FORM 1-A

Regulation A Offering Statement

Part II – Offering Circular

Amendment No. 2

Multi-Housing Income REIT, LLC

9050 N. Capital of Texas Highway

Suite 320

Austin, TX 78759

(512) 872-2898

investors@upsideavenue.com

www.upsideavenue.com

November 15, 2023

This Offering Circular Follows the Form 1-A Disclosure Format

Multi-Housing Income REIT, LLC, a limited liability company organized under the laws of Delaware (which we refer to as the “Company,” “we,” “us” or “our”), was formed to acquire interests in real estate assets in the United States. We are a real estate investment trust, or “REIT,” for federal income tax purposes.

The Company is seeking to raise up to $74,500,000 of capital by offering to the public limited liability company interests designated as “Common Shares,” in what we refer to as the “Offering.” You can read a complete description of these securities in “Securities Being Offered.” We refer to individuals and entities that purchase Common Shares as “Investors.”

The Offering will begin as soon as our offering statement is “qualified” by the SEC. The Offering will end upon the earlier of (1) the date we have sold $74,500,000 of Common Shares, (2) the date two years after it begins, or (3) the date we decide to end it.

Initially, the Company will sell Common Shares for $11.29 each, with a minimum initial investment of $2,000. We may raise or lower the price of the Common Shares during this Offering to reflect the value of the Company’s assets by filing an amendment to this Offering Circular. For more information, see “Securities Being Offering – Price of Common Shares.”

We are selling these securities directly to the public at our website, www.upsideavenue.com. We are not using a placement agent or a broker and we are not paying commissions to anyone. All the money we raise goes directly to the Company:

| Common Shares | Price to Public | Underwriting Discounts and Commissions | Proceeds to Issuer | Proceeds to Other Persons | ||||||||||||

| One Share | $ | 11.29 | $ | 0 | $ | 11.29 | $ | 0 | ||||||||

| Total | $ | 74,500,000 | $ | 0 | $ | 74,500,000 | $ | 0 | ||||||||

When you invest, your funds will first be deposited in an escrow account with North Capital until we determine whether you are qualified to invest. We try to make that determination within 30 days.

The owners of our Common Shares do not have voting rights. You should consider an investment only if you are willing to entrust all aspects of the Company’s business to its management team.

Please note that the Company’s governing instruments (i) restrict the ability of Investor to sell or otherwise transfer Common Shares, and (ii) allow the Manager has the right to buy back the Common Shares of Investors without their consent in certain circumstances. See “Summary of LLC Agreement.”

Investing in our Common Shares is speculative and involves substantial risks, including the risk that you could lose all your money. Before investing, you should carefully review “Risks of Investing.”

THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OF OR GIVE ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERM OF THE OFFERING. NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SELLING LITERATURE. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED HEREUNDER ARE EXEMPT FROM REGISTRATION.

GENERALLY, NO SALE MAY BE MADE TO YOU IN THIS OFFERING IF THE AGGREGATE PURCHASE PRICE YOU PAY IS MORE THAN 10% OF THE GREATER OF YOUR ANNUAL INCOME OR NET WORTH. DIFFERENT RULES APPLY TO ACCREDITED INVESTORS AND NON-NATURAL PERSONS. BEFORE MAKING ANY REPRESENTATION THAT YOUR INVESTMENT DOES NOT EXCEED APPLICABLE THRESHOLDS, WE ENCOURAGE YOU TO REVIEW RULE 251(d)(2)(i)(C) OF REGULATION A. FOR GENERAL INFORMATION ON INVESTING, WE ENCOURAGE YOU TO REFER TO WWW.INVESTOR.GOV. FOR MORE INFORMATION, SEE “Limits on How Much Non-Accredited Investors Can Invest” STARTING ON PAGE 26.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR PASSED UPON THE ADEQUACY OR ACCURACY OF THIS OFFERING CIRCULAR. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

NORTH AMERICAN SECURITIES ADMINISTRATORS ASSOCIATION UNIFORM LEGEND:

YOU SHOULD MAKE YOUR OWN DECISION WHETHER THIS OFFERING MEETS YOUR INVESTMENT OBJECTIVES AND RISK TOLERANCE LEVEL. NO FEDERAL OR STATE SECURITIES COMMISSION HAS APPROVED, DISAPPROVED, ENDORSED, OR RECOMMENDED THIS OFFERING. NO INDEPENDENT PERSON HAS CONFIRMED THE ACCURACY OR TRUTHFULNESS OF THIS DISCLOSURE, NOR WHETHER IT IS COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS ILLEGAL.

THESE SECURITIES ARE SUBJECT TO RESTRICTIONS ON TRANSFERABILITY AND RESALE AND MAY NOT BE TRANSFERRED OR RESOLD EXCEPT AS PERMITTED UNDER THE ACT AND APPLICABLE STATE SECURITIES LAWS, PURSUANT TO REGISTRATION OR EXEMPTION THEREFROM. YOU SHOULD BE AWARE THAT YOU WILL BE REQUIRED TO BEAR THE FINANCIAL RISKS OF THIS INVESTMENT FOR AN INDEFINITE PERIOD OF TIME.

Table of Contents

i

ii

iii

A WARNING ABOUT FORWARD-LOOKING STATEMENTS

The term “forward-looking statements” means any statements, including financial projections, that relate to events or conditions in the future. Often, forward-looking statements include words like “we anticipate,” “we believe,” “we expect,” “we intend,” “we plan to,” “this might,” or “we will.” The statement “We believe interest rates will rise” is an example of a forward-looking statement.

Because we are talking about a new business, most of the things we say in this Offering Circular are forward-looking statements. In fact, everything we say is a forward-looking statement, other than statements of historical fact.

Forward-looking statements are, by their nature, subject to uncertainties and assumptions. The statement “We believe interest rates will rise” is not like the statement “We believe the sun will rise in the East tomorrow.” It is impossible for us to know exactly what is going to happen in the future, or even to anticipate all the things that could happen. Our business could be subject to many unanticipated events, including all of the things we talk about in “Risks of Investing.”

Consequently, the actual result of investing in the Company could (and almost certainly will) differ from those anticipated or implied in any forward-looking statement, and the differences could be both material and adverse. We do not undertake any obligation to revise, or publicly release the results of any revision to, any forward-looking statements, except as required by applicable law. GIVEN THE RISKS AND UNCERTAINTIES, PLEASE DO NOT PLACE UNDUE RELIANCE ON ANY FORWARD-LOOKING STATEMENTS.

