Post-Qualification Offering Statement Amendment No. 4

File No.

As filed with the Securities and Exchange Commission on August 8, 2023

PART II – INFORMATION REQUIRED IN OFFERING CIRCULAR

Offering Circular

August 8, 2023

PHOENIX CAPITAL GROUP HOLDINGS, LLC

4643 South Ulster Street, Suite 1510

Denver, CO 80237

18575 Jamboree Road, Suite 830

Irvine, CA 92612

152 North Durbin Street, Suite 220

Casper, WY

(303) 749-0074

9.0% Bonds (Bonds)

Up to $20,076,000 in Bonds ( 20,076 Bonds)

$5,000 Minimum Purchase Amount (5 Bonds)

This is a post-qualification amendment (the “PQA”) to the offering statement on Form 1-A qualified by the U.S. Securities and Exchange Commission (“SEC”) on December 23, 2021, as previously amended. The purpose of this PQA is to update the maximum offering amount of the offering and the financial statements of the Company, and to provide updated information related to, among other things the broker/dealer of record, use of proceeds and management of the Company.

Phoenix Capital Group Holdings, LLC, a Delaware limited liability company (the “Company” or “Phoenix”), is offering a maximum of $20,076,000 in the aggregate, of its 9.0% unsecured bonds, or the “Bonds,” pursuant to this offering circular.

The Company is continuing to offer up to $20,076,000 (“Maximum Offering Amount”) of our Bonds, which represents the value of the Bonds available to be offered as of August 2, 2023 out of the rolling 12-month maximum offering amount of $75,000,000 million in securities we are permitted to issue pursuant to Regulation A. The Company’s offering statement of which this offering circular is a part was qualified on December 23, 2021. From the date of qualification until August 1, 2022, we sold $20,076,000 in gross proceeds of Bonds, and, as of May 25, 2023, the Company had sold $74,987,000 of Bonds in total. Other than the Bonds, we have not sold securities under Regulation A in the last 12 months. If we sell the entirety of the amount left to be sold under this offering circular, we will have sold an aggregate of $94,973,000 of our Bonds pursuant to this Offering,

The purchase price per Bond is $1,000, with a minimum purchase amount of $5,000, or the “minimum purchase”; however, the Company, in our sole discretion, reserves the right to accept smaller purchase amounts. The Bonds will bear interest at nine percent (9.0%) per year. The company reserves the right to qualify additional Bonds for sale in compliance with the $75,000,000 annual limit under Rule 251 of Regulation A. The Bonds are being offered serially, over a maximum period of 3 years, starting on December 23, 2021, with the sole difference between the series being their respective maturity dates. Each series of Bonds beginning with Series A will correspond to a particular closing. Each series of Bonds will mature on the third anniversary of the initial issuance date of such series. The Company may elect to extend the maturity date of the Bonds for up to two additional one-year periods in the Company’s sole discretion. If the Company elects to extend the maturity date of the Bonds, the Bonds will bear interest at 10.0% per annum during the first one-year extension period and will bear interest at 11.0% per annum during the second one-year extension period. Interest on the Bonds will be paid in equal monthly installments to the record holders of the Bonds on the 10th day of each month, or if any day is not a business day, the next business day, thereafter until the Bonds have been repaid in full or are otherwise no longer outstanding.

Bondholders will have the right to have their Bonds redeemed at any time prior to the maturity date, subject to an annual cap of 10% on all redemptions, regardless of the reason for the redemption, at a price equal to $950 plus all accrued but unpaid interest per Bond, regardless of when such Bonds are redeemed (the “10% Limit”). Bondholders will also have the right to have their Bonds redeemed in the case of a bondholder’s death, disability or bankruptcy, subject to notice, discounts and other provisions contained in this offering circular. Redemptions due to death, disability or bankruptcy shall count towards the annual 10% Limit on redemptions described above. See “Description of Bonds – Redemption Upon Death, Disability or Bankruptcy” and “Description of Bonds – Bond Redemptions” for more information.

NTD

As of March 15, 2023, or the “Effective Date,” the Bonds have been offered to prospective investors on a commercially reasonable efforts basis by Dalmore Group, LLC (our “Managing Broker-Dealer”) a New York limited liability company and a member of the Financial Industry Regulatory Authority, or “FINRA,” which includes a maximum broker-dealer fee of up to 4.5% of the gross proceeds of the offering. The Bonds are offered to prospective investors on a commercially reasonable efforts basis by Dalmore Group. “Commercially reasonable efforts” means that our broker/dealer of record is not obligated to purchase any specific number or dollar amount of Bonds but will use commercially reasonable efforts to sell the Bonds. At each closing date, the net proceeds for such closing will be disbursed to our Company and Bonds relating to such net proceeds will be issued to their respective investors. Certain of our personnel, including Mr. Willer, our Managing Director, Capital Markets, are licensed registered representatives of Dalmore and will be paid a portion of the Broker-Dealer Fee (as defined herein) as sales compensation with respect to the sales of our Bonds. Mr. Willer will be paid up to 2.0% of the gross proceeds of the offering out of the Broker-Dealer Fee. We commenced the sale of the Bonds on December 23, 2021, or the “Commencement Date” and will terminate the offering on the earliest of: (i) the date we sell the Maximum Offering Amount; (ii) December 23, 2024; or (iii) such date upon which we determine to terminate the offering, in our sole discretion.

|

|

| Price to Investors |

|

| Broker-Dealer Fee (1)(2) |

|

| Proceeds to Company |

|

| Proceeds to Other Persons |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

| Per Bond (1)(2) |

| $ | 1,000 |

|

| $ | 45 |

|

| $ | 955 |

|

| $ | 0 |

|

| Offering Amount Based on Bonds Remaining to be Sold (1)(2) |

| $ | 20,076,000 |

|

| $ | 903,420 |

|

| $ | 19,172,580 |

|

| $ | 0 |

|

| (1) | This includes a maximum broker-dealer fee of up to 4.5% of the gross proceeds of the offering (the “Broker-Dealer Fee”). The Broker-Dealer Fee will be paid to Dalmore Group as our broker/dealer of record. Dalmore Group will pay a portion of the Broker-Dealer Fee to its associated persons, including certain of our personnel , including Mr. Willer, who are licensed registered representatives of Dalmore Group. See “Use of Proceeds” and “Plan of Distribution” for more information. |

| (2) | All figures are rounded to the nearest dollar. |

Generally, no sale may be made to you in the offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

An investment in the Bonds is subject to certain risks and should be made only by persons or entities able to bear the risk of and to withstand the total loss of their investment. Currently, there is no market for the Bonds being offered, nor does our Company anticipate one developing. Prospective investors should carefully consider and review that risk as well as the RISK FACTORS beginning on page 10 of this offering circular.

THE SEC DOES NOT PASS UPON THE MERITS OR GIVE ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SELLING LITERATURE. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE SEC; HOWEVER, THE COMMISION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION.

FORM 1-A DISCLOSURE FORMAT IS BEING FOLLOWED.

| 4 | |

|

|

|

| 5 | |

|

|

|

| 9 | |

|

|

|

| 10 | |

|

|

|

| 18 | |

|

|

|

| 19 | |

|

|

|

| MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 25 |

|

|

|

| 27 | |

|

|

|

| 34 | |

|

|

|

| 37 | |

|

|

|

| 39 | |

|

|

|

| 45 | |

|

|

|

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 46 |

|

|

|

| 47 | |

|

|

|

| 49 | |

|

|

|

| 50 | |

|

|

|

| 51 | |

|

|

|

| 52 | |

|

|

|

| 53 |

| 3 |

| Table of Contents |

The information in this offering circular may not contain all of the information that is important to you. You should read this entire offering circular and the exhibits carefully before deciding whether to invest in the Bonds. See “Where You Can Find Additional Information” in this offering circular.

Unless the context otherwise indicates, references in this offering circular to the terms “Company,” “we,” “us,” and “our,” refer to Phoenix Capital Group Holdings, LLC, a Delaware limited liability company.

[Remainder of page intentionally left blank]

| 4 |

| Table of Contents |

This summary highlights information contained elsewhere in this offering circular. This summary does not contain all of the information that you should consider before deciding whether to invest in the Bonds. You should carefully read this entire offering circular, including the information under the heading “Risk Factors” and all information included in this offering circular.

