. |

The subscription of any eligible member who subscribes for more than 100,000 shares will be reduced to 100,000 shares.

We have the right in our absolute discretion and without liability to any participant in the subscription offering or to any other person to determine which persons and which subscriptions and orders in this offering meet the criteria provided in the plan of conversion for eligibility to purchase shares of common stock and the number of shares eligible for purchase by any person. Our determination of these matters will be final and binding on all parties and all persons.

Oversubscription

If you are an eligible member and we receive subscriptions in the subscription offering for more than 3,060,000 shares, your requested subscription for shares may be reduced.

If eligible members in the aggregate subscribe for more than 3,060,000 shares, the shares of common stock will be allocated so as to permit each subscribing eligible member to purchase up to the lesser of the number of shares subscribed for or 1,000 shares. Any remaining shares will be allocated among the eligible members whose subscriptions remain unsatisfied in the proportion in which the number of shares as to which each such eligible member’s subscription remains unsatisfied bears to the aggregate number of shares as to which all such eligible members’ subscriptions remain unsatisfied.

Management Purchases of Stock

If the eligible members and the ESOP subscribe for less than the maximum number of shares, the trustees, officers, and employees of ACIC, together with their affiliates and associates, have indicated their intention to purchase up to approximately 800,000 shares of common stock in the subscription offering. The trustees, officers, and employees of ACIC and their affiliates and associates are not obligated to purchase this number of shares, and in the aggregate they may purchase a greater or smaller number of shares. See “The Conversion and Offering — Proposed Management Purchases.”

If there are insufficient shares remaining after the subscriptions of eligible members and the ESOP to satisfy in full all of the subscriptions of trustees, officers, and employees of ACIC, the available shares of common stock will be allocated among the subscribing trustees, officers, and employees in the proportion in which the number of shares as to which each such person subscribed bears to the aggregate number of shares remaining.

Undersubscription

If less than 2,260,000 shares are subscribed for in the subscription and public offerings, we will promptly return all funds received in the offerings to purchasers, without interest. In that event, we may cause a new valuation of ACIC to be performed, and based on this valuation amend the Offering Statement of which this offering circular is a part and commence a new offering of our common stock. In that event, people who submitted subscriptions or orders will be permitted to submit new subscriptions or orders. See “The Conversion and the Offering — Resolicitation.” Shares purchased by the ESOP and by directors, trustees, officers, and employees in the offering will be counted towards satisfying the requirement that at least 2,260,000 shares must be sold in the offerings.

10

Table of Contents

Benefits to Management

Our board of directors has also adopted a stock based incentive plan for the benefit of our directors, executive officers, and other eligible employees. Under the stock based incentive plan, we may award options to purchase common stock or award shares of restricted stock or restricted stock units to directors, executive officers, and other eligible employees. The exercise price of stock options will be no less than the fair market value of our common stock on the date of the option award. All awards under the stock based incentive plan will be subject to such vesting, performance criteria, or other conditions as the compensation committee of our board of directors may establish. Restricted stock units, shares of restricted stock, and options to purchase shares in an amount equal to 14.0% of the number of shares issued in the offerings may be awarded under the stock based incentive plan, provided that the total number of shares represented by restricted stock units and restricted shares can be no more than 4.0% of the number of shares issued in the offerings.

As discussed in more detail under “Executive Compensation,” we expect that grants of stock options to purchase 260,000 shares will be made to our executive officers and grants of 15,000 shares of restricted stock will be made to our non-employee directors, subject to completion of this offering.

