Preliminary Offering Circular

December 4, 2020

Subject to Completion

LIGHTHOUSE LIFE CAPITAL, LLC

1100 E. Hector Street, Suite 415

Conshohocken, PA 19428

445-200-5650

8.5% Senior Beacon Bonds (Class A Bonds)

6.5% Senior Beacon Bonds (Class B Bonds)

$50,000,000 Aggregate Maximum Offering Amount (50,000

Bonds)

$10,000 Minimum Purchase Amount (10 Bonds)

Lighthouse Life

Capital, LLC, a Delaware limited liability company, or the company,

is offering a maximum of $50,000,000 in the aggregate, of its 8.5%

senior beacon bonds, or “Class A Bonds,” and its 6.5%

senior beacon bonds, or “Class B Bonds,” collectively

the “Bonds,” pursuant to this offering circular. The

purchase price per Bond is $1,000, with a minimum purchase amount

of $10,000, or the “minimum purchase”; however, the

company, in our sole discretion, reserves the right to accept

smaller purchase amounts. The Class A Bonds and the Class B Bonds

will bear interest at 8.5% and 6.5% per year, respectively. The

maximum offering amount of Bonds across both classes is $50,000,000

(the “Maximum Offering Amount”); however, the sale of

the Class B Bonds will be limited to a maximum of $30,000,000. The

Class A Bonds and Class B Bonds will each be offered serially, over

a maximum period of two years, starting from the date of

qualification of the Offering Statement of which this Offering

Circular is a part, with the sole difference between the series

being their respective maturity dates. Each series of Bonds

beginning with Series A-1 for Class A Bonds and Series B-1 for

Class B Bonds will correspond to a particular closing for the

applicable class of Bonds. Each series of Class A Bonds will mature

on the fifth anniversary of the issuance date of such series and

each series of Class B Bonds will mature on the third anniversary

of the issuance date of such series. Upon maturity, and subject to the terms and

conditions described in this offering circular, the Bonds will be

automatically renewed at the same interest rate and

for the same term, unless redeemed

upon maturity at our or your election. If the Bonds are not renewed

and without the consent of the Bondholders, we may elect to extend

the maturity date of the Bonds for an additional six months to

facilitate the redemption of the Bonds. Interest on the

Bonds will be paid monthly on the 15th day of the month. The first interest

payment on a Bond will be paid on the 15th day of the month following the issuance

of such Bond.

Bondholders will have the right to have their

Bonds redeemed at any time prior to the maturity date, subject to

an annual cap of 10% on all redemptions, regardless of the reason

for the redemption, and a penalty of between 6.5% and 8.5% for the

Class A Bonds, and 8.5% on the Class B Bonds, regardless of when

such Class A Bonds or Class B Bonds are redeemed (the “10%

Limit”). Bondholders will also have the right to have their

Bonds redeemed in the case of a bondholder’s death,

disability or bankruptcy, subject to notice, discounts and other

provisions contained in this offering circular. Redemptions due to

death, disability or bankruptcy shall count towards the

annual 10% Limit on redemptions described above. See

“Description of Bonds

– Redemption Upon Death, Disability or

Bankruptcy” and “Description of Bonds

– Bond Redemptions” for more

information.

(i)

The

Bonds will be offered to prospective investors on a best efforts

basis by International Assets Advisory LLC (“IAA”), our

underwriter and managing broker-dealer, a Florida limited liability

company and a member of the Financial Industry Regulatory

Authority, or “FINRA.” “Best efforts” means

that our managing broker-dealer is not obligated to purchase any

specific number or dollar amount of the Bonds, but it will use its

best efforts to sell the Bonds. Our managing broker-dealer may

engage additional broker-dealers, or “Selling Group

Members,” who are members of FINRA, to assist in the sale of

the Bonds. At each closing date, the net proceeds for such

closing will be disbursed to our company and Bonds relating to

such net proceeds will be issued to their respective investors. We

expect to commence the sale of the Bonds as of the date on which

the offering statement is declared qualified by the United States

Securities and Exchange Commission, or the “SEC,” and

terminate the offering on earliest of: (i) the date we sell the

Maximum Offering Amount; (ii) the second anniversary of the date of

qualification of this offering statement; or (iii) such date upon

which we determine to terminate the offering, in our sole

discretion. Notwithstanding the

previous sentence, we have the right, in our sole discretion, to

extend this offering beyond the second anniversary of the date of

qualification for an additional year.

|

|

Price to

Investors

|

Managing

Broker-Dealer Fee, Commissions, Reallowance and Wholesaling Fee

(1)(2)

|

Proceeds

to

Company

|

Proceeds to

Other Persons

|

|

|

|

|

|

|

|

Per Class A Bond

(3)

|

$1,000

|

$80

|

$920

|

$0

|

|

Per Class B Bond

(3)

|

$1,000

|

$80

|

920

|

$0

|

|

Maximum Offering

Amount of Class A Bonds (3)

|

$50,000,000

|

$4,000,000

|

$46,000,000

|

$0

|

|

Maximum Offering

amount of Class B Bonds (3)

|

$30,000,000

|

$2,400,000

|

$27,600,000

|

$0

|

(1)

This includes (a) selling commissions of (i) 5.00% of gross

offering proceeds on the sale of Class A Bonds and (ii) 4.50% of

gross offering proceeds on the sale of Class B Bonds, (b) a

managing broker-dealer fee of up to 2.00% of the gross proceeds of

the offering, (c) a reallowance 1.00% of gross proceeds from the

certain sales of the Bonds, and

(d) wholesaling fee of 0.50% of

gross offering proceeds on the sale of Class B Bonds, or,

collectively, Selling Commissions and Expenses. All Selling

Commissions and Expenses will be paid to IAA as our managing

broker-dealer, who may reallow all or any portion of the selling

commissions and reallowance to Selling Group Members. Selling

Commissions and Expenses will not exceed 8.0% of the gross proceeds

of the Class A Bonds or Class B Bonds. See “Use of

Proceeds” and “Plan of

Distribution” for more information.

(2) The

table above does not include organizational and offering expenses,

or O&O Expenses, estimated to be 2.00% of offering proceeds

($1,000,000 at the Maximum Offering Amount).

(3) All

figures are rounded to the nearest dollar.

_________

Generally,

no sale may be made to you in the offering if the aggregate

purchase price you pay is more than 10% of the greater of your

annual income or net worth. Different rules apply to accredited

investors and non-natural persons. Before making any representation

that your investment does not exceed applicable thresholds, we

encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For

general information on investing, we encourage you to refer to

www.investor.gov.

An

investment in the Bonds is subject to certain risks and should be

made only by persons or entities able to bear the risk of and to

withstand the total loss of their investment. Currently, there is

no market for the Bonds being offered, nor does our company

anticipate one developing. Prospective investors should carefully

consider and review that risk as well as the RISK FACTORS beginning

on page 10 of this offering circular.

THE

SEC DOES NOT PASS UPON THE MERITS OR GIVE ITS APPROVAL TO ANY

SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS

UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR

OTHER SELLING LITERATURE. THESE SECURITIES ARE OFFERED PURSUANT TO

AN EXEMPTION FROM REGISTRATION WITH THE SEC; HOWEVER, THE COMMISION

HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES

OFFERED ARE EXEMPT FROM REGISTRATION.