Our Company, Phoenix Capital Group Holdings, LLC, a Delaware limited liability company, was formed on April 23, 2019 to purchase (i) property rights to extract natural resources from the property (“mineral rights”), and (ii) ownership interests in property without operating rights on the property (“non-operated working interests”) in the United States, primarily in the Williston Basin, Permian Basin, Powder River, and Denver Julesburg Basin (“DJ Basin”), using the Company’s proprietary software system to identify unique opportunities. Although the Company has targeted specific regions, we are agnostic to geography and look to focus exclusively on the best asset for profitability when determining which assets to buy. The more area the Company can cover, the more we can ensure we are achieving the optimal return for invested capital.

The Company focuses on assets that present high near-term predictable cashflow. This analysis includes the geography of the asset, the probability of future oil wells and predictability of both the timing and value of the cashflow. Following its acquisition of the asset, the Company partners with an oil and gas extraction operator to share in the proceeds of the natural resources extracted and sold by the operator. Using the proprietary software that the Company has developed internally, the Company is typically able to achieve an average payback period of 9-30 months on assets it buys. Additionally, the Company employs a tax-efficient strategy of offsetting royalty income through use of intangible drilling costs (non-operated working interests).

We have also developed a highly customized and proprietary software platform to help us identify opportunities. This aggregate, niche, scalable software platform is specific to us and there is no known competitive product. As such, the software creates considerable intrinsic value to operational efficiencies.

While the Company anticipates that extraction activities at its assets will continue to be primarily performed by third parties for the foreseeable future, the Company has formed Phoenix Operating, LLC (“ PhoenixOp”), a wholly-owned subsidiary, to drill and operate producing wells on oil and gas properties contributed to it by the Company. PhoenixOp has its own employees. The Company is and will remain the sole voting member and manager of PhoenixOp. The Company has agreed to grant certain minority, non-voting interests to PhoenixOp’s employees. The Company intends to make capital contributions to PhoenixOp to finance the operations of PhoenixOp, which may include financing out of the proceeds of the Loan, until such time as PhoenixOp receives its own financing or has sufficient revenues to operate without financing from the Company. The Company will also contribute oil and gas properties (but not those subject to our subordinate mortgage interests) to PhoenixOp from time to time as capital contributions. It is anticipated these contributed properties will be the drilling projects undertaken by PhoenixOp. PhoenixOp expects to begin operations in September 2023, subject to the availability of financing; however, we do not expect PhoenixOp to conduct extraction operations on a material amount of the Company’s oil and gas properties until 2024 at the earliest.

See “General Information About The Company – The Company's Business Strategy”

The Offering. We are offering to investors the opportunity to purchase up to an aggregate of $20,076,000 of Bonds. See “Plan of Distribution - Who May Invest” for further information. The offering will terminate on the earliest of: (i) the date we sell the Maximum Offering Amount; (ii) December 23, 2024; or (iii) such date upon which we determine to terminate the offering, in our sole discretion.

Our Company will conduct closings in this offering on at least at a weekly basis assuming there are funds to close until the offering termination. Once a subscription has been submitted and accepted by the Company, an investor will not have the right to request the return of its subscription payment prior to the next closing date. If subscriptions are received on a closing date and accepted by the Company prior to such closing, any such subscriptions will be closed on that closing date. If subscriptions are received on a closing date but not accepted by the Company prior to such closing, any such subscriptions will be closed on the next closing date. It is expected that settlement will occur on the same day as each closing date. On each closing date, offering proceeds for that closing will be disbursed to us and Bonds will be issued to investors, or the “Bondholders.” If the Company is dissolved or liquidated after the acceptance of a subscription, the respective subscription payment will be returned to the subscriber.

| 5 |

| Table of Contents |

| Issuer |

| Phoenix Capital Group Holdings, LLC, a Delaware limited liability company. |

|

|

|

|

| Securities Offered |

| Maximum – $20,076,000, aggregate principal amount of the Bonds. |

|

|

|

|

| Maturity Date |

| The Bonds are being offered serially, over a maximum period of 3 years starting from December 23, 2021, with the sole difference between the series being their respective maturity dates. The Bonds will mature on the third anniversary of the initial issuance date of each series.

The Company may elect to extend the maturity date of the Bonds for up to two additional one-year periods in the Company’s sole discretion. Each such extension would constitute a new offering for the purpose of the registration requirements of the Securities Act and, as such, would be required to be registered or conducted pursuant to an exemption from registration. Any such subsequent offering conducted pursuant to Regulation A would count against the aggregate dollar limitations in Rule 251(a) of Regulation A. See “Description of Bonds – Interest and Maturity” for more information. |

|

|

|

|

| Interest Rate |

| 9.0% per annum computed on the basis of a 360-day year.

If we elect to extend the maturity date of the Bonds, the Bonds will bear interest at 10.0% per annum in the first one-year extension period and 11.0% per year in the second one-year extension period. |

|

|

|

|

| Interest Payments |

| Interest payments will be paid in equal monthly installments to the record holders of the Bonds on the 10th day of each month, or if any day is not a business day, the next business day, thereafter until the Bonds have been repaid in full or are otherwise no longer outstanding. Interest will accrue and be paid on the basis of a 360-day year consisting of twelve 30-day months. |

