Post-Qualification Offering Circular Amendment No. 1

File No. File No. 024-10896

An offering statement pursuant to Regulation A relating to these securities has been filed with the Securities and Exchange Commission. Information contained in this Preliminary Offering Circular is subject to completion or amendment. These securities may not be sold nor may offers to buy be accepted before the offering statement filed with the Commission is qualified. This Preliminary Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy nor may there be any sales of these securities in any state in which such offer, solicitation or sale would be unlawful before registration or qualification under the laws of any such state. We may elect to satisfy our obligation to deliver a Final Offering Circular by sending you a notice within two business days after the completion of our sale to you that contains the URL where the Final Offering Circular or the offering statement in which such Final Offering Circular was filed may be obtained.

PRELIMINARY OFFERING CIRCULAR

SUBJECT TO COMPLETION; DATED APRIL 17, 2019

| MY RACEHORSE CA LLC |

250 W. 1st Street, Suite 256

Claremont, CA 91711

(909) 740-9175

www.myracehorse.com

| Series Membership Interests Overview | |||||

| Number of Shares | Price to Public | Underwriting Discounts and Commissions(1) | Proceeds to Issuer | ||

| Series Palace Foal | Per Unit | 1 | $120.00 | $0.00 | $120.00 |

| Total Maximum | 510 | $61,200.00 | $0.00 | $61,200.00 | |

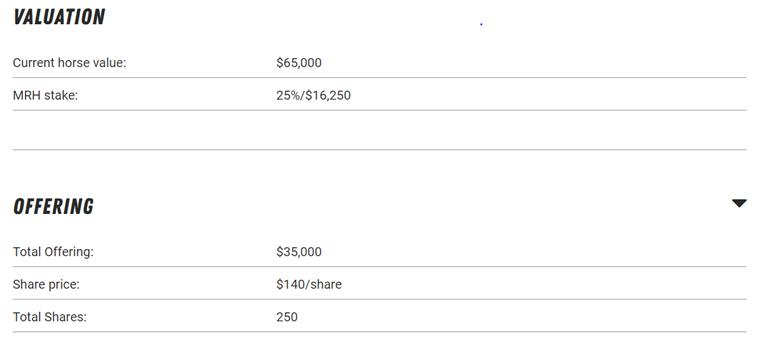

| Series De Mystique ‘17 | Per Unit | 1 | $140.00 | $0.00 | $140.00 |

| Total Maximum | 250 | $35,000.00 | $0.00 | $35,000.00 | |

(1) No underwriter has been engaged in connection with the Offering. The securities being offered hereby will only be offered by us and persons associated with us, in reliance on the exemption from registration contained in Rule 3a4-1 of the Securities Exchange Act of 1934. We intend to distribute all offerings of membership interests in any series of the Company principally through the MyRacehorse™ Platform as described in greater detail under “Plan of Distribution and Subscription Procedure.”

My Racehorse CA LLC, a Nevada series limited liability company (“we,” “us,” “our,” “MRH” or the “Company”) is offering, on a best efforts basis, up to the following amount of membership interests of each of the following series of the Company (the “Maximum”) without any minimum target:

| · | Up to 510

membership interests in the Series Palace Foal (the “Series Palace Foal Interests,” the offering

of which is described as the “Series Palace Foal Offering”); and |

| · | Up to 250 membership interests in the Series De Mystique ‘17

(the “Series De Mystique ‘17 Interests,”

the offering of which is described as the “Series De Mystique ‘17 Offering”). |

All of the series of the Company offered hereunder may collectively be referred to herein as the “Series” and each, individually, as a “Series”. The interests of all series described above may collectively be referred to herein as the “Interests” and each, individually, as an “Interest” and the offerings of the Interests may collectively be referred to herein as the “Offerings” and each, individually, as an “Offering”.

An Offering Circular, presented in Offering Circular format, was filed with the Securities and Exchange Commission with respect to the Series Palace Foal Offering and was qualified by the Commission on February 22, 2019 (the “Original Offering Circular”). This Post-Effective Amendment No. 1 to the Original Offering Circular describes the Series Palace Foal Offering (with respect to the Series Palace Foal Interests unsubscribed as of the qualification date) and also describes the Series De Mystique ‘17 Offering, (the “Offering Circular”).

| · | Sale of the Series Palace Foal Interests are expected to begin on or before May 1, 2019 to a maximum of 2,000 qualified purchasers (no more than 500 of which may be non-“accredited investors”). |

| · | Sale of the Series De Mystique ’17 Interests will begin upon qualification of the Offering Circular to a maximum of 2,000 qualified purchasers per Series (no more than 500 of which may be non-“accredited investors”). |

A purchaser of the Interests shall be deemed an “Investor” or “Interest Holder.” There will be separate closings with respect to each Offering. The Company may undertake one or more closings on a rolling basis with respect to each Offering (each, a “Closing”). After each Closing, funds tendered by Investors will be available to the Company. Because the Offering is being made on a best efforts basis and without a minimum offering amount, the Company may close the offering at any level of proceeds raised. Each such Offering shall be terminated on the earlier of (i) the date subscriptions for the Maximum Interests of such Series have been accepted, (ii) a date determined by the Manager in its sole discretion, or (iii) the date which is one year from the date this Offering Circular is qualified by the Commission which period may be extended by an additional six months by the Manager in its sole discretion.

No securities are being offered by existing security holders. Each Offering is being conducted under Regulation A (17 CFR 230.251 et. seq.) and the information contained herein is being presented in Offering Circular format. See “Plan of Distribution and Subscription Procedure” and “Description of Interests Offered” for additional information.

GENERALLY, NO SALE MAY BE MADE TO YOU IN ANY OFFERING IF THE AGGREGATE PURCHASE PRICE YOU PAY IS MORE THAN 10% OF THE GREATER OF YOUR ANNUAL INCOME OR NET WORTH. DIFFERENT RULES APPLY TO ACCREDITED INVESTORS AND NON-NATURAL PERSONS. BEFORE MAKING ANY REPRESENTATION THAT YOUR INVESTMENT DOES NOT EXCEED APPLICABLE THRESHOLDS, WE ENCOURAGE YOU TO REVIEW RULE 251(d)(2)(i)(C) OF REGULATION A. FOR GENERAL INFORMATION ON INVESTING, WE ENCOURAGE YOU TO REFER TO WWW.INVESTOR.GOV.

The United States Securities and Exchange Commission does not pass upon the merits of or give its approval to any securities offered or the terms of the offering, nor does it pass upon the accuracy or completeness of any offering circular or other solicitation materials. These securities are offered pursuant to an exemption from registration with the Commission; however, the Commission has not made an independent determination that the securities offered are exempt from registration. This Preliminary Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy, nor may there be any sales of these securities in, any state in which such offer, solicitation or sale would be unlawful before registration or qualification of the offer and sale under the laws of such state.

An investment in the Interests involves a high degree of risk. See “Risk Factors” on Page 7 for a description of some of the risks that should be considered before investing in the Interests.

MY RACEHORSE CA LLC

| i |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

The information contained in this Offering Circular includes some statements that are not historical and that are considered “forward-looking statements.” Such forward-looking statements include, but are not limited to, statements regarding our development plans for our business; our strategies and business outlook; anticipated development of the Company, the Manager, each series of the Company and the MyRacehorse™ Platform (defined below); and various other matters (including contingent liabilities and obligations and changes in accounting policies, standards and interpretations). These forward-looking statements express the Manager’s expectations, hopes, beliefs, and intentions regarding the future. In addition, without limiting the foregoing, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipates”, “believes”, “continue”, “could”, “estimates”, “expects”, “intends”, “may”, “might”, “plans”, “possible”, “potential”, “predicts”, “projects”, “seeks”, “should”, “will”, “would” and similar expressions and variations, or comparable terminology, or the negatives of any of the foregoing, may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements contained in this Offering Circular are based on current expectations and beliefs concerning future developments that are difficult to predict. Neither the Company nor the Manager can guarantee future performance, or that future developments affecting the Company, the Manager or the MyRacehorse™ Platform will be as currently anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements.