FORM 1-A DISCLOSURE FORMAT IS BEING

FOLLOWED.

(ii)

TABLE OF CONTENTS

|

Contents

|

|

|

OFFERING

CIRCULAR SUMMARY

|

2

|

|

CAUTIONARY

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

|

9

|

|

RISK

FACTORS

|

10

|

|

USE OF

PROCEEDS

|

20

|

|

PLAN OF

DISTRIBUTION

|

21

|

|

MANAGEMENT'S

DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

|

28

|

|

GENERAL

INFORMATION AS TO OUR COMPANY

|

30

|

|

MATERIAL

U.S. FEDERAL INCOME TAX CONSIDERATIONS

|

35

|

|

ERISA

CONSIDERATIONS

|

38

|

|

DESCRIPTION

OF BONDS

|

40

|

|

LEGAL

PROCEEDINGS

|

45

|

|

SECURITY

OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT

|

46

|

|

BOARD

OF DIRECTORS AND EXECUTIVE OFFICERS

|

47

|

|

EXECUTIVE

COMPENSATION

|

48

|

|

INDEPENDENT

AUDITORS

|

49

|

|

LEGAL

MATTERS

|

50

|

|

WHERE

YOU CAN FIND ADDITIONAL INFORMATION

|

51

|

|

INDEX

TO FINANCIAL STATEMENTS

|

F-1

|

(iii)

ABOUT THIS OFFERING CIRCULAR

The information in this offering circular may not

contain all of the information that is important to you. You should

read this entire offering circular and the exhibits carefully

before deciding whether to invest in the Bonds. See

“Where You

Can Find Additional Information” in this offering

circular.

Unless

the context otherwise indicates, references in this offering

circular to the terms “company,” “we,”

“us,” and “our,” refer to Lighthouse Life

Capital, LLC, a Delaware limited liability company, and the term

“our predecessor” refers to Lighthouse Life Solutions,

LLC, a Delaware limited liability company.

References

to a “Lawful Policyowner” refer to the owner of a life

insurance policy obtained in accordance with applicable laws and

the terms of the life insurance policy through (a) the initial

purchase of the policy by persons with insurable interest in the

individual insured under the policy, or (b) the acquisition of a

policy through the assignment, bequest, gift, sale or other

transfer executed under the terms of the policy, including but not

necessarily limited to the contract’s assignment, change of

ownership, and/or change of beneficiary clauses.

References

to a “Lawful Purchaser” refer to purchaser of a life

insurance policy from a Lawful Policyowner in accordance with

applicable laws and the terms of the policy.

1

This

summary highlights information contained elsewhere in this offering

circular. This summary does not contain all of the information that

you should consider before deciding whether to invest in the Bonds.

You should carefully read this entire offering circular, including

the information under the heading “Risk Factors”

and all information included in this offering

circular.

Our

Company,

Lighthouse Life Capital, LLC, a Delaware limited liability company,

was formed on July 8, 2020, to continue and grow the business of our

predecessor, to originate and acquire life

insurance policies through the highly regulated life settlement

market for the benefit of third-party purchasers of those policies.

In addition to other sources of revenue described below, our

company, through its subsidiaries, receives fees from third-party

purchasers and/or a share of third-party purchasers’ profits

on the acquired policies (above a certain target return threshold)

in exchange for our company’s services.

A

life settlement is the sale of a life insurance policy by the

Lawful Policyowner to a Lawful Purchaser of the policy; this

includes the sale of life insurance policies insuring the lives of

individuals who have been diagnosed as terminally ill or

chronically ill, also known as viatical settlements. The life

settlement asset class and the returns generated by the

origination, acquisition, sale and/or maturity of life insurance

policies are generally uncorrelated to traditional asset classes

(stocks, bonds, real estate and commodities). As such, life

settlements have been utilized to diversify portfolios and generate

non-correlated yield.

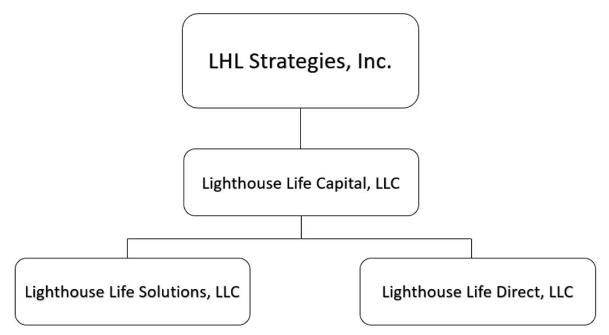

We generate substantially all of our revenues

through our wholly owned subsidiaries, Lighthouse Life Solutions,

LLC (“Lighthouse Life Solutions”) and Lighthouse Life

Direct, LLC (“Lighthouse Life Direct”). We acquired

Lighthouse Life Solutions and Lighthouse Life Direct from our sole

member, LHL Strategies, Inc. (“LHL Strategies”)

on July 8, 2020.

It’s

100% membership interest in us is our sole member’s only

asset, and it has not previously conducted an offering of any

direct participation program. Lighthouse Life

Solutions is considered our predecessor.

Through

Lighthouse Life Solutions, the company originates and acquires life

insurance policies from Lawful Policyowners for the benefit of

third-party purchasers. We employ a single-brand marketing strategy

to market and advertise life settlements (a) to a wide range of

financial professionals, such as insurance producers and financial

advisors and (b) directly to life insurance policyowners and

others.

Our

principal executive offices are located at 1100 Hector Street,

Suite 415, Conshohocken, PA 19428, and our telephone number is

445-200-5650.

Our

company, through Lighthouse Life Solutions, is an originator of

life insurance policies. Lighthouse Life Solutions is currently a

licensed buyer of policies, known as a life settlement provider, in

22 states. In states we are not licensed, Lighthouse Life Solutions

has relationships with other licensed entities for the origination

and purchase of life insurance policies, which expands our ability

to originate life insurance policies to additional states. Eight

states do not require a license to originate and/or acquire life

insurance policies. In total, we currently can engage in the

origination and/or acquisition of life insurance policies in 39

states, plus the District of Columbia, in which approximately 94

percent of the US population resides. Lighthouse Life Solutions

currently has applications for life settlement provider licenses

pending with a number of state insurance departments and we expect

to continue to apply for and obtain additional life settlement

provider licenses in the future.

Lighthouse

Life Solutions receives potential life settlement opportunities

from several sources, including:

●

Financial

professionals (i.e. insurance producers and financial advisors)

through the Lighthouse Life Settlement Advisor

Program;

●

Lighthouse

Life Direct, our advertising company, which engages in a full-range

of direct-to-consumer marketing and advertising to life insurance

policyowners and others; and

●

Intermediaries,

including licensed life settlement brokers and life settlement

providers.

2

We

currently generate revenues from three sources:

●

Fees

paid by third-party purchasers of policies for originating and

acquiring life insurance policies for the benefit of such

third-party purchasers. When originating life insurance policies

for a fee, we do not use the company’s funds to purchase the

policies, and we do not take possession of the

policies.

●

Fees

and, if applicable, profit sharing paid to us for the origination

and acquisition of life insurance policies for the benefit of a

third-party purchaser, pursuant to the Letter Agreement (as defined

herein) with Lighthouse Life Solutions.