The following table presents information regarding the participants in the stock based incentive plan, and the total amount, the percentage, and the dollar value of the stock that we intend to set aside for the stock based incentive plan. The table assumes the following:

| • | that 2,260,000 shares will be sold in the offerings; and |

| • | that the value of the stock in the table is $10.00 per share. |

The exercise price of any options granted under the stock based incentive plan will be at least equal to the fair market value of the stock on the day the options are awarded or, in the case of options granted at the time of this offering, the price at which stock is sold in this offering. As a result, anyone who receives an option will benefit from the option only if the price of the stock rises above the exercise price and the option is exercised. The numbers in the following table assumes that 2,660,000 shares are sold in the offering, which is the midpoint of the offering.

| Stock Based Incentive Plan |

Individuals |

Number of Shares |

Percentage of shares issued in the offering |

Value of shares Based on $10.00 Share Price |

||||||||||

| ESOP |

All full time employees | 263,340 | 9.9 | % | $ | 2,633,400 | ||||||||

| Shares available for restricted stock or restricted stock unit awards |

Directors and selected officers | 106,400 | (1) | 4.0 | % | $ | 1,064,000 | |||||||

| Shares available for stock options |

Directors and selected officers | 266,000 | (1) | 10.0 | % | (1 | ) | |||||||

| (1) | Assumes that options to purchase 10% of the number of shares issued in the offering are awarded under the plan and shares of restricted stock or restricted stock unit awards equal to 4.0% of the number of shares issued in the offerings are granted under the plan. Stock options will be granted with a per share exercise price at least equal to the market price of our common stock on the date of the grant. The value of a stock option will depend, among other things, upon increases, if any, in the price of our common stock during the term of the option. |

A minimum of 2,260,000 shares and a maximum of 3,060,000 shares of our common stock will be issued in the subscription and public offerings, excluding any shares that may be issued under our stock based incentive plan.

11

Table of Contents

Use of Proceeds

We estimate the net proceeds from the offerings will be approximately $15.0 million at the minimum, $18.3 million at the midpoint, and $21.7 million at the maximum of the offering range. See the “Offering Summary” on the front cover of this offering circular for the assumptions used to arrive at these amounts. The amount of net proceeds from the sale of common stock in the offerings will depend on the total number of shares actually sold in the subscription and public offerings.

We expect to use up to approximately $2.4 million of the net proceeds of the offerings to pay the redemption price for subscriptions redeemed by eligible members. We may use a portion of the net proceeds to repay all or part of the $1.4 million of indebtedness that we will assume as part of the purchase of ARM. We plan to contribute approximately $2.0 million of the net proceeds from the offerings to ACIC, which will be used to (i) support organic growth of our insurance business; (ii) fund new product launches; and (iii) selectively deploy new capital to retain, acquire, and bolster talent in key areas.

We expect to retain any remaining net proceeds from the offerings at the Company, to be used for general corporate purposes, which may include acquisitions of other insurance companies or related businesses, and stock repurchases or cash dividends, including dividends on our Series A Preferred Stock. On a short term basis, the proceeds retained at the Company will be invested primarily in securities consistent with our investment strategy until utilized. We have no other current specific plans for use of the net proceeds of the offering. See “Use of Proceeds.”

Dividend Policy

Following completion of this offering, our board of directors will have the authority to declare dividends on our shares of common stock, subject to statutory and regulatory requirements. Any decision to pay a dividend will depend on many factors, including our financial condition and results of operations, liquidity requirements, market opportunities, capital requirements of our subsidiaries, legal requirements, regulatory constraints, intercompany dividends from our subsidiaries, and other factors as the board of directors deems relevant.

We currently expect to pay quarterly cash dividends on our Series A Preferred Stock when such dividends are due. The accrued dividends payable on our Series A Preferred Stock will total $468 thousand per year. For additional information regarding restrictions on our ability to pay dividends, see “Dividend Policy.”

Market for Common Stock

We do not intend to apply for the listing of our common stock on the NASDAQ Capital Market or any other stock exchange. People considering purchasing shares in the offerings should note that this will materially and adversely affect the liquidity of our stock. See “Risk Factors — Risks Relating to Ownership of Our Common Stock — Our shares will not be listed on any stock exchange, and there will not be an active, liquid market for our common stock.” We intend to apply to have “buy” and “sell” quotes for shares of our common stock reported on the “OTC Pink” market by broker-dealers that agree to make a market in our common stock. We may also engage in share repurchases from time to time if we determine that we have excess capital.

How You May Obtain Additional Information Regarding this Offering

If you have any questions regarding the stock offering, please call the Stock Information Center at (610) 205-6005, Monday through Friday between 10:00 a.m. and 4:00 p.m., Eastern Time.

