AN OFFERING STATEMENT PURSUANT TO REGULATION A RELATING TO THESE SECURITIES HAS BEEN FILED WITH THE SECURITIES AND EXCHANGE COMMISSION (“SEC”). INFORMATION CONTAINED IN THIS PRELIMINARY OFFERING CIRCULAR IS SUBJECT TO COMPLETION OR AMENDMENT. THESE SECURITIES MAY NOT BE SOLD NOR MAY OFFERS TO BUY BE ACCEPTED BEFORE THE OFFERING STATEMENT FILED WITH THE COMMISSION IS QUALIFIED. THIS PRELIMINARY OFFERING CIRCULAR SHALL NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY NOR MAY THERE BE ANY SALES OF THESE SECURITIES IN ANY STATE IN WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE UNLAWFUL BEFORE REGISTRATION OR QUALIFICATION UNDER THE LAWS OF SUCH STATE. WE MAY ELECT TO SATISFY OUR OBLIGATION TO DELIVER A FINAL OFFERING CIRCULAR BY SENDING YOU A NOTICE WITHIN TWO BUSINESS DAYS AFTER THE COMPLETION OF OUR SALE TO YOU THAT CONTAINS THE URL WHERE THE FINAL OFFERING CIRCULAR OR THE OFFERING STATEMENT IN WHICH SUCH FINAL OFFERING CIRCULAR WAS FILED MAY BE OBTAINED.

PRELIMINARY OFFERING CIRCULAR DATED JULY 15, 2019

ERC HOMEBUILDERS 1, INC.

2738 FALKENBURG ROAD SOUTH

RIVERVIEW, FL 33578

(813) 621-5000

Up to 8,333,333 shares of Preferred Stock and

up to 8,333,333 shares of Class A Common Stock into which the Preferred Stock may convert

The Preferred Stock is convertible into Class A Common Stock either at the discretion of the investor or automatically upon effectiveness of registration of the securities in an initial public offering. The total number of shares of the Class A Common Stock into which the Preferred may be converted will be determined by dividing the original issue price per share by the conversion price per share. See “Securities Being Offered” at Page 41 for additional details.

Minimum investment 83.33 shares of Preferred Stock ($500)

SEE “SECURITIES BEING OFFERED” AT PAGE 41

| Price to Public | Broker-Dealer discount and commissions (1) | Proceeds to issuer (2) | Proceeds to other persons | |||||||||||||

| Per share | $ | 6 | 0.06 | $ | 5.94 | 0 | ||||||||||

| Total Maximum | $ | 50,000,000 | $ | 518,000 | $ | 49,482,000 | 0 | |||||||||

(1) The company has engaged Sageworks Capital, LLC, member FINRA/SIPC (“Sageworks”), to perform administrative and technology related functions in connection with this offering, but not for underwriting or placement agent services. This includes the 1% commission, but it does not include the one-time set-up fees payable by the company to Sageworks. See “Plan of Distribution” for details.

(2) The company expects that, not including state filing fees, the minimum amount of expenses of the offering that we will pay will be approximately $483,000 regardless of whether the number of shares that are sold in this offering. In the event that the maximum offering amount is sold, the total offering expenses will be approximately $5,500,000.

This offering (the “offering”) will terminate at the earlier of (1) the date at which the Maximum Offering amount has been sold, (2) the date which is one year from this offering being qualified by the United States Securities and Exchange Commission, or (3) the date at which the offering is earlier terminated by the company at its sole discretion. The company plans to engage an escrow agent to hold any funds that are tendered by investors. The offering is being conducted on a best-efforts basis without any minimum target. Provided that an investor purchases shares in the amount of the minimum investment, $504 (84 shares), there is no minimum number of shares that needs to be sold in order for funds to be released to the company and for this offering to close, which may mean that the company does not receive sufficient funds to cover the cost of this offering. The company may undertake one or more closings on a rolling basis. After each closing, funds tendered by investors will be made available to the company. After the initial closing of this offering, we expect to hold closings on at least a monthly basis.

Each holder of ERC Homebuilders 1 preferred stock (the “Preferred Stock”) is entitled to one vote for each share on all matters submitted to a vote of the stockholders. Holders of Preferred Stock will vote together with the holders of Common Stock as a single class on all matters (including the election of directors) submitted to vote or for the consent of the stockholders of ERC Homebuilders 1. Holders of the Common Stock will continue to hold a majority of the voting power of all of the company’s equity stock at the conclusion of this offering and therefore control the board.

THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OR GIVE ITS APPROVAL OF ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SOLICITATION MATERIALS. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION

GENERALLY, NO SALE MAY BE MADE TO YOU IN THIS OFFERING IF THE AGGREGATE PURCHASE PRICE YOU PAY IS MORE THAN 10% OF THE GREATER OF YOUR ANNUAL INCOME OR NET WORTH. DIFFERENT RULES APPLY TO ACCREDITED INVESTORS AND NON-NATURAL PERSONS. BEFORE MAKING ANY REPRESENTATION THAT YOUR INVESTMENT DOES NOT EXCEED APPLICABLE THRESHOLDS, WE ENCOURAGE YOU TO REVIEW RULE 251(d)(2)(i)(C) OF REGULATION A. FOR GENERAL INFORMATION ON INVESTING, WE ENCOURAGE YOU TO REFER TO www.investor.gov.

This offering is inherently risky. See “Risk Factors” on page 8.

Sales of these securities will commence on approximately , 2019.

The company is following the “Offering Circular” format of disclosure under Regulation A.

In the event that we become a reporting company under the Securities Exchange Act of 1934, we intend to take advantage of the provisions that relate to “Emerging Growth Companies” under the JOBS Act of 2012. See “Implications of Being an Emerging Growth Company.

TABLE OF CONTENTS

In this Offering Circular, the term “ERC Homebuilders 1,” “we,” “us, “our” or “the company” refers to ERC Homebuilders 1, Inc., a Delaware corporation.

THIS OFFERING CIRCULAR MAY CONTAIN FORWARD-LOOKING STATEMENTS AND INFORMATION RELATING TO, AMONG OTHER THINGS, THE COMPANY, ITS BUSINESS PLAN AND STRATEGY, AND ITS INDUSTRY. THESE FORWARD-LOOKING STATEMENTS ARE BASED ON THE BELIEFS OF, ASSUMPTIONS MADE BY, AND INFORMATION CURRENTLY AVAILABLE TO THE COMPANY’S MANAGEMENT. WHEN USED IN THE OFFERING MATERIALS, THE WORDS “ESTIMATE,” “PROJECT,” “BELIEVE,” “ANTICIPATE,” “INTEND,” “EXPECT” AND SIMILAR EXPRESSIONS ARE INTENDED TO IDENTIFY FORWARD-LOOKING STATEMENTS, WHICH CONSTITUTE FORWARD LOOKING STATEMENTS. THESE STATEMENTS REFLECT MANAGEMENT’S CURRENT VIEWS WITH RESPECT TO FUTURE EVENTS AND ARE SUBJECT TO RISKS AND UNCERTAINTIES THAT COULD CAUSE THE COMPANY’S ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE CONTAINED IN THE FORWARD-LOOKING STATEMENTS. INVESTORS ARE CAUTIONED NOT TO PLACE UNDUE RELIANCE ON THESE FORWARD-LOOKING STATEMENTS, WHICH SPEAK ONLY AS OF THE DATE ON WHICH THEY ARE MADE. THE COMPANY DOES NOT UNDERTAKE ANY OBLIGATION TO REVISE OR UPDATE THESE FORWARD-LOOKING STATEMENTS TO REFLECT EVENTS OR CIRCUMSTANCES AFTER SUCH DATE OR TO REFLECT THE OCCURRENCE OF UNANTICIPATED EVENTS.