●

Fees,

if applicable, on policies acquired by a third-party purchaser,

which policies were originated by Lighthouse Life

Direct.

We

may, in the future, generate revenues from the following additional

sources related to the acquisition of policies using our own

funds:

●

Proceeds

from the sale of life insurance policies originated and purchased

by our company and subsequently sold to third-party purchasers;

and

●

Death

benefits received from the maturity of life insurance policies

owned by the company.

See “General

Information About Our Company – Business

Strategy”

Our company is managed by its sole member, LHL

Strategies, and its management team, who are also our executive

officers. Each member of our management team has over 18 years of

senior management experience in the business of life settlements.

Michael D. Freedman, our chief executive officer, previously served

as president of GWG Holdings, Inc. and its subsidiary life

settlement provider, GWG Life, LLC, or GWG, during which

time GWG became the second most active company in the industry,

based on the number of policies purchased and the net death benefit

of policies purchased1. Prior to that,

Michael led the life settlement market’s legal and regulatory

development while at Coventry First LLC (“Coventry”).

James J. Dodaro, our chief investment and financial officer, has

over 19 years of industry experience and was previously the chief

underwriting officer for Coventry where he structured and led the

company’s efforts in the purchase, management and resale of

life insurance policies. Andrew M. Brecher, our chief operating

officer, has over 20 years of experience in the life settlement

market, specializing in technology and security, and was previously

the chief information officer at Coventry. Michael L. Coben, our

chief distribution and business development officer, has more than

30 years of expertise in building strategic alliances managing

wholesaling teams in life insurance, annuities and life settlement

distribution. For 13 years he led national sales as SVP, National

Distribution at Coventry. The

company’s founders, together with their senior management

team, have over 100 years of collective experience in life

settlements, life insurance and financial

services.

3

The

following summarizes the relationship of the foregoing

entities:

Our company has no employees. All of our

operations will be performed by employees of LHL Strategies, our

sole member. Currently, LHL Strategies’ only asset is

its 100% membership interest in Lighthouse Life Capital, LLC, a

member-managed limited liability company. We anticipate that

distributions of cash will be made from us to LHL Strategies, in

amounts as determined by LHL Strategies, as our sole member, and

that such amounts will be at least sufficient to pay all expenses

and liabilities of our sole member. As

our sole member , LHL Strategies, through its board of directors,

will control our company. LHL Strategies and its subsidiaries are

subject to certain operating restrictions related to covenants in

the agreements governing outstanding indebtedness of LHL

Strategies, including a requirement that LHL Strategies’

lender consent to any other financing or creation of any liens on

the assets of LHL Strategies or any of its subsidiaries, including

our company. LHL Strategies’ lender has consented to this

offering.

Th total revenue of

LHL Solutions, Inc. for the fiscal year ended September 30, 2019

was $277,275 compared to $0 in the prior year period due to

increased policy origination and policy origination fee income.

Total expenses for the period were $2,079,077 compared to the prior

year period of $852,686.

The Offering. We are offering to

investors the opportunity to purchase up to an aggregate of

$50,000,000, of Beacon Bonds. See “Plan of Distribution - Who

May Invest” for further information. The offering will

terminate on the earliest of: (i) the date we sell the Maximum

Offering Amount; (ii) the second anniversary of the date of

qualification of this offering statement; or (iii) such date upon

which we determine to terminate the offering, in our sole

discretion. Notwithstanding the

previous sentence, we have the right to extend this offering beyond

the second anniversary of the date of qualification for an

additional year.

Our

company will conduct closings in this offering on the first and

third Thursday of each month or the “closing dates,”

and each, a “closing date,” until the offering

termination. Once a subscription has

been submitted and accepted by the company, an investor will not

have the right to request the return of its subscription payment

prior to the next closing date. If subscriptions are received on a

closing date and accepted by the company prior to such closing, any

such subscriptions will be closed on that closing date. If

subscriptions are received on a closing date but not accepted by

the company prior to such closing, any such subscriptions will be

closed on the next closing date. It is expected that settlement

will occur on the same day as each closing date.

On each closing date, offering proceeds for that closing will

be disbursed to us and Bonds will be issued to investors, or the

“Bondholders.” If the company is dissolved or

liquidated after the acceptance of a subscription, the respective

subscription payment will be returned to the subscriber. The

offering is being made on a best-efforts basis through IAA, our

underwriter

and Managing Broker-Dealer.

______________

1 The Deal - Life Settlement League Tables:

2017

4

|

Issuer

|

|

Lighthouse

Life Capital, LLC, a Delaware limited liability

company.

|

|

|

|

|

|

Securities Offered

|

|

Maximum

– $50,000,000, aggregate principal amount of the Bonds, with

sales of Class B Bonds limited to $30,000,000, in the

aggregate.

|

|

|

|

|

|

Maturity Date

|

|

The

Class A Bonds and Class B Bonds will each be offered serially, over

a maximum period of two years (subject to extension) starting from

the date of qualification of the Offering Statement of which this

Offering Circular is a part, with the sole difference between the

series being their respective maturity dates. Each series of Class

A Bonds will mature on the fifth anniversary of the issuance date

of such series and each series of Class B Bonds will mature on the

third anniversary of the issuance date of such series.

Upon maturity, and subject to the terms and conditions described in

this offering circular, the Bonds will be automatically renewed at

the same interest rate and for

the same term, unless redeemed upon maturity at our or your

election. Each

such renewal would constitute a new offering for the purpose of the

registration requirements of the Securities Act and, as such, would

be required to be registered or conducted pursuant to an exemption

from registration. Any such subsequent offering conducted pursuant

to Regulation A would count against the aggregate dollar

limitations in Rule 251(a) of Regulation A. If the

Bonds are not renewed and without the consent of the Bondholders,

we may elect to extend the maturity date of the Bonds for an

additional six months to facilitate the redemption of the Bonds.

See “Description

of Bonds – Maturity and Renewal” for more information.

|

|

|

|

|

|

Interest Rate

|

|

Class A

Bonds – 8.5% per annum computed on the basis of a 360-day

year.

Class B

Bonds – 6.5% per annum computed on the basis of a 360-day

year.

|

|

|

|

|

|

Interest Payments

|

|

Commencing

on the 15th day of the month, or the next business day, if the

15th is a

weekend or a holiday, following the issuance of such Bond and

continuing monthly until its maturity date. Interest will accrue

and be paid on the basis of a 360-day year consisting of twelve

30-day months. Interest on each Bond will accrue and be cumulative

from the end of the most recent interest period for which interest

has been paid on such Bond, or if no interest has paid, from the

date of issuance.

|

|

|

|

|

|

Offering Price

|

|

$1,000

per Bond.

|

|

|

|

|

|

Ranking

|

|

The Bonds are senior unsecured indebtedness of our company.

They rank equally with our other senior unsecured indebtedness and

structurally subordinated to all indebtedness of our

subsidiaries. The Bonds would

rank junior to any of our secured indebtedness; however, we have

covenanted not to incur any secured indebtedness or other

indebtedness that would be senior to the Bonds or to permit our

subsidiaries to incur any indebtedness.

|

|

|

|

|

|

Use of Proceeds

|

|

We estimate that the net proceeds we will receive from this

offering will be approximately $45,000,000 if we sell the Maximum

Offering Amount, after deducting O&O Expenses, selling

commissions and fees payable to our managing broker-dealer and

Selling Group Members.