BUYING COMMON SHARES IS SPECULATIVE AND INVOLVES SIGNIFICANT RISK, INCLUDING THE RISK THAT YOU COULD LOSE SOME OR ALL OF YOUR MONEY. THIS SECTION DESCRIBES WHAT WE BELIEVE ARE THE MOST SIGNIFICANT RISK FACTORS AFFECTING THE FUND AND ITS INVESTORS. THE ORDER IN WHICH THESE FACTORS ARE DISCUSSED IS NOT INTENDED TO SUGGEST THAT SOME FACTORS ARE MORE IMPORTANT THAN OTHERS.

You Might Lose Your Money: When you buy a certificate of deposit from a bank, the federal government (through the FDIC) guarantees you will get your money back. Our Common Shares have no such guarantee. The ability of the Company to make distributions depends on a number of factors, including some beyond our control. Nobody guarantees that you will receive payments and you might lose some or all of your money.

Our Track Record Does not Guaranty Future Performance: The section of this Offering Circular captioned “Past Performance: Our Track Record So Far” illustrates the performance of the Company and certain affiliates. However, there is no guaranty that the Company will do well in the future as it has done in the past.

Speculative Nature of Real Estate Investing: Real estate can be risky and unpredictable. For example, many experienced, informed people lost money when the real estate market declined in 2007-8. Time has shown that the real estate market goes down without warning, sometimes resulting in significant losses. Some of the risks of investing in real estate include changing laws, including environmental laws; floods, fires, and other Acts of God, some of which can be uninsurable; changes in national or local economic conditions; changes in government policies, including changes in interest rates established by the Federal Reserve; and international crises. You should invest in real estate in general, and in the Company in particular, only if you can afford to lose your investment and are willing to live with the ups and downs of the real estate industry.

Our Growth Focus Increases Risk: The Company intends to focus on real estate projects on the “growth” side of the growth/income spectrum. By definition, these projects will tend to carry greater risk, along with the potential for higher profits.

Page | 1

Investors Must Wait 90 Days Before Receiving Dividends: If the Company pays a dividend, Investors who have acquire their Common Shares within the preceding 90 days will not share in the dividend.

Risks from Rising Interest Rates: Over the last six months interest rates have risen significantly. Meanwhile, consumer-level inflation has reached levels not seen for 40 years. While many economists believe the increase in inflation will be short-lived, caused by supply chain bottlenecks created by the COVID-19 pandemic, nobody knows for sure. If interest rates continue to rise it will likely harm our business.

Pricing of Common Shares: The price of our Common Shares was determined by the Manager based on the Manager’s estimate of the value of the Company’s assets. The Manager’s estimate was not necessarily based on third-party appraisals of the Company’s assets.

Property Values Could Decrease: The value of the properties in which we invest could decline, perhaps significantly. Factors that could cause the value of a property to decline include, but are not limited to:

| ● | Changes in interest rates |

| ● | Competition from existing properties and new construction |

| ● | Changes in national or local economic conditions |

| ● | Changes in zoning |

| ● | Environmental contamination or liabilities |

| ● | Changes in local market conditions |

| ● | Fires, floods, and other casualties |

| ● | Uninsured losses |

| ● | Undisclosed defects in property |

| ● | Incomplete or inaccurate due diligence |

Illiquidity of Real Estate: Real estate is generally illiquid, meaning that it is not typically capable of being readily sold for cash at fair market value. Thus, the Company might not be able to sell a real estate project as quickly or on the terms that it would like. Moreover, the overall economic conditions that might cause the Company to want to sell properties are generally the same as those in which it would be most difficult to sell.

Competition: To achieve satisfactory returns for our Investors, the Manager must identify projects that satisfy our investment selection criteria and that can be acquired at reasonable prices. There is no guaranty that the Manager will be able to do so. The real estate industry is highly competitive and fragmented. The Manager, directly or through affiliates, will compete with other real estate developers for the most promising projects, and some of those other real estate developers could have substantially greater resources, allowing them to move more quickly, pay more, or have greater access to the best projects. The result could be that the Company winds up investing in projects of lower quality, or where the owner of the project (an affiliate of the Manager) paid too much as a result of intense competition. In addition, each project acquired will face competition from other projects, including both existing properties and new properties. Such competition could limit the ability of the Company to raise rents in its projects or even force the Company to decrease rents, at the risk of higher vacancy rates.

The Company will Invest Primarily in the Sponsor’s Projects: To date, the Company has invested primarily in projects sponsored by the Sponsor. We expect that will continue in the future. These projects will not necessarily be the best projects available.

Entitlement Risks: The Company might invest in projects before some or all of the necessary zoning approvals have been obtained. Securing zoning approval can take a long time and be very expensive, and even after a long and expensive process there is no guaranty that approval will be given. If approvals cannot be obtained the value of the real estate could go down and Investors could lose some or all of their money.

Governmental Regulation: In addition to zoning approval, any development project will require the approval of numerous government authorities regulating such matters as density levels, the installation of utility services such as water and waste disposal, and the dedication of acreage for open space, parks, schools and other community purposes. Governmental authorities have imposed impact fees as a means of defraying the cost of providing certain governmental services to developing areas and the amount of these fees has increased significantly during recent years. Many state laws require the use of specific construction materials which reduce the need for energy consuming heating and cooling systems. Local governments also, at times, declare moratoriums on the issuance of building permits and impose other restrictions in areas where sewage treatment facilities and other public facilities do not reach minimum standards. All of these regulations will impose costs and risks on our Projects.

Page | 2

Lack of Representations and Warranties from Sellers: The Company might invest in projects where the seller of the real estate made limited or no representations and warranties concerning the condition of the real estate, the status of leases, the presence of hazardous materials or hazardous substances, the status of governmental approvals and entitlements, and other important matters. If we fail to discover defects through our own due diligence review but discover them only after the project has been acquired and the Company has made its investment, we may have little or no recourse against the sellers.

Incomplete Due Diligence: The Manager or an affiliate of the Manager will perform “due diligence” on each project, meaning we will review available information about the project, its current zoning, the surrounding community, and other information we believe is relevant. As a practical matter, however, it is simply impossible to review all of the information about a given piece of real estate (or about anything) and there is no assurance that all of the information we have reviewed is accurate. For example, sometimes important information is hidden or unavailable, or a third party might have an incentive to conceal information or provide inaccurate information, or we might not think of all the relevant information, or we might not be able to verify all the information we review. It is also possible that we will reach inaccurate conclusions about the information we have reviewed. Due diligence is as much an art as it is a science, and there is a risk that, especially with the benefit of hindsight, our due diligence will turn out to have been incomplete or inadequate.