IMAGES CONTAINED IN THIS OFFERING CIRCULAR ARE ARTIST’S IMPRESSIONS AND THE ACTUAL PROPERTIES MAY VARY.

Implications of Being an Emerging Growth Company

As an issuer with less than $1 billion in total annual gross revenues during our last fiscal year, we will qualify as an “emerging growth company” under the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) and this status will be significant if and when we become subject to the ongoing reporting requirements of the Exchange. An emerging growth company may take advantage of certain reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies. In particular, as an emerging growth company we:

| · | will not be required to obtain an auditor attestation on our internal controls over financial reporting pursuant to the Sarbanes-Oxley Act of 2002; |

| · | will not be required to provide a detailed narrative disclosure discussing our compensation principles, objectives and elements and analyzing how those elements fit with our principles and objectives (commonly referred to as “compensation discussion and analysis”); |

| · | will not be required to obtain a non-binding advisory vote from our shareholders on executive compensation or golden parachute arrangements (commonly referred to as the “say-on-pay,” “say-on-frequency” and “say-on-golden-parachute” votes); |

| 3 |

| · | will be exempt from certain executive compensation disclosure provisions requiring a pay-for-performance graph and CEO pay ratio disclosure; |

| · | may present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations, or MD&A; and |

| · | will be eligible to claim longer phase-in periods for the adoption of new or revised financial accounting standards. |

We intend to take advantage of all of these reduced reporting requirements and exemptions, including the longer phase-in periods for the adoption of new or revised financial accounting standards under Section 107 of the JOBS Act. Our election to use the phase-in periods may make it difficult to compare our financial statements to those of non-emerging growth companies and other emerging growth companies that have opted out of the phase-in periods under Section 107 of the JOBS Act.

Under the JOBS Act, we may take advantage of the above-described reduced reporting requirements and exemptions for up to five years after our initial sale of common equity pursuant to a registration statement declared effective under the Securities Act of 1933, as amended, or such earlier time that we no longer meet the definition of an emerging growth company. Note that this offering, while a public offering, is not a sale of common equity pursuant to a registration statement, since the offering is conducted pursuant to an exemption from the registration requirements. In this regard, the JOBS Act provides that we would cease to be an “emerging growth company” if we have more than $1 billion in annual revenues, have more than $700 million in market value of our common stock held by non-affiliates, or issue more than $1 billion in principal amount of non-convertible debt over a three-year period.

Certain of these reduced reporting requirements and exemptions are also available to us due to the fact that we may also qualify, once listed, as a “smaller reporting company” under the Commission’s rules. For instance, smaller reporting companies are not required to obtain an auditor attestation on their assessment of internal control over financial reporting; are not required to provide a compensation discussion and analysis; are not required to provide a pay-for-performance graph or CEO pay ratio disclosure; and may present only two years of audited financial statements and related MD&A disclosure.

| 4 |

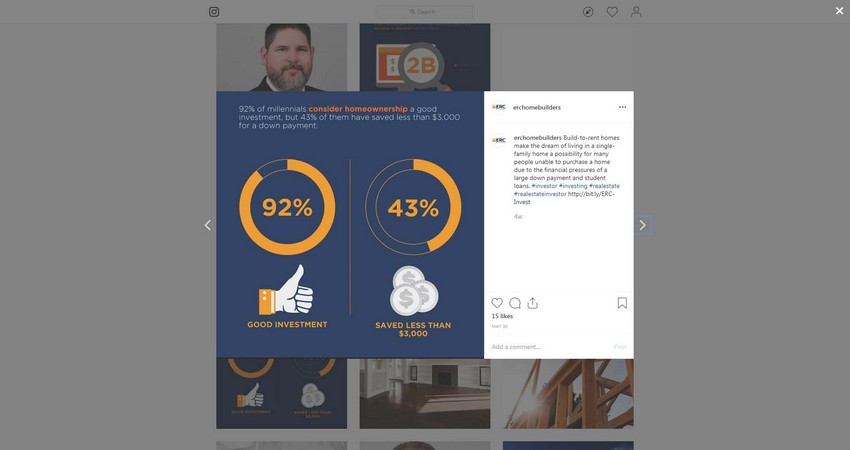

ERC Homebuilders 1 was formed in 2018 and is intended to become a next generation wholesaler of build-for-rent (“Build-For-Rent”) single and two-family residences. As home ownership continues to drop and more Millennials, Gen-X’ers and Baby-Boomers want to rent, demand in the rental market for new units is increasing. There is a corresponding demand for such properties by institutional investors. The company plans to target this rising demand for single-family rental properties, and specifically the unmet demand of institutional buyers such as private equity firms, hedge funds and national rental operators by developing and wholesaling Build-For-Rent units, initially in its home state of Florida and expanding to other parts of the country from there.

The company will operate under the brand name ERC Homebuilders 1, Inc. and is a subsidiary of ERC Home Builders, Inc., (“ERC Parent”). ERC was incorporated in 2018 by the company’s principals, who jointly operated a home renovation and new-building company in Central Florida – ERC Homes, LLC.

ERC Parent intends to operate two operating subsidiaries, ERC Homebuilders 1 and ERC Homebuilders 2, each an “Operating Subsidiary” and collectively the “Operating Subsidiaries”). Each Operating Subsidiary will be located in a different region in Florida, and will operate under the names listed below:

| REGION | NAME |

| South Florida | ERC Homebuilders 1, Inc. |

| North Florida | ERC Homebuilders 2, Inc. |

The company was incorporated in Delaware on October 24, 2018 as ERC Home Builders South Florida, Inc. On February 19, 2019 the company changed its name to ERC Homebuilders 1, Inc and the company is not currently profitable.

Our plan to differentiate ourselves from competitors

The company’s principals have decades of real estate development experience and are responsible for over a billion dollars of successful development, construction and real estate management. The company plans to differentiate itself from other Build-For-Rent developers in a number of ways including by bundling 20+ Build-For-Rents in contiguous areas, which increases simplicity and redundancy and improves efficiency over piecemeal construction. We plan to enter into pre-sale agreements for the properties in bundles prior to the construction’s completion and we plan to add features called for by our buyer entities, which may include such items as Eco Living Options, remote security options, etc. No such pre-sale agreements have been entered into as of the date of this offering circular.

The Offering

| Securities offered | Up to 8,333,333 shares of Preferred Stock and up to 8,333,333 shares of Class A Common Stock into which they may convert. | |

| Class A Stock Common outstanding before the offering | 0 shares of Class A Common Stock. | |

| Preferred Stock outstanding before the offering | 0 shares of Preferred Stock. | |

| Preferred Stock outstanding after the offering | 8,333,333 shares of Preferred Stock | |

| Share Price | $6 per share | |

| Minimum Investment | $500 |

Terms of the Preferred Stock

Holders of the Preferred Stock are entitled to the following:

| · | Dividend distribution: |

| o | Accrual of dividends: |

| § | Investors in this offering will begin to accrue an annual 8% dividend after the issuance of their Preferred Stock. |

| 5 |

| § | Payment of dividends: |

| · | Payments will be made monthly providing legally available funds are available. |

| · | Declared dividends |

| o | In the event the company declares a dividend distribution to the Common Stock holders, holders of Preferred Stock will receive dividend distribution. Dividends will be distributed to holders on a pro-rata on an as converted basis. |

| · | Voting: |

| o | Holders of the Preferred Stock are entitled to one vote for each share on all matters submitted to a vote of the shareholders. |

| o | Holders of Preferred Stock at all times will vote together with the holders of Common Stock as a single class on all matters (including the election of directors) submitted to vote or for the consent of the stockholders of ERC Homebuilders 1. |

| o | Holders of Class B Common Stock (currently held exclusively ERC Parent) are entitled to five votes per share (see, “Risk Factors – The officers of ERC Homebuilders |