We plan to use substantially all of the net proceeds from this

offering for working capital, general corporate purposes, including

distribution to our sole member for the payment of its expenses and

liabilities related to the formation of our business and other

expenses related to originating and acquiring life insurance

policies, marketing and advertising life settlements, and paying

interest and principal on the Bonds. A portion of the net proceeds

will be used by our subsidiaries to finance the acquisition of life

insurance policies and we will contribute such proceeds to them to

fulfill these purposes. See “Use of

Proceeds” for additional

information.

|

5

|

Certain Covenants

|

|

We will issue the Bonds under an indenture, or the Indenture,

to be dated as of the initial issuance date of the Bonds between us

and UMB Bank, as the trustee. The Indenture contains covenants that

limit our ability to incur, or permit our subsidiaries to incur,

third party indebtedness that would be senior to the Bonds, whether

secured or unsecured, unless all of the net proceeds of such

indebtedness, are used for the repayment of the Bonds. Further, we

are prohibited from selling any equity interest in any of our

subsidiaries, or causing any of our subsidiaries to issue new

equity to any third party, unless the net proceeds of such sale or

issuance are used for the repayment of the Bonds.

Pursuant to the Indenture, we are also required to maintain a bond

service reserve equal to 3% of the net proceeds raised in this

Offering, or

the Bond Service Reserve, which will be used for payment of

interest on the Bonds. The funds subject to the Bond Service

Reserve will be made available to the company for general busines

purposes, one year following the termination of the

Offering. See “Description

of Company’s Securities Certain Covenants” in this Offering

Circular.

|

|

|

|

|

|

Redemption at the Option of the Bondholder

|

|

Redemptions

made pursuant to the Optional

Redemption of the Bonds for Class A Bonds shall be subject

to a penalty of 8.5% of the total amount due to the Bondholder as

of the date of redemption, if redeemed within 0 – 12 months

of issuance, 8.0% of the total amount due to the Bondholder if

redeemed during months 13 – 24 from issuance, 7.5% of the

total amount due to the bondholder as of the date of redemption if

redeemed during months 25 – 36 from issuance, 7.0% of the

total amount due to the Bondholder as of the date of redemption if

redeemed during months 37 – 48 from issuance and 6.5% of the

total amount due to the Bondholder as of the date of redemption if

redeemed during months 49 – 60 from issuance. Redemptions

made pursuant to the Optional

Redemption of the Bonds for Class B Bonds shall be subject

to a penalty of 8.5% of the total amount due to the Bondholder as

of the date of redemption

Our

obligation to redeem Bonds in any given year pursuant to this

redemption is limited to 10% of the outstanding principal balance

of the Bonds, in the aggregate, on the most recent of January

1st, April

1st, July

1st or

October 1st of the applicable

year while the Offering is open, and January 1st of the applicable

year, following the offering termination. In addition, any Bonds

redeemed as a result of a Bondholder's right upon death, disability

or bankruptcy, will be included in calculating the 10% Limit and

will thus reduce the number of Bonds, in the aggregate, to be

redeemed pursuant to the redemption. Bond redemptions will occur in

the order that notices are received. We are not required to

establish a sinking fund or reserve for the redemption of Bonds and

our ability to redeem Bonds will be subject to the availability of

cash or other financing sources and cannot be

assured.

|

|

Redemption at the Option of the Company

|

|

The

Bonds may be redeemed at our option at no penalty. If the Bonds are

renewed for an additional term, we may redeem the Bonds at any time

during such renewal period. Any redemption will occur at a price

equal to the then outstanding principal amount of the Bonds, plus

any accrued but unpaid interest. For the specific terms of the

Optional Redemption, please see “Description of Bonds

– Optional Redemption” for more

information.

|

|

|

|

|

|

Redemption Upon Death, Disability or Bankruptcy

|

|

Within

60 days of the death, disability or bankruptcy of a Bondholder who

is a natural person, the estate of such Bondholder, or legal

representative of such Bondholder may request that we repurchase,

in whole but not in part and without penalty, the Bonds held by

such Bondholder by delivering to us a written notice requesting

such Bonds be redeemed. Redemptions due to death, disability or

bankruptcy shall count towards the annual 10% Limit on redemptions

described above; provided, however, that any redemptions pursuant

to death, disability or bankruptcy shall not be subject to the 10%

Limit. Any such request shall specify

the particular event giving rise to the right of the holder or

beneficial holder to redeem his or her Bonds. If a Bond is held

jointly by natural persons who are legally married, then such

request may be made by (i) the surviving Bondholder upon the death

of the spouse, or (ii) the disabled Bondholder (or a legal

representative) upon disability of the spouse. In the event a Bond

is held together by two or more natural persons that are not

legally married, neither of these persons shall have the right to

request that the company repurchase such Bond unless each

Bondholder has been affected by such an event.

|

6

|

|

|

Disability shall mean with respect to any Bondholder or beneficial

holder, a determination of disability based upon a physical or

mental condition or impairment arising after the date such

Bondholder or beneficial holder first acquired Bonds. Any such

determination of disability must be made by any of: (1) the Social

Security Administration; (2) the U.S. Office of Personnel

Management; or (3) the Veteran’s Benefits Administration, or

the Applicable Governmental Agency, responsible for reviewing the

disability retirement benefits that the applicable Bondholder or

beneficial holder could be eligible to receive.

Bankruptcy shall mean, with respect to any Bondholder the final

adjudication related to (i) the filing of any petition seeking to

adjudicate the Bondholder bankrupt or insolvent, or seeking for

itself any liquidation, winding up, reorganization, arrangement,

adjustment, protection, relief, or composition of such Bondholder

or such Bondholder’s debts under any law relating to

bankruptcy, insolvency, or reorganization or relief of debtors, or

seeking, consenting to, or acquiescing in the entry of an order for

relief or the appointment of a receiver, trustee, custodian, or

other similar official for such Person or for any substantial part

of its property, or (ii) without the consent or acquiescence of

such Bondholder, the entering of an order for relief or approving a

petition for relief or reorganization or any other petition seeking

any reorganization, arrangement, composition, readjustment,

liquidation, dissolution, or other similar relief under any

bankruptcy, liquidation, dissolution, or other similar statute,

law, or regulation, or, without the consent or acquiescence of such

Bondholder, the entering of an order appointing a trustee,

custodian, receiver, or liquidator of such Bondholder or of all or

any substantial part of the property of such Bondholder which order

shall not be dismissed within ninety (90) days.

|

|

|

|

Subject

to the annual cap on redemptions, upon our receipt of a redemption

request in the event of death, disability or bankruptcy of a

Bondholder, we will designate a date for the redemption of such

Bonds, which date shall not be later than 90 days after we receive

documentation and/or certifications establishing (to the reasonable

satisfaction of the company) the right to be redeemed. On the

designated date, we will redeem such Bonds at a price per Bond that is equal to all accrued and

unpaid interest, to but not including the date on which the Bonds

are redeemed plus the then outstanding principal amount of such

Bond.

|

|

|

|

|

|

Default

|

|

The

indenture governing the Bonds will contain events of default, the

occurrence of which may result in the acceleration of our

obligations under the Bonds in certain circumstances. Events of

default, other than payment defaults, will be subject to our

company's right to cure within a certain number of days of such

event of default. Our company will have the right to cure any

payment default within 60 days before the trustee may declare a

default and exercise the remedies under the indenture. See

“Description of Bonds -

Event of Default” for more information.