Pricing of Assets: The success of the Company and its ability to make distributions to Investors depends on the Manager’s ability to gauge the value of real estate assets. Although the Manager and its principals are experienced real estate investors and will rely on various objective criteria to select properties for investment, including, in all or almost all cases, third-party appraisals, ultimately the value of these assets is as much an art as a science, and there is no guaranty that the Company and its advisors will be successful.

Americans with Disabilities Act: Under the Americans with Disabilities Act (the “ADA”), public accommodations must meet certain federal requirements related to access and use by disabled persons. Some (although not all) of the projects in which the Company invests will be “public accommodations,” and complying with the ADA and other similar laws will make those projects more expensive to build and maintain than they would have been otherwise. Furthermore, it is possible that the ADA could be extended by law or regulation, requiring existing projects to be retrofitted at great expense.

Difficulty Attracting Buyers and Tenants: Some of the projects in which the Company invests will involve the construction of houses, with the expectation that the houses will be sold once construction is complete. Other projects will involve the construction of multi-family apartment communities, with the expectation that the apartments will be leased to tenants once construction is complete. In either situation, the projects will be built on “spec,” meaning that we will not have a buyer for the house or tenants for the apartments at the time construction begins. Depending on market conditions, we might experience difficulty finding a buyer or tenants, with adverse effects on the profitability of the project.

Construction Risks: From time to time we may acquire unimproved real property or properties that are under development or construction. No matter how carefully we plan, the construction process is notorious for cost overruns and delays. If the construction of a project ended up costing significantly more than we had budgeted, or took significantly longer to complete than forecast, or were done improperly, the profitability or even the viability of the project could suffer.

Environmental Risks: The Manager or its affiliates will conduct typical environmental testing on each project to determine the existence of significant environmental hazards. However, it is impossible to be certain of all the ways that a given piece of real estate has been used, raising the possibility that environmental hazards could exist despite our environmental investigations. Under federal and state laws, moreover, a current or previous owner or operator of real estate may be required to remediate any hazardous conditions without regard to whether the owner knew about or caused the contamination. Similarly, the owner of real estate could become subject to common law claims by third parties based on damages and costs resulting from environmental contamination. The cost of investigating and remediating environmental contamination can be substantial, even catastrophic. The existence of an environmental hazard could therefore present direct or indirect risks to the Company.

Page | 3

Inability to Implement Liquidity Transactions: We will typically aim to invest in projects that can be liquidated (i.e., sold) within approximately five years. However, there is no guarantee that we will be able to successfully pursue a liquidity event with respect to any of our projects. Market conditions may delay or even prevent the Manager from pursuing liquidity events. If we do not or cannot liquidate our real estate portfolio, or if we experience delays due to market conditions, this could delay Investors’ ability to receive a return of their investment indefinitely and may even result in losses.

Need for Additional Capital: The real estate industry is capital-intensive, and the inability to obtain financing could limit our growth. We may need to raise more money in the future so we can continue to acquire and operate projects. In addition, we might need to raise money to make capital improvements required by law or by market conditions, or for other purposes. There is no guarantee that funding will be available to us when we need it, or on terms that are not adverse to your interests. If we cannot raise additional funding when needed, our operations and prospects could be negatively affected.

Future Securities Could Have Superior Rights: The Company might issue securities in the future that have rights superior to the rights associated with the Common Shares. For example, the holders of those securities could have the right to receive distributions before any distributions are made to Investors, or distributions that are higher, dollar for dollar, than the distributions paid to the holders of the Common Shares, or the right to receive all their money back on a liquidation of the Company before the holders of the Common Shares receive anything.

Risks Associated with Leverage: We intend to borrow money to finance most or all of the projects in which the Company invests. While debt financing can improve returns in a good market, it carries significant risks in a bad market, and therefore increases our vulnerability to downturns in the real estate market or in economic conditions generally. There is no guaranty that we will generate sufficient cash flow to meet our debt service obligations, and we may be unable to repay, refinance or extend our debt when due. We may also give our lender(s) security interests in our assets as collateral for our debt obligations. If we are unable to meet our debt service obligations, those assets could be foreclosed upon, which could negatively affect our ability to generate cash flows to fund distributions to Investors. We may also be required to sell assets to repay debt and may be forced to sell at times that are unfavorable to the Company, which would likewise negatively affect our ability to operate successfully.

Uninsured Losses: The Manager or an affiliate of the Manager will try to ensure that each project carries adequate insurance coverage against foreseeable risks. However, there can be no assurance that our insurance will be adequate, and insurance against some risks, like the risk of earthquakes and/or floods, might be unavailable altogether or available at commercially unreasonable rates or in amounts that are less than the full market value or replacement cost of the underlying properties. Hence, it is possible that a project would suffer an uninsured loss, resulting in a loss to the Company and Investors. Given the Company’s initial focus on Southern California, the risk of uninsured losses from earthquakes is especially significant.

Broad Investment Strategy: The Manager has broad discretion to choose projects. An Investor might prefer a more focused strategy.

Loss of Uninsured Bank Deposits: Any cash the Company has on hand from time to time will likely be held in regular bank accounts. While the FDIC insures deposits up to a specified amount, it is possible that the amount of cash in the Company’s account would exceed the FDIC limits, resulting in a loss if the bank failed.

Potential Liability to Return Distributions: Under some circumstances, Investors who received distributions from the Company could be required to return some or all of those distributions. However, Investors generally will not be liable for the debts and obligations of the Company beyond the amount they paid for the Common Shares.

Page | 4

Limited Liability of Manager: Under the Company’s First Amended and Restated Limited Liability Company Agreement, the grounds for which an Investor may sue the Manager is very limited. For example, the First Amended and Restated Limited Liability Company Agreement waives all fiduciary obligations of the Manager. This means that except in rare circumstances, you will not be able to sue the Manager even if the Manager makes mistakes and those mistakes cost you money.

Limited Participation in Management: Investors will not have a right to vote or otherwise participate in managing the Company. For example, Investors will have no voice in selecting the projects in which the Company invests, deciding on the terms of the investment, or deciding when a project should be sold. Only those willing to give complete control to our management team should consider an investment in the Company.

Reliance on Management: The success of the Company depends almost exclusively on the abilities of its current management team. If any of these individuals resigned, died, or became ill, the Company and its Investors could suffer.