All forward-looking statements attributable to us are expressly qualified in their entirety by these risks and uncertainties. These risks and uncertainties, along with others, are also described below under the heading “Risk Factors.” Should one or more of these risks or uncertainties materialize, or should any of the parties’ assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. You should not place undue reliance on any forward-looking statements and should not make an investment decision based solely on these forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

| 1 |

The following summary is qualified in its entirety by the more detailed information appearing elsewhere herein and in the Exhibits hereto. You should read the entire Offering Circular and carefully consider, among other things, the matters set forth in the section captioned “Risk Factors.” You are encouraged to seek the advice of your attorney, tax consultant, and business advisor with respect to the legal, tax, and business aspects of an investment in the Interests. All references in this Offering Circular to “$” or “dollars” are to United States dollars.

| The Company: | The Company is My Racehorse CA LLC, a Nevada series limited liability company formed on December 27, 2016. |

| Underlying Asset: |

The respective Series will hold the following respective assets:

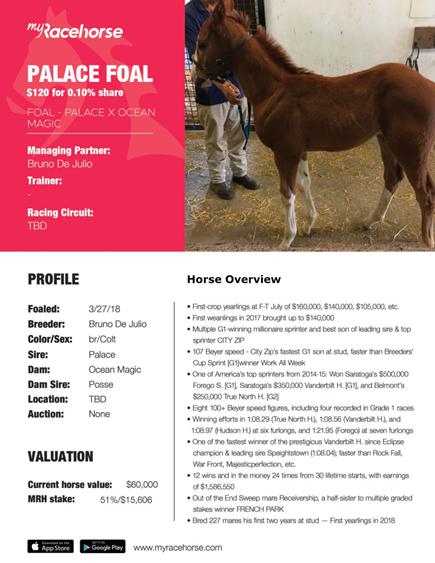

· The Series Palace foal will hold a fifty-one percent (51%) interest in a 2018 foal named Palace Foal (“Palace Foal”).

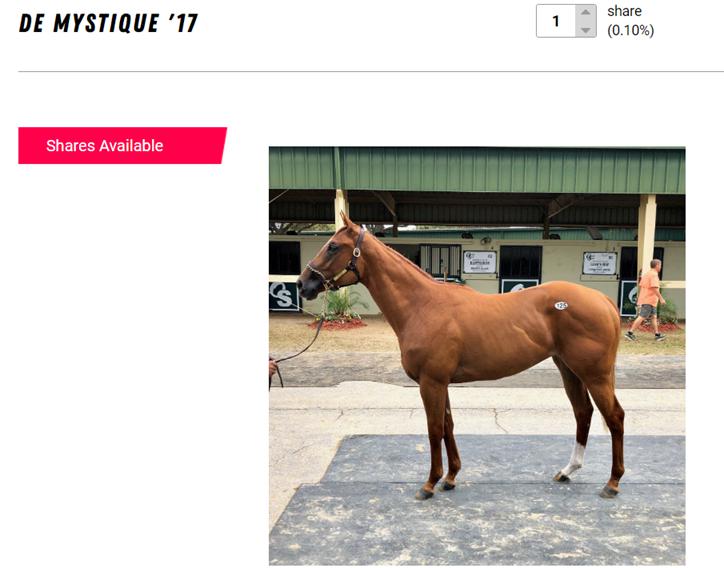

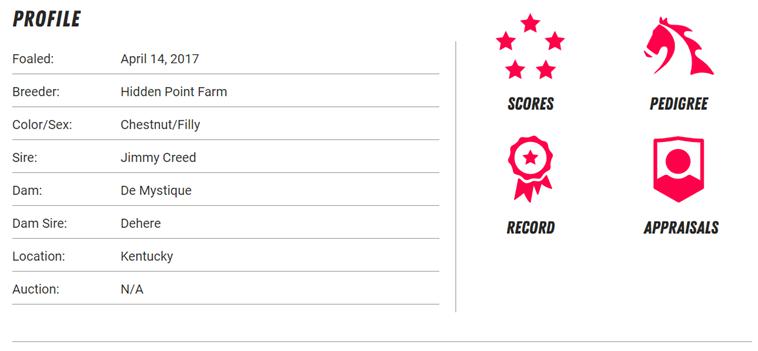

· The Series De Mystique ’17 will hold a twenty-five percent (25%) interest in a 2017 filly named De Mystique ’17 (“De Mystique ’17”).

The assets of all Series described above may collectively be referred to herein as the “Underlying Assets” and each, individually, as an “Underlying Asset.”

It is not anticipated that any of the above Series would own any assets other than said interest in such Underlying Asset, plus cash reserves for maintenance, training, insurance and other expenses pertaining to the Series and amounts earned from the monetization of such Underlying Asset. See “Description of Palace Foal,” and “Description of De Mystique ’17” for further details. |

| Securities offered: | Investors will acquire membership interests in a Series of the Company, each of which is intended to be a separate series of the Company for purposes of assets and liabilities. It is intended that owners of interest in a Series will only have assets, liabilities, profits and losses pertaining to the specific Underlying Assets owned by that Series. For example, an owner of interests in Series Palace Foal will only have an interest in the assets, liabilities, profits and losses pertaining to the Series Palace Foal and its related operations and not as it relates to Series De Mystique ‘17. See the “Description of Interests Offered” section for further details. The Interests will be non-voting except with respect to certain matters set forth in the Amended and Restated Series Limited Liability Company Agreement of the Company (the “Operating Agreement”). The purchase of membership interests in a Series of the Company is an investment only in that Series (and with respect to that Series’ Underlying Asset) and not an investment in the Company as a whole. |

| Investors: | Each Investor must be a “qualified purchaser.” See “Plan of Distribution and Subscription Procedure – Investor Suitability Standards” for further details. The Manager may, in its sole discretion, decline to admit any prospective Investor, or accept only a portion of such Investor’s subscription, regardless of whether such person is a “qualified purchaser”. |

| 2 |

| Manager: |

Experiential Squared, Inc., a Delaware corporation, will serve as the manager of the Company and of each Series (the “Manager”) pursuant to that certain Management Services Agreement (the “Management Agreement”). Experiential Squared, Inc., also owns and operates a mobile app-based investment platform called MyRacehorse™ (the MyRacehorse™ platform and any successor platform used by the Company for the offer and sale of interests, the “MyRacehorse™ Platform”), which is licensed to the Company pursuant to the terms of the Management Agreement, through which the Interests are sold.

The Manager and/or its affiliates may, from time to time, purchase Interests at their discretion on the same terms and conditions as the Investors. The Company, the Manager, its affiliates and/or third parties may also (1) acquire horses that are listed on MyRacehorse.com pursuant to a promissory note between the Series and lender or (2) have the Series acquire the horses upon close of the respective offering. In many instances, said lender will have a right, prior to completion of the Offering, to participate in pre-closing dividends from revenue generated by its interest in the Underlying Asset and the right to convert into the unsold portion of the offering prior to being fully funded.

The Series Palace Foal being offered hereunder was acquired initially by the Chief Executive Officer of our Manager pursuant to such a promissory note. A copy of the Profit Participation Convertible Promissory Note for Series Palace Foal is attached hereto as Exhibit 6.3.

The Series De Mystique ‘17 being offered hereunder was acquired initially by the Manager pursuant to such a promissory note. A copy of the Profit Participation Convertible Promissory Note for Series De Mystique ‘17 is attached hereto as Exhibit 6.45. |

| Price per Series Interest: |

The price per Series Palace Foal Interest is $120.00.