1 control the company and the company does not currently have any independent directors”) and thus will control the board.

| · | Liquidation preference: |

| o | In the event of a liquidation, investors will be entitled to receive the greater of the amount of their total investment in the shares of Preferred Stock and any accrued and unpaid dividends or their pro rata percentage of the proceeds calculated based on the number of shares owned by each investor on an “as converted to Common Stock” basis. |

| · | Conversion: |

| o | Holders of the Preferred Stock may convert their shares of Preferred Stock into Class A Common Stock in their sole discretion. |

| o | In the event of an initial public offering, as defined in the Amended and Restated Certificate of Incorporation, conversion of the Preferred Stock is mandatory. |

| o | Anti-dilution protection is provided to holders of the Preferred Stock using the weighted average method. See, “Securities Being Offered – Preferred Stock – Anti-Dilution Rights”; Section 5 of the Amended and Restated Certificate of Incorporation, filed as an exhibit to this Offering Statement of which this Offering Circular forms a part. |

Use of Proceeds

Proceeds from this offering will be used to fund the company’s construction and development of single family homes for the Build-For-Rent market, related marketing efforts and operational expenses. See “Use of Proceeds to Issuer” section of this Offering Circular.

Summary Risk Factors

ERC Homebuilders 1 is a startup. The company was incorporated on October 24, 2018 and is still in an early stage of development. The company is not close to profitability as initial projects can take as long as at a minimum one year to develop and construct, and may not provide a return on investment for at least as long as 18 months. Investing in the company involves a high degree of risk (see “Risk Factors”). As an investor, you should be able to bear a complete loss of your investment. Some of the more significant risks include those set forth below:

| · | This is a very young company. |

| · | The company’s affiliated entities have no prior performance record. |

| · | The company’s auditor has issued a “going concern” opinion. |

| · | The company has minimal operating capital, no significant assets and no revenue from operations. |

| · | The success of ERC Homebuilders 1 business is dependent on purchasing large parcels of land with specific characteristics at favorable prices. |

| · | The company plans to raise significantly more capital and future fundraising rounds could result in dilution. |

| · | Success in the real estate industry is highly unpredictable, and there is no guarantee the company’s business plan will be successful in the market. |

| · | The company may not be able to attract purchasers for its already developed homes in a timely manner, which may negatively affect its operations and revenues. |

| · | ERC Homebuilders 1 operates in a highly competitive market. |

| · | Investor or ultimate lessee complaints or litigation on behalf of such individuals or entities or employees may adversely affect our business, results of operations or financial condition. |

| · | The company’s insurance coverage may not be adequate to cover all possible losses that it could suffer and its insurance costs may increase. |

| · | The company may not be able to develop its properties, or obtain and maintain licenses and permits necessary for such developments, in compliance with laws, regulations and other requirements, which could adversely affect its business, results of operations or financial condition. |

| 6 |

| · | The company has concentrated its investments in single-family real estate, which is subject to the risk that the values of their investments may decline if there is a prolonged downturn in real estate values. |

| · | The illiquidity of real estate may make it difficult for the company to dispose of one or more of our properties or negatively affect its ability to profitably sell such properties and access liquidity. |

| · | The company’s development and growth strategy depends on its ability to fund, develop and sell single-family real estate profitably. |

| · | The company’s development and construction of the first properties in Florida depends on its ability to obtain favorable mortgage financing. |

| · | ERC Homebuilders 1 depends on a small management team and may need to hire more people to be successful. |

| · | The company will be materially harmed if it loses the services of any of its current executive officers. |

| · | The company will require a general manager, who has not yet been hired. |

| · | The payment of accrued dividends is paid out of the company’s reserved funds for the foreseeable future. |

| · | Distributions will be only made if permitted under Delaware law, which is subject to change, and in the sole discretion of the board of directors. |

| · | The tax treatment of dividends may vary and distributions to shareholders may be taxed as capital gains. |

| · | The company is responsible for certain administrative burdens relating to taxation. |

| · | The Offering price has been arbitrarily set by the company. |

| · | There is no minimum amount set as a condition to closing this offering. |

| · | The officers of ERC Homebuilders 1 control the company and the company does not currently have any independent directors. |

| · | The exclusive forum provision in the company’s Amended and Restated Certificate of Incorporation may have the effect of limiting an investor’s ability to bring legal action against the company and could limit an investor’s ability to obtain a favorable judicial forum for disputes. |

| · | Investors in this offering may not be entitled to a jury trial with respect to claims arising under the subscription agreement and claims where the forum selection provision is applicable, which could result in less favorable outcomes to the plaintiff(s) in any such action. |

| · | There is no current market for ERC Homebuilders 1’s shares. |

| · | There are conflicts of interest between the company, its management and their affiliates. |

| · | The interests of ERC Homebuilders 1, ERC Parent and the company’s other affiliates may conflict with your interests. |

| · | There are conflicts of interest between the company and some of the members of the Board of Directors. |

| · | Loans issued by ERC Parent to ERC Homebuilders 1 may not be made at arm’s length. |

| · | ERC Parent and ERC Homebuilders 1 intend to share some services. |

| 7 |

The SEC requires the company to identify risks that are specific to its business and its financial condition. The company is still subject to all the same risks that all companies in its business, and all companies in the economy, are exposed to. These include risks relating to economic downturns, political and economic events and technological developments (such as hacking and the ability to prevent hacking). Additionally, early-stage companies are inherently riskier than more developed companies. You should consider general risks as well as specific risks when deciding whether to invest.

Risks relating to our business

This is a very young company.

The company was incorporated in October 2018. It is a startup company that has not yet started operations, and has not started to build its Build-For-Rent properties. There is no history upon which an evaluation of its past performance and future prospects can be made. Statistically, most startup companies fail.

The company’s auditor has issued a “going concern” opinion.

ERC Homebuilders 1’s auditor has issued a “going concern” opinion on its financial statements, which means the company may not be able to succeed as a business without additional financing. ERC Homebuilders 1 was incorporated in October 2018. As of November 19, 2018, the date of its financial statements, it has no revenues and is not close to profitability. It has an accumulated deficit of $62,122 as of November 18, 2018. The audit report states that the company’s ability to continue as a going concern for the next twelve months is dependent upon its ability to generate cash from operating activities and/or to raise additional capital to fund its operations. The company’s failure to raise additional short-term capital could have a negative impact on not only their financial condition but also their ability to remain in business.

The company has minimal operating capital, no significant assets and no revenue from operations.

The company currently has minimal operating capital and for the foreseeable future will be dependent upon its ability to finance its planned operations from the sale of securities or other financing alternatives. There can be no assurance that it will be able to successfully raise operating capital in this or other offerings of securities, or to raise enough funds to fully construct and market single-family homes as described in this offering plan. The failure to successfully raise operating capital could result in its inability to execute its business plan and potentially lead to bankruptcy, which would have a material adverse effect on the company and its investors.

The success of ERC Homebuilders 1 business is dependent on purchasing large and specific parcels of land at favorable prices.

ERC Homebuilders 1 is a capital-intensive operation and requires the purchase of large and specific parcels of land appropriate for the construction of one and two-family homes. As of the date of this Offering Circular the company has not purchased land for the first Florida/Southeastern development. Further, the company does not know whether it will be able to obtain purchase terms that are favorable. Finally, if this offering does not raise enough capital to purchase the land and begin construction, the company will need to procure external financing for the purchase of the land and/or construction of the properties.

The company plans to raise significantly more capital and future fundraising rounds could result in dilution.