Conflicts of Interest: The interests of the Manager could conflict with the interests of Investors in a number of important ways, including these:

| ● | The interests of Investors might be better-served if our management team devoted its full attention to the business of the Company. Instead, our team will manage a number of different projects. |

| ● | Members of our management team have business interests wholly unrelated to the Company and its affiliates, all of which require a commitment of time. |

| ● | Our Sponsor operates other real estate funds and might establish new real estate funds in the future. Where the Manager identifies an attractive real estate project there could be conflicts whether the project should be acquired by the Company or by one of the other real estate funds. |

| ● | The lawyers who prepared the First Amended and Restated Limited Liability Company Agreement, the Investment Agreement, and this Offering Circular represent us, not you. You must hire your own lawyer (at your own expense) if you want your interests to be represented. |

Waiver of Right to Jury Trial: The Investment Agreement and the LLC Agreement both provide that legal claims will be decided only by a judge, not by a jury. The provision in the LLC Agreement will apply not only to an Investor who purchases Common Shares in the Offering, but also to anyone who acquires Common Shares in secondary trading. Having legal claims decided by a judge rather than by a jury could be favorable or unfavorable to the interests of an owner of Common Shares, depending on the parties and the nature of the legal claims involved. It is possible that a judge would find the waiver of a jury trial unenforceable and allow an owner of Common Shares to have his, her, or its legal claim decided by a jury. In any case, the waiver of a jury trial in both the Investment Agreement and the LLC Agreement do not apply to claims arising under the federal securities laws.

Forum Selection Provision: Our Investment Agreement and our LLC Agreement both provide that disputes will be handled solely in the state or federal courts located in or most geographically convenient to Austin, Texas. We included this provision primarily because the Company’s headquarters are in Austin. This provision could be unfavorable to an Investor to the extent that (i) a court in a different jurisdiction would be more likely to find in favor of an Investor, (ii) bringing a claim in Austin, Texas would be geographically inconvenient to an Investor or increase his, her, its costs, or (iii) this provision discourages Investors from bringing claims. It is possible that a judge would find this provision unenforceable and allow an Investor to file a lawsuit in a different jurisdiction.

Section 27 of the Exchange Act provides that federal courts have exclusive jurisdiction over lawsuits brought under the Exchange Act, and that such lawsuits may be brought in any federal district where the defendant is found or is an inhabitant or transacts business. Section 22 of the Securities Act provides that federal courts have concurrent jurisdiction with State courts over lawsuits brought under the Securities Act, and that such lawsuits may be brought in any federal district where the defendant is found or is an inhabitant or transacts business. Investors cannot waive our (or their) compliance with federal securities laws. Hence, to the extent the forum selection provisions of the Investment Agreement or the LLC Agreement conflict with these federal statutes, the federal statutes would prevail.

Page | 5

Limitation on Rights in LLC Agreement: The Company’s First Amended and Restated Limited Liability Company Agreement limits your rights in several important ways, including these:

| ● | The LLC Agreement significantly curtails your right to bring legal claims against management. |

| ● | The LLC Agreement limits your right to obtain information about the Company and to inspect its books and records. |

| ● | Investors can remove the Manager only in very limited circumstances, even if you think the Manager is doing a bad job. |

| ● | The Manager is allowed to amend the LLC Agreement in certain respects without your consent. |

| ● | The LLC Agreement restricts your right to sell or otherwise transfer your Common Shares. |

| ● | The LLC Agreement gives the Manager the right to buy back your Common Shares without your consent if the Manager determines that (i) the Company would otherwise become subject to the Employee Retirement Income Security Act of 1974 (after referred to as “ERISA”), or (ii) you have engaged in certain misconduct. |

| ● | The LLC Agreement provides that all disputes will be conducted in Travis County, Texas. |

Limitations on Rights in Investment Agreement: To purchase Common Shares, you are required to sign our Investment Agreement. The Investment Agreement would limit your rights in several important ways if you believe you have claims against us arising from the purchase of your Common Shares:

| ● | Any claims arising from your purchase of Common Shares or the Investment Agreement must be brought in the state or federal courts located in Austin, Texas, which might not be convenient to you. |

| ● | You would not be entitled to a jury trial. However, the waiver of trial by jury does not apply to claims arising under the Federal securities laws. |

| ● | You would not be entitled to recover any lost profits or special, consequential, or punitive damages. However, this limitation of damages does not apply to claims arising under the Federal securities laws. |

| ● | If you lost your claim against us, you would be required to pay our expenses, including reasonable attorney’s fees. If you won, we would be required to pay yours. |

Limits on Transferability: There are several obstacles to selling or otherwise transferring your Common Shares:

| ● | There will be no established market for your Common Shares, meaning you could have difficulty finding a buyer. |

| ● | Under the LLC Agreement, the Common Shares may not be transferred in some circumstances. |

| ● | If you want to sell your Common Shares, you must first offer it to the Manager. |

| ● | Under the LLC Agreement, a transferee will not be admitted as a member of the Company unless the transferor and transferee satisfy certain conditions, including satisfying the Manager that the proposed transfer will not violate any laws. |

| ● | Under the Limited Liability Company Agreement, the Common Shares may not be transferred if the Manager determines that the transfer could jeopardize the status of the Company as a REIT. |

| ● | To qualify as a REIT, the Limited Liability Company Agreement limits the amount of the Company that any one person may own, which may restrict your ability to sell Common Shares to others who have invested in the Company. |

Page | 6

Risk of Failure to Comply with Securities Laws: The Company is conducting this Offering under Regulation A, an exemption from registration authorized by the SEC, and engaged in a previous offering under Regulation A, which was qualified by the SEC on June 18, 2018. While the Company has been guided by the advice of legal counsel, the securities laws are very complicated and it is possible to violate one rule or another without intending to. If the Company fails to comply with the securities laws in the future or has failed to comply in the past, the Company could be subject to severe penalties and/or prohibited from raising additional capital, in both cases with material adverse effects for investors.

Risk of Severe Penalties Without Doing Anything Wrong: Under SEC Rule 262(a)(7), the Company could be disqualified from selling securities even if it has done nothing wrong, merely because the SEC has begun an investigation of the Company. Thus, for example, if a competitor with an ax to grind contacts the SEC with false information and the SEC begins an investigation, it could prohibit the Company from raising capital, thereby imposing substantial harm on the Company and its investors, harm that would not be mitigated or compensated even when the investigation reveals no wrongdoing.

Reduced Disclosure Requirements Under the JOBS Act: The Common Shares are being offered pursuant to Tier 2 of Regulation A issued by the SEC, as amended pursuant to the Jumpstart Our Business Startups Act of 2012 (known as the “JOBS Act”). Regulation A does not require us to provide you with all of the information that would be required in a registration statement in connection with an initial public offering (IPO) of securities. As a Regulation A issuer, we are also not subject to the same level of ongoing reporting obligations as a typical public reporting company, including, but not limited to, many of the disclosure requirements applicable to public reporting companies under the Securities Exchange Act of 1934.