The price per Series De Mystique ‘17 Interest is $140.00. |

| Minimum Interest purchase: | The minimum subscription by an Investor is 1 Interest in a Series. The Purchase Price will be payable in cash in United States Dollars at the time of subscription. |

| Offering size: |

There is no minimum offering amount for the sale of Interests in each Offering.

The Company may offer and sell a maximum of 510 Series Palace Foal Interests pursuant to this Offering, for a maximum aggregate offering amount of $61,200.

The Company may offer and sell a maximum of 250 Series De Mystique ‘17 Interests pursuant to this Offering, for a maximum aggregate offering amount of $35,000. |

| 3 |

| Offering Period: | There will be a separate closing for each Offering. Each Offering is being conducted on a best efforts basis without any minimum target. The Company may undertake one or more closings on a rolling basis for each Offering. After each closing, funds tendered by Investors will be available to the Company. Because each Offering is being made on a best efforts basis and without a minimum offering amount, the Company may close each Offering at any level of proceeds raised. Each respective Offering shall be terminated on the earlier of (i) the date subscriptions for the Maximum Interests of such Series have been accepted, (ii) a date determined by the Manager in its sole discretion, or (iii) the date which is one year from the date this Offering Circular is qualified by the Commission which period may be extended by an additional six months by the Manager in its sole discretion. |

| Additional Investors: | After Closing of each Offering, no Member will be required to make additional capital contributions. If a Series’ funds are insufficient to meet the needs of the Series, the Manager shall notify the Members of the need for additional capital and the Members may be permitted, but not required, to make additional capital contributions to the Series on a pro-rata basis. In the event all Members do not make additional capital contributions, the Manager has discretion to sell additional Interests to third parties to meet the capital needs of such Series. |

| Use of proceeds: |

The proceeds received by a Series from its respective Offering will be applied in the following order of priority of payment:

(i) Due Diligence Fee: A fee equal to approximately 15.0% of the amount raised through this Offering, on average, paid to Manager as compensation for due diligence services in evaluating, investigation and discovering the Underlying Assets (fee is subject to change in sole discretion of Manager as disclosed in each Series Agreement);

(ii) Asset Cost of the Underlying Asset: Actual cost of the Underlying Asset paid to the Horse Seller (which may have been paid off prior to such Offering through a loan to the Company), including any accrued interest under potential loans to the Company and through down-payments by the Manager and/or its affiliates to acquire an interest in the Underlying Asset prior to an Offering.

In the case of the Offering for Series Palace Foal Interests, the 51% interest in the Palace Foal was acquired prior to the Offering through a down-payment by an affiliate of the Manager and loan to the Company;

In the case of the Offering for Series De Mystique ‘17 Interests, the 25% interest in the Palace Foal was acquired prior to the Offering through a down-payment by an affiliate of the Manager and loan to the Company; and

(iii) Offering Expenses: In general these costs include actual legal, accounting, underwriting, filing and compliance costs incurred by the Company in connection with an Offering of a series of Interests (and excludes ongoing costs described in Operating Expenses), as applicable, paid to legal advisors, brokerage, printing and accounting firms, as the case may be.

In the case of the Offering for Series Palace Foal Interests, the Manager has agreed to pay and not be reimbursed for Offering Expenses.

The Manager bears all expenses related to items (iii) above on behalf of a Series and is reimbursed by a Series through the proceeds of a successful offering. In addition, the Manager or an affiliate may loan the Company or a Series the funds required to pay any costs identified in item (ii), which will be reimbursed through the proceeds of a successful offering or refunded if an offering is aborted. Any loans made under item (iii), other than down-payments, accrue interest at the Applicable Federal Rate (as defined in the Internal Revenue Code). See “Use of Proceeds” and “Plan of Distribution and Subscription Procedure – Fees and Expenses” sections for further details. |

| 4 |

| Operating expenses: | “Operating Expenses” are costs and expenses attributable to the activities of the Series (collectively, “Operating Expenses”), which may be as much as or greater than the actual cost of a Series’ interest in the applicable Underlying Asset, including: |

| · | costs incurred in managing the Underlying Asset, including, but not limited to boarding, maintenance, training and transportation costs (the “Upkeep Fees”); |

| · | costs incurred in preparing any reports and accounts of the Series, including any tax filings and any annual audit of the accounts of the Series (if applicable) or costs payable to any third party registrar or transfer agent and any reports to be filed with the Commission including periodic reports on Forms 1-K, 1-SA and 1-U; |

| · | any indemnification payments; and |

| · | any and all insurance premiums or expenses in connection with the Underlying Asset, including mortality, liability and/or medical insurance of the Underlying Asset to insure against the death, injury or third party liability of racehorse ownership (as described in “Description of the Business – Business of the Company”). The decision to purchase insurance on a horse is made on a horse-by-horse basis. There is no guarantee that a horse you invest in will be insured. |

| The Company has purchased insurance for Palace Foal. | |

|

The Company has not yet purchased insurance for the De Mystique ‘17, but intends to do so just prior to the commencement of the Offering of Series De Mystique ’17 Interests.

The Manager has agreed to pay and not be reimbursed for Operating Expenses related to each Series incurred prior to Closing. Operating Expenses incurred post-Closing shall be the responsibility of a Series. We allocate a sizable portion of the Offering to a cash reserve to be spent on Upkeep Fees which cover operating expenses related specifically to the training, upkeep and maintenance of the applicable Underlying Asset. However, if the Operating Expenses exceed the amount of revenues generated from the applicable Underlying Asset, the Manager may (a) pay such Operating Expenses and not seek reimbursement, (b) loan the amount of the Operating Expenses to such Series, on which the Manager may impose a reasonable rate of interest, which shall not be lower than the Applicable Federal Rate (as defined in the Internal Revenue Code), and be entitled to reimbursement of such amount from future revenues generated by such Series (“Operating Expenses Reimbursement Obligation(s)”), and/or (c) cause additional Interests to be issued in order to cover such additional amounts.

Until a Series generates revenues from its interest in the applicable Underlying Asset, we expect a Series to, initially, deplete only the Upkeep Fees. We may incur Operating Expenses Reimbursement Obligations or the Manager pays such Operating Expenses incurred and will not seek reimbursement if Operating Expenses exceed revenues and Upkeep Fees. See discussion of “Description of the Business – Operating Expenses” for additional information. | |

| Further issuance of Interests: | A further issuance of Interests of a Series may be made in the event the Operating Expenses of that Series exceed the income generated from its interest in the Underlying Asset and cash reserves of that particular Series. This may occur if the Company does not take out sufficient amounts under an Operating Expenses Reimbursement Obligation to pay such excess Operating Expenses, or the Manager does not pay such amounts without seeking reimbursement. |

| 5 |

| Distributable Cash: |

“Distributable Cash” shall mean the net income (as determined under U.S. generally accepted accounting principles (“GAAP”)) generated by a Series plus any change in net working capital and depreciation and amortization (and any other non-cash Operating Expenses) for such Series and less any capital expenditures related to its interest in the applicable Underlying Asset. The Manager may maintain Distributable Cash funds in a deposit account or an investment account for the benefit of each Series.

A Series will typically generate Distributable Cash from revenue-generating events of such Series. The frequency with which such event occurs is dependent on the racing schedule of the Underlying Asset, potential sales of the Underlying Asset, and other revenue-generating events which do not occur on a fixed or set time period (e.g. quarterly or monthly) but which will recur on an ongoing basis so long as revenue is generated. |

| Management Fee: |

As compensation for the services provided by the Manager under the Management Agreement, the Manager will be paid an initial one-time 15% Due Diligence Fee from each Series and a subsequent fee of 10% of Gross Proceeds generated by each Series. “Gross Proceeds” is defined as the sum of all money generated by a Series, prior to any deductions that have been made or will be used for expenses.