|

|

|

|

|

|

Form

|

|

The

Bonds purchased through a participant in the Depository Trust

Company, or DTC, will be evidenced by global bond certificates

deposited with a nominee holder, either DTC or its nominee Cede

& Co. Bonds purchased directly will be registered in book-entry

form only on the books and records of UMB Bank, N.A. in the name of

Phoenix American Financial Services, Inc. (“Phoenix

American”) as record holder of such Bonds for the benefit of

such direct purchasers. See "Description of Bonds -

Book-Entry, Delivery and Form" for more

information.

|

|

|

|

|

|

Denominations

|

|

We will

issue the Bonds only in denominations of $1,000.

|

7

|

Payment of Principal and Interest

|

|

Principal

and interest on the Bonds will be payable in U.S. dollars or other

legal tender, coin or currency of the U.S.

|

|

|

|

|

|

Future Issuances

|

|

We may,

from time to time, without notice to or consent of the Bondholders,

increase the aggregate principal amount of any series of the Bonds

outstanding by issuing additional bonds in the future with the same

terms of such series of Bonds, except for the issue date and

offering price, and such additional bonds shall be consolidated

with the applicable series of Bonds and form a single

series.

|

|

|

|

|

|

Securities Laws Matters:

|

|

The

Bonds being offered are not being registered under the Securities

Act in reliance upon exemptions from the registration requirements

of the Securities Act and such state securities laws and may not be

transferred or resold except as permitted under the Securities Act

and applicable state securities laws pursuant to registration or

exemption therefrom. In addition, the company does not intend to be

registered as an investment company under the Investment Company

Act of 1940, as amended.

|

|

|

|

|

|

Trustee, Registrar and Paying Agent

|

|

We have

designated UMB Bank, N.A. as paying agent and Phoenix American

Financial Services, Inc., a California corporation as co-paying

agent in respect of Bonds registered to it as record holder. UMB

Bank, N.A. will also act as trustee under the indenture and

registrar for the Bonds. As such, UMB Bank, N.A. will make payments

on the Bonds to DTC or to Phoenix American (who will forward such

payments to the applicable Bondholders). The Bonds will be issued

in book-entry form only, evidenced by global certificates, as such,

payments are being made to DTC, its nominee or to Phoenix

American.

|

|

|

|

|

|

Governing Law

|

|

The

indenture and the Bonds will be governed by the laws of the State

of Delaware.

|

|

|

|

|

|

Material Tax Considerations

|

|

You

should consult your tax advisors concerning the U.S. federal income

tax consequences of owning the Bonds in light of your own specific

situation, as well as consequences arising under the laws of any

other taxing jurisdiction.

|

|

|

|

|

|

Risk Factors

|

|

An investment in the Bonds involves certain risks. You should

carefully consider the risks above, as well as the other risks

described under “Risk

Factors” of this offering

circular before making an investment decision. The

risks discussed herein include:

● our ability to

fulfill our obligations to make interest and principal payments

under the Bonds and our ability to satisfy redemption

requests;

● our critical

reliance on the funds raised from this Offering to grow our

business to a size sufficient to generate cash to fulfill our

obligations under the Bonds;

● our

predecessor’s limited operating history and history of

operating losses;

● our ability to

execute our business plan in the emerging market for life

settlements which has low consumer awareness and has suffered from

negative publicity and uncertainty. Accordingly, our prospects may

be adversely affected by lack of growth, increased competition or

other changes in the life settlement market;

● our ability to

engage and retain third-party purchasers of the policies we

originate and acquire in sufficient volumes and attendant revenue

from fees and profit sharing;

● changes in the

economy, financial and credit markets that affect the overall

demand for and ability of third-party purchasers to purchase life

insurance policies we originate and acquire, such as a prolonged

economic recession caused by COVID-19 or other factors, rising

inflation, continued market volatility among others;

● our

reliance on information provided and obtained by third parties

including changes in underwriting factors and methodologies and the

risk that insureds may live longer than anticipated;

● federal,

state statutory and regulatory matters, and FINRA

requirements;

|

8

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING

STATEMENTS

This

offering circular contains certain forward-looking statements that

are subject to various risks and uncertainties. Forward-looking

statements are generally identifiable by use of forward-looking

terminology such as "may," "will," "should," "potential," "intend,"

"expect," "outlook," "seek," "anticipate," "estimate,"

"approximately," "believe," "could," "project," "predict," or other

similar words or expressions. Forward-looking statements are based

on certain assumptions, discuss future expectations, describe

future plans and strategies, contain financial and operating

projections or state other forward-looking information. Our ability

to predict results or the actual effect of future events, actions,

plans or strategies is inherently uncertain. Although we believe

that the expectations reflected in our forward-looking statements

are based on reasonable assumptions, our actual results and

performance could differ materially from those set forth or

anticipated in our forward-looking statements. Factors that could

have a material adverse effect on our forward-looking statements

and upon our business, results of operations, financial condition,

funds derived from operations, cash flows, liquidity and prospects

include, but are not limited to, the factors referenced in this

offering circular, including those set forth below.

When

considering forward-looking statements, you should keep in mind the

risk factors and other cautionary statements in this offering

circular. Readers are cautioned not to place undue reliance on any

of these forward-looking statements, which reflect our views as of

the date of this offering circular. The matters summarized below

and elsewhere in this offering circular could cause our actual

results and performance to differ materially from those set forth

or anticipated in forward-looking statements. Accordingly, we

cannot guarantee future results or performance. Furthermore, except

as required by law, we are under no duty to, and we do not intend

to, update any of our forward-looking statements after the date of

this offering circular, whether as a result of new information,

future events or otherwise.

9

RISK FACTORS

An investment in the Bonds is highly speculative and is suitable

only for persons or entities that are able to evaluate the risks of

the investment. An investment in the Bonds should be made only by

persons or entities able to bear the risk of and to withstand the

total loss of their investment. Prospective investors should

consider the following risks before making a decision to purchase

the Bonds. To the best of our knowledge, we have included all

material risks to investors in this section.

Risks Related to the Bonds and to this Offering

The Bonds are not obligations of our subsidiaries and will be

subordinated to all of the liabilities of the company’s

subsidiaries, if any. Such subordination increases the risk that we

will be unable to meet our obligations on the Bonds.

The

Bonds are obligations of the company exclusively and not of any of

our subsidiaries. The Bonds are also effectively subordinated to

all of the liabilities of the company’s subsidiaries, to the

extent of their assets, since they are separate and distinct legal

entities with no obligation to pay any amounts due under the

company’s indebtedness, including the Bonds, or to make any

funds available to make payments on the Bonds. The company’s

right to receive any assets of any subsidiary in the event of a

bankruptcy or liquidation of the subsidiary, and therefore the

right of the company's creditors, including holders of the Bonds,

to participate in those assets, will be effectively subordinated to

the claims of that subsidiary's creditors, including trade

creditors, in each case to the extent that the company is not

recognized as a creditor of such subsidiary. In addition, even

where the company is recognized as a creditor of a subsidiary, the

company’s rights as a creditor with respect to certain

amounts are subordinated to other indebtedness of that subsidiary,

including secured indebtedness to the extent of the assets securing

such indebtedness.