12

Table of Contents

An investment in our common stock involves a number of risks. Before making a decision to purchase our common stock, you should carefully consider the following information about these risks, together with the other information contained in this offering circular. Many factors, including the risks described below, could result in a significant or material adverse effect on our business, financial condition, and results of operations. If this were to happen, the price of our common stock could decline significantly and you could lose all or part of your investment.

Risks Relating to Our Business

ACIC has incurred both statutory and GAAP net losses in recent years.

ACIC has incurred both statutory and GAAP net losses in three of the last six years. ACIC’s losses are due principally to high loss ratios resulting from our expansion into unprofitable non-core product lines such as non-emergency medical transportation and into unprofitable states, as well as prevailing low returns on our investment portfolio. We need to increase the sales of our profitable core insurance products and deploy new profitable insurance products, by investing in new product development, expanding distribution capability, and implementing technology solutions in order to continue our return to profitability.

If we cannot expand our distribution network and resulting sales of our products, we may incur further losses.

Our ability to increase sales of our existing and new insurance products will depend on our success in expanding our distribution network. We depend on ARM, ACIC’s controlling producer, and on its network of independent insurance agents to generate almost all of the sales of our insurance products. If we are unable to increase sales to customers by establishing relationships with other distribution partners, it may be difficult to remain profitable.

The impact of COVID-19 and responses thereto, and related risks, could continue to materially affect our results of operations, financial position, and/or liquidity.

Beginning in March 2020, the global pandemic related to novel coronavirus COVID-19 started to impact the global and U.S. economy. The extent of this pandemic continues to evolve, thus the full direct and indirect impacts of COVID-19 are not yet known and may not emerge for some time. ACIC has experienced a decrease in premiums due to the COVID-19 pandemic, that has negatively impacted our taxi cab and sedan customers, who are highly exposed to the travel and leisure industries. Those industries have been adversely impacted by COVID-19, and our premiums may continue to decrease as the travel and leisure industries remain depressed and our insureds seek to limit expenses, including the cost of insurance.

Federal, state, and local government actions to address and contain the impact of COVID-19 may adversely affect us. For example, we could be subject to proposed legislative and/or regulatory action that seeks to retroactively mandate coverage for losses which our insurance policies were not designed or priced to cover. Currently, in some states, there is proposed legislation to require insurers to cover business interruption claims irrespective of terms, exclusions, or other conditions included in the policies that would otherwise preclude coverage. Regulatory restrictions or requirements could also impact pricing, risk selection, and our rights and obligations with respect to our policies and insureds, including our ability to cancel policies or our right to collect premiums. At least one state regulator has issued an order requiring insurers to issue premium refunds, and regulators in other states could take similar actions. It is also possible that changes in economic conditions and steps taken by federal, state, and local governments in response to COVID-19 could require an increase in taxes at the federal, state, and local levels, which would adversely impact our results of operations and place further stress on our insureds.

Our corporate fixed income portfolio may be adversely impacted by ratings downgrades, increased bankruptcies, and credit spread widening in distressed industries. In addition, many state and local governments

13

Table of Contents

may be operating under deficits or projected deficits. These deficits may be exacerbated by the costs of responding to COVID-19 and reduced tax revenues due to adverse economic conditions. The severity and duration of these deficits could have an adverse impact on the collectability and valuation of our municipal bond portfolio. Our investment portfolio also includes residential and commercial mortgage-backed securities, which could be adversely impacted by declines in real estate valuations and/or financial market disruption, including a heightened collection risk on the underlying mortgages. Further disruptions in global financial markets due to the continuing impact of COVID-19 could result in additional net realized and unrealized investment losses. In addition, declines in fixed income yields would result in decreases in net investment income from future investment activity, including re-investments.

We expect that the impact of COVID-19 on general economic activity may continue to negatively impact our premium volumes. We have experienced this impact in the last three quarters of 2020 and this impact may further persist for much of 2021, but the degree of the impact will depend on the extent and duration of the economic contraction. As a result of the anticipated impact of the pandemic on our earned premiums, our underwriting expense ratio may increase in the near term.