|

|

|

|

| Offering Price |

| $1,000 per Bond. |

|

|

|

|

| Ranking |

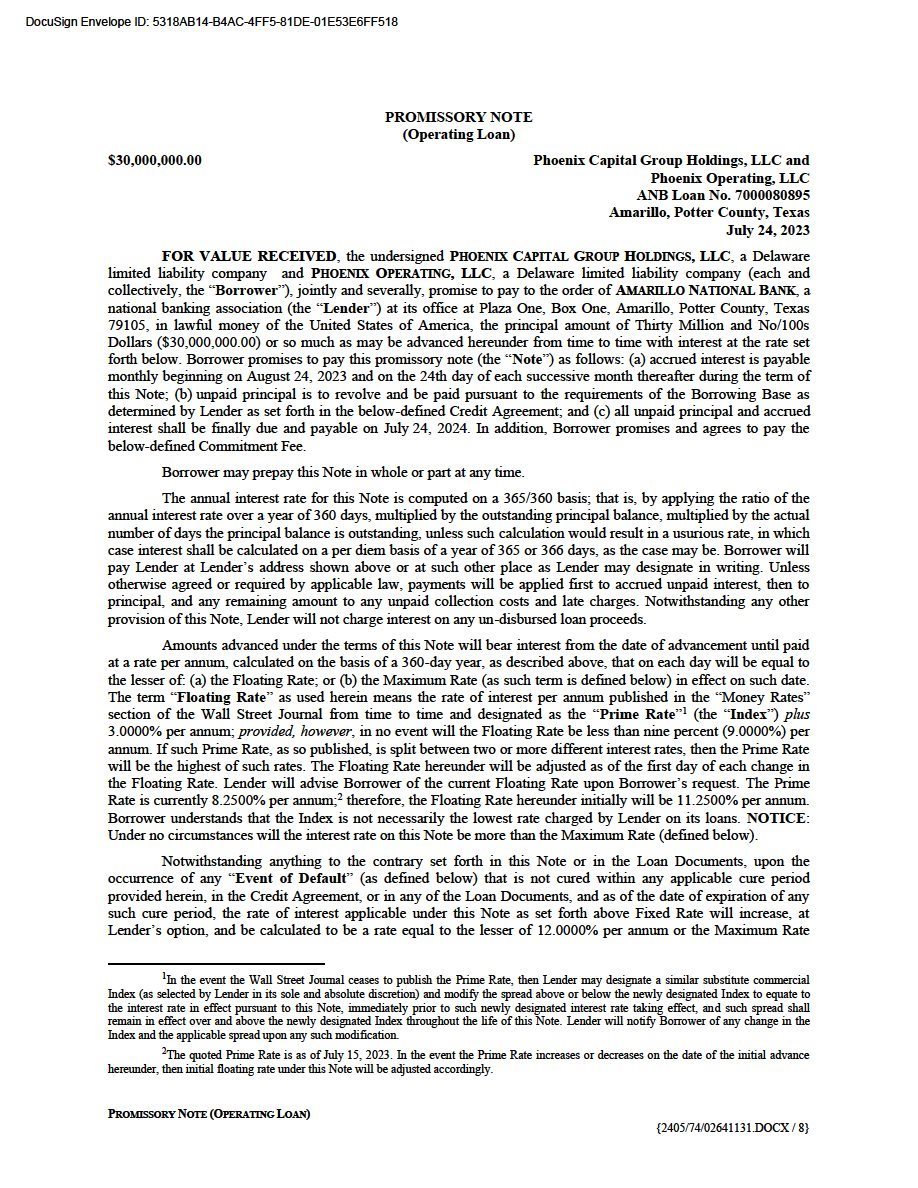

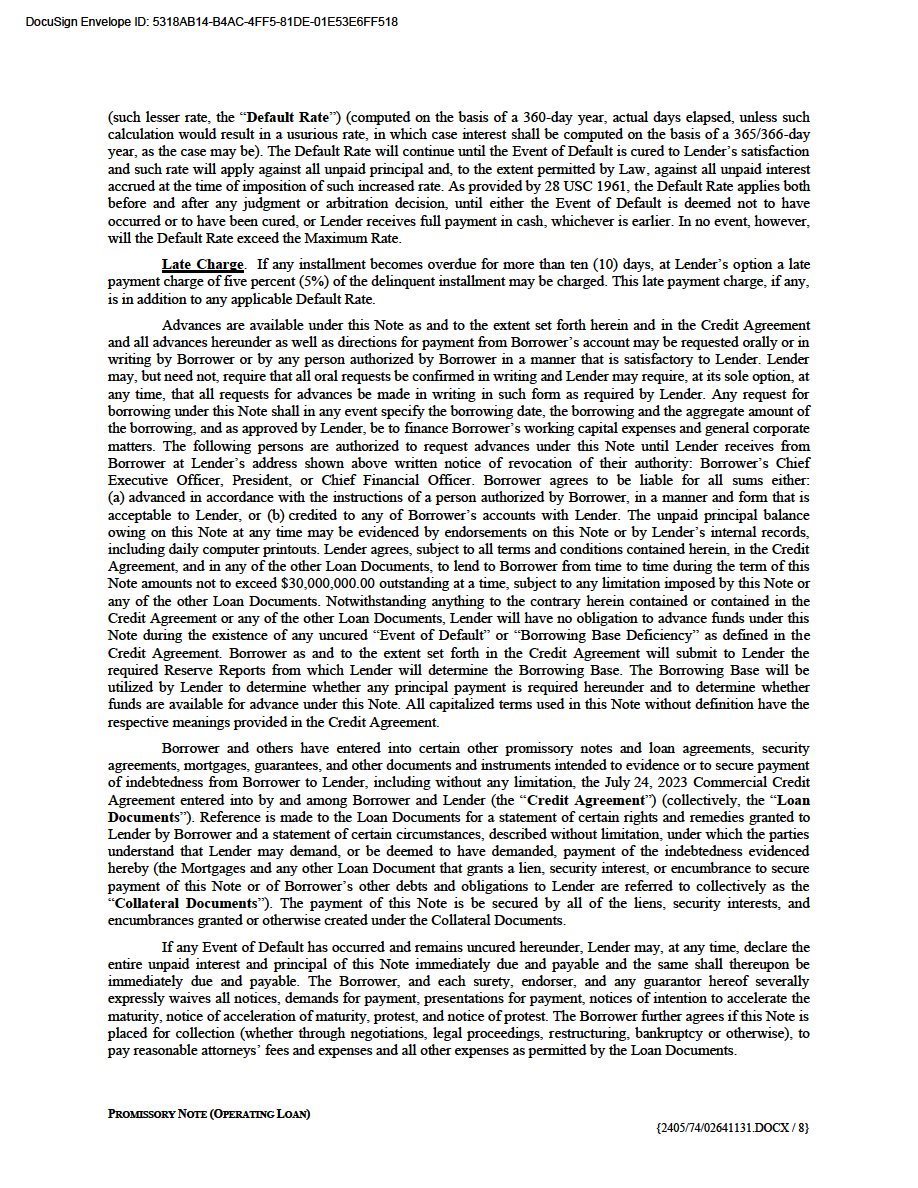

| The Bonds are subordinated, unsecured indebtedness of our Company. They rank pari passu with certain of our other unsecured indebtedness, including: (i) unsecured notes offered and sold pursuant to an offering under Rule 506(b) of Regulation D that commenced in July 2020 and was terminated in September 2020 with maturity dates ranging from one to four years and interest rates ranging from 6.5% to 15% (the “506(b) Notes”); (ii) unsecured notes offered and sold pursuant to an offering under Rule 506(c) of Regulation D that commenced on October 22, 2020 and terminated in December 2021 with maturity dates ranging from one year to four years and annual interest from 6.5% to 15% (the “506(c) Notes”); (iii) unsecured bonds offered and sold pursuant to an offering under Rule 506(c) of Regulation D that commenced in July 2022 and terminated in December of 2022 with five year maturity and annual interest of 11% (the “11% Bonds”) and (iv) unsecured bonds offered and sold pursuant to Rule 506(c) that commenced on July 22, 2022 and terminated in December of 2022 with a nine month maturity and interest rates of 8% or 9% (together, the “Short Term Bonds,” and, collectively with the Rule 506(b) Notes, the 506(c) Notes, the 11% Bonds and the Bonds, the “Pari Passu Obligations”). The Bonds rank senior to the Series AAA through Series D-1 Bonds offered pursuant to an offering under Rule 506(c) of Regulation D that commenced in December 2022 with maturity dates from nine months to seven years with interest rates from 8% to 12% (the “Subordinated Reg D Bonds,” and together with the Bonds and the Pari Passu Obligations, the “Unsecured Debt Obligations”). The Bonds are structurally subordinated to all indebtedness of our subsidiaries. The Bonds rank junior to any of our current or future secured indebtedness. Our current secured indebtedness is that certain revolving credit loan from Amarillo National Bank (“ANB”) in the maximum and current principal amount of $30,000,000 (the “ANB Loan”) pursuant to that certain Commercial Credit Agreement dated as of July 24, 2023 (the “Credit Agreement”) by and among ANB, the Company and its subsidiary, PhoenixOP, as borrower, which is secured by a senior security interest in all of our assets. For the alleviation of doubt, any future secured lenders will rank senior to the Bonds with respect to their collateral interests. We also intend to enter into the PCGHI Loan (as defined herein) which will be secured by junior mortgages (to the ANB Loan or other senior secured debt) on certain properties of the Company and will be senior to the Bonds with respect to PCGHI’s collateral interest in such properties. Collectively, as of July 31, 2023, there were: (i) $34,145,860 of Pari Passu Obligations outstanding, with maturities ranging from August 31, 2023 to December 31, 2027; (ii) $162,292,653 of Subordinated Reg D Bonds outstanding, with maturities ranging from September 30, 2023 to August 31, 2030; (iii) $65,880,681 of Bonds outstanding, with maturities ranging from January 31, 2025 to May 31, 2026 and (iv) $30,000,000 outstanding under the ANB Loan. See “General Information About Our Company – Current Indebtedness” for more information. |

|

|

|

|

| Use of Proceeds |

| We estimate that the net proceeds we will receive from this offering will be approximately $19,172,580, after deducting the Broker-Dealer Fee.

We plan to use substantially all of the net proceeds from this offering for the purchase mineral rights and non-operated working interests, as well as additional asset acquisitions. See “Use of Proceeds” for additional information. |

| 6 |

| Table of Contents |

| Redemption at the Option of the Bondholder |

| Bondholders will have the right to have their Bonds redeemed at any time prior to the maturity date, subject to an annual cap referenced below, regardless of the reason for the redemption, at a price equal to $950 plus all accrued but unpaid interest per Bond, regardless of when such Bonds are redeemed.