We may engage in a variety of transactions that may impair our

ability to pay interest and principal on the Bonds.

The indenture governing the Bonds will contain

covenants that will limit us from making any fundamental changes

including any merger, consolidation, winding up or liquidation. We

are also limited from paying dividends or issuing preferred equity

or any other equity with preference over our common stock.

Additionally, we may not enter into or

maintain any transaction or agreement with our affiliates, except

in the ordinary course of business, subject to certain conditions.

However, if we violate this covenant or engage in any of

transaction limited by the covenants pursuant to a waiver to the

indenture, it could have an adverse impact on

Bondholders.

Some significant restructuring transactions that may adversely

affect Bondholders may not constitute a Change of

Control/Repurchase Event under the indenture, in which case we

would not be obligated to offer to repurchase the

Bonds.

Some

restructuring transactions that result in a change in control may

not qualify as a Repurchase Event under the Indenture; therefore,

Bondholders will not have the right to repurchase their Bonds, even

though the company is under new management. These

transactions are limited to those which cause a non-affiliate of

the Company to gain voting control. For example, if our Sole Member

determined to cause the Company to become Manager-Managed by a

third-party, the change in control would not qualify as a

Repurchase Event under the Indenture. Upon the occurrence of

a transaction which results in a change in control of the company,

Bondholders will have no voting rights with respect to such a

transaction. In the event of any such transaction, Bondholders

would not have the right to require us to repurchase their Bonds,

even though such a transaction could increase the amount of our

indebtedness, or otherwise adversely affect the

Bondholders.

The Bonds will limit but do not eliminate our ability to incur

additional debt which could negatively impact

Bondholders.

The Indenture contains covenants that limit our

ability to incur, or to permit our subsidiaries to incur, third

party indebtedness except with respect to the issuance of Bonds in

this offering and with respect to the issuance of indebtedness, the

net proceeds of which is used exclusively to pay off the

Bonds. In the event we are in violation of the covenant,

incur debt pursuant to a waiver of the indenture, or otherwise,

that debt may be senior to Bondholders.

10

We are not limited in the amount of distributions we may make to

our parent and sole member, LHL Strategies, Inc.

Neither

the Indenture nor the forms of Bonds contain any covenant limiting

the ability of LHL Strategies to cause us to make distributions of

cash from us to LHL Strategies in respect of LHL Strategies 100%

membership interest in us. We anticipate that distributions of cash

will be made from us to LHL Strategies, in amounts as determined by

LHL Strategies, as our sole member, and that such amounts will be

at least sufficient to pay all expenses and liabilities of our sole

member, As LHL Strategies will conduct all of our operations

through its personnel, we believe such distributions to be

necessary; however, amounts distributed to LHL Strategies will not

be available to us to make payments of interest or principal or to

fund redemption requests on the Bonds.

Our company objectives critically rely on the amount of funds

raised in this offering.

While

we believe it is possible to achieve our objectives regardless of

the amount of the raise, it will be significantly more difficult to

do so if we sell fewer Bonds than we anticipate. Such a result may

negatively impact our ability to originate and acquire life

insurance policies at projected volumes, which may decrease our

ability to service and repay our debt

when and as it comes due, including honoring redemptions on the

Bonds. Additionally, if we are successful raising capital, we

cannot predict the amounts and timing of such raise. Therefore, we

may have to adjust our business plan and such amendments may be

suboptimal.

If we sell substantially less than all of the Bonds we are

offering, the costs we incur to comply with the rules of the

Securities and Exchange Commission, or the SEC, regarding financial

reporting and other fixed costs (such as those relating to the

offering) will be a larger percentage of our revenue and may reduce

our financial performance and our ability to fulfil our obligations

under the Bonds.

We

expect to incur significant costs in maintaining compliance with

the financial reporting for a Tier II Regulation A issuer and that

our management will spend a significant amount of time assessing

the effectiveness of our internal control over financial reporting.

We do not anticipate that these costs or the amount of time our

management will be required to spend will be significantly less if

we sell substantially less than all of the Bonds we are

offering.

Upon maturity, unless redeemed at our or your election, the bonds

will be automatically renewed at the same interest rate and for the

same term.

Upon maturity, and subject to the terms and

conditions described in this offering circular including

registration or availability of an exemption from registration

under the Securities Act, the Bonds will be automatically renewed

at the same interest rate and for the same term, unless redeemed upon maturity

at our or your election. As a result, if we do not elect to redeem

Bonds at maturity, a Bondholder must affirmatively request

redemption in accordance with the process set forth below under

“Description

of Bonds – Interest and Maturity.” If a Bondholder does not request

redemption as prescribed then such Bondholders will not be repaid

upon maturity and will be automatically renewed for another term,

subject to the Bondholder’s ability to request redemption

subject to limitations and penalties. See

“Description

of Bonds - Optional Redemption at Election of

Bondholder”

for more information.

Redemption requests of Bonds at the option of the Bondholder will

be limited by the 10% Limit and to the extent they are accepted,

will be subject to financial penalties for early

redemption.

While the Bonds

carry an early redemption right and a redemption right in the event

of death, disability or bankruptcy of the Bondholder, redemptions

are subject to an annual 10% redemption limit. As a result,

requests for redemption from Bondholders may be rejected by the

Company. Additionally, with respect to redemptions at the option of

the Bondholders, except for death, disability or bankruptcy, early

redemption penalties of between 6.5% and 8.5% based on when Bonds

are redeemed, for Class A Bonds and 8.5% for Class B Bonds will

apply, which will adversely affect Bondholders seeking to redeem

Bonds prior to maturity.

Redemption requests for Bonds at the option of the Bondholder or in

the event of death, disability or bankruptcy of a Bondholder may

have an adverse effect on the company’s overall growth and

ability to fulfil our obligations on the Bonds.

The

Bonds carry an early redemption right and a redemption right in the

event of death, disability or bankruptcy of the Bondholder. As a

result, one or more Bondholders may elect to have their Bonds

redeemed prior to maturity. In such an event, we may not have

access to the necessary cash to redeem such Bonds. Additionally,

any cash used to satisfy such redemption requests will be diverted

from cash required to fund the continued growth of the company.

Accordingly, the use of funds towards redemptions could result in

the company’s inability to meet projected growth targets,

which could, in turn, limit the company’s ability to make

interest and principal payments to Bondholders.

Our trustee shall be under no obligation to exercise any of the

rights or powers vested in it by the indenture at the request,

order or direction of any of the Bondholders, pursuant to the

provisions of the indenture, unless such Bondholders shall have

offered to the trustee reasonable security or indemnity against the

costs, expenses and liabilities that may be incurred therein or

thereby.

The

indenture governing the Bonds provides that in case an event of

default occurs and not be cured, the trustee will be required, in

the exercise of its power, to use the degree of care of a

reasonable person in the conduct of his own affairs. Subject to

such provisions, the trustee will be under no obligation to

exercise any of its rights or powers under the indenture at the

request of any Bondholder, unless the Bondholder has offered to the

trustee security and indemnity satisfactory to it against any loss,

liability or expense.

11

There is no established trading market for the Bonds and we do not

expect one to develop. Therefore, Bondholders may not be able to

resell them for the price that they paid or sell them at

all.