It is possible that changes in economic conditions and steps taken by the federal government and the Federal Reserve in response to COVID-19 could lead to higher inflation than we had anticipated, which could in turn lead to an increase in our loss costs and the need to strengthen claims and claim adjustment expense reserves. These impacts of inflation on loss costs and claims and claim adjustment expense reserves could be more pronounced for those types of claims that require a relatively longer period of time to finalize and settle and, accordingly, are relatively more inflation sensitive. Inflation could also adversely impact our general and administrative expenses. Changes in interest rates caused by inflation affect the carrying value of our fixed maturity investments and returns on our fixed maturity and short-term investments. An increase in interest rates reduces the market value of existing fixed maturity investments, thereby negatively impacting our book value.

Our results of operations have been adversely affected by the current low interest rate environment and will continue to be adversely affected if interest rates remain low or if interest rates should rapidly increase.

Although the Federal Reserve moved to marginally increase short-term interest rates from 2015 to December 2019, medium and long-term interest rates have remained at historically low levels. In response to the economic downturn resulting from the COVID-19 pandemic, the Federal Reserve has cut short-term interest rates to near record lows. During a period of decreasing interest rates or a prolonged period of low interest rates, our investment earnings may decrease because the interest earnings on our recently purchased fixed income investments will likely have declined in parallel with market interest rates. In addition, callable fixed income securities in our investment portfolio will be more likely to be prepaid or redeemed as borrowers seek to borrow at lower interest rates. Consequently, we may be required to reinvest the proceeds in securities bearing lower interest rates. An extended period of declining or prolonged low interest rates may also cause us to change our assumptions of the interest rates that we can earn on our investments and the long-term interest rate that we assume in our calculation of insurance assets and liabilities under GAAP. This revision would result in increased reserves, accelerated amortization of deferred acquisition costs (“DAC”), and other unfavorable consequences. In addition, certain statutory capital and reserve requirements are based on formulas or models that consider interest rates, and an extended period of low interest rates may increase the statutory capital we are required to hold and the amount of assets we must maintain to support statutory reserves.

Conversely, an increase in market interest rates could also have a material adverse effect on the value of our investment portfolio by, for example, decreasing the estimated fair values of the fixed income securities within our investment portfolio. Also, certain statutory reserve requirements are based on formulas or models that consider forward interest rates and an increase in forward interest rates may increase the statutory reserves we are required to hold, thereby reducing statutory capital.

14

Table of Contents

Our B++ rating from A.M. Best limits our ability to attract agents and to sell rating sensitive products.

ACIC is rated B++ by A.M. Best. This rating adversely affects our ability to attract agents and sell our products because ratings assigned by A.M. Best are an important factor influencing the competitive position of insurance companies. Financial strength ratings are used by producers and customers as a means of assessing the financial strength and quality of insurers. A.M. Best ratings, which are reviewed at least annually, represent independent opinions of financial strength and ability to meet obligations to policyholders and are not directed toward the protection of investors. Any future downgrade of our A.M. Best rating could negatively affect our ability to implement our strategy. See “Business — Competition and Ratings.”

We rely on our systems and employees, and those of certain third-party vendors and service providers, in conducting our operations, and certain failures, operational errors, systems malfunctions, or cyber-security incidents, could materially adversely affect our operations.

We are exposed to many types of operational risk, including clerical and recordkeeping errors, and computer or telecommunications systems malfunctions. If any of our operational, accounting, or other data processing systems fail or have other significant shortcomings, we could be materially adversely affected. We use a third party servicer to provide all of our data processing and storage functions. While our third party provider takes commercially reasonable measures to keep their systems and our data secure, it is difficult or impossible to defend against all risks being posed by changing technologies as well as criminals intent on committing cybercrime. Increasing sophistication of cyber criminals and terrorists make keeping up with new threats difficult and could result in a breach. As a result, our outside service provider may be unable to anticipate the type or manner of attempts to breach their security or to implement adequate preventative measures against these attempts. We may be required to expend significant capital to alleviate problems caused by security breaches.