ERC Homebuilders1 will need to raise additional funds to finance its operations or fund its business plan. Even if the company manages to raise subsequent financing or borrowing rounds, the terms of those borrowing rounds might be more favorable to new investors or creditors than to existing investors such as you. New equity investors or lenders could have greater rights to our financial resources (such as liens over our assets) compared to existing shareholders. Additional financings could also dilute your ownership stake, potentially drastically. See “Dilution” and the “Management’s Discussion and Analysis of Financial Condition and Results of Operations– Plan of Operation” for more information.

| 8 |

Risks Related to investments in real estate

There are inherent risks with real estate investments.

Real estate assets are subject to varying degrees of risk. For example, the real estate we intend to acquire will not be able to be quickly converted to cash, limiting our ability to promptly vary our portfolio in response to changing economic, financial and investment conditions. Real estate assets also are subject to adverse changes in general economic conditions which reduce the demand for rental space. Other factors also affect the value of real estate assets, including:

| · | federal, state or local regulations and controls affecting rents, zoning, prices of goods, fuel and energy consumption, water and environmental restrictions; |

| · | the attractiveness of a property to tenants; and |

| · | labor and material costs. |

Further, our investments may not generate revenues sufficient to meet operating expenses.

Your investment is directly affected by general economic and regulatory factors that impact real estate investments.

Because we will primarily develop residential real estate, we are impacted by general economic and regulatory factors impacting real estate investments. These factors are generally outside of our control. Among the factors that could impact our real estate assets and the value of your investment are:

| · | local conditions such as an oversupply of space or reduced demand for real estate assets of the type that we own or seek to acquire; |

| · | inability to find investors interested in our residential developments; |

| · | inability to purchase land on favorable terms; |

| · | inflation and other increases in operating costs, including insurance premiums, utilities and real estate taxes; |

| · | adverse changes in the laws and regulations applicable to us; |

| · | the relative illiquidity of real estate investments; | |

| · | changing market demographics; |

| · | an inability to acquire and finance properties on favorable terms; |

| · | acts of God, such as earthquakes, floods or other uninsured losses; and |

| · | changes or increases in interest rates and availability of permanent mortgage funds. |

In addition, periods of economic slowdown or recession, or declining demand for real estate, or the public perception that any of these events may occur, could result in a general decline in rents or increased defaults under existing leases.

Success in the real estate industry can be highly unpredictable and there is no guarantee the company’s business model will be successful in the market.

The company’s success will depend on whether it can successfully build and market two-family homes specifically for the Build-For-Rent market. The company is exposed to a lack of interest for the kind of properties we build by wholesalers as well as its inability to predict whether consumers would be interested in renting the properties. Consumer tastes, trends and preferences frequently change and are notoriously difficult to predict. If the company fails to anticipate future real estate investor and consumer preferences its business and financial performance will likely suffer. The real estate industry is fiercely competitive. The company may not be able to develop and sell properties in a profitable way.

The company may not secure pre-commitments for developments prior to breaking ground.

The company has not yet signed any pre-sale agreements with any institutional investors. While we plan to enter into such agreements prior to completion of our developments, there is no guarantee that we will be able to do so. If we cannot sign any agreements prior to breaking ground or at some time prior to the construction and completion of our developments, we may incur additional costs related to sales and marketing and may be delayed in completing our developments or be subject to additional management expenses.

| 9 |

If we successfully develop our Build-For-Rent properties but are not able to sell them in a timely manner, we may need to operate the and manage the properties as owners, which would add additional operational expenses and may result in significant losses

The company’s success will also depend on whether it can successfully resell it properties developed for the Build-For-Rent market either prior to completion of construction or in a timely manner thereafter. There is no guarantee that we will be able to sell our properties in a timely manner or ever. If we are unable to sell the completed properties, we will need to dedicate significant resources to managing and leasing our properties, which would pose an added financial and management burden on the company.

Geographic concentration of our portfolio may make us particularly susceptible to adverse economic developments in the real estate markets of those areas.

In the event that we have a concentration of properties in a particular geographic area, our operating results and ability to make distributions are likely to be impacted by economic changes affecting the real estate markets in that area. A shareholder’s investment will be subject to greater risk to the extent that we lack a geographically diversified portfolio of properties.

Our operating results may be negatively affected by potential development and construction delays and the resulting increase in costs and risks.

Developing real estate properties subjects us to uncertainties such as the ability to achieve desired zoning for development, environmental concerns of governmental entities or community groups, ability to control construction costs or to build in conformity with plans, specifications and timetables. Delays in completing construction also could give tenants the right to terminate preconstruction leases for spaces at a newly-developed project and any potential investors we pre-sold our developments to may pull out of such agreements. We may incur additional risks when we make periodic progress payments or advance other costs to third parties prior to completing construction. These and other factors can increase the costs of a project or cause us to lose our investment. In addition, we will be subject to normal lease-up risks relating to newly constructed projects. Furthermore, we must rely upon projections of rental income and expenses and estimates of fair market value upon completing construction when agreeing upon a price to be charged for the property. If our projections are inaccurate, we may not be able to sell a property on favorable terms.

Potential development and construction delays and increases in the prices of building materials due to tariffs or other reasons and resultant increased costs and risks may hinder our operating results and decrease our net income.

Uncertainties associated with the development and construction of real property, including those related to re-zoning land for development, environmental concerns of governmental entities and/or community groups and our builders’ ability to build in conformity with plans, specifications, budgeted costs and timetables. If a builder fails to perform, we may resort to legal action to rescind the construction contract or to compel performance. A builder’s performance may also be affected or delayed by conditions beyond the builder’s control including availability of raw materials and related expenses. Delays in completing construction could also give tenants the right to terminate preconstruction leases. We may incur additional risks when we make periodic progress payments or other advances to builders before they complete construction. These and other factors including price increases in raw materials can result in increased costs of a project or loss of our investment.

Terrorist attacks and other acts of violence or war may affect the markets in which we operate, our operations and our profitability.

We may acquire real estate assets located in areas that are susceptible to attack. These attacks may directly impact the value of our assets through damage, destruction, loss or increased security costs. Although we may obtain terrorism insurance, we may not be able to obtain sufficient coverage to fund any losses we may incur. Risks associated with potential acts of terrorism could sharply increase the premiums we pay for coverage against property and casualty claims. Further, certain losses resulting from these types of events are uninsurable or not insurable at reasonable costs.

More generally, any terrorist attack, other act of violence or war, including armed conflicts, could result in increased volatility in, or damage to, the United States and worldwide financial markets and economy. Any terrorist incident may contribute to increased economic volatility and could adversely affect our tenants’ ability to pay rent on their leases or our ability to borrow money or issue capital stock at acceptable prices.

The costs of complying with environmental laws and other governmental laws and regulations may adversely affect us.

All real property and the operations conducted on real property are subject to federal, state and local laws and regulations relating to environmental protection and human health and safety. These laws and regulations generally govern wastewater discharges, air emissions, the operation and removal of underground and above-ground storage tanks, the use, storage, treatment, transportation and disposal of solid and hazardous materials, and the remediation of contamination associated with disposals. Some of these laws and regulations may impose joint and several liability on tenants, owners or operators for the costs of investigating or remediating contaminated properties, regardless of fault or whether the original disposal was legal. In addition, the presence of these substances, or the failure to properly remediate these substances, may adversely affect our ability to sell or rent the property or to use the property as collateral for future borrowing.

| 10 |

Some of these laws and regulations have been amended to require compliance with new or more stringent standards as of future dates. Compliance with new or more stringent laws or regulations or stricter interpretation of existing laws may require us to spend material amounts of money. Future laws, ordinances or regulations may impose material environmental liability. Further, the condition of our properties may be affected by tenants, the condition of the land, operations in the vicinity of the properties, such as the presence of underground or above-ground storage tanks, or the activities of unrelated third parties. We also are required to comply with various local, state and federal fire, health, life-safety and similar regulations.