The Management Fee does not accumulate if no Gross Proceeds are generated. The Management Fee is due only upon each revenue-generating event of such Series. The frequency with which such event occurs is dependent on the racing schedule of the applicable Underlying Asset, potential sales of the applicable Underlying Asset, and other revenue-generating events which do not occur on a fixed or set time period (e.g. quarterly or monthly) but which will recur on an ongoing basis so long as revenue is generated. |

| Distribution Rights: | The Manager has sole discretion in determining what distributions of Distributable Cash, if any, are made to Interest Holders of a Series. Any Distributable Cash generated by a Series from the utilization of the Underlying Asset shall be applied by that Series in the following order of priority: |

| · | 10% of the Gross Proceeds for that Series to the Manager as a Management Fee; |

| · | Thereafter, to repay any amounts outstanding under Operating Expenses Reimbursement Obligations for that Series plus accrued interest; |

| · | thereafter to create such reserves for that Series as the Manager deems necessary, in its sole discretion, to meet future Operating Expenses and/or Upkeep Fees of that Series; and |

| · | thereafter, 100% (net of corporate income taxes applicable to a Series) by way of distribution to the Interest Holders of that Series on a percentage basis. |

| Timing of Distributions: | The Manager may make periodic distributions of Distributable Cash remaining to Interest Holders of a Series subject to it having the right, in its sole discretion, to withhold distributions in order to meet anticipated costs and liabilities of a Series. The Manager may change the timing of potential distributions to a Series in its sole discretion. |

| No Trading Market | There is currently no public trading market for our Interests, and we do not intend or expect that any such market will ever develop. If an active public trading market for our securities does not develop or is not sustained, it may be difficult or impossible for you to resell your shares at any price. Even if a public market does develop, the market price could decline below the amount you paid for your shares.

The Company estimates that each Series will exist for 4-6 years (the racing life cycle) and then the Underlying Asset will be sold, which will be the primary liquidity event other than Distributions on Gross Proceeds as discussed above. A sale of the Underlying Asset may occur at a lower value than when the Underlying Asset was first acquired or at a lower price than the aggregate of costs, fees and expenses used to purchase the Underlying Asset. |

| 6 |

| Manager Duties: | The Manager may not be liable to the Company, any Series or the Investors for errors in judgment or other acts or omissions not amounting to fraud, willful misconduct or gross negligence, since provision has been made in the Operating Agreement for exculpation of the Manager. Therefore, Investors have a more limited right of action than they would have absent the limitation in the Operating Agreement. |

| Indemnification: | To the fullest extent permitted by applicable law, subject to approval of each Series Manager, all officers, directors, shareholders, partners, members, employees, representatives or agents of the Manager or a Series Manager, or their respective affiliates, employees or agents (each, a “Covered Person”) shall be entitled to indemnification from such Series (and the Company generally) for any loss, damage or claim incurred by such Covered Person by reason of any act or omission performed or omitted by such Covered Person in good faith on behalf of the Series Manager, or such Series and in a manner reasonably believed to be within the scope of authority conferred on such Covered Person by this Agreement and any Series Agreement, except that no Covered Person shall be entitled to be indemnified for any loss, damage or claim incurred by such Covered Person by reason of fraud, deceit, gross negligence, willful misconduct or a wrongful taking with respect to such acts or omissions; provided, however, that any indemnity under the Operating Agreement shall be provided out of and to the extent of the assets of the such Series only, and no other Covered Person or any other Series or the Company shall have any liability on account thereof. |

| To the fullest extent permitted by applicable law, subject to approval of a Series Manager, all expenses (including legal fees) incurred by a Covered Person in defending any claim, demand, action, suit or proceeding shall, from time to time, be advanced by such Series prior to the final disposition of such claim, demand, action, suit or proceeding upon receipt by such Series of an undertaking by or on behalf of the Covered Person to repay such amount if it shall be determined that the Covered Person is not entitled to be indemnified as authorized in the Operating Agreement. | |

| Transfers: | The Manager may refuse a transfer by an Interest Holder of its Interest(s) if such transfer would result in (a) there being more than 2,000 beneficial owners in a Series or more than 500 beneficial owners that are not “accredited investors”, (b) the assets of a Series being deemed “plan assets” for purposes of ERISA, (c) result in a change of U.S. federal income tax treatment of the Company and/or a Series, or (d) the Company, a Series or the Manager being subject to additional regulatory requirements. Furthermore, as the Interests are not registered under the Securities Act of 1933, as amended (the “Securities Act”), transfers of Interests may only be effected pursuant to exemptions under the Securities Act and permitted by applicable state securities laws and there is a right of first refusal on transfers of Interests. See “Description of Interests Offered – Limitations on Transferability” for more information. |

| Governing law: | The Company and the Operating Agreement will be governed by Nevada law and any dispute in relation to the Company and the Operating Agreement is subject to the dispute resolution provisions set forth therein. If an Interest Holder were to bring a claim against the Company or the Manager pursuant to the Operating Agreement, it would be required to do so in compliance with these dispute resolution provisions. Notwithstanding the foregoing, mandatory arbitration provisions set forth therein do not apply to claims made under the federal securities laws. |

| 7 |

The Interests offered hereby are highly speculative in nature, involve a high degree of risk and should be purchased only by persons who can afford to lose their entire investment. There can be no assurance that the Company’s investment objectives will be achieved or that a secondary market would ever develop for the Interests, whether via the MyRacehorse™ Platform, via third party registered broker-dealers or otherwise. The risks described in this section should not be considered an exhaustive list of the risks that prospective Investors should consider before investing in the Interests. Prospective Investors should obtain their own legal and tax advice prior to making an investment in the Interests and should be aware that an investment in the Interests may be exposed to other risks of an exceptional nature from time to time. The following considerations are among those that should be carefully evaluated before making an investment in the Interests.

Risks relating to the structure, operation and performance of the Company

An investment in our Interests is a speculative investment and, therefore, no assurance can be given that you will realize your investment objectives.

No assurance can be given that Investors will realize a return on their investments in us or that they will not lose their entire investment in our Interests. For this reason, each prospective subscriber for our Interests should carefully read this Offering Circular. All such persons or entities should consult with their legal and financial advisors prior to making an investment in the Interests.

An investment in an Offering constitutes only an investment in that Series and not in the Company, any other Series or the Underlying Asset.

A purchase of Interests in a Series does not constitute an investment in the Company, any other Series of the Company, or the Underlying Asset directly. This results in limited voting rights of the Investor, which are solely related to such Series. Investors will have voting rights only with respect to certain matters, primarily relating to the removal of the Manager for “cause.” The Manager thus retains significant control over the management of the Company and the Underlying Asset. Furthermore, because the Interests in a Series do not constitute an investment in the Company as a whole, holders of the Interests in the Series will not receive any economic benefit from, or be subject to the liabilities of, the assets of any other Series. In addition, the economic interest of a holder in a Series will not be identical to owning a direct undivided interest in the applicable Underlying Asset because, among other things, a Series will be required to pay corporate taxes before distributions are made to the holders, and the Manager will receive a fee in respect of its management of the applicable Underlying Asset.

There is no public trading market for our securities.

There is currently no public trading market for any of our Interests, and we do not intend or expect that any such market will ever develop. If an active public trading market for our securities does not develop or is not sustained, it may be difficult or impossible for you to resell your Interests at any price. Even if a public market does develop, the market price could decline below the amount you paid for your Interests.

There may be state law restrictions on an Investor’s ability to sell the Interests.

Each state has its own securities laws, often called “blue sky” laws, which (1) limit sales of securities to a state’s residents unless the securities are registered in that state or qualify for an exemption from registration and (2) govern the reporting requirements for broker-dealers and stock brokers doing business directly or indirectly in the state. Before a security is sold in a state, there must be a registration in place to cover the transaction, or it must be exempt from registration. We do not know whether our securities will be registered, or exempt, under the laws of any states. There may be significant state blue sky law restrictions on the ability of Investors to sell, and on purchasers to buy, our Interests. Investors should consider the resale market for our securities to be limited. Investors may be unable to resell their securities, or they may be unable to resell them without the significant expense of state registration or qualification.

| 8 |

Lack of operating history.