Any breach or perceived breach of our security could damage our reputation and our relationship with our policyholders and agents. Reputational damage of this kind could significantly harm our business. For example, insureds and agents may be less likely to use our products following a breach because of a perceived weakness in our information security measures. Additionally, we could be subject to significant liability as well as regulatory action, which would have a material and adverse effect on our business, financial condition, results of operations, and prospects.

Our operations are dependent on access to key technology tools; if we lose access to these tools, our ability to conduct business could be significantly impaired.

In the event of a disaster such as a natural catastrophe, an epidemic, an industrial accident, a blackout, a computer virus, a terrorist attack, a cyber-attack, or a war that causes the data processing systems of our third party servicers to not function, unanticipated problems with our disaster recovery systems would have an adverse impact on our ability to conduct business and on our results of operations and financial position, particularly if those problems affect our internet access, computer-based data processing, transmission, storage and retrieval systems or destroy valuable data. Despite such third party servicers’ implementation of security measures, disaster recovery plans, system backup plans, and offsite arrangements to reduce the risk of a loss of access to these critical systems, there is no assurance that these security measures and backup plans will work when needed or would protect the Company in all circumstances that could arise. An interruption in our business because of our inability to access our key technology tools could result in the loss of revenue and damage to our reputation, and could have a material and adverse effect on our business, financial condition, results of operations, and prospects.

In the ordinary course of our business we can face coverage disputes and lawsuits that are expensive and time consuming and may include claims for extra-contractual damages, which, if resolved adversely, could harm our business, financial condition, or results of operations.

From time to time, we are involved in coverage and other types of lawsuits in the ordinary course of our business. Defending these claims is costly and can impose a significant burden on our management and

15

Table of Contents

employees. We utilize reinsurance to limit our exposure on the insurance policies we issue. Our reinsurance arrangements provide a level of coverage for extra-contractual damages, subject to the terms and limits of those arrangements. If we are found to be liable for significant extra-contractual damages in future cases, however, there could be a material and adverse effect on our business, financial condition, results of operations, and prospects.

Legal and regulatory investigations and actions are increasingly common in the insurance business and may result in financial losses and harm our reputation.

We face a risk of litigation and regulatory investigations and actions in the ordinary course of operating our business, including the risk of class action lawsuits. ACIC may become subject to class actions and regulatory actions or may become subject to individual lawsuits relating, among other things, to sales or underwriting practices, payment of contingent or other sales commissions, claims payments and procedures, product design, disclosure, administration, additional premium charges for premiums paid on a periodic basis, denial or delay of benefits, and breaches of fiduciary or other duties to customers. Plaintiffs in class action and other lawsuits against ACIC may seek very large or indeterminate amounts, including punitive and treble damages, which may remain unknown for substantial periods of time.

ACIC is also subject to various regulatory inquiries, such as information requests, subpoenas, market conduct exams, and books and record examinations, from state and federal regulators and other authorities, which may result in fines, recommendations for corrective action or other regulatory actions. Current or future investigations, proceedings, or regulatory actions could have an adverse effect on our business, results of operations, and financial condition. Moreover, even if we ultimately prevail in the investigation, proceeding, or regulatory action, we could suffer significant reputational harm, which could have an adverse effect on our business. Increased regulatory scrutiny and any resulting investigations or proceedings could result in new legal actions or precedents and industry-wide regulations or practices that could have a material and adverse effect on our business, financial condition, results of operations, and prospects.

We rely on the leadership of the members of our executive management team. The loss of any of these executives could have an adverse impact on our business and our ability to implement our business strategy.

The success of our business is dependent, to a large extent, on our ability to attract and retain key employees including the following members of our executive management team: Patrick Bracewell, Chairman, President and Chief Executive Officer; Daniel McFadden, Treasurer and Secretary; Richard Hutchinson, President and Chief Operating Officer of ACIC, Brian Mancino, Vice President — Distribution of ACIC; Michael McColley, Vice President — Insurance Operations of ACIC; and Joseph Niemer, Vice President — Digital Commerce and Technology of ACIC. Our executive management team has extensive experience in the insurance business. Were we to lose any of these employees, it may be challenging for us to attract a replacement employee with comparable skills and experience in our market niches. Except for the employment agreement with Patrick Bracewell, we do not have employment agreements with our executive officers. See “Executive Compensation- Employment Agreements.” We do not currently maintain key man life insurance policies with respect to any member of our senior management team.