Prior

to this offering, there was no active market for the Bonds and we

do not expect one to develop. We do not have any present intention

to apply for a quotation for the Bonds on an alternative trading

system or over the counter market and even if we obtain that

quotation in the future, we do not know the extent to which

investor interest will lead to the development and maintenance of a

liquid trading market. Further, the Bonds will not be quoted

on an alternative trading system or over the counter

market until after the termination of this offering, if at

all. Therefore, investors will be required to wait until at least

after the final termination date of this offering for such

quotation. The initial public offering price for the Bonds has been

determined by us. You may not be able to sell the Bonds you

purchase at or above the initial offering price or sell them at

all.

Alternative trading

systems and over the counter markets, as with other public

markets, may from time to time experience significant price

and volume fluctuations. As a result, if the Bonds are listed on

such a trading system, the market price of the Bonds may be

similarly volatile, and Bondholders may from time to time

experience a decrease in the value of their Bonds, including

decreases unrelated to our operating performance or prospects. The

price of the Bonds could be subject to wide fluctuations in

response to a number of factors, including those listed in this

"Risk

Factors" section of this offering circular. No assurance can

be given that the market price of the Bonds will not fluctuate or

decline significantly in the future or that Bondholders will be

able to sell their Bonds when desired on favorable terms, or at

all. Further, the sale of the Bonds may have adverse federal income

tax consequences.

We rely on IAA, our managing broker-dealer, to sell the Bonds

pursuant to this offering. If our managing broker-dealer is not

able to market the Bonds effectively, we may be unable to raise

sufficient proceeds to meet our business objectives.

We have

engaged IAA to act as our underwriter

and managing broker-dealer for this offering. We rely on our

managing broker-dealer to use its best efforts to sell the Bonds

offered hereby. If our

managing broker-dealer is not able to market the Bonds effectively,

it would be challenging and disruptive to locate an alternative

managing broker-dealer for this offering. Without an effective

effort to sell the Bonds, our ability to originate and acquire life

insurance policies may be limited, which could affect our ability

to meet revenue projections, which in turn, could limit the

company’s ability to make interest and principal payments to

Bondholders. See “Our company objectives

critically rely on the amount of funds raised in this

offering.”

We may redeem all or any part of the Bonds that have been issued

before their maturity, and you may be unable to reinvest the

proceeds at either the same or a higher rate of

return.

We may

redeem all or any part of the outstanding Bonds prior to maturity.

See “Description of Bonds -

Optional Redemption” for more information. If

redeemed, you may be unable to reinvest the money you receive in

the redemption at a rate that is equal to or higher than the rate

of return on the Bonds.

Risks Related to Our Business and Our Industry

Our predecessor has a limited history of operations and a history

of operating losses. Consequently, our future earnings and cash

flows, if any, may be volatile, resulting in future losses and

uncertainty about our ability to fulfil our obligations under the

Bonds including honoring redemption requests of the

Bonds.

We

are a company with a limited history, which makes it difficult to

accurately forecast our earnings and cash flows. While we have a

limited operating history, our predecessor, Lighthouse Life

Solutions, LLC had a net loss of approximately $853,563 and $1.8

million, for the fiscal years ended September 30, 2018 and 2019.

Our limited history, our history of operating losses and the

evolving nature of our market make it likely that there are risks

inherent in our business that are yet to be recognized by us or

others, or not fully appreciated, and that could result in us

earning less than we anticipate or suffering further losses. As a

result of the foregoing, an investment in the Bonds necessarily

involves significant uncertainty about the stability of our

earnings and cash flows, if any, and, ultimately, our ability to

service and repay our debt. Accordingly, there is a significant

risk that you could lose your entire investment.

12

Substantially all of our predecessor’s historical revenues

have been generated from one source.

Substantially all our predecessor’s

historical revenue has been derived from certain fees and, if any,

profit sharing, paid to it pursuant to a Letter Agreement (as defined herein)

related to Lighthouse Life Solutions’ acquisition of life

insurance policies for the applicable trust series of Merlion Park Trust (the

“Merlion Trust”). Although the

Merlion Trust has a right of first refusal pursuant to the Letter

Agreement (as defined herein). (“See “General

Information About Our Company – Business

Strategy”), it has no obligation to purchase policies that

we originate and in the event the Merlion Trust chooses to no

longer purchase policies or purchase fewer policies from us, our

revenue would be adversely affected as we cannot guarantee we would

be able to earn sufficient revenues from other third-party

purchasers, which would limit our ability to fulfill our

obligations under the Bonds. However,

we are not aware of any intention on the part of Merlion Trust to

reduce their historical acquisitions of policies through our

company.

We are controlled by our sole member and Bondholders will have no

control over changes in our strategies, policies and day-to-day

operations, which lack of control increases the uncertainty and

risks you face as an investor in the Bonds. In addition, we may

change our strategies and operational policies without your

approval.

You should

not purchase Bonds unless you are willing to entrust all aspects of

the day-to-day management to the board of directors and executive

officers of our sole member, LHL Strategies. As a Bondholder, you

will not have any voting rights under our operating agreement.

Specifically, our sole member is controlled by Michael Freedman,

James Dodaro, Andrew Brecher, and Michael Coben, who together also

comprise the board of directors of our sole member, and as a

result, they will be able to exert significant control over

the operations of our sole member, and in turn, the operations of

the company. The board of directors of our sole member has

exclusive control over the operations of our company. As a result,

we are dependent on the board of directors of our sole member to

properly manage our sole member and in turn, the company.

None of our sole member, our

executive officers or the board of directors of our sole member

have any fiduciary duty to bondholders.

LHL Strategies, our sole member, has entered into agreements

governing outstanding indebtedness which provide certain consent

rights to our sole member’s senior lender which may adversely

affect Bondholders.

LHL

Strategies and its subsidiaries are

subject to certain operating restrictions related to covenants in

the agreements governing outstanding indebtedness of LHL

Strategies, including a requirement that LHL Strategies’

lender consent to any other financing or creation of any liens on

the assets of LHL Strategies or any of its direct or indirect

subsidiaries. This consent right is expected to expire with final

maturity of LHL Strategies’ indebtedness on May 31, 2024;

provided that if the LHL Strategies indebtedness is not fully paid

at maturity or is otherwise extended then such consent right will

remain in effect until such indebtedness is repaid. While LHL

Strategies’ lender has consented to this offering, these

consent rights may limit the ability of our company and its

subsidiaries to procure future financing which may inhibit the

growth of our company or the ability of our company to refinance,

if necessary, the Bonds. Further, in the event LHL Strategies was

in violation of the aforementioned covenants, it could be subject

to litigation with respect to the agreements, which in turn could

adversely affect its and its personnel’s ability to manage

our company.

The inability of our sole member to hire and retain key personnel

could delay or hinder implementation of our business strategies,

which could impair our ability to fulfil our obligations under the

Bonds and could reduce the value of your investment.

Our

success depends to a significant degree upon the contributions of

our sole member’s management team and highly skilled

personnel. While our sole member has employment agreements with its

executive officers, if any of them were to cease their affiliation

with our sole member, it may be unable to find suitable

replacements, and our operating results could suffer. Competition

for highly skilled personnel is intense, our sole member may be

unsuccessful in attracting and retaining such highly skilled

personnel. If our sole member loses or is unable to obtain the

services of highly skilled personnel, the ability of our sole

member to facilitate implementation of our strategies could be

delayed or hindered, and our ability to pay obligations on the

Bonds may be materially and adversely affected.