The Company and each Series were recently formed, have generated nominal revenues and have limited operating history upon which prospective Investors may evaluate their performance. No guarantee can be given that the Company and any Series will achieve their investment objectives, the value of any Underlying Asset will increase or that any Underlying Asset will be successfully monetized.

Limited Investor appetite.

Due to the start-up nature of the Company, there can be no guarantee that the Company will reach its funding target from potential Investors with respect to any Series or future proposed Series. In the event the Company does not reach a funding target, it may not be able to achieve its investment objectives by acquiring additional interests in underlying assets through the issuance of further Series and monetizing them together with interests in such Underlying Assets to generate distributions for Investors. In addition, if the Company is unable to raise funding for additional Series, this may impact any Investors already holding interests as they will not see the benefits which arise from economies of scale following the acquisition by other Series of additional underlying assets and other monetization opportunities (e.g., Membership Experience Programs - hosting events with the race horses, winners circle access, race day privileges, etc.).

There are few, if any, businesses that have pursued a strategy or investment objective similar to the Company’s.

We do not believe that any other company crowd funds racehorse ownership interests or proposes to run a platform for crowd funding of interests in racehorses. The Company and the Interests may not gain market acceptance from potential Investors, potential Horse Sellers or service providers within the racehorse ownership/syndicate industry, including insurance companies, syndicate managers, training facilities or maintenance partners. This could result in an inability of the Manager to operate the Underlying Asset profitably. This could impact the issuance of further series of interests and additional underlying assets being acquired by the Company. This would further inhibit market acceptance of the Company and if the Company does not acquire any additional underlying assets, Investors would not receive any benefits which arise from economies of scale (such as reduction in offering costs as a large number of interests in underlying assets may be listed on subsequent offering circulars, group discounts on mortality insurance and the ability to monetize its interest in underlying assets through Membership Experience Programs, as described below, that would require the Company to own a substantial number of its interest in underlying assets).

Offering amount exceeds value of Underlying Asset.

The size of each Offering will exceed the purchase price of such Series’ interest in the applicable Underlying Asset as at the date of such Offering (as the proceeds of each Offering in excess of the purchase price of the applicable Underlying Asset will be used to pay fees, costs and expenses incurred in making each Offering, acquiring the interest in the applicable Underlying Asset, Due Diligence Fees and Upkeep Fees). If the applicable Underlying Asset had to be sold and there has not been substantial appreciation of the applicable Underlying Asset prior to such sale, there may not be sufficient proceeds from the sale of the applicable Underlying Asset to repay Investors the amount of their initial investment (after first paying off any liabilities on the horse at the time of the sale including but not limited to any outstanding Operating Expenses Reimbursement Obligation) or any additional profits in excess of this amount.

Excess Operating Expenses

Operating Expenses related to a particular Series incurred post-Closing shall be the responsibility of the Series. The Company maintains a reserve for estimated Upkeep Fees for the Underlying Asset. However, if the Operating Expenses of a particular Series exceed the amount of revenues generated from the interest in the Underlying Asset of such Series, the Manager may (a) pay such Operating Expenses and not seek reimbursement, (b) loan the amount of the Operating Expenses to the Series, on which the Manager may impose a reasonable rate of interest, and be entitled to reimbursement of such amount from future revenues generated by its interest in the Underlying Asset (“Operating Expenses Reimbursement Obligation(s)”), and/or (c) cause additional Interests to be issued in order to cover such additional amounts.

If there is an Operating Expenses Reimbursement Obligation, this reimbursable amount between related parties would be repaid from the Distributable Cash generated by the Series and could reduce the amount of any future distributions payable to Investors. If additional Interests are issued in a particular Series, this would dilute the current value of the Interests held by existing Investors and the amount of any future distributions payable to such existing Investors.

| 9 |

Reliance on the Manager and its personnel.

The successful operation of the Company (and therefore, the success of the Interests) is in part dependent on the ability of the Manager to source, acquire and manage the Underlying Assets. As Experiential Squared, Inc. has only been in existence since June 2016 and is an early-stage startup company, it has no significant operating history within the horse racing sector, which evidences its ability to find, acquire, manage and utilize the Underlying Assets.

The success of the Company (and therefore, the Interests) will be highly dependent on the expertise and performance of the Manager and its team, its expert network and other professionals (which include third party experts) to find, acquire, manage and utilize the Underlying Assets. There can be no assurance that these individuals will continue to be associated with the Manager. The loss of the services of one or more of these individuals could have a material adverse effect on the Underlying Assets and, in particular, their ongoing management and use to support the investment of the Interest Holders.

Furthermore, the success of the Company and the value of the Interests is dependent on there being critical mass from the market for the Interests and that the Company is able to acquire a number of underlying assets in multiple series of interests so that the Investors can benefit from economies of scale which arise from holding more than one Underlying Assets (e.g., a reduction in offering costs if a large number of Underlying Assets are listed on subsequent offering circulars at the same time). In the event that the Company is unable to source additional Underlying Assets due to, for example, competition for such Underlying Assets or lack of Underlying Assets available in the marketplace, then this could materially impact the success of the Company and its objectives of acquiring additional Underlying Assets through the issuance of further series of interests and monetizing them together with the Underlying Assets at the Membership Experience Programs to generate distributions for Investors.

Liability of investors between series of interests.

The Company is structured as a Nevada series limited liability company that issues a separate series of interests for each Underlying Asset. Each Series will merely be a separate series and not a separate legal entity. Under the Nevada Revised Statutes (the “NRS”), if certain conditions (as set forth in NRS Section 86.296(3)) are met, the liability of investors holding one series of interests is segregated from the liability of investors holding another series of interests and the assets of one series of interests are not available to satisfy the liabilities of other series of interests. Although this limitation of liability is recognized by the courts of Nevada, there is no guarantee that if challenged in the courts of another U.S. State or a foreign jurisdiction, such courts will uphold a similar interpretation of Nevada corporation law, and in the past certain jurisdictions have not honored such interpretation. If the Company’s series limited liability company structure is not respected, then Investors may have to share any liabilities of the Company with all investors and not just those who hold the same series of interests as them. Furthermore, while we intend to maintain separate and distinct records for each series of interests and account for them separately and otherwise meet the requirements of the NRS, it is possible a court could conclude that the methods used did not satisfy Section 86.296(3) of the NRS and thus potentially expose the assets of such Series to the liabilities of another Series. The consequence of this is that Investors may have to bear higher than anticipated expenses which would adversely affect the value of their Interests or the likelihood of any distributions being made by a particular Series to its Investors. In addition, we are not aware of any court case that has tested the limitations on inter-series liability provided by Section 86.296(3) in federal bankruptcy courts and it is possible that a bankruptcy court could determine that the assets of one series of interests should be applied to meet the liabilities of the other series of interests or the liabilities of the Company generally where the assets of such other series of interests or of the Company generally are insufficient to meet our liabilities.

If any fees, costs and expenses of the Company are not allocable to a specific Series, they will be borne proportionately across all of the Series (which may include future Series and Interests yet to be issued). Although the Manager will allocate fees, costs and expenses acting reasonably and in accordance with its sole discretion, there may be situations where it is difficult to allocate fees, costs and expenses to a specific series of interests and therefore, there is a risk that a series of interests may bear a proportion of the fees, costs and expenses for a service or product for which another series of interests received a disproportionately high benefit.

| 10 |

Potential breach of the security measures of the MyRacehorse™ Platform.