We may be required to establish an additional valuation allowance against deferred income tax assets if our business does not generate sufficient taxable income or if our tax planning strategies are modified, which could have a material adverse effect on our results of operations and financial condition.

Deferred income tax represents the tax effect of the differences between the financial accounting and tax basis of assets and liabilities. Deferred tax assets represent the tax benefit of future deductible temporary differences, operating loss carryforwards, and tax credit carryforwards. We periodically evaluate and test our ability to realize our deferred tax assets. Deferred tax assets are reduced by a valuation allowance if, based on the weight of evidence, it is more likely than not that some portion, or all, of the deferred tax assets will not be

16

Table of Contents

realized. In assessing the more likely than not criteria, we consider future taxable income as well as prudent tax planning strategies. Future facts, circumstances, tax law changes, and financial accounting or GAAP developments may result in an increase in the valuation allowance. An increase in the valuation allowance could have a material adverse effect on the Company’s results of operations and financial condition.

As of December 31, 2020, ACIC had recorded a valuation allowance of $221 thousand to the net deferred tax asset of $221 thousand. To the extent we are required to establish an additional valuation allowance against future deferred income tax assets, the amount of such valuation allowance would be charged against our net income for the period in which that valuation allowance is established, which could have a material and adverse effect on our business, financial condition, results of operations, and prospects.

We operate in a heavily state regulated industry, and the prospect exists for further federal involvement in the regulation of insurance companies.

Our business is regulated by government agencies in the states in which we do business, and we must comply with a number of state and federal laws and regulations. Most insurance regulations are intended to protect the interests of current and potential policyholders rather than those of shareholders and other investors in insurance services companies.

State laws and regulations that apply to us include those governing the financial condition of insurers, including standards of solvency, risk-based capital requirements, types, quality and concentration of investments, establishment and maintenance of reserves, required methods of accounting, reinsurance and requirements, and those governing the business conduct of insurers, including transactions with affiliates, sales and marketing practices, claim procedures and practices, and policy form content. In addition, state insurance laws require licensing of insurers and their agents. State insurance regulators have the power to grant, suspend, and revoke licenses to transact business and to impose substantial fines and other penalties.

We may be unable to comply fully with the wide variety of applicable laws and regulations that are frequently undergoing revision. In addition, we follow practices based on our interpretations of laws and regulations that we believe are generally followed by the insurance industry. These practices may be different from interpretations of insurance regulatory agencies. Moreover, in order to enforce applicable laws and regulations or to protect policyholders, insurance regulatory agencies have relatively broad discretion to impose a variety of sanctions, including examinations, corrective orders, suspension, revocation or denial of licenses, and the takeover of insurance companies. As a result, if we fail to comply with these laws and regulations, state insurance departments can exercise a range of remedies from the imposition of fines to being placed in rehabilitation or liquidation. State insurance departments also conduct periodic examinations of the affairs of insurance companies and require the filing of annual, quarterly, and other reports relating to financial condition, holding company issues and other matters. These regulatory requirements may adversely affect or inhibit our ability to achieve some or all of our business objectives. Changes in the level of regulation of the insurance industry or changes in laws or regulations or interpretations of laws and regulations by regulatory authorities could adversely affect our ability to operate our business.

We are subject to various accounting and financial requirements established by the National Association of Insurance Commissioners (“NAIC”) as adopted by the states in which we operate. In addition, state regulators and the NAIC continually re-examine existing laws and regulations, with an emphasis on insurance company solvency issues and fair treatment of policyholders. Insurance laws and regulations could change or additional restrictions could be imposed that are more burdensome. Because these laws and regulations are for the protection of policyholders, any changes may not be in your best interest as a shareholder.

The commercial auto specialty transportation insurance industry in which we operate is highly competitive, which may limit our ability to maintain and increase our share of our target market.