We Are an “Emerging Growth Company” Under the JOBS Act: Today, the Company qualifies as an “emerging growth company” under the JOBS Act. If the Company were to become a public company (e.g., following an IPO) and continued to qualify as an emerging growth company, it would be able to take advantage of certain exemptions from the reporting requirements under the Securities Exchange Act of 1934 and exemptions from certain investor protection measures under the Sarbanes Oxley Act of 2002. Using these exemptions could benefit the Company by reducing compliance costs but could also mean that investors receive less information and receive fewer protections than they would otherwise. However, these exemptions – and the status of the Company as an “emerging growth company” in the first place – will not be relevant unless the Company becomes a public reporting company, which we do not plan or foresee.

We Are Not Subject to the Corporate Governance Requirements that Apply to Companies Listed on a National Exchange: Companies whose securities are listed on a national stock exchange (for example, the New York Stock Exchange) are generally subject to a number of rules about corporate governance that are intended to protect investors. For example, the major U.S. stock exchanges require listed companies to have an audit committee made up entirely of independent members of the board of directors (i.e., directors with no material outside relationships with the company or management), which is responsible for monitoring the Company’s compliance with the law. As of the date of this Offering Statement, neither the Common Shares nor any other securities of the Company are listed on a national exchange, and it is likely that our securities will never be listed on a national exchange. Accordingly, you may not have the same protections afforded to stockholders of companies that are subject to all of the corporate governance requirements of a national exchange.

Regulation As An Investment Company: If the Company were treated as an “investment company” under the Investment Company Act of 1940, we would be required to comply with a number of special rules and regulations and incur significant cost doing so. In addition, if it were determined that the Company had operated as an investment company without registering as such, we could be subject to significant penalties and, among other things, any contracts the Company had entered into could be rendered unenforceable. As described in “Investment Company Act Limitations,” we intend to conduct our business so that we are not treated as an investment company. However, we might not be successful.

Failure to Satisfy Conditions of REIT; Taxes on REITs: We intend to be taxed as a real estate investment trust, or “REIT,” under Sections 856 through 860 of the Internal Revenue Code (the “Code”) for purposes of federal income taxes. To qualify as a REIT, the Company must satisfy a number of criteria, both now and on an ongoing basis. Should the Company fail to satisfy any of these criteria, even inadvertently, it could become subject to penalty taxes and/or lose its REIT status altogether, which would make the Company subject to federal income tax and thereby reduce the returns to investors substantially. Further, even if it maintains its REIT status, the Company could be subject to various taxes in some situations. While the Company intends to seek guidance from tax advisors and operate its business accordingly, there is no guaranty that it will be able to avoid taxes and maintain its qualification as a REIT.

Page | 7

REIT Requirements Could Restrict Actions: REITs are subject to a 100% tax on income from “prohibited transactions,” which include sales of assets that constitute inventory or other property held for sale in the ordinary course of a business, other than foreclosure property. This 100% tax could impact our desire to sell assets and other investments at otherwise opportune times if we believe such sales could be considered a prohibited transaction.

Required Distributions: As a REIT, we generally must distribute 90% of our annual taxable income to our investors. From time to time we might generate taxable income greater than our net income for financial reporting purposes from, among other things, amortization of capitalized purchase premiums, or our taxable income might be greater than our cash flow available for distribution to our stockholders. If we do not have other funds available in these situations, we might be unable to distribute 90% of our taxable income as required by the REIT rules. In that case, we would need to borrow funds, sell a portion of our investments, potentially at disadvantageous prices, or find another alternative source of funds. These alternatives could increase our costs or reduce our equity and reduce amounts to invest in real estate assets and other investments. Moreover, the distributions received by our stockholders in such an event could constitute a return of capital for federal income tax purposes, as the distributions would be in excess of our earnings and profits.

Federal and State Income Taxes as a REIT: Even if the Company qualifies and maintains its qualification as a REIT, it may be subject to federal income taxes and related state taxes. For example, if we have net income from a “prohibited transaction,” such income will be subject to a 100% tax. The Company may not be able to make sufficient distributions to avoid excise taxes applicable to REITs. The Company may also decide to retain income it earns from the sale or other disposition of its property and pay income tax directly on such income. In that event, the Company’s investors will be treated as if they earned that income and paid the tax on it directly. However, shareholders that are tax-exempt would have no benefit from their deemed payment of such tax liability. The Company may also be subject to state and local taxes on its income or property. Any federal or state taxes paid by the Company will reduce the Company’s operating cash flow and cash available for distributions.

FIRPTA Tax on Non-U.S. Sellers: A non-U.S. Investor who sells Common Shares for a gain would generally be subject to tax under the Foreign Investment in Real Property Tax Act (FIRPTA) if the Company does not qualify as a “domestically controlled REIT,” meaning a REIT in which less than 50% of the value of the outstanding shares are owned by non-U.S. persons. We intend to qualify as a domestically controlled REIT, but there can be no assurance we will always do so.

Changes in Tax Laws: At any time, the federal income tax laws or regulations governing REITs or the administrative interpretations of those laws or regulations may be amended. We cannot predict when or if any new federal income tax law, regulation or administrative interpretation, or any amendment to any existing federal income tax law, regulation or administrative interpretation, will be adopted, promulgated or become effective and any such law, regulation or interpretation may take effect retroactively. Any such change could result in an increase in our, or our shareholders’, tax liability or require changes in the manner in which we operate in order to minimize increases in our tax liability. A shortfall in tax revenues for states and municipalities in which we operate may lead to an increase in the frequency and size of such changes. If such changes occur, we may be required to pay additional taxes on our assets or income or be subject to additional restrictions. These increased tax costs could, among other things, adversely affect our financial condition, the results of operations and the amount of cash available for the payment of dividends. We and our shareholders could be adversely affected by any such change in, or any new, federal income tax law, regulation, or administrative interpretation.

Breaches of Security: It is possible that our systems would be “hacked,” leading to the theft or disclosure of confidential information you have provided to us. Because techniques used to obtain unauthorized access or to sabotage systems change frequently and generally are not recognized until they are launched, we and our vendors may be unable to anticipate these techniques or to implement adequate defensive measures.

The

Foregoing Are Not Necessarily The Only Risks Of Investing

Please Consult With Your Professional Advisors

Page | 8

Summary of Our Company and its Investment Strategies

The Company was formed on October 17, 2017 to invest in a diversified portfolio of predominantly income-producing real estate assets throughout the United States. The Company focuses primarily on student housing, multi-housing, conventional apartments, and senior living (both existing and new development projects) but also looks for opportunities across other commercial real estate sectors.