ERC Homebuilders 1 operates in a highly competitive market.

ERC Homebuilders 1 plans to operate in a highly competitive market and faces intense competition. Competitors include The Mungo Companies, Bernard Partnership, and T.W. Lewis, which have all been building Build-For-Rent properties for over a decade. Taylor Morrison is now entering the Build-For-Rent market. Big developers like Lennar and others are likely to pursue this market in time. Many of the company’s current and potential competitors have greater resources, longer histories, more customers, and greater brand recognition. Competitors may secure better terms from vendors, adopt more aggressive pricing and devote more resources to technology, infrastructure, fulfillment, and marketing. Further, ERC Homebuilders 1 properties will compete on a local and regional level developers that are active in the company’s initial markets that include NexMetro, AHV Communities, BB Living, Christopher Todd Communities and Camillo Homes. The number and variety of competitors in this business will vary based on the location and setting and is also subject to fluctuating economic factors.

Customer complaints or litigation on behalf of our customers or employees may adversely affect our business, results of operations or financial condition.

The company’s business may be adversely affected by legal or governmental proceedings brought by or on behalf of their customers or employees. Regardless of whether any claims against the company are valid or whether they are liable, claims may be expensive to defend and may divert time and money away from operations and hurt our financial performance. A judgment significantly in excess of their insurance coverage or not covered by insurance could have a material adverse effect on the company’s business, results of operations or financial condition. Also, adverse publicity resulting from these allegations may materially affect the company.

The company’s insurance coverage may not be adequate to cover all possible losses that it could suffer and its insurance costs may increase.

The company has not yet acquired insurance. It may not be able to acquire insurance policies that cover all types of losses and liabilities. Additionally, once the company acquires insurance, there can be no assurance that its insurance will be sufficient to cover the full extent of all of its losses or liabilities for which it is insured. Further, insurance policies expire annually and the company cannot guarantee that it will be able to renew insurance policies on favorable terms, or at all. In addition, if it sustains significant losses or makes significant insurance claims, then its ability to obtain future insurance coverage at commercially reasonable rates could be materially adversely affected. If the company’s insurance coverage is not adequate, or it becomes subject to damages that cannot by law be insured against, such as punitive damages or certain intentional misconduct by their employees, this could adversely affect the company’s financial condition or results of operations.

The company has concentrated its investments single-family homes to be built in smaller groupings, which are subject to numerous risks, including the risk that the values of their investments may decline if there is a prolonged downturn in real estate values.

The company’s operations will consist entirely of large amounts of real estate holdings. Accordingly, the company is subject to the risks associated with holding real estate investments. Changes in the preferences and interests of potential purchasers of properties developed by the company and fluctuations in the value of real estate in the areas where the company has purchased real estate may negatively affect the company’s business.

The company’s real estate holdings will be subject to risks typically associated with investments in real estate. The investment returns available from equity investments in real estate depend in large part on the amount of income earned, expenses incurred and capital appreciation generated by the related properties. In addition, a variety of other factors affect income from properties and real estate values, including governmental regulations, real estate, insurance, zoning, tax and eminent domain laws, interest rate levels and the availability of financing. For example, new or existing real estate zoning or tax laws can make it more expensive and time-consuming to expand, modify or renovate older properties. Under eminent domain laws, governments can take real property. Sometimes this taking is for less compensation than the owner believes the property is worth. Any of these factors could have an adverse impact on our business, financial condition or results of operations.

| 11 |

The illiquidity of real estate may make it difficult for the company to dispose of one or more of our properties or negatively affect its ability to profitably sell such properties and access liquidity.

The company’s business is to sell its real estate assets. Because real estate holdings generally, are relatively illiquid, the company may not be able to dispose of one or more real estate assets on a timely basis. In some circumstances, sales may result in investment losses which could adversely affect the company’s financial condition. The illiquidity of its real estate assets could mean that it is forced to hold on to real estate for longer than planned or indefinitely. Failure to dispose of a real estate asset in a timely fashion, or at all, could adversely affect the company’s business, financial condition and results of operations.

The company’s development and construction of the first Florida Build-For-Rent properties depends on its ability to obtain favorable mortgage financing.

The company intends to secure mortgage financing to fund up to 70% of its first Florida developments and plans to use debt financing to develop and construct subsequent Build-For-Rent properties. There is no guarantee that the company will be able to obtain financing on favorable terms. In the event that the company is unable to obtain such financing it may limit the company’s ability to effectuate its plans and will increase the costs and expenses of the company, thereby negatively impacting its financial prospects.

ERC Homebuilders 1 depends on a small management team and may need to hire more people to be successful.

The success of ERC Homebuilders 1 will greatly depend on the skills, connections and experiences of the executives, Gerald Ellenburg, Ryan Koenig and Mark Morris. ERC Homebuilders 1 has not entered into employment agreements with the aforementioned executives. There is no guarantee that the executives will agree to terms and execute employment agreements that are favorable to the company. Should any of them discontinue working for ERC Homebuilders 1, there is no assurance that the company will continue. Further, there is no assurance that the company will be able to identify, hire and retain the right people for the various key positions.

Key Man Risk.

The company’s founders and key men are serial entrepreneurs. It is likely that some, if not all of the founders and key men, may exit the business within the next three years. In the event one or more of our founders and/or key men exit the business the company may experience following:

| · | financial loss; |

| · | a disruption to the organization's future projects; |

| · | damage to the brand; and |

| · | potentially supporting a competitor. |

The company will require a general manager, who has not yet been hired.

ERC Parent is currently performing an executive search for the general manager and operator of ERC Homebuilders 1. There is no way to be certain that the general manager of ERC Homebuilders 1, once appointed, will be able to execute the same vision as ERC Parent itself. If an appropriate person is not identified and hired, the company will not succeed and since its performance will depend on that person’s performance, it is possible that other ERC subsidiaries will be more successful than the company.

Risks relating to this offering and our shares

The payment of accrued dividends is paid out of the company’s reserved funds for the foreseeable future.

As soon as the company receives proceeds from this offering and it is legally permissible, the company intends to pay dividends to investors. The dividend will initially be paid to investors out of the company’s reserved funds, as opposed to its revenues. Payment of the dividends and the establishment of the reserve fund will reduce the capital the company has to develop and begin marketing its single-family Build-For-Rent properties. These reserved funds will be held in a segregated account money market account located at Fifth Third Bank, Cincinnati, OH. Most, if not all, of the reserved funds in the dividend reserve account will be the proceeds from this offering. (See “Use of Proceeds”). It is not certain when, if at all, the company will be able to make dividends payments to investors out of the company’s revenues.

| 12 |

If we pay distributions from sources other than cash flow from operations, we will have less capital available for investments and your overall return is likely to be reduced.

Although our distribution policy is to use our cash flow from operations to make distributions to shareholders, our operating agreement permits us to pay distributions from any source, including offering proceeds, borrowings, or sales of assets. We have not placed a cap on the use of proceeds to fund distributions. Until the proceeds from this offering are fully invested and from time to time during the operational stage, we may not generate sufficient cash flow from operations to fund distributions. If we pay distributions from sources other than our cash flow from operations, we will have less capital available to make investments, and your overall return is likely be reduced.

Distributions will be only made if permitted under Delaware law, which is subject to change, and in the sole discretion of the board of directors.

Pursuant to section 170 of the Delaware General Corporation Law (“Delaware Law”), dividends may be paid out of “surplus” even in the absence of profits. Under section 154, “surplus” may be defined by the board of directors, in their sole discretion, but generally may not be less than the par value of the shares issued. Accordingly, most of the proceeds of this offering may be considered surplus. However, Delaware Law is subject to change, and the company cannot guarantee that dividend payments will always be permitted under Delaware Law.

The tax treatment of dividends may vary and distributions to shareholders may be taxed as capital gains.

The distributions made pursuant to the Preferred Stock dividend provisions will be taxable as dividends to shareholders only to the extent of current and accumulated earnings and profits. To the extent the company does not have current and accumulated earnings and profits, the distributions will be treated as a non-taxable return of capital to the extent of the shareholder’s adjusted basis. If distributions still exceed the amount of adjusted basis, such excess would be considered as capital gains income to the shareholder, who will generally be subject to federal (and possibly State) income tax on such gains at a rate that depends upon the shareholder’s holding period with respect to the shares in question, among other factors. Since the tax treatment of any distributions may vary according to the financial performance of the company, as well as the particular circumstances of the investor, investors should consult their own tax advisers, and should further not assume that the distributions will be subject to the same tax treatment from year to year.

The company is responsible for certain administrative burdens relating to taxation.

Federal law required that the company report annually all distributions to shareholders on a Form 1099-DIV. The company is responsible for ensuring that the extent to which such distributions constitute a distribution of earnings and profits is correctly identified on form 1099-DIV. This reporting requirement adds to the administrative burdens of the company.

The Offering price has been arbitrarily set by the company.

ERC Homebuilders 1 has set the price of its Preferred Stock at $6.00 per share. Valuations for companies at ERC Homebuilders 1 stage are purely speculative. The company’s valuation has not been validated by any independent third party and may fall precipitously. It is a question of whether you, the investor, are willing to pay this price for a percentage ownership of a start-up company. You should not invest if you disagree with this valuation.

There is no minimum amount set as a condition to closing this offering.

Because this is a “best efforts” offering with no minimum, the company will have access to any funds tendered. This might mean that any investment made could be the only investment in this offering, leaving the company without adequate capital to pursue its business plan or even to cover the expenses of this offering.

| 13 |

The officers of ERC Homebuilders 1 control the company and the company does not currently have any independent directors.

ERC Parent is currently the company’s controlling shareholder. Moreover, the company’s executive officers and directors, through their ownership in ERC Parent, are currently ERC Homebuilders 1 controlling shareholders. As holders of the Class B Common Stock which gives ERC Parent 5 votes per share, as opposed to 1 vote per share for holders of Class A Common Stock and Class A Preferred Stock, ERC Parent will continue to hold a majority of the voting power of all the company’s equity stock and therefore control the board at the conclusion of this offering. Even if ERC Parent were to own as little as 16.7% of the equity securities of the company, ERC Parent would still control a majority of the voting stock. This could lead to unintentional subjectivity in matters of corporate governance, especially in matters of compensation and related party transactions. The company does not benefit from the advantages of having independent directors, including bringing an outside perspective on strategy and control, adding new skills and knowledge that may not be available within ERC Homebuilders 1, and having extra checks and balances to prevent fraud and produce reliable financial reports.

The exclusive forum provision in the company’s Amended and Restated Certificate of Incorporation may have the effect of limiting an investor’s ability to bring legal action against the company and could limit an investor’s ability to obtain a favorable judicial forum for disputes.

Section VII of the company’s Amended and Restated Certificate of Incorporation contain exclusive forum provisions for certain lawsuits, see “Securities Being Offered – All Classes of Stock – Forum Selection Provisions.” Further, Section 6 of the subscription agreement for this offering includes exclusive forum provisions for certain lawsuits pursuant to the subscription agreement; see “Securities Being Offered – All Classes of Stock – Forum Selection Provisions.” The forum for these lawsuits will be the Court of Chancery in the State of Delaware. None of the forum selections provisions will be applicable to lawsuits arising from the federal securities laws. These provisions may have the effect of limiting the ability of investors to bring a legal claim against us due to geographic limitations. There is also the possibility that the exclusive forum provisions may discourage stockholder lawsuits, or limit stockholders’ ability to bring a claim in a judicial forum that it finds favorable for disputes with us and our officers and directors. Alternatively, if a court were to find this exclusive forum provision inapplicable to, or unenforceable in respect of, one or more of the specified types of actions or proceedings, the company may incur additional costs associated with resolving such matters in other jurisdictions, which could adversely affect its business and financial condition.

Investors in this offering may not be entitled to a jury trial with respect to claims arising under the subscription agreement and claims where the forum selection provision is applicable, which could result in less favorable outcomes to the plaintiff(s) in any such action.

Investors in this offering will be bound by the subscription agreement, which includes a provision under which investors waive the right to a jury trial of any claim they may have against the company arising out of or relating to the subscription agreement, including any claim under the federal securities laws. Further, the Court of Chancery in Delaware is a non-jury trial court and therefore those claims will not be adjudicated by a jury. See “Securities Being Offered – All Classes of Stock – Jury Trial Waiver.”

If the company opposed a jury trial demand based on the waiver, a court would determine whether the waiver was enforceable based on the facts and circumstances of that case in accordance with the applicable state and federal law. To the company’s knowledge, the enforceability of a contractual pre-dispute jury trial waiver in connection with claims arising under the federal securities laws has not been finally adjudicated by a federal court. However, the company believes that a contractual pre-dispute jury trial waiver provision is generally enforceable, including under the laws of the State of New York, which governs the subscription agreement, in the Court of Chancery in the State of Delaware. In determining whether to enforce a contractual pre-dispute jury trial waiver provision, courts will generally consider whether the visibility of the jury trial waiver provision within the agreement is sufficiently prominent such that a party knowingly, intelligently and voluntarily waived the right to a jury trial. The company believes that this is the case with respect to the subscription agreement. Investors should consult legal counsel regarding the jury waiver provision before entering into the subscription agreement.

If an investor brings a claim against the company in connection with matters arising under the subscription agreement, including claims under federal securities laws, an investor may not be entitled to a jury trial with respect to those claims, which may have the effect of limiting and discouraging lawsuits against the company. If a lawsuit is brought against the company under the subscription agreement, it may be heard only by a judge or justice of the applicable trial court, which would be conducted according to different civil procedures and may result in different outcomes than a trial by jury would have had, including results that could be less favorable to the plaintiff(s) in such an action.

Nevertheless, if this jury trial waiver provision is not permitted by applicable law, an action could proceed under the terms of the subscription agreement with a jury trial. No condition, stipulation or provision of the subscription agreement serves as a waiver by any holder of common shares or by us of compliance with any substantive provision of the federal securities laws and the rules and regulations promulgated under those laws.

In addition, when the shares are transferred, the transferee is required to agree to all the same conditions, obligations and restrictions applicable to the shares or to the transferor with regard to ownership of the shares that were in effect immediately prior to the transfer of the shares of Preferred Stock, including but not limited to the subscription agreement.

| 14 |

There is no current market for ERC Homebuilders 1’s shares.

There is no formal marketplace for the resale of our securities. Shares of the company’s Preferred Stock may eventually be traded to the extent any demand and/or trading platform(s) exists. However, there is no guarantee there will be demand for the shares, or a trading platform that allows you to sell them. The company does not have plans to apply for or otherwise seek trading or quotation of its Preferred Stock on an over-the-counter market. It is also hard to predict if the company will ever be acquired by a bigger company. Investors should assume that they may not be able to liquidate their investment or pledge their shares as collateral for some time.

Risks related to certain conflicts of interest

There are conflicts of interest between the company, its management and their affiliates.

ERC Parent is the parent company of ERC Homebuilders 1 and currently holds all of the issued Common Stock of ERC Homebuilders 1. ERC Parent is also affiliated with ERC Homebuilders 2, KGEM Golf, Inc. (“KGEM”) and its six subsidiaries. , and many if not all of the executives are the same for ERC Parent, ERC Homebuilders 2, KGEM, and KGEM’s subsidiaries. Therefore, it is likely that conflicts of interest will arise between the affiliates. Conflicts of interest could include, but are not limited to the following:

| · | use of time, |

| · | use of human capital, and |

| · | competition regarding the acquisition of properties and other assets. |

The interests of ERC Homebuilders 1, ERC Parent and the company’s other affiliates may conflict with your interests.

The company’s Amended and Restated Certificate of Incorporation, bylaws and Delaware law provide company management with broad powers and authority that could result in one or more conflicts of interest between your interests and those of the officers and directors of ERC Homebuilders 1, ERC Parent, and the company’s other affiliates. This risk is increased by the affiliated entities being controlled by ERC Parent who currently owns all of the company’s Common Stock and all our officers and directors currently have an interest in ERC Parent, through ownership, as an officer or director in ERC Parent contractually or any combination thereof. Potential conflicts of interest include, but are not limited to, the following:

| ● | ERC Parent and the company’s other affiliates will not be required to disgorge any profits or fees or other compensation they may receive from any other business they own separate from the company, and you will not be entitled to receive or share in any of the profits, return, fees or compensation from any other business owned and operated by the management and their affiliates for their own benefit. |

| ● | The company may engage ERC Parent, or other companies affiliated with ERC Homebuilders 1 to perform services, and determination for the terms of those services will not be conducted at arms’ length negotiations; and |

| ● | The company’s officers and directors are not required to devote all of their time and efforts to the affairs of the company. |

There are conflicts of interest between the company and some of the members of the Board of Directors.

Rod Turner, the CEO of the online platform on which the company is offering shares, is also a member of the Board of Directors. It is likely that conflicts of interest will arise between the company and the board member. Conflicts of interest include, but are not limited to the following:

| · | Determining whether something is in the best interest of the company or the online platform on which the company is listing the Preferred Stock. |

| · | Whether to keep the offering open or to close it. |

| · | Use of time. |

| · | Payment to the online platform. |

Loans issued by ERC Parent to ERC Homebuilders 1 may not be made at arm’s length.

ERC Parent may make various loans to ERC Homebuilders 1. These transactions may not be at arm’s length and therefore there is no way to assure third parties that ERC Parent and ERC Homebuilders 1 will be acting in their own self-interest and not subject to pressure or duress from the other party.

| 15 |

ERC Parent, ERC Homebuilders 1 and ERC Homebuilders 2 intend to share some services.

ERC Parent, ERC Homebuilders 1 and ERC Homebuilders 2 will share the following services:

| · | licensing for the use of the name and brand identity, and |

| · | the services of Manhattan Street Capital. |

| · | Participating lease agreements as described in “Support from ERC Parent.” |

Internal transactions incorporating products and services, fee sharing, cost allocations, and financing activities can create inefficiency, financial exposures and reporting risk. This arrangement could result in potential actual or perceived conflicts of interest.

| 16 |

Dilution means a reduction in value, control or earnings of the shares the investor owns.

Immediate dilution

An early-stage company typically sells its shares (or grants options over its shares) to its founders and early employees at a very low cash cost, because they are, in effect, putting their “sweat equity” into the company. When the company seeks cash investments from outside investors, like you, the new investors typically pay a much larger sum for their shares than the founders or earlier investors, which means that the cash value of your stake is diluted because all the shares are worth the same amount, and you paid more than earlier investors for your shares. If you invest in our Preferred Stock, your interest will be diluted immediately to the extent of the difference between the offering price per share of our Preferred Stock and the pro forma net tangible book value per share of our Preferred Stock after this offering.

As of December 31, 2018, the net tangible book value of the Company was ($157,375). Based on the number of shares of Common Stock issued and outstanding as of the date of the offering (16,000,000 shares) that equates to a net tangible book value of approximately ($0.0098) per share of Common Stock on a pro forma basis. Net tangible book value per share consists of stockholders’ aggregate deficit divided by the total number of shares of Common Stock outstanding. Without giving effect to any changes in such net tangible book value after December 31, 2018, other than to give effect to the sale of 8,333,333 shares of Preferred Stock being offered by the company in this offering for the net subscription amount of $44,500,000 the pro forma net tangible book value, assuming full subscription, would be $44,342,625. Based on the total number of shares of Common and Preferred Stock that would be outstanding assuming full subscription (24,333,333), that equates to approximately $1.8223 of tangible net book value per share.

Thus, if the offering is fully subscribed, the net tangible book value per share of Common Stock owned by our current stockholders will have immediately increased by approximately $1.8321 without any additional investment on their behalf and the net tangible book value per Share for new investors will be immediately diluted by $4.1777 per share. These calculations do not include the costs of the offering, and such expenses will cause further dilution.

| Offering price per share of Preferred Stock* | $ | 6.00 | ||

| Net Tangible Book Value per share of Preferred Stock before the offering (based on 16,000,000 shares) | $ | (0.0098 | ) | |

| Increase in Net Tangible Book Value per Share Attributable to Shares Offered in the offering (based on 8,333,333 shares) | $ | 1.8321 | ||

| Net Tangible Book Value per Share after the offering (based on 24,333,333 shares) | $ | 1.8223 | ||

| Dilution of Net Tangible Book Value per Share to Purchasers in this offering | $ | 4.1777 |

*before deduction of offering expenses.

Future dilution

Another important way of looking at dilution is the dilution that happens due to future actions by the company. The investor’s stake in a company could be diluted due to the company issuing additional shares. In other words, when the company issues more shares, the percentage of the company that you own will go down, even though the value of the company may go up. You will own a smaller piece of a larger company. This increase in number of shares outstanding could result from a stock offering (such as an initial public offering, another crowdfunding round, a venture capital round, angel investment), employees exercising stock options, or by conversion of certain instruments (e.g. convertible bonds, preferred shares or warrants) into stock.

If the company decides to issue more shares, an investor could experience value dilution, with each share being worth less than before, and control dilution, with the total percentage an investor owns being less than before. There may also be earnings dilution, with a reduction in the amount earned per share (though this typically occurs only if the company offers dividends, and most early stage companies are unlikely to offer dividends, preferring to invest any earnings into the company).

| 17 |

The type of dilution that hurts early-stage investors most often occurs when the company sells more shares in a “down round,” meaning at a lower valuation than in earlier offerings. An example of how this might occur is as follows (numbers are for illustrative purposes only):

| · | In June 2014 Jane invests $20,000 for shares that represent 2% of a company valued at $1 million. |

| · | In December, the company is doing very well and sells $5 million in shares to venture capitalists on a valuation (before the new investment) of $10 million. Jane now owns only 1.3% of the company but her stake is worth $200,000. |

| · | In June 2015, the company has run into serious problems and in order to stay afloat it raises $1 million at a valuation of only $2 million (the “down round”). Jane now owns only 0.89% of the company and her stake is worth only $26,660. |

This type of dilution might also happen upon conversion of convertible notes into shares. Typically, the terms of convertible notes issued by early-stage companies provide that in the event of another round of financing, the holders of the convertible notes get to convert their notes into equity at a “discount” to the price paid by the new investors, i.e., they get more shares than the new investors would for the same price. Additionally, convertible notes may have a “price cap” on the conversion price, which effectively acts as a share price ceiling. Either way, the holders of the convertible notes get more shares for their money than new investors. In the event that the financing is a “down round” the holders of the convertible notes will dilute existing equity holders, and even more than the new investors do, because they get more shares for their money. Investors should pay careful attention to number of convertible notes that the company has issued (and may issue in the future, and the terms of those notes.

If you are making an investment expecting to own a certain percentage of the company or expecting each share to hold a certain amount of value, it’s important to realize how the value of those shares can decrease by actions taken by the company. Dilution can make drastic changes to the value of each share, ownership percentage, voting control, and earnings per share.

| 18 |

PLAN OF DISTRIBUTION AND SELLING SECURITYHOLDERS

Plan of Distribution

ERC Homebuilders 1, Inc. is offering a maximum of 8,333,333 shares of Preferred Stock on a “best efforts” basis.

The cash price per share of Preferred Stock is $6.

The company intends to market the shares in this offering both through online and offline means. Online marketing may take the form of contacting potential investors through electronic media and posting our Offering Circular or “testing the waters” materials on an online investment platform.

The offering will terminate at the earliest of: (1) the date at which the maximum offering amount has been sold, (2) the date which is one year from this offering being qualified by the Commission, and (3) the date at which the offering is earlier terminated by ERC Homebuilders 1, Inc. in its sole discretion.

The company may undertake one or more closings on an ongoing basis. After each closing, funds tendered by investors will be available to the company. After the initial closing of this offering, the company expects to hold closings on at least a monthly basis.

The company is offering its securities in all states.

The company has engaged Sageworks Capital, LLC (“Sageworks”) a broker-dealer registered with the SEC and a member of FINRA, to perform the following administrative and technology related functions in connection with this offering, but not for underwriting or placement agent services:

| · | Review investor information, including KYC (“Know Your Customer”) data, AML (“Anti Money Laundering”) and other compliance background checks, and provide a recommendation to the company whether or not to accept investor as a customer. |

| · | Review each investors subscription agreement to confirm such investors participation in the offering, and provide a determination to the company whether or not to accept the use of the subscription agreement for the investors participation. |

| · | Contact and/or notify the company, if needed, to gather additional information or clarification on an investor; |

| · | Not provide any investment advice nor any investment recommendations to any investor. |

| · | Keep investor details and data confidential and not disclose to any third-party except as required by regulators or pursuant to the terms of the agreement (e.g. as needed for AML and background checks). |

| · | Coordinate with third party providers to ensure adequate review and compliance. |

As compensation for the services listed above, the company has agreed to pay Sageworks $18,000 in one-time set up fees, consisting of a $10,000 agreement fee and approximately $8,000 for fees to be paid to FINRA, plus a commission equal to 1% of the amount raised in the offering to support the offering once the SEC has qualified the Offering Statement and the offering commences. Assuming that the offering is open for 12 months, the company estimates that total fees due to pay Sageworks would be $518,000 for a fully-subscribed offering. These assumptions were used in estimating the fees due in the “Use of Proceeds.”

No Minimum Offering Amount

The shares being offered will be issued in one or more closings. No minimum number of shares must be sold before a closing can occur; however, investors may only purchase shares in minimum increments of $500. Potential investors should be aware that there can be no assurance that any other funds will be invested in this offering other than their own funds.

No Selling Shareholders

No securities are being sold for the account of security holders; all net proceeds of this offering will go to ERC Homebuilders 1, Inc.

The Online Platform

The company will pay FundAthena, Inc., d/b/a Manhattan Street Capital (“Manhattan Street Capital” or “MSC” as applicable) for its services in hosting the offering of the shares on its online platform.

| 19 |

Further, ERC Parent has entered into a Consulting Agreement with MSC effective July 15, 2018 (the “Consulting Agreement”), which includes consulting services and technology services, see “Plan of Distribution and Selling Securityholders – The Online Platform.” ERC Parent, or the company as applicable, will pay MSC the following:

| · | A technology and administration fee of $25 per investor, in cash, paid by the company when each investor deposits funds into the escrow account. |

| · | A cashless 10 year warrant to purchase 100 shares of ERC Parent common stock for $0.25 per share, per investment into the escrow account, in each Operating Subsidiary Regulation A offering. |

| o | The warrant calculations shall be capped at a maximum of 30,000 investors, aggregated from the 2 contemplated Regulation A offerings of the two Operating Subsidiaries. Which results in warrants to purchase a maximum of 3,000,000 shares of ERC Parent common stock; |

| · | AML check fees between $2 and $6 per investor. AML fees will be dependent on the location of the investor. |

| · | A technology license fee of $300 per month. |

| · | Any applicable fees for fund transfers (ACH $2, debit card fees of $0.35 + 3% as charged by debit card processor, check $5, wire $15 or $35 for international fund transfers). |

Pursuant to the Consulting Agreement, on July 15, 2018, ERC Parent has paid $135,000 ($15,000 per month for 9 months) in cash. ERC Parent will pay $15,000 per month in excess of 9 months. Prior to the launch of this Offering, ERC Parent will deliver to MSC cashless 10 year warrants for 540,000 shares of ERC Parent common stock with an exercise price of $0.25 per share.

ERC Homebuilders 1 will reimburse ERC Parent for its portion of the fee to MSC in accordance with the Management Services Agreement. All fees are due to MSC regardless of whether investors are rejected after AML checks or the success of the offering.

For additional information please see “Interests of Management and Others in Certain Transactions”.

Manhattan Street Capital does not directly solicit or communicate with investors with respect to offerings posted on its site, although it does advertise the existence of its platform, which may include identifying issuers listed on the platform. Our Offering Circular will be furnished to prospective investors in this offering via download 24 hours a day, 7 days a week on the www.manhattanstreetcapital.com website.

Investors’ Tender of Funds

After the Offering Statement has been qualified by the Securities and Exchange Commission (the “SEC”), the company will accept tenders of funds to purchase whole shares and fractional shares. Prospective investors who submitted non-binding indications of interest during the “test the waters” period will receive an automated message from us indicating that the offering is open for investment. We will conduct multiple closings on investments (so not all investors will receive their shares on the same date). Each time the company accepts funds transferred from the Escrow Agent is defined as a “Closing." The funds tendered by potential investors will be held by our escrow agent, to be determined (the “Escrow Agent”) and will be transferred to us at each Closing. The escrow agreement can be found in Exhibit 8 to the Offering Statement of which this Offering Circular is a part.

Process of Subscribing

You will be required to complete a subscription agreement in order to invest. The subscription agreement includes a representation by the investor to the effect that, if you are not an “accredited investor” as defined under securities law, you are investing an amount that does not exceed the greater of 10% of your annual income or 10% of your net worth (excluding your principal residence).

If you decide to subscribe for the Preferred Stock in this offering, you should complete the following steps:

| 1. | Go to www.manhattanstreetcapital.com/ERC1 and click on the "Invest Now" button; |

| 2. | Complete the online investment form; |

| 3. | Deliver funds directly by check, wire, debit card, or electronic funds transfer via ACH to the specified account or deliver evidence of cancellation of debt; |

| 4. | Once funds or documentation are received an automated AML check will be performed to verify the identity and status of the investor; |

| 5. | Once AML is verified, investor will electronically receive, review, execute and deliver to us a Subscription Agreement. |

Any potential investor will have ample time to review the subscription agreement, along with their counsel, prior to making any final investment decision. Sageworks will review all subscription agreements completed by the investor. After Sageworks has completed its review of a subscription agreement for an investment in the company, the funds may be released by the escrow agent.

| 20 |

If the subscription agreement is not complete or there is other missing or incomplete information, the funds will not be released until the investor provides all required information. In the case of a debit card payment, provided the payment is approved, Sageworks will have up to three days to ensure all the documentation is complete. Sageworks will generally review all subscription agreements on the same day, but not later than the day after the submission of the subscription agreement.

All funds tendered (by check, wire, debit card, or electronic funds transfer via ACH to the specified account or deliver evidence of cancellation of debt) by investors will be deposited into an escrow account at the Escrow Agent for the benefit of the company. All funds received by wire transfer will be made available immediately while funds transferred by ACH will be restricted for a minimum of three days to clear the banking system prior to deposit into an account at the Escrow Agent.