The highly automated nature of the MyRacehorse™ Platform through which potential investors may acquire interests may make it an attractive target and potentially vulnerable to cyber-attacks, computer viruses, physical or electronic break-ins or similar disruptions. The MyRacehorse™ Platform processes certain confidential information about investors, the Horse Sellers and the underlying assets. While we intend to take commercially reasonable measures to protect the confidential information and maintain appropriate cybersecurity, the security measures of the MyRacehorse™ Platform, the Company, the Manager or the Company’s service providers could be breached. Any accidental or willful security breaches or other unauthorized access to the MyRacehorse™ Platform could cause confidential information to be stolen and used for criminal purposes or have other harmful effects. Security breaches or unauthorized access to confidential information could also expose the Company to liability related to the loss of the information, time-consuming and expensive litigation and negative publicity, or loss of the proprietary nature of the Manager’s and the Company’s trade secrets. If security measures are breached because of third-party action, employee error, malfeasance or otherwise, or if design flaws in the MyRacehorse™ Platform software are exposed and exploited, the relationships between the Company, investors, users and the Horse Sellers could be severely damaged, and the Company or the Manager could incur significant liability or have their attention significantly diverted from utilization of the underlying assets, which could have a material negative impact on the value of interests or the potential for distributions to be made on the interests.

Because techniques used to sabotage or obtain unauthorized access to systems change frequently and generally are not recognized until they are launched against a target, the Company, and other third-party service providers may be unable to anticipate these techniques or to implement adequate preventative measures. In addition, federal regulators and many federal and state laws and regulations require companies to notify individuals of data security breaches involving their personal data. These mandatory disclosures regarding a security breach are costly to implement and often lead to widespread negative publicity, which may cause investors, the Horse Sellers or service providers within the industry, including insurance companies, to lose confidence in the effectiveness of the secure nature of the MyRacehorse™ Platform. Any security breach, whether actual or perceived, would harm the reputation of the Company and the MyRacehorse™ Platform and the Company could lose investors and the Horse Sellers. This would impair the ability of the Company to achieve its objectives of acquiring additional underlying assets through the issuance of further series of interests and monetizing them together with the Underlying Asset at the Membership Experience Programs.

Risks relating to the Offerings

We are offering our Interests pursuant to recent amendments to Regulation A promulgated pursuant to the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, and we cannot be certain if the reduced disclosure requirements applicable to Tier 2 issuers will make our Interests less attractive to investors.

As a Tier 2 issuer, we will be subject to scaled disclosure and reporting requirements which may make an investment in our Interests less attractive to investors who are accustomed to enhanced disclosure and more frequent financial reporting. In addition, given the relative lack of regulatory precedent regarding the recent amendments to Regulation A, there is a significant amount of regulatory uncertainty in regards to how the Commission or the individual state securities regulators will regulate both the offer and sale of our securities, as well as any ongoing compliance that we may be subject to. If our scaled disclosure and reporting requirements, or regulatory uncertainty regarding Regulation A, reduces the attractiveness of the Interests, we may be unable to raise the funds necessary to fund future offerings, which could impair our ability to develop a diversified portfolio of racehorses and create economies of scale, which may adversely affect the value of the Interests or the ability to make distributions to Investors.

There may be deficiencies with our internal controls that require improvements, and if we are unable to adequately evaluate internal controls, we may be subject to penalties.

As a Tier 2 issuer, we will not need to provide a report on the effectiveness of our internal controls over financial reporting, and we will be exempt from the auditor attestation requirements concerning any such report so long as we are a Tier 2 issuer. We are in the process of evaluating whether our internal control procedures are effective and therefore there is a greater likelihood of undiscovered errors in our internal controls or reported financial statements as compared to issuers that have conducted such evaluations.

| 11 |

Impact of non-compliance with regulations.

The Interests will be qualified in each state where the Offering and sale of such Interests will occur. If a regulatory authority determines that the Manager, who is not a registered broker-dealer under the Exchange Act or any state securities laws, has itself engaged in brokerage activities, the Manager may need to stop operating and therefore, the Company will not have an entity managing its interest in the Underlying Assets. In addition, if the Manager is required to register as a ‘broker-dealer’, there is a risk that any Interests offered and sold while the Manager was not registered may be subject to a right of rescission, which may result in the early termination of the Series.

Furthermore, the Company is not registered and will not be registered as an investment company under the Investment Company Act of 1940, as amended (the “Investment Company Act”), and the Manager will not be registered as an investment adviser under the Investment Advisers Act of 1940, as amended (the “Investment Advisers Act”), and thus the Interests do not have the benefit of the protections of the Investment Company Act or the Investment Advisers Act. The Company and the Manager have taken the position that the underlying assets are either (i) not “securities” within the meaning of the of the Investment Company Act or the Investment Advisers Act or (ii) such Underlying Assets deemed “securities” will be limited such that the Company’s assets will comprise of less than 40% investment securities under the Investment Company Act and the Manager will not be advising with respect to securities under the Investment Advisers Act. This position, however, is based upon applicable case law that is inherently subject to judgments and interpretation. If the Company were to be required to register under the Investment Company Act or the Manager were to be required to register under the Investment Advisers Act, it could have a material and adverse impact on the results of operations and expenses of each Series and the Manager may be forced to liquidate and wind up each Series or rescind the Offerings for any of the Series or the offering for any other series of interests.

Possible Changes in Federal Tax Laws.

The Internal Revenue Code (the “Code”) is subject to change by Congress, and interpretations of the Code may be modified or affected by judicial decisions, by the Treasury Department through changes in regulations and by the Internal Revenue Service through its audit policy, announcements, and published and private rulings. Although significant changes to the tax laws historically have been given prospective application, no assurance can be given that any changes made in the tax law affecting the Company, a series, or an investment in any series of interest of the Company would be limited to prospective effect. Accordingly, the ultimate effect on an Investor’s tax situation may be governed by laws, regulations or interpretations of laws or regulations which have not yet been proposed, passed or made, as the case may be.

There is substantial doubt about our ability to continue as a going concern.

The Company's ability to continue as a going concern is dependent upon its ability to generate future profitable operations and/or obtain the necessary financing to meet its obligations and repay its liabilities arising from normal business operations when they become due.

We have elected to delay compliance with certain new or revised financial accounting standards.

We have elected to delay compliance with the new revenue recognition accounting standard, ASC Topic 606 Revenue from Contracts with Customers, which took effect on January 1, 2018 until the date that a company that is not an issuer (as defined under section 2(a) of the Sarbanes-Oxley Act of 2002 (15 U.S.C. 7201(a)) is required to comply with such new or revised accounting standard, if such standard also applies to companies that are not issuers. Management does not believe the provisions of ASC Topic 606 will have a material impact on our financial position or results of operations, but some investors may view this as a lack of access to certain information they may deem important.

Risks relating to the Horse Racing industry

There can be no assurances that the value of the racehorse (whether it is a Thoroughbred, Quarter Horse or Standardbred) which is owned by the Series will not decrease in the future which may have an adverse impact on the Company’s or an Individual Series’ activities and financial position.

The business of owning, training and racing horses is a high-risk venture. There is no assurance that any horse and therefore any interest in such horse acquired by the Series will be successful. Horses are subject to aging, illness, injury and disease which may result in permanent or temporary retirement from racing, restrictions in racing schedules, layups, and even natural death or euthanasia of the animal. There can be no assurances that the value of the interest in such Underlying Asset which may be acquired and owned by a Series, will not decrease in the future or that a Series will not subsequently incur losses on the racing careers or sale or other disposition of any or all of the horses which such Series may acquire. No combination of management ability, experience, knowledge, care or scientific approach can avoid the inherent possibilities of loss.

| 12 |

While the Company believes that there is a market for horse breeding, training and racing, such a market is highly volatile. The horse industry is dependent upon the present and future values of horses and of the Company’s and Series’ horse(s) in particular. The Company can provide no assurance that it will be successful in its proposed activity. The expenses incurred may result in operating losses for the Company and there is no assurance that the Company will generate profits or that any revenues generated will be sufficient to offset expenses incurred or would result in a profit to the Company. As a result, it is possible that Investors will lose all or a substantial part of their investment in the Company. Additionally, there is no assurance that there will be any cash available for distribution.