13

Material changes in the life settlement market, a relatively new

and evolving market, may adversely affect our operating results,

business prospects and our ability to repay our obligations under

the Bonds.

Our sole business is to originate

and acquire life insurance policies through the highly regulated

life settlement market for the benefit of third-party purchasers of

those policies. The life settlement market is a relatively new and

evolving market. The success of our business and our ability to

repay the principal and interest on our obligations, including the

Bonds, depends in large part on the continued development of the

life settlement market, and, in part, the solvency of life

insurance companies to pay the face value of the life insurance

benefits, both of which will critically impact the performance of

the life insurance assets we currently own and acquire in the

future. We expect that the development of the life settlement

market will primarily be impacted by a variety of factors such as

the interpretation of existing laws and regulations, the adoption

or amendment of statutes and regulations, and the addressable

market. Importantly, all of the factors that we believe will

significantly affect the development of the life settlement market

are beyond our control. Any material and adverse development in the

life settlement market, including the life insurance industry,

could adversely affect our operating results, our business

prospects and viability, our access to capital, our ability to

repay our various obligations, including the Bonds. Because of

this, an investment in the Bonds generally involves greater risk as

compared to investments offered by companies with more diversified

business operations in more established

markets.

Our business and prospects may be adversely affected by changes,

lack of growth, increased competition or other changes in the life

settlement market.

The

life settlement market and our operation within the market may be

negatively affected by a variety of factors within and beyond our

control, including:

●

the

inability to receive interest from qualified policyowners in

response to our advertising and marketing about life settlements

and our company’s services;

●

the

inability to receive referral of qualified policyowners from

financial professionals, life settlement brokers and providers,

third-party advertisers and other intermediaries;

●

the

inability to engage with third-party purchasers of the life

insurance policies we originate;

●

competition

from other companies, including other life settlement companies,

life insurance companies (which are larger and more well

capitalized than us), and other financial service product

providers;

●

negative

publicity, misunderstandings and uncertainty about life settlements

and the life settlement market by the public and life insurance

policyowners; and

●

the

adoption or amendment of governmental statutes, regulations or

administrative actions that would negatively impact the life

settlement market.

The

relatively new and evolving nature of the life settlement market in

which we operate makes these risks unique and difficult to

quantify. Nevertheless, contractions in the life settlement market,

whether resulting from general economic conditions, regulatory or

legal pressures or otherwise (including regulatory pressures

exerted on us or others involved in the life settlement market or

involved with participants in that market), could make

participation in that market generally less desirable. This could,

in turn, depress the prices at which life insurance policies are

bought and sold.

Contestability and

Validity of Life Insurance Policies.

Life

insurance policies that we originate and acquire may be subject to

contest by the issuing life insurance company. If the

insurance company successfully contests a policy, the policy will

be rescinded and declared void. Additionally, pursuant to our

origination agreements and pursuant to state insurance laws and the

forms approved for use by state insurance departments, for each of

the policies we acquire, we represent that to our knowledge, there

were no misrepresentation or fraud by any insured, underlying

seller, or person, including insurance agent, broker or producer

with respect to that policy. As such, if a policy acquired by the

company is deemed to be invalid following the acquisition of the

policy by a third-party purchaser, we could be subject to

litigation in connection with such origination.

14

Competition in the Life Settlement Market.

The

life settlement market is highly competitive and there are several

substantial barriers to prevent new competitors from entering this

market. However, we expect to face competition from existing

competitors and new market entrants in the future. As a

result, we may not be able to originate or acquire life settlement

policies for third-party purchasers on a commercially viable

basis.

Risks related to the origination and acquisition of life settlement

policies for the benefit of third-party purchasers; our model

relies on a sufficient number of purchasers for the policies we

originate and acquire.

Our

business model relies on relationships with third-party purchasers

that purchase the policies that our company originates and

acquires. Our business model requires that we continually develop

relationships with third-party purchasers for the life insurance

policies that we originate. While we currently have a sufficient

number of such purchasers, as we grow, so will our need to develop

additional relationships with third-party purchasers. Any lack of

relationships with third-party purchasers will have a materially

adverse effect on our business, which will limit our ability to

continue operating the business and adversely affect our ability to

fulfill our obligations under the Bonds to make interest and

principal payments to Bondholders.

Changes in the economy, financial and credit markets that affect

the overall demand for and ability of investors to finance life

insurance policy purchases such as a prolonged economic recession

caused by COVID-19 and related factors, rising inflation, continued

market volatility and widespread loan defaults among

others.

Life

insurance policies are a financial asset and, as such, are impacted

by macro-economic factors such as the economy, employment, and

interest rates to name a few. The availability of credit is also a

critical condition that impacts all financial assets including life

insurance policies. Additionally, the life settlement market is a

relatively new and niche market that comparatively few investors

and lenders are aware of. Therefore, any adverse changes in the

macro-economic factors that affect the availability of credit

broadly may have a disproportionate impact on the life settlement

market. This could have the effect of depressing demand or reducing

the prices we receive for the life insurance policies we purchase

and hold for resale or to maturity. If such conditions persist, it

could have a material negative impact on our business, prospects

and ability to fulfil the obligations under the bonds.

COVID-19

is a factor that has and could continue to result in the

persistence of negative economic conditions that impact our

business as described above. However, there remains significant

uncertainty about the path of the virus and the pace of future

economic growth in addition to the unknown secondary future impacts

of these actions (national debt). As such, there can be no

assurance that we will be execute our business and funding plans in

the midst of COVID-19 and in the future if it

persists.

Risks related with purchasing and holding life insurance policies

until maturity,

including the risk that insureds live longer than we anticipated,

the requirement to fund on-going premium payments for a substantial

period of time and various operating risks and costs associated

with holding life insurance policies.

While our primary business is to originate and

acquire life insurance policies for the benefit of third-party

purchasers, we may decide to purchase and own a certain number of

policies to maturity. While we estimate a rate of return when we

purchase the life insurance policy, the actual rate of return

cannot be known prior to the mortality of the insured. The

longer the insured lives, the lower the rate of return on the life

insurance policy will be (and vice versa). The rate of return on

any single life insurance policy held to maturity can be

substantially less than zero. Additionally, any estimate of life

expectancy is based upon available medical and actuarial data at

the time of purchase that we generally rely on third parties to

provide us with (see “If

actuarial assumptions we obtain from third-party

providers…”). Life

insurance estimates on any single insured are inherently broad (not

an exact date of mortality but rather a probability of mortality at

any given date in the future) and there can be no assurance of the

accuracy of such third-party estimates. We may also rely on

alternative methods of obtaining life expectancy estimates

including methods created by us or others on our behalf using a

smaller or different data and analysis than that typically used in

the market today. Additionally, it is possible that advanced in

medical treatment and technology will result in insureds living

longer than we anticipated at the time of purchase and such changes

would have a material negative impact on our portfolio and

business. Delays in the collection of the proceeds on a substantial

number of life insurance policies we own, caused by the

aforementioned or any other reason, could have a material adverse

effect on the company’s financial results, which, in turn,

may have a material adverse effect on the company’s ability