Our obligation to redeem Bonds in any given year pursuant to this redemption is limited to 10% of the outstanding principal balance of the Bonds, in the aggregate, on the most recent of January 1st, April 1st, July 1st or October 1st of the applicable year while the Offering is open, and January 1st of the applicable year, following the offering termination. In addition, any Bonds redeemed as a result of a Bondholder's right upon death, disability or bankruptcy, will be included in calculating the 10% Limit and will thus reduce the number of Bonds, in the aggregate, to be redeemed pursuant to the redemption. Bond redemptions will occur in the order that notices are received. We are not required to establish a sinking fund or reserve for the redemption of Bonds and our ability to redeem Bonds will be subject to the availability of cash or other financing sources and cannot be assured. |

|

|

|

|

| Redemption at the Option of the Company |

| The Bonds may be redeemed at our option at no penalty. If the Bonds are renewed for an additional term, we may redeem the Bonds at any time during such renewal period. Any redemption will occur at a price equal to the then outstanding principal amount of the Bonds, plus any accrued but unpaid interest. For the specific terms of the Optional Redemption, please see “Description of Bonds – Optional Redemption” for more information. |

|

|

|

|

| Redemption Upon Death, Disability or Bankruptcy |

| Within 90 days of the death, disability or bankruptcy of a Bondholder who is a natural person, the estate of such Bondholder, or legal representative of such Bondholder may request that we repurchase, in whole but not in part and without penalty, the Bonds held by such Bondholder by delivering to us a written notice requesting such Bonds be redeemed. Redemptions due to death, disability or bankruptcy shall count towards the annual 10% Limit on redemptions described above; provided, however, that any redemptions pursuant to death, disability or bankruptcy shall not be subject to the 10% Limit. Any such request shall specify the particular event giving rise to the right of the holder or beneficial holder to redeem his or her Bonds. If a Bond is held jointly by natural persons who are legally married, then such request may be made by (i) the surviving Bondholder upon the death of the spouse, or (ii) the disabled Bondholder (or a legal representative) upon disability of the spouse. In the event a Bond is held together by two or more natural persons that are not legally married, neither of these persons shall have the right to request that the Company repurchase such Bond unless each Bondholder has been affected by such an event.

Disability shall mean with respect to any Bondholder or beneficial holder, a determination of disability based upon a physical or mental condition or impairment arising after the date such Bondholder or beneficial holder first acquired Bonds. Any such determination of disability must be made by any of: (1) the Social Security Administration; (2) the U.S. Office of Personnel Management; or (3) the Veteran’s Benefits Administration, or the Applicable Governmental Agency, responsible for reviewing the disability retirement benefits that the applicable Bondholder or beneficial holder could be eligible to receive.

Bankruptcy shall mean, with respect to any Bondholder the final adjudication related to (i) the filing of any petition seeking to adjudicate the Bondholder bankrupt or insolvent, or seeking for itself any liquidation, winding up, reorganization, arrangement, adjustment, protection, relief, or composition of such Bondholder or such Bondholder’s debts under any law relating to bankruptcy, insolvency, or reorganization or relief of debtors, or seeking, consenting to, or acquiescing in the entry of an order for relief or the appointment of a receiver, trustee, custodian, or other similar official for such Person or for any substantial part of its property, or (ii) without the consent or acquiescence of such Bondholder, the entering of an order for relief or approving a petition for relief or reorganization or any other petition seeking any reorganization, arrangement, composition, readjustment, liquidation, dissolution, or other similar relief under any bankruptcy, liquidation, dissolution, or other similar statute, law, or regulation, or, without the consent or acquiescence of such Bondholder, the entering of an order appointing a trustee, custodian, receiver, or liquidator of such Bondholder or of all or any substantial part of the property of such Bondholder which order shall not be dismissed within ninety (90) days.

Subject to the annual cap on redemptions, upon our receipt of a redemption request in the event of death, disability or bankruptcy of a Bondholder, we will designate a date for the redemption of such Bonds, which date shall not be later than 90 days after we receive documentation and/or certifications establishing (to the reasonable satisfaction of the Company) the right to be redeemed. On the designated date, we will redeem such Bonds at a price per Bond that is equal to all accrued and unpaid interest, to but not including the date on which the Bonds are redeemed plus the then outstanding principal amount of such Bond. |

| 7 |

| Table of Contents |

| Default |

| The Indenture governing the Bonds will contain events of default, the occurrence of which may result in the acceleration of our obligations under the Bonds in certain circumstances. Events of default, other than payment defaults, will be subject to our Company's right to cure within a certain number of days of such event of default. Our Company will have the right to cure any payment default within 60 days before the trustee may declare a default and exercise the remedies under the Indenture. See “Description of Bonds - Event of Default” for more information. |

|

|

|

|

| Form |

| Bonds will be registered in book-entry form on the books and records of the Company. See "Description of Bonds - Book-Entry, Delivery and Form" for more information. |

|

|

|

|

| Denominations |

| We will issue the Bonds only in denominations of $1,000. |

|

|

|

|

| Payment of Principal and Interest |

| Principal and interest on the Bonds will be payable in U.S. dollars or other legal tender, coin or currency of the U.S. |

|

|

|

|

| Future Issuances |

| We may, from time to time, without notice to or consent of the Bondholders, increase the aggregate principal amount of any series of the Bonds outstanding by issuing additional bonds in the future with the same terms of such series of Bonds, except for the issue date and offering price, and such additional bonds shall be consolidated with the applicable series of Bonds and form a single series. |

|

|

|

|

| Securities Laws Matters: |

| The Bonds being offered are not being registered under the Securities Act in reliance upon exemptions from the registration requirements of the Securities Act and such state securities laws and may not be transferred or resold except as permitted under the Securities Act and applicable state securities laws pursuant to registration or exemption therefrom. In addition, the Company does not intend to be registered as an investment company under the Investment Company Act of 1940, as amended. |

|

|

|

|

| Trustee, Registrar and Paying Agent

|

| We previously designated UMB Bank, N.A. as paying agent and Phoenix American Financial Services, Inc., a California corporation as co-paying agent in respect of Bonds registered to it as record holder. Effective July 18, 2022, the Company is the registrar and designated paying agent with respect to the Bonds, and as such, will make payments on the Bonds. UMB Bank, N.A. acts as trustee under the Indenture. The Bonds will be issued in book-entry form only, evidenced by global certificates. |

|

|

|

|

| Governing Law |

| The Indenture and the Bonds will be governed by the laws of the State of Delaware. |

|

|

|

|

| Material Tax Considerations |

| You should consult your tax advisors concerning the U.S. federal income tax consequences of owning the Bonds in light of your own specific situation, as well as consequences arising under the laws of any other taxing jurisdiction. |

|

|

|

|

| Risk Factors |

| An investment in the Bonds involves certain risks. You should carefully consider the risks above, as well as the other risks described under “Risk Factors” of this offering circular before making an investment decision. |

[Remainder of page intentionally left blank]

| 8 |

| Table of Contents |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This offering circular contains certain forward-looking statements that are subject to various risks and uncertainties. Forward-looking statements are generally identifiable by use of forward-looking terminology such as "may," "will," "should," "potential," "intend," "expect," "outlook," "seek," "anticipate," "estimate," "approximately," "believe," "could," "project," "predict," or other similar words or expressions. Forward-looking statements are based on certain assumptions, discuss future expectations, describe future plans and strategies, contain financial and operating projections or state other forward-looking information. Our ability to predict results or the actual effect of future events, actions, plans or strategies is inherently uncertain. Although we believe that the expectations reflected in our forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth or anticipated in our forward-looking statements. Factors that could have a material adverse effect on our forward-looking statements and upon our business, results of operations, financial condition, funds derived from operations, cash flows, liquidity and prospects include, but are not limited to, the factors referenced in this offering circular, including those set forth below.

When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this offering circular. Readers are cautioned not to place undue reliance on any of these forward-looking statements, which reflect our views as of the date of this offering circular. The matters summarized below and elsewhere in this offering circular could cause our actual results and performance to differ materially from those set forth or anticipated in forward-looking statements. Accordingly, we cannot guarantee future results or performance. Furthermore, except as required by law, we are under no duty to, and we do not intend to, update any of our forward-looking statements after the date of this offering circular, whether as a result of new information, future events or otherwise.

[Remainder of page intentionally left blank]

| 9 |

| Table of Contents |

An investment in the Bonds is highly speculative and is suitable only for persons or entities that are able to evaluate the risks of the investment. An investment in the Bonds should be made only by persons or entities able to bear the risk of and to withstand the total loss of their investment. Prospective investors should consider the following risks before making a decision to purchase the Bonds. To the best of our knowledge, we have included all material risks to investors in this section.

Risks Related to the Bonds and to this Offering

The Bonds are not obligations of our subsidiaries and will be subordinated to all of the liabilities of the Company’s subsidiaries, if any. Such subordination increases the risk that we will be unable to meet our obligations on the Bonds.