The valuation of racehorses is a highly speculative matter and the market for racehorses is extremely volatile. If the valuation of an individual Series' horse decreases the individual Series will still be responsible for the expenses of maintaining, training and racing the horse at lower level races or smaller venues which could negatively impact the revenues from the horse.

The valuation of horses (particularly racehorses) is a highly speculative matter and prices fluctuated widely, particularly in recent years. The success of the Company, and each an individual Series, is dependent upon the present and future values of racehorses generally, and of the Company's racehorses in particular, the racing industry in general, as well as the racing success of the Underlying Assets. Although the future value of horses generally cannot be predicted, it will be affected by general economic conditions such as inflation, employment, recessions, tariffs, unstable or adverse credit market conditions, other business conditions, the amount of money available for investment purposes, and the continued interest of investors and enthusiasts in the racehorse industry. In the past, there has been growing foreign investment in certain types of racehorses, and the continued ability of foreign investors to acquire horses is subject to change due to economic, political or regulatory conditions. The value of racehorses is also subject to federal income tax treatment of racing and related activities, the continuation or expansion of legalized gambling and the size of racing purses, all which cannot be predicted. The expense of maintaining, boarding, training and racing horses can be expected to increase during the term of a Series or the Company, regardless of what happens to the future market price of racehorses or the performance of the Company racehorses. Further, there is always a risk of liability for damages caused by the Underlying Assets to other persons or property.

The cost of racing is unpredictable and speculative and may negatively impact the Company’s and each individual Series’ ability to generate revenue.

Increases in operation costs, labor rates and other variable costs, such as costs of feed and grain and costs of transporting animals (all of which are subject to inflationary pressure and should be expected to increase), to an extent which cannot be matched by increases in revenue. The racehorse industry, like other industries, is subject to labor disputes, labor shortages, and government intervention, changes in laws, licensing or regulatory restrictions may adversely impact the availability of grooms, trainers, jockeys and other horse industry workers. Adverse weather and economic conditions may result in unforeseen circumstances including, without limitation, restrictions on attendance at a particular race or racetrack, ability to transport the horses, and increases in costs or decreases in revenues. Changes in government regulations, whether or not relating to the horse racing industry, may result in additional expenses or reduced revenue from operations.

If a horse is unsuccessful in racing, becomes sick or injured, the Underlying Asset’s value will be adversely affected which may have a negative impact of the Company's and such individual Series' valuation and its revenue.

Horse racing is extremely speculative and expensive. In the event that a horse in which a Series has an interest was to be transported to various tracks and training centers throughout the United States, and thus exposed too many other horses in training, the risk of illness, injury or death increases significantly. A horse in which a Series has an interest must earn enough through racing to cover expenses of boarding and training. If a horse in which a Series has an interest is unsuccessful in racing, their value will be adversely affected. Furthermore, revenues from racing are dependent upon the size of the purses offered. The size of the purses depends in general on the extent of public interest in horse racing, and in particular on the relative quality of the specific horses in contention in any specific meeting or race. Although public interest has been strong in recent years, there is no assurance that public interest will remain constant, much less increase. Legalized gambling proliferating in many states threatens to curtail interest in horse racing as a means of recreation. In addition, there is no assurance that the horse in which a Series has an interest will be of such quality that they may compete in any races which offer purses of a size sufficient to cover such Series' expenses.

| 13 |

Horse racing could be subjected to restrictive regulation or banned entirely which could adversely affect the conduct of the Company's business.

The racing future of and/or market for the horses in which the Company and/or a Series' has an interest depends upon continuing governmental acceptance of horse racing as a form of legalized gambling. Although horse racing has a long history of acceptance in the United States and as a source of revenue, at any time, horse racing could be subjected to restrictive regulation or banned entirely. The value of the interest in an Underlying Asset would be substantially diminished by any such regulation or ban. Horse racing is regulated in various states and foreign countries by racing regulatory bodies which oversee the conduct of racing as well as the licensing of owners, trainers and others. Further, other forms of gambling are being approved throughout the United States and therefore no assurance can be provided that the legalization of other forms of gambling and competition from non-gambling sports and other activities will not adversely affect attendance and participation, and therefore the profitability of horse racing and sales. Lastly, our ownership structure is novel and may prepare us to seek regulatory approval to race in certain jurisdictions.

The Company may not purchase insurance on its horse which could require Company resources to be spent to cover any loses from the death or injury of a horse.

The decision to purchase insurance on a horse is made on a horse-by-horse basis. There is no guarantee that a horse you invest in will be insured. Mortality insurance insures against the death of a horse during the Company's partial ownership. Medical insurance covers possible risks of injury during racing or training. Liability insurance covers the risk that the horse in which the Company or a Series has an interest causes death, injury or damage to persons or property. Without insurance an individual Series is responsible for the cost of injury of veterinary expenses, surgery, and rehabilitation, or in the event of death, the Company will lose its investment in the horse. The payment of such liabilities may have a material adverse effect on our financial position. The Company has not yet purchased insurance for the Palace Foal or De Mystique ‘17, but intends to do so just prior to the commencement of the Offering of Series Palace Foal and Series De Mystique ‘17 Interests.

A decrease in average attendance per racing date coupled with increasing costs could jeopardize the continued existence of certain racetracks which could negatively impact the Company's operations.

A decrease in average attendance per racing date coupled with increasing costs could jeopardize the continued existence of certain racetracks which could impact the availability of race tracks available for horses in which the Company or a Series has an interest to race at and then negativity impact its operations.

Industry practices and structures have developed which may not be attributable solely to profit-maximizing, economic decision-making which may have an adverse impact on our Company's activities business.

Because horse racing is a sport as well as a business, industry practices and structures have developed which not be attributable solely to profit-maximizing, economic decision-making. For instance, a particular bloodline could command substantial prices owing principally to the interest of a small group of individuals having particular goals unrelated to economics. A decline in this interest could be expected to adversely affect the value of the bloodline.

Series may only own a minority interest in Underlying Assets as a result it may not have sufficient control regarding the training or racing of the Underlying Asset.

Currently, the Company has begun purchasing interests in race horses through series, mainly under an existing California intrastate permit offering. A Series will not always own a majority interest in a particular horse. Therefore, despite its best efforts to build in oversight rights and major decision rights (such as the sale of an Underlying Asset) a Series and the Company may have minimal input with regard to the race selection and training of the horse(s). As a result, the Company and such Series may be dependent on the majority owners’ decisions as to when and where to race or show the horse and to its training regime. Additionally, there are situations in which a trainer or owner may have a conflict of interest which could negatively impact the ability of a horse to be placed in a particular race and given priority in workout times, jockeys or stabling.

Market shortages may impact the ability of the Series to generate revenue.

The Company, through its individual Series, will primarily engage in horse racing in the United States. The future success of these activities will depend upon the ability of the Manager to purchase an interest in high-quality horses through an individual Series. The future success of these activities also depends upon whether the horse is being handled by highly skilled trainers and ridden by highly skilled jockeys. Because horse racing is an intensely competitive activity and the Company will be competing with a number of persons who have substantially greater experience and financial resources than Company to purchase interests in the best racehorses, there can be no assurance that the Company will be successful in the endeavors of pursuing certain racehorses for any Series. Further, once purchased, because the Company may have only a minority interest in such horse, the Company will have limited input into the training, handling, and management of the horse and therefore can make no assurances as to the success of the investment.

| 14 |

The Company, via an individual Series, has no intention of paying dividend payments on a regular schedule as revenues are irregular, seasonal, and unpredictable.