The Company typically targets projects with capitalization rates in the single digits and where we believe we can achieve a double digit IRR. Our typical expected holding period is between three to seven years, subject to market conditions. We do not expect to invest more than 50% of our assets in any one property.

Our investment strategies include the following:

| ● | Core Plus Strategy – Our Core Plus Strategy focuses on quality multi-housing properties with quality residents in primary and secondary markets with an opportunity to increase net operating income. |

| ● | Value Add Strategy – Our Value Add Strategy focuses on increasing occupancy and net operating income on multi-housing properties through renovations and repositioning of the properties. |

| ● | Opportunistic Strategy – Our Opportunistic Strategy focuses on finding opportunities to participate in multi-housing new development, distressed sales, and/or bankruptcy auctions, including land development and new construction. |

To the extent allowed by the rules governing REITs, we might also invest, to a limited extent, in other real estate-related assets, including mortgage-backed obligations and loans where the business of the borrower is significantly related to real estate, or highly liquid shares of REITs or other securities representing real estate assets traded on national and international exchanges such as the TSX, ASX, NSE, BSE, and US-domiciled OTC markets.

As of the date of this Offering Circular, the Company has invested a total of $ 5,618,858 in nine different real estate projects.

The sponsor of the Company is Casoro Capital Partners, LLC, also a Texas limited liability company (the “Sponsor”). Monte K. Lee-Wen is a principal of the Sponsor. See “Our Management Team.”

Over the last 10 years, the Sponsor has raised approximately $203 million of capital and acquired approximately 22 apartment communities. See “Our Sponsor’s Track Record.”

Investments Through Other Entities

Sometimes the Company will own real estate directly. Most of the time, however, the investments made by the Company will be through other entities (“Project Entities”). For example, if the Company invests in a student housing property, the property will be owned by a Project Entity formed as a limited partnership or a limited liability company. Typically, Project Entities will be controlled by the Sponsor or another entity controlled by the Sponsor. However, if the Company does not control the Project Entity itself then it will retain control rights, meaning the Company’s consent will be required to certain major actions taken by the Project Entity, such as the sale or refinancing of its real estate and the replacement of its manager or general partner.

Investments in Sponsor Projects

To date, the Company has not acquired any real estate directly. Instead, the Company has invested only as an investor in projects sponsored by the Sponsor. However, the Company could acquire real estate directly in the future and/or invest in projects with different sponsors.

Page | 9

The Company is governed by a Limited Liability Company Agreement dated September 29, 2023, which we refer to as the “LLC Agreement.” You can read a summary in “Summary of LLC Agreement” and a copy of the LLC Agreement is attached as Exhibit 1A-2B.

The Company is managed by Casoro Investment Advisory Firm LLC, a Texas limited liability company (the “Manager”). The LLC Agreement generally gives the Manager exclusive control over all aspects of the Company’s business. Other members of the Company, including Investors who purchase Common Shares in the Offering, generally have no right to participate in the management of the Company.

There is only one exception to this rule: the owners of Common Shares may, in some situations, remove the Manager for cause. For more information, see “Summary of LLC Agreement.”

We expect that all the real estate projects we invest in, whether as a direct owner or as an investor, will be “leveraged,” meaning encumbered by debt. As a general rule, we will invest in projects only where the ratio of the loan amount to the value of the property is no more than 80%. In certain cases, depending on the property and its underwriting, we might also use mezzanine debt or preferred equity.

The Company competes with many other companies for suitable projects, ranging from small real estate investors owning one or two projects to large, public REITs owning dozens.

Our competitive advantages include the following:

| ● | Our management team has over 100 years of combined experience in acquisition, asset management, and property management. |

| ● | We are vertically integrated, giving us greater control over how assets are owned and managed. |

Our Conversion to Limited Liability Company Structure

The Company was formed as a Maryland corporation on October 17, 2017. Early in 2022 our management team decided that the flexibility associated with limited liability companies would be better suited to our business. Hence, after gaining the approval of our shareholders, the Company was converted to a Delaware limited liability company effective on March 18, 2022.

Although the Company is now a limited liability company for purposes of state law, it has elected to be treated as a “C” corporation for tax purposes. Hence, it remains eligible to be treated as a REIT.

Page | 10

Our Previous Regulation A Offerings

The Company has already conducted two previous offerings under Regulation A. The first offering was qualified by the SEC on June 18, 2018 and the second on July 22, 2022. Together, the Company raised approximately $609,541 in those offerings. All the documents relating to the previous offerings are available on EDGAR.

We will begin deploying the capital we raise in this Offering right away. We intend to operate the Company indefinitely.

To wind down the Company, the Manager will seek to generate liquidity for Investors and realize any gains in the value of our investments by selling or refinancing our properties and returning capital to Investors on an orderly basis. Sales and refinancing will be subject to prevailing market conditions and there is no guarantee that we will be successful in executing any such liquidity transactions on terms favorable to the Company and Investors, or that we will be able to do so within the time frame we have anticipated.

The following summarizes the Company’s existing investments:

| Name of Project Entity | Casoro Jax LP | PPA Water Ridge LP | Newport Apartments LP | Casoro Lach LP |

| Type of Entity | Limited Partnership | Limited Partnership | Limited Partnership | Limited Partnership |

| State of Formation | Delaware | Texas | Texas | Texas |

| Address of Project Entity | 9050 North Capital of Texas Highway Suite 320 Austin, TX 78759 |

9050 North Capital of Texas Highway Suite 320 Austin, TX 78759 |

9050 North Capital of Texas Highway Suite 320 Austin, TX 78759 |

9050 North Capital of Texas Highway Suite 320 Austin, TX 78759 |

| Description of Project Entity’s Real Estate Project | ● Multifamily property ● 322 units ● Currently 88.23% occupied |

● Multifamily property ● 476 units ● Currently 90.69% occupied |

● Multifamily property ● 308 units ● Currently 86.6% occupied |

● Multifamily property ● 150 units ● Currently 92.93% occupied |

| Location of Project | 12222 Vance Jackson Rd, San Antonio, TX | 4600 West Pioneer, Irving, TX | 3466 N Belt Line Rd, Irving, TX | 14722 Nacogdoches Rd, San Antonio, TX |

| Nature of Company’s Interest in Project Entity |

Partnership Interest |

Partnership Interest |

Partnership Interest |

Partnership Interest |

| Amount of Actual or Anticipated Investment |

$480,682 Actual |

$400,000 Actual |

$100,000 Actual |

$780,500 Actual |

| Ownership Percentage | 2.7389 2.7389% | 2.4396% | 1.326% | 13.9114% |

| Fees and Compensation to Sponsor | Acquisition, Asset Management, Construction Management, Property Management, Utility Billing Management | Acquisition, Asset Management, Construction Management, Property Management, Utility Billing Management | Acquisition, Asset Management, Construction Management, Property Management, Utility Billing Management | Acquisition, Asset Management, Construction Management, Property Management, Utility Billing Management |

| Distributions to Sponsor | In accordance with provisions in the Partnership Agreement | In accordance with provisions in the Partnership Agreement |

In accordance with provisions in the Partnership Agreement |

In accordance with provisions in the Partnership Agreement |

Page | 11

| Name of Project Entity | CG Jax Investors, LP | Casoro Capitol on 28th, LP | Houston Flats JV, LLC | CG Sunset Land LLC |

| Type of Entity | Limited Partnership | Limited Partnership | Limited Liability Company |

Limited Partnership |

| State of Formation | Delaware | Texas | Delaware | Texas |

| Address of Project Entity | 9050 North Capital of Texas Highway Suite 320 Austin, TX 78759 |

9050 North Capital of Texas Highway Suite 320 Austin, TX 78759 |

9050 North Capital of Texas Highway Suite 320 Austin, TX 78759 |

9050 North Capital of Texas Highway Suite 320 Austin, TX 78759 |

| Description of Project Entity’s Real Estate Project | ● Multifamily property ● 322 units ● Currently 88.23% occupied |

● Multifamily property ● 231 units ● Currently 93.07% occupied |

● Multifamily property ● 368 units ● Currently 85.65% occupied |

● Land

|

| Location of Project | 12222 Vance Jackson Rd, San Antonio, TX | 215 NE 28th Street, Oklahoma City, OK | 2101 Hayes Rd, Houston, TX 77077 | 2170 Thousand Oaks Dr, San Antonio, TX |

| Nature of Company’s Interest in Project Entity |

Partnership Interest |

Partnership Interest |

Preferred Equity |

Partnership Interest |

| Amount of Actual or Anticipated Investment |

$534,500 Actual |

$210,000 Actual |

$2,000,000 Actual |

$525,658 Actual |

| Ownership Percentage | 3.0456% | 6.67% | 0% | 33% |

| Fees and Compensation to Sponsor | Acquisition, Asset Management, Construction Management, Property Management, Utility Billing Management | Acquisition, Asset Management, Construction Management, Property Management, Utility Billing Management | Acquisition, Asset Management, Construction Management, Property Management, Utility Billing Management | Acquisition, Asset Management, Construction Management, Property Management, Utility Billing Management |

| Distributions to Sponsor | In accordance with provisions in the Partnership Agreement | In accordance with provisions in the Partnership Agreement |

In accordance with provisions in the Partnership Agreement |

In accordance with provisions in the Partnership Agreement |

Page | 12

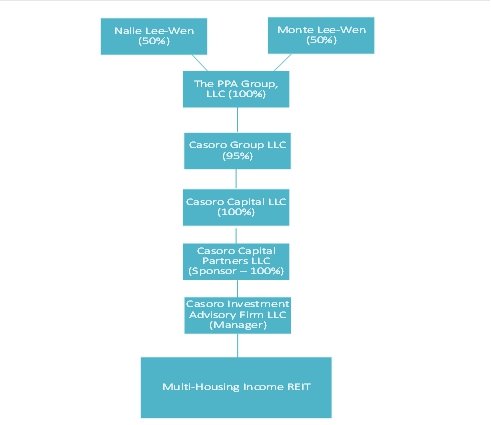

When you buy Common Shares you will become an owner of the Company, Multi-Housing Income REIT LLC, a Delaware limited liability company.

The Manager of the Company is Casoro Investment Advisory Firm, LLC, a Texas limited liability company.

Casoro Investment Advisory Firm, LLC is wholly-owned by the Sponsor, Casoro Capital Partners, LLC, also a Texas limited liability company.

Casoro Capital Partners, LLC is wholly-owned by Casoro Capital LLC, a Delaware limited liability company.

Casoro Capital, LLC is owned 95% by Casoro Group, LLC, a Delaware limited liability company.

Casoro Group LLC is wholly-owned by The PPA Group, LLC, a Nevada limited liability company.

The PPA Group, LLC is owned 50% by Monte K. Lee-Wen and 50% by Nalie Lee-Wen. Mr. and Mrs. Lee-Wen are married.

The following chart shows our ownership structure:

Summary and Narrative Description

The Sponsor of the Company is Casoro Capital Partners, LLC, which we refer to as “CCP.” The principal owner and manager of the Sponsor is Monte Lee-Wen. Mr. Lee-Wen is also the Chief Executive Officer The PPA Group, LLC, a real estate investment firm, which we refer to as “PPA.”

Since 2002, PPA has acquired over 37 multifamily apartment communities and invested equity amounts in excess of $221.3 million in Washington, Arizona, and Texas. The communities purchased or developed by Mr. Lee-Wen and his team involved approximately 11 different offerings, raising over $18.9 million in equity from more than 100 investors. We refer to each of these securities offerings as a “Program.”

Page | 13

All of the Programs are similar to the Company in the following respects:

| ● | They all involved raising money from investors. |

| ● | They all involve conducting the same business as the business in which the Company will be engaged, i.e., investing in multi-housing apartment communities. |

| ● | They all have the same investment objectives as the Company. |

Because of these similarities, investors who are considering investing in the Company’s common stock might find it useful to review information about the Programs. Of course, prospective investors should bear in mind that PRIOR PERFORMANCE DOES NOT GUARANTY FUTURE RESULTS. The fact that Mr. Lee-Wen and PPA have been successful with the Programs does not mean the Company will experience the same results.

There have been no major adverse business developments or conditions experienced by any Program that would be material to purchasers of the Company’s Common Shares.

None of the Programs:

| ● | Has been registered under the Securities Act of 1933; |

| ● | Has been required to report under section 15(d) of the Securities Exchange Act of 1934; |

| ● | Has had a class of equity securities registered under section 12(g) of the Securities Exchange Act of 1934; or |

| ● | Has, or has had, 300 or more security holders. |

Of the 37 multifamily apartment communities PPA acquired, 28 have completed their full investment cycle, from acquisition to renovation to operation to disposition. The financial results of these 28 “round trip” projects are as follows:

| Property | Class | Units | Years Owned | Sale Date | Project IRR | Investor IRR | ||||||||||||||

| #1 - #5 | B | 1070 | 1.75 | Nov-21 | 47 | % | 37 | % | ||||||||||||

| #6 | B | 204 | 2.87 | Jul-21 | 29 | % | 24 | % | ||||||||||||

| #7 | B | 236 | 4.32 | Jul-21 | 7 | % | 1 | % | ||||||||||||

| #8 | B | 252 | 4.81 | Jul-21 | 13 | % | 13 | % | ||||||||||||

| #9 | C | 208 | 4.87 | Sep-19 | 13 | % | 10 | % | ||||||||||||

| #10 | C+ | 232 | 10.88 | Jun-19 | 13 | % | 11 | % | ||||||||||||

| #11 | B | 466 | 10.88 | Jun-19 | 18 | % | 14 | % | ||||||||||||

| #12 | B- | 504 | 2.67 | Jul-18 | 32 | % | 25 | % | ||||||||||||

| #13 | C | 168 | 9.25 | Dec-17 | 12 | % | 8 | % | ||||||||||||

| #14 | C | 332 | 10.09 | Jun-17 | 25 | % | 25 | % | ||||||||||||

| #15 | B | 254 | 8.41 | Dec-16 | 23 | % | 10 | % | ||||||||||||

| #16 | C+ | 205 | 2.93 | Oct-16 | 29 | % | 22 | % | ||||||||||||

| #17 | C | 69 | 8.67 | Aug-16 | 14 | % | 14 | % | ||||||||||||

| #18 | B- | 188 | 5.16 | Oct-12 | 32 | % | 25 | % | ||||||||||||

| #19 | B | 140 | 1.69 | Aug-12 | 97 | % | 61 | % | ||||||||||||

| #20 | C+ | 196 | 4.29 | Sep-10 | 24 | % | 20 | % | ||||||||||||

| #21 | C+ | 100 | 2.72 | Apr-10 | 25 | % | 21 | % | ||||||||||||

| #22 | C+ | 178 | 2.14 | Mar-09 | 42 | % | 27 | % | ||||||||||||

| #23 | C | 40 | 3.16 | Sep-08 | 54 | % | 48 | % | ||||||||||||

| #24 | C | 24 | 0.48 | Jun-07 | 114 | % | 114 | % | ||||||||||||

| #25 | C+ | 20 | 2.24 | Dec-05 | 55 | % | 55 | % | ||||||||||||

| #26 | C+ | 39 | 3.3 | Jul-05 | 36 | % | 26 | % | ||||||||||||

| #27 | C | 24 | 2.24 | Jul-05 | 97 | % | 64 | % | ||||||||||||

| #28 | C+ | 45 | 2.46 | Apr-05 | 31 | % | 21 | % | ||||||||||||

Page | 14

| Property | Project ROI | Investor ROI | Project MOIC | Investor MOIC | Average Annual CoC | |||||||||||||||

| #1 - #5 | 92 | % | 69 | % | 1.92 | 1.68 | 7.0 | % | ||||||||||||

| #6 | 108 | % | 89 | % | 2.08 | 1.89 | 3.2 | % | ||||||||||||

| #7 | 36 | % | 5 | % | 1.36 | 1.05 | 1.0 | % | ||||||||||||

| #8 | 70 | % | 69 | % | 1.7 | 1.69 | 3.0 | % | ||||||||||||

| #9 | 77 | % | 50 | % | 1.77 | 1.5 | 4.0 | % | ||||||||||||

| #10 | 236 | % | 178 | % | 3.36 | 2.78 | 7.5 | % | ||||||||||||

| #11 | 434 | % | 290 | % | 5.34 | 3.9 | 10.0 | % | ||||||||||||

| #12 | 105 | % | 75 | % | 2.05 | 1.75 | 7.4 | % | ||||||||||||

| #13 | 150 | % | 80 | % | 2.5 | 1.8 | 2.8 | % | ||||||||||||

| #14 | 540 | % | 540 | % | 6.4 | 6.4 | 10.4 | % | ||||||||||||

| #15 | 168 | % | 115 | % | 2.68 | 2.15 | 5.0 | % | ||||||||||||

| #16 | 102 | % | 77 | % | 2.02 | 1.77 | 3.6 | % | ||||||||||||

| #17 | 50 | % | 50 | % | 1.5 | 1.5 | 6.8 | % | ||||||||||||

| #18 | 231 | % | 167 | % | 3.31 | 2.67 | 16.8 | % | ||||||||||||

| #19 | 195 | % | 100 | % | 2.95 | 2 | 7.0 | % | ||||||||||||

| #20 | 123 | % | 101 | % | 2.23 | 2.01 | 3.4 | % | ||||||||||||

| #21 | 131 | % | 108 | % | 2.31 | 2.08 | 5.3 | % | ||||||||||||

| #22 | 100 | % | 60 | % | 2 | 1.6 | 4.0 | % | ||||||||||||

| #23 | 251 | % | 216 | % | 3.51 | 3.16 | 7.6 | % | ||||||||||||

| #24 | 114 | % | 114 | % | 2.14 | 2.14 | 0.0 | % | ||||||||||||

| #25 | 169 | % | 169 | % | 2.69 | 2.69 | 0.0 | % | ||||||||||||

| #26 | 143 | % | 95 | % | 2.43 | 1.95 | 6.5 | % | ||||||||||||

| #27 | 279 | % | 116 | % | 3.79 | 2.16 | 9.3 | % | ||||||||||||

| #28 | 116 | % | 73 | % | 2.16 | 1.73 | 8.9 | % | ||||||||||||

In addition, the other nine projects – the nine that have not yet completed their “round trip” – have paid an aggregate of $29.3 million to investors, either as a return of capital or as profit.

Property Class

In the world of real estate investing, properties and locations are ranked on a scale from A to D, with A best and D worst. Our ranking combines both the location of the project and its condition.

Internal Rate of Return (IRR)

Internal rate of return, or IRR, measures the financial performance of an investment taking into account the time the investment is held. For example, suppose that a bond costs $100, pays $10 at the end of each year for four years, and is redeemed after five years for $110. The IRR of that bond is 10%. But if the only payment on the bond were $150 at the end of the fifth year, the IRR would drop to 8.45%, even though the investor had still received a total of $150. The reason: the investor had to wait longer for her money.

Return on Investment (ROI)

Return on investment, or ROI is a fraction, where the numerator (the top of fraction) is the total distributions from the investment minus the total contributions to the investment, and the denominator (the bottom of the fraction) is the total contributions to the investment. For example, if an investment is capitalized with $100 and returns $135, the ROI is 135%.

Multiple on Invested Capital (MOIC)

Multiple on invested capital, or MOIC, is a fraction, the numerator of which is the total amount returned from the investment and the denominator of which is the total amount invested. For example, if an investment is purchased for $100 and is later sold for $225, net of expenses, the MOIC is 2.25.

Page | 15

Average Annual Cash-on-Cash Return (CoC)

Cash-on-cash return, or CoC, for any year, is