The Bonds are obligations of the Company exclusively and not of any of our subsidiaries. The Bonds are also effectively subordinated to all of the liabilities of the Company’s subsidiaries, to the extent of their assets, since they are separate and distinct legal entities with no obligation to pay any amounts due under the Company’s indebtedness, including the Bonds, or to make any funds available to make payments on the Bonds. The Company’s right to receive any assets of any subsidiary in the event of a bankruptcy or liquidation of the subsidiary, and therefore the right of the Company's creditors, including holders of the Bonds, to participate in those assets, will be effectively subordinated to the claims of that subsidiary's creditors, including trade creditors, in each case to the extent that the Company is not recognized as a creditor of such subsidiary. In addition, even where the Company is recognized as a creditor of a subsidiary, the Company’s rights as a creditor with respect to certain amounts are subordinated to other indebtedness of that subsidiary, including secured indebtedness to the extent of the assets securing such indebtedness.

The Bonds are subordinate to our current and future secured indebtedness including the ANB Loan and the PCGHI Loan with respect to the collateral pledged to ANB under the Credit Agreement and to PCGHI under the Credit Loan Agreement.

The Bonds will be subordinate to any debt outstanding under the Company’s ANB Loan with respect to the collateral pledged under the Credit Agreement which is all of the company's assets. The Bonds will also be subordinate to any debt outstanding under the PCGHI Loan with respect to the junior mortgage collateral securing the PCGHI Loan. The Bonds will be subordinate to the collateral interest of any future secured indebtedness of the Company.

In the event of the Company’s bankruptcy, liquidation, reorganization or other winding up, ANB and PCGHI, as the lenders under the various credit agreements will be in senior position with respect to the collateral securing their loans. If the Company defaults under the Credit Agreement or other ANB Loan documents on the one hand or the Credit Loan Agreement or other PCGHI Loan documents on the other, either of ANB or PCGHI could foreclose on its security interest in our assets pledged as collateral, which may result in our inability to pay interest or principal on the Bonds and exist as a going concern. The Bonds will be subordinate to any future secured indebtedness of the Company with respect to the assets securing such indebtedness. In the event of default, there may not be sufficient assets remaining to pay amounts due on any or all of the Bonds then outstanding.

| 10 |

| Table of Contents |

We may engage in a variety of transactions that may impair our ability to pay interest and principal on the Bonds.

The Indenture governing the Bonds will contain covenants that will limit us from making any fundamental changes including any merger, consolidation, winding up or liquidation. However, if we violate this covenant or engage in any transaction limited by the covenants pursuant to a waiver to the Indenture, it could have an adverse impact on Bondholders. In addition, other than the limited covenants contained in the Indenture discussed in this offering circular, we are not subject to additional restrictions on our activities. We may engage in activities, such as issuing additional debt that may rank senior or pari passu with the Bonds, that may hinder our ability to pay our bond service obligations.

The Trustee may exercise its rights under the Indenture in the event of default subject to the rights of the Company's secured lenders .

Trustee may pursue its rights under the Indenture in the event of default; however, the Company’s secured lenders, including ANB and PCGHI, have senior positions with respect to the collateral securing their respective loans.

Some significant restructuring transactions that may adversely affect Bondholders may not constitute a Change of Control/Repurchase Event under the Indenture, in which case we would not be obligated to offer to repurchase the Bonds.

Some restructuring transactions that result in a change in control may not qualify as a Repurchase Event under the Indenture; therefore, Bondholders will not have the right to repurchase their Bonds, even though the Company is under new management. These transactions are limited to those which cause a non-affiliate of the Company to gain voting control. Upon the occurrence of a transaction which results in a change in control of the Company, Bondholders will have no voting rights with respect to such a transaction. In the event of any such transaction, Bondholders would not have the right to require us to repurchase their Bonds, even though such a transaction could increase the amount of our indebtedness, or otherwise adversely affect the Bondholders.

If we sell substantially less than all of the Bonds we are offering, the costs we incur to comply with the rules of the Securities and Exchange Commission, or the SEC, regarding financial reporting and other fixed costs (such as those relating to the offering) will be a larger percentage of our revenue and may reduce our financial performance and our ability to fulfil our obligations under the Bonds.

We expect to incur significant costs in maintaining compliance with the financial reporting for a Tier II Regulation A issuer and that our management will spend a significant amount of time assessing the effectiveness of our internal control over financial reporting. We do not anticipate that these costs or the amount of time our management will be required to spend will be significantly less if we sell substantially less than all of the Bonds we are offering.

| 11 |

| Table of Contents |

Redemption requests of Bonds at the option of the Bondholder will be limited by the 10% Limit and to the extent they are accepted, will be subject to financial penalties for early redemption.

While the Bonds carry an early redemption right and a redemption right in the event of death, disability or bankruptcy of the Bondholder, redemptions are subject to an annual 10% redemption limit. As a result, requests for redemption from Bondholders may be rejected by the Company. Additionally, with respect to redemptions at the option of the Bondholders, except for death, disability or bankruptcy, early redemption penalties will apply, which will adversely affect Bondholders seeking to redeem Bonds prior to maturity. If the Company elects to extend the maturity of the Bonds as set forth herein, then a Bondholder may be required to redeem its Bonds, inclusive of the early redemption penalty, if the Bondholder does not wish to keep its Bonds through the extended maturity.

Redemption requests for Bonds at the option of the Bondholder or in the event of death, disability or bankruptcy of a Bondholder may have an adverse effect on the Company’s overall growth and ability to fulfil our obligations on the Bonds.

The Bonds carry an early redemption right and a redemption right in the event of death, disability or bankruptcy of the Bondholder. As a result, one or more Bondholders may elect to have their Bonds redeemed prior to maturity. In such an event, we may not have access to the necessary cash to redeem such Bonds. Additionally, any cash used to satisfy such redemption requests will be diverted from cash required to fund the continued growth of the Company. Accordingly, the use of funds towards redemptions could result in the Company’s inability to meet projected growth targets, which could, in turn, limit the Company’s ability to make interest and principal payments to Bondholders.

Our trustee shall be under no obligation to exercise any of the rights or powers vested in it by the Indenture at the request, order or direction of any of the Bondholders, pursuant to the provisions of the Indenture, unless such Bondholders shall have offered to the trustee reasonable security or indemnity against the costs, expenses and liabilities that may be incurred therein or thereby.

The Indenture governing the Bonds provides that in case an event of default occurs and not be cured, the trustee will be required, in the exercise of its power, to use the degree of care of a reasonable person in the conduct of his own affairs. Subject to such provisions, the trustee will be under no obligation to exercise any of its rights or powers under the Indenture at the request of any Bondholder, unless the Bondholder has offered to the trustee security and indemnity satisfactory to it against any loss, liability or expense.

There is no established trading market for the Bonds and we do not expect one to develop. Therefore, Bondholders may not be able to resell them for the price that they paid or sell them at all.

Prior to this offering, there was no active market for the Bonds and we do not expect one to develop. We do not have any present intention to apply for a quotation for the Bonds on an alternative trading system or over the counter market and even if we obtain that quotation in the future, we do not know the extent to which investor interest will lead to the development and maintenance of a liquid trading market. Further, the Bonds will not be quoted on an alternative trading system or over the counter market until after the termination of this offering, if at all. Therefore, investors will be required to wait until at least after the final termination date of this offering for such quotation. The initial public offering price for the Bonds has been determined by us. You may not be able to sell the Bonds you purchase at or above the initial offering price or sell them at all.

Alternative trading systems and over the counter markets, as with other public markets, may from time to time experience significant price and volume fluctuations. As a result, if the Bonds are listed on such a trading system, the market price of the Bonds may be similarly volatile, and Bondholders may from time to time experience a decrease in the value of their Bonds, including decreases unrelated to our operating performance or prospects. The price of the Bonds could be subject to wide fluctuations in response to a number of factors, including those listed in this "Risk Factors" section of this offering circular. No assurance can be given that the market price of the Bonds will not fluctuate or decline significantly in the future or that Bondholders will be able to sell their Bonds when desired on favorable terms, or at all. Further, the sale of the Bonds may have adverse federal income tax consequences.

| 12 |

| Table of Contents |

We may redeem all or any part of the Bonds that have been issued before their maturity, and you may be unable to reinvest the proceeds at either the same or a higher rate of return.

We may redeem all or any part of the outstanding Bonds prior to maturity. See “Description of Bonds - Optional Redemption” for more information. If redeemed, you may be unable to reinvest the money you receive in the redemption at a rate that is equal to or higher than the rate of return on the Bonds.

Risks Related to Our Business and Our Industry

Because of the unique difficulties and uncertainties inherent in the mineral rights investment business, we face a potential risk of business failure.

Potential investors should be aware of the difficulties normally encountered by companies investing in mineral rights and the potential failure of such enterprises. The likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays encountered in connection with the mineral rights investment that we plan to undertake. These potential problems include, but are not limited to, unanticipated problems relating to finding mineral rights assets, and additional costs and expenses that may exceed current estimates. The search for minerals may also involve numerous hazards. Thus, we may become subject to liability for such hazards, including pollution, cave-ins and other hazards against which we cannot insure or against which we may elect not to insure. The payment of such liabilities may have a material adverse effect on our financial position. In addition, there is no assurance that the expenditures to be made by us in the exploration phase will result in the discovery of economic deposits of minerals. Problems such as unusual or unexpected formations and other conditions are involved in mineral exploration and often result in unsuccessful exploration efforts.

If we are unable to successfully compete within the mineral rights business, we will not be able to achieve profitable operations.

The mineral rights business is highly competitive. This industry has a multitude of competitors. Our exploration activities will be focused on attempting to locate commercially viable mineral deposits. Many of our competitors have greater financial resources than us. As a result, we may experience difficulty competing with other businesses when investing in mineral rights. If we are unable to retain qualified third-party operators to assist us in production activities if a commercially viable deposit is found to exist, we may be unable to enter into production and achieve profitable operations.

Because of factors beyond our control which could affect the marketability of minerals found, we may experience difficulty selling any minerals we discover.

Even if commercial quantities of mineral reserves are discovered, a ready market may not exist for the sale of these reserves. Numerous factors beyond our control may affect the marketability of any minerals discovered. These factors include market fluctuations, the proximity and capacity of minerals markets and processing equipment, government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. These factors could inhibit our ability to sell minerals in the event that commercial amounts of minerals are found.

Because we will be subject to compliance with government regulation which may change, the anticipated costs of our exploration program may increase.

State and local government bodies regulate mineral exploration or exploitation within that state. We may be required to obtain work permits, post bonds and perform remediation work for any physical disturbance to the land in order to comply with these regulations. While our planned exploration program budgets for regulatory compliance, there is a risk that new regulations could increase our costs of doing business, prevent us from carrying out our exploration program, and make compliance with new regulations unduly burdensome.

| 13 |

| Table of Contents |

A shortage of equipment and supplies for our third-party operators could adversely affect our ability to operate our business.

Our third-party operators are dependent on various supplies and equipment in order to carry out its extraction operations. Any shortage of such supplies, equipment and parts could have a material adverse effect on their ability to carry out operations and therefore limit or increase the cost of production and, ultimately, our profitability.

We will be contracting with third parties to perform the actual extraction operations, and these third-party contractors may not perform as we expect.

We will be utilizing third-party contractors to perform the drilling and extraction operations on our assets to extract the natural resources we rely on to generate revenue. If the third-party contractors we hire do not perform as we expect, we may not generate as much of a profit as we anticipate, which could limit our ability to make interest and principal payments to Bondholders. Further, if the contractors are not competent with respect to environmental laws and risks, we may face enforcement actions, lawsuits, civil or criminal fines or penalties, loss or reputation or other costly expenditures, all of which could damage our business operations. Reckless action on the part of incompetent contractors could also lead to damage to, or destruction of, our assets leading to delays in future actions and loss of revenue, among other costly outcomes.

We are subject to significant governmental regulations, which affect our operations and costs of conducting our business.

The current and future operations of our business and that of the third-party contractors on our land are and will be governed by laws and regulations, including:

|

| · | laws and regulations governing mineral concession acquisition, prospecting, development, mining and production; |

|

| · | laws and regulations related to exports, taxes and fees; |

|

| · | labor standards and regulations related to occupational health and mine safety; |

|

| · | environmental standards and regulations related to waste disposal, toxic substances, land use and environmental protection; and |

|

| · | other matters. |

Companies engaged in exploration activities often experience increased costs and delays in production and other schedules as a result of the need to comply with applicable laws, regulations and permits. Failure of the third parties we contract with to comply with applicable laws, regulations and permits may result in enforcement actions, including the forfeiture of claims, orders issued by regulatory or judicial authorities requiring operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment or costly remedial actions. We may be required to compensate those suffering loss or damage by reason of our mineral exploration activities and may have civil or criminal fines or penalties imposed for violations of such laws, regulations and permits.

Regulations and pending legislation governing issues involving climate change could result in increased operating costs, which could have a material adverse effect on our business.

A number of governments or governmental bodies have introduced or are contemplating regulatory changes in response to various climate change interest groups and the potential impact of climate change. Legislation and increased regulation regarding climate change could impose significant costs on us, the third parties we will contract with to perform the mining operations, our venture partners and our suppliers, including costs related to increased energy requirements, capital equipment, environmental monitoring and reporting and other costs to comply with such regulations. Any adopted future climate change regulations could also negatively impact our ability to compete with companies situated in areas not subject to such limitations. Given the emotion, political significance and uncertainty around the impact of climate change and how it should be dealt with, we cannot predict how legislation and regulation will affect our financial condition, operating performance and ability to compete. Furthermore, even without such regulation, increased awareness and any adverse publicity in the global marketplace about potential impacts on climate change by us or other companies in our industry could harm our reputation. The potential physical impacts of climate change on our operations are highly uncertain, and would be particular to the geographic circumstances in areas in which we operate. These may include changes in rainfall and storm patterns and intensities, water shortages, changing sea levels and changing temperatures. These impacts may adversely impact the cost, production and financial performance of our operations.

| 14 |

| Table of Contents |

Existing and possible future laws, regulations and permits governing operations and activities of exploration companies, or more stringent implementation, could have a material adverse impact on our business and cause increases in capital expenditures or require abandonment or delays in exploration.

Our exploration and development activities are subject to environmental risks, which could expose us to significant liability and delay, suspension or termination of our operations.

The exploration and possible future development phases of our business will be subject to federal, state and local environmental regulation. These regulations mandate, among other things, the maintenance of air and water quality standards and land reclamation. They also set out limitations on the generation, transportation, storage and disposal of solid and hazardous waste. Environmental legislation is evolving in a manner which will require stricter standards and enforcement, increased fines and penalties for non-compliance, more stringent environmental assessments, and a heightened degree of responsibility for companies and their officers, directors and employees. Future changes in environmental regulations, if any, may adversely affect the operations of the third-party contractors on our land as well as our business. If we fail to comply with any of the applicable environmental laws, regulations or permit requirements, we could face regulatory or judicial sanctions. Penalties imposed by either the courts or administrative bodies could delay or stop the operations of the third-party contractors on our land or require a considerable capital expenditure. Although we and our third-party operators intend to comply with all environmental laws and permitting obligations in conducting our business, there is a possibility that those opposed to exploration and mining will attempt to interfere with our operations, whether by legal process, regulatory process or otherwise.

Environmental hazards unknown to us, which have been caused by previous or existing owners or operators of the properties, may exist on the properties in which we hold an interest. It is possible that our properties could be located on or near the site of a Federal Superfund cleanup project. Although we will endeavor to avoid such sites, it is possible that environmental cleanup or other environmental restoration procedures could remain to be completed or mandated by law, causing unpredictable and unexpected liabilities to arise.

U.S. Federal Laws

The Comprehensive Environmental, Response, Compensation, and Liability Act (“CERCLA”), and comparable state statutes, impose strict, joint and several liability on current and former owners and operators of sites and on persons who disposed of or arranged for the disposal of hazardous substances found at such sites. It is not uncommon for the government to file claims requiring cleanup actions, demands for reimbursement for government-incurred cleanup costs, or natural resource damages, or for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by hazardous substances released into the environment. The Federal Resource Conservation and Recovery Act (“RCRA”), and comparable state statutes, govern the disposal of solid waste and hazardous waste and authorize the imposition of substantial fines and penalties for noncompliance, as well as requirements for corrective actions. CERCLA, RCRA and comparable state statutes can impose liability for clean-up of sites and disposal of substances found on exploration, mining and processing sites long after activities on such sites have been completed.

The Clean Air Act, as amended, restricts the emission of air pollutants from many sources, including mining and processing activities. The mining operations conducted by third parties on our land may produce air emissions, including fugitive dust and other air pollutants from stationary equipment, storage facilities and the use of mobile sources such as trucks and heavy construction equipment, which are subject to review, monitoring and/or control requirements under the Clean Air Act and state air quality laws. New facilities of theirs may be required to obtain permits before work can begin, and existing facilities may be required to incur capital costs in order to remain in compliance. In addition, permitting rules may impose limitations on their production levels or result in additional capital expenditures in order to comply with the rules.

| 15 |

| Table of Contents |

The National Environmental Policy Act (“NEPA”) requires federal agencies to integrate environmental considerations into their decision-making processes by evaluating the environmental impacts of their proposed actions, including issuance of permits to mining facilities, and assessing alternatives to those actions. If a proposed action could significantly affect the environment, the agency must prepare a detailed statement known as an Environmental Impact Statement (“EIS”). The U.S. Environmental Protection Agency, other federal agencies, and any interested third parties will review and comment on the scoping of the EIS and the adequacy of and findings set forth in the draft and final EIS. This process can cause delays in issuance of required permits or result in changes to a project to mitigate its potential environmental impacts, which can in turn impact the economic feasibility of a proposed project.

The Clean Water Act (“CWA”), and comparable state statutes, imposes restrictions and controls on the discharge of pollutants into waters of the United States. The discharge of pollutants into regulated waters is prohibited, except in accordance with the terms of a permit issued by the Environmental Protection Agency (“EPA”) or an analogous state agency. The CWA regulates storm water mining facilities and requires a storm water discharge permit for certain activities. Such a permit requires the regulated facility to monitor and sample storm water run-off from its operations. The CWA and regulations implemented thereunder also prohibit discharges of dredged and fill material in wetlands and other waters of the United States unless authorized by an appropriately issued permit. The CWA and comparable state statutes provide for civil, criminal and administrative penalties for unauthorized discharges of pollutants and impose liability on parties responsible for those discharges for the costs of cleaning up any environmental damage caused by the release and for natural resource damages resulting from the release.

The Safe Drinking Water Act (“SDWA”) and the Underground Injection Control (“UIC”) program promulgated thereunder, regulate the drilling and operation of subsurface injection wells. EPA directly administers the UIC program in some states and in others the responsibility for the program has been delegated to the state. The program requires that a permit be obtained before drilling a disposal or injection well. Violation of these regulations and/or contamination of groundwater by mining related activities may result in fines, penalties, and remediation costs, among other sanctions and liabilities under the SWDA and state laws. In addition, third-party claims may be filed by landowners and other parties claiming damages for alternative water supplies, property damages, and bodily injury.

We or our third-party operators could be subject to environmental lawsuits.

Neighboring landowners and other third parties could file claims based on environmental statutes and common law for personal injury and property damage allegedly caused by the release of hazardous substances or other waste material into the environment on or around our properties. There can be no assurance that our defense of such claims will be successful. A successful claim against us or any of the third parties we contract with to conduct operations on our land could have an adverse effect on our business prospects, financial condition and results of operation.

While the testing of our mineral right exploration software system has been successful to date, there can be no assurance that we will be able to replicate the process, along with all of the expected economic advantages, on a large commercial scale.

As of the date of this offering circular, we have built and operated our mineral right exploration software system on a limited scale. While we believe that our development and testing to date has proven the concept of our software, there can be no assurance that as we commence large scale operations that we will not incur unexpected costs or hurdles that might restrict the desired scale of our intended operations or negatively impact our projected gross profit margin.

We do not currently own any intellectual property rights relating to our mineral right exploration software system and may be subject to competitors developing the same technology.

As of the date of this offering circular, we do not own any intellectual property rights for any of our software used in our mineral rights exploration. We substantially rely on this software to identify profitable assets ahead of our competitors. If a competitor or anyone else replicates our software, then our business would materially suffer and our ability to repay any of our debts, including the obligations under the Bonds, may be affected.

| 16 |

| Table of Contents |

Our mineral right exploration software system may infringe on the intellectual property rights of others, which could lead to costly disputes or disruptions.

The applied science industry is characterized by frequent allegations of intellectual property infringement. Though we do not expect to be subject to any of these allegations, any allegation of infringement could be time consuming and expensive to defend or resolve, result in substantial diversion of management resources, cause suspension of operations or force us to enter into royalty, license, or other agreements rather than dispute the merits of such allegation. If patent holders or other holders of intellectual property initiate legal proceedings, we may be forced into protracted and costly litigation. We may not be successful in defending such litigation and may not be able to procure any required royalty or license agreements on acceptable terms or at all.

Our business is sensitive to the price of oil and timing of oil production, which may have an adverse effect on our ability to generate returns for investors.

We are in the business of purchasing mineral rights and non-operated working interests in land in the United States, including the rights to drill for oil and gas. A decline in oil prices can have an adverse effect on the value of our interests in the land which will materially and adversely affect our ability to generate cash flows and in turn our ability to make interest payments on the Bonds. Further, a slowdown in the timing of oil production may reduce our ability to collect lease payments from leaseholders, which could limit our ability to make interest and principal payments to Bondholders.

Our investments are focused on acquiring properties where oil production is either ongoing or imminent. Therefore, very few of our investments are expected to generate returns that substantially exceed our projections.

We focus on acquiring properties where oil production is ongoing or imminent, which provide predictable near-term cash flows. Less than ten percent (10%) of our total portfolio is expected to include investments with no current drill schedule, therefore investors should not expect our investments to generate returns that substantially exceed our current projections.

Our business could be adversely affected by unfavorable economic and political conditions, which in turn, can negatively impact our ability to generate returns to you.

The Company’s future business and operations are sensitive to general business and economic conditions in the United States. National and regional economies and financial markets have become increasingly interconnected, which increases the possibilities that conditions in one country, region, or market might adversely impact issuers in a different country, region, or market. Major economic or political disruptions, such as the slowing economy in China, the war in Ukraine and sanctions on Russia, and a potential economic slowdown in the United Kingdom and Europe, may have global negative economic and market repercussions. While the Company does not have or intend to have operations in those countries, such disruptions may nevertheless cause fluctuations in oil prices, which could impact our ability to generate cash flows, and in turn, make payments to you.

The lingering effects of the coronavirus (also known as the COVID-19 virus) pandemic and uncertainty in the financial markets may adversely affect our ability to generate revenues.

The long-term impact of the coronavirus pandemic on the U.S. and world economies remains unknown, but effects of the pandemic, as well as inflation and rising interest rates, has led to uncertainty in the financial markets that could significantly and negatively impact the global, national and regional economies, the length and breadth of which cannot currently be predicted. Extended disruptions to the global economy are likely to cause fluctuations in oil prices and the timing of oil production, which could have a material adverse effect on our ability to generate cash flow, which in turn could limit our ability to pay interest on the Bonds.

The Company, through its investment in PhoenixOp and future assignment of oil and gas properties to PhoenixOp intends to begin drilling activities. Such activities will pose additional risks to the Company which could adversely affect the Company.

PhoenixOp, a wholly-owned subsidiary of the Company, will face numerous risks while drilling, including: failing to place a well bore in the desired target producing zone; not staying in the desired drilling zone while drilling horizontally through the formation; failing to run its casing the entire length of the well bore; and not being able to run tools and other equipment consistently through the horizontal well bore. Risks PhoenixOp may face while completing our wells include, but are not limited to, not being able to fracture stimulate the planned number of stages; failing to run tools the entire length of the well bore during completion operations; not successfully cleaning out the well bore after completion of the final fracture stimulation stage; increased seismicity in areas near its completion activities; unintended interference of completion activities performed by us or by third p arties with nearby operated or non-operated wells being drilled, completed, or producing; and failure of our optimized completion techniques to yield expected levels of production.

Further, many factors may occur that cause PhoenixOp to curtail, delay or cancel scheduled drilling and completion projects, including but not limited to:

|

| · | abnormal pressure or irregularities in geological formations; |

|

| · | shortages of or delays in obtaining equipment or qualified personnel; |

|

| · | shortages o f or delays in obtaining components used in fracture stimulation processes such as water and proppants; |

|

| · | delays associated with suspending our operations to accommodate nearby drilling or completion operations being conducted by other operators; |

|

| · | mechanical difficulties, fires, explosions, equipment failures or accidents, including ruptures of pipelines or storage facilities, or train derailments; |

|

| · | restrictions on the use of underground injection wells for disposing of waste water from oil and gas activities; |

|

| · | political events, public protests, civil disturbances, terrorist acts or cyber attacks; |

|

| · | decreases in, or extended periods of low, crude oil and natural gas prices; |

|

| · | title problems; |

|

| · | environmental hazards, such as uncontrollable flows of crude oil, natural gas, brine, well fluids, hydraulic fracturing fluids, toxic gas or other pollutants into the environment, including groundwater and shoreline contamination; |

|

| · | adverse climatic conditions and natural disasters; |

|

| · | spillage or mishandling of crude oil, natural gas, brine, well fluids, hydraulic fracturing fluids, toxic gas or other pollutants by us or by third party service providers; |

|

| · | limitations in infrastructure, including transportation, processing, refining and exportation capacity, or markets for crude oil and natural gas; and |

|

| · | delays imposed by or resulting from compliance with regulatory requirements including permitting. |

PhoenixOp is not insured against all risks associated with our business. PhoenixOp may elect to not obtain insurance if we believe the cost of available insurance is excessive relative to the risks presented or for other reasons. In addition, pollution and environmental risks are generally not fully insurable.

Losses and liabilities arising from any of the above events could reduce the value o f the Company’s capital contributions to PhoenixOp, increase the need for the Company to provide additional capital to PhoenixOp, and otherwise harm the Company’s financial position, which could adversely affect the Company and its ability to pay its obligations under the Bonds.

Any cybersecurity-attack or other security breach of our technology systems, or those of third-party vendors we rely on, could subject us to significant liability and harm our business operations and reputation.

Cybersecurity attacks and security breaches of our technology systems, including those of our clients and third-party vendors, may subject us to liability and harm our business operations and overall reputation. Our operations rely on the secure processing, storage and transmission of confidential and other information in its computer systems and networks. Threats to information technology systems associated with cybersecurity risks and cyber incidents continue to grow, and there have been a number of highly publicized cases involving financial services companies, consumer-based companies and other organizations reporting the unauthorized disclosure of client, customer or other confidential information in recent years. Cybersecurity risks could disrupt our operations, negatively impact our ability to compete and result in injury to our reputation, downtime, loss of revenue, and increased costs to prevent, respond to or mitigate cybersecurity events. Although we have developed, and continue to invest in, systems and processes that are designed to detect and prevent security breaches and cyber-attacks, our security measures, information technology and infrastructure may be vulnerable to attacks by hackers or breached due to employee error, malfeasance or other disruptions that could result in unauthorized disclosure or loss of sensitive information; damage to our reputation; the incurrence of additional expenses; additional regulatory scrutiny or penalties; or our exposure to civil or criminal litigation and possible financial liability, any of which could have a material adverse effect on our business, financial condition and results of operations.

[Remainder of page intentionally left blank]

| 17 |

| Table of Contents |

We estimate that the net proceeds we will receive from this offering will be $19,172,580 after deducting the Broker-Dealer Fee. We previously paid the Broker-Dealer Fee to our former broker/dealer of record and may pay the Broker-Dealer Fee to broker-dealers who we retain to assist in the placement of Bonds.

We plan to use substantially all of the net proceeds from this offering on continued acquisitions of mineral rights and non-operated working interests, as well as additional asset acquisitions. The table below demonstrates our anticipated uses of offering proceeds, but the table below does not require us to use offering proceeds as indicated. Our actual use of offering proceeds will depend upon market conditions, among other considerations. The numbers in the table are approximate.

|

|

| Maximum Offering Amount* |

| |||||

|

|

| Amount(2) |

|

| Percent |

| ||

| Gross offering proceeds |

| $ | 20,076,000 |

|

|

| 100 | % |

| Less offering expenses: |

|

|

|

|

|

|

|

|

| Broker-Dealer Fee(1) |

| $ | 903,420 |

|

|

| 4.5 | % |

| Net Proceeds |

| $ | 19,172,580 |

|

|

| 95.5 | % |

| Acquisitions of Mineral Rights and Non-Operated Working Interests(3) |

| $ | 18,214,954.80 |

|

|

| 90.73 | % |

| Working Capital and other asset acquisitions(4) |

| $ | 957,625.20 |

|

|

| 4.77 | % |

| * | Amounts and percentages may vary from the above, provided that selling commission and expenses will not exceed 4.5% of gross offering proceeds. | |

|

|

| |

| (1) | This represents the maximum broker-dealer fee payable to Dalmore Group of up to 4.5% of the gross proceeds of the offering. See “Plan of Distribution” for more information. Certain of our employees, including Mr. Willer, are registered as associated persons of our broker-dealer and will be paid part of any Broker-Dealer Fee resulting from Bonds sold with their assistance. | |

| (2) | This assumes we sell the Maximum Offering Amount comprised of $20,076,000 which represents the value of The maximum gross proceeds of Bonds available to be offered as of the date of this offering circular out of the rolling 12-month maximum offering amount $75 million of securities that we are permitted to issued pursuant to Regulation A. | |

| (3) | We anticipate approximately 90.73% of the gross proceeds of this offering (95% of net proceeds) will be used to acquire the mineral rights and non-operated working interests which represent our core business. | |

| (4) | We anticipate approximately 4.77% of our gross proceeds (5% of net proceeds) will be used for general working capital needs, such as the payment of executive and employee salaries, general overhead and operating costs, and the acquisition of assets in the oil and gas space that are not mineral rights or non-operated working interests. | |

[Remainder of page intentionally left blank]

| 18 |

| Table of Contents |

Who May Invest

As a Tier II, Regulation A offering, investors must comply with the 10% limitation on investment in the offering, as prescribed in Rule 251. The only investor in this offering exempt from this limitation is an accredited investor, an "Accredited Investor," as defined under Rule 501 of Regulation D. If you meet one of the following tests you qualify as an Accredited Investor:

(i) You are a natural person who has had individual income in excess of $200,000 in each of the two most recent years, or joint income with your spouse (or spousal equivalent) in excess of $300,000 in each of these years, and have a reasonable expectation of reaching the same income level in the current year;

(ii) You are a natural person and your individual net worth, or joint net worth with your spouse (or spousal equivalent), exceeds $1,000,000 at the time you purchase the Bonds (please see below on how to calculate your net worth);

(iii) You are an executive officer, director, trustee, general partner or advisory board member of the issuer or a person serving in a similar capacity as defined in the Investment Company Act of 1940, as amended, the Investment Company Act, or a manager or executive officer of the general partner of the issuer;

(iv) You are an investment adviser registered pursuant to Section 203 of the Investment Advisers Act of 1940 or an exempt reporting adviser as defined in Section 203(l) or Section 203(m) of that act, or an investment adviser registered under applicable state law.

(v) You are an organization described in Section 501(c)(3) of the Internal Revenue Code of 1986, as amended, the Code, a corporation, a Massachusetts or similar business trust or a partnership or a limited liability company, not formed for the specific purpose of acquiring the Bonds, with total assets in excess of $5,000,000;

(vi) You are an entity, with investments, as defined under the Investment Company Act, exceeding $5,000,000, and you were not formed for the specific purpose of acquiring the Bonds;

(vii) You are a bank or a savings and loan association or other institution as defined in the Securities Act, a broker or dealer registered pursuant to Section 15 of the Securities Exchange Act of 1934, as amended, the Exchange Act, an insurance company as defined by the Securities Act, an investment company registered under the Investment Company Act of 1940, as amended, the Investment Company Act, or a business development company as defined in that act, any Small Business Investment Company licensed by the Small Business Investment Act of 1958, any Rural Business Investment Company as defined in the Consolidated Farm and Rural Development Act of 1961 or a private business development company as defined in the Investment Advisers Act of 1940;

(viii) You are an entity with total assets not less than $5,000,000 (including an Individual Retirement Account trust) in which each equity owner is an accredited investor;