The revenues, if any, of an individual Series may be highly irregular and seasonal. While the Manager will endeavor to sell horses or interests in horses for cash at the time of sale, there can be no assurance that other payment terms will not be required by the relevant market conditions. The consequent variance in the amount or the timing of the Company's dividends, if any, could pose particular risks for Investors who seek to transfer their Interests during the term of the Company.

Competitive interests and other factors can have unforeseen consequences.

The horseracing industry is highly competitive and speculative. Horseracing in the United States and in foreign countries draws competitors and participants from locations throughout the United States and overseas, who have been in the business of horseracing for many years and have substantially greater financial resources than Company. The Company will be competing in its racing and selling activities with such persons. Similarly, horse markets are international, and auctions are frequently internationally advertised. This can be favorable in that it increases the value of Underlying Assets but, by the same token, Company has little influence and may not be able to compete with such competitors in the acquisition of interests in horses. The Company will be competing in the purchase and sale of horses with most of the major horse breeders and dealers in the United States and foreign countries. Thus, prices at which the Company buys or sells its interests in the Underlying Assets may vary dramatically. Market factors, which are beyond the Company’s control, will greatly affect the profitability of the Company. Such factors include, but are not limited to, auction prices, private sales, foreign investors, federal income tax treatment of the racing industry and the size of racing purses. Further, the Company and the concept of crowdfunding in the racehorse industry is a new venture and thus the risk of unforeseen issues and problems is high.

There is a lack of financial forecasts for the Company and for individual Series.

While the Company believes that there is a market for racehorse breeding, training and racing, such a market is highly volatile. The racehorse industry is dependent upon the present and future values of racehorses and of the horses in which the Company or a Series invested in particular. There can be no assurance that the Company will be successful in its proposed activity. The expenses incurred may result in operating losses for the Company and there is no assurance that the Company will generate profits or that any revenues generated will be sufficient to offset expenses incurred or would result in a profit to the Company. As a result, it is possible that the Investors will lose all or a substantial part of their investment in the Company. Additionally, there is no assurance that there will be any cash available for dividends. In addition, dividends, if any, may be less than their distributive share of taxable income and the Investors’ tax liability could require out-of-pocket expenditures by the Investors.

Lack of Diversification.

It is not anticipated that each Series would own any assets other than its interest in such Underlying Asset, plus potential cash reserves for maintenance, training, insurance and other Upkeep Fees pertaining to its interest in such Underlying Asset and amounts earned by such Series from the monetization of its interest in such Underlying Asset. Investors looking for diversification will have to create their own diversified portfolio by investing in other opportunities in addition to such Series.

Risks Related to Ownership of our Interests

You will have only limited “major decision” rights regarding our management and it will be difficult to remove our Manager, therefore, you will not have the ability to actively influence the day-to-day management of our business and affairs.

Our Manager has sole power and authority over the management of our Company and the individual Series. Furthermore, our Manager may only be removed for “Good Cause” meaning fraud, deceit, gross negligence, willful misconduct or a wrongful taking, bad faith, death, disability or disappearance, etc.

To remove the Manager for “Good Cause”, Members holding in excess of 75% of the percentage interests, must approve. Therefore, you will not have an active role in our Company’s management and it would likely be difficult to cause a change in our management. As a result, you will not have the ability to alter our management’s path if you feel they have erred.

| 15 |

Lack of voting rights.

The Manager has a unilateral ability to amend the Operating Agreement in certain circumstances without the consent of the Investors, and the Investors only have limited voting rights in respect of a Series. Investors will therefore be subject to any amendments the Manager makes (if any) to the Operating Agreement and also any decision it takes in respect of the Company and the applicable Series, which the Investors do not get a right to vote upon. Investors may not necessarily agree with such amendments or decisions and such amendments or decisions may not be in the best interests of all of the Investors as a whole but only a limited number.

Furthermore, the Manager can only be removed as manager of the Company and each Series in very limited circumstances. Investors would therefore not be able to remove the Manager merely because they did not agree, for example, with how the Manager was operating an underlying asset.

The offering price for the Interests determined by us may not necessarily bear any relationship to established valuation criteria such as earnings, book value or assets that may be agreed to between purchasers and sellers in private transactions or that may prevail in the market if and when our Interests can be traded publicly.

The price of the Interests was derived as a result of our negotiations with Horse Sellers based upon various factors including prevailing market conditions, our future prospects and our capital structure, as well as certain expenses incurred in connection with the Offerings and the acquisition of interests in each Underlying Asset. These prices do not necessarily accurately reflect the actual value of the Interests or the price that may be realized upon disposition of the Interests.

Funds from purchasers accompanying subscriptions for the Interests will not accrue interest prior to admission of the subscriber as an Investor in the Series, if it occurs, in respect of such subscriptions.

The funds paid by purchasers for the Interests will go into the Company’s general operating account and be allocated to the specific Series which is subject of the investment. Investors will not have the use of such funds or receive interest thereon pending the completion of said Offering. No subscriptions will be accepted and Interests sold unless valid subscriptions for such Offering are received and accepted prior to the termination of the Offering Period. If we terminate an Offering prior to accepting a subscriber’s subscription, funds will be returned, without interest or deduction, to the proposed Investor.

The Company’s Operating Agreement contains mandatory arbitration provisions that restrict your ability to bring claims against the company, except in instances of claims related to Federal and State securities laws.

Investors will be obligated to submit any claims against the Company to arbitration, except in instances of claims related to Federal and State securities laws. Investors will be limited in the location, venue and circumstances under which a claim for damages can be brought against the Company or its officer, directors, managers or related parties. This limitation reduces the ability of Investors to dispute or fight against decisions made by the Company or its managers which may be viewed as having a negative impact on the value of your underlying investment.

| 16 |

POTENTIAL CONFLICTS OF INTEREST

We have identified the following conflicts of interest that may arise in connection with the Interests, in particular, in relation to the Company, the Manager and the Underlying Assets. The conflicts of interest described in this section should not be considered as an exhaustive list of the conflicts of interest that prospective Investors should consider before investing in the Interests.

Manager’s Fees and Compensation

None of the compensation set forth under "Compensation to Manager and Its Affiliates" was determined by arms' length negotiations. It is anticipated that the commissions and profits received by the Manager may be higher or lower depending upon market conditions.

This conflict of interest will exist in connection with Company management and Investors must rely upon the duties of the Manager of good faith and fair dealing to protect their interests, as qualified by the Operating Agreement.

The Manager has the right to retain the services of other firms, in addition to or in lieu of the Manager, to perform various services, asset management and other activities in connection with the business that is described in this Offering Circular.

Loans or Other Related Party Transactions

The Company converted an advance from founders outstanding as of December 31, 2017 to equity in the Company to ease the cash flow burden to the Company. The Company also has borrowed up to $31,275 from the manager of the Company in order to acquire horse assets prior to establishing and issuing securities in the underlying series holding the horse assets. Because these are related party transactions, no guarantee can be made that the terms of the arrangements are at arm’s length.

Other Series or Businesses

The Manager may engage for its own account, or for the account of others, in other business ventures, similar to that of the Company or otherwise, and neither the Company nor any Investor shall be entitled to any interest therein.

The Company will not have independent management and it will rely on the Manager for the operation of the Company. The Manager will devote only so much time to the business of the Company as is reasonably required. The Manager will have conflicts of interest in allocating management time, services and functions between its existing business interests other than the Company and any future entities which it may organize as well as other business ventures in which it may be involved. The Manager believes it has sufficient staff available to be fully capable of discharging its responsibilities to all such entities.

The Manager, acting in the same capacities for other investors, companies, partnerships or entities, may result in competition with individual Series, including other Series. There are no restrictions on the Manager, or any of its affiliates, against operating other businesses in such competition with the Company. If the Manager or any of its affiliates did operate such a business that competed for clients with the Company, it could substantially impair the Company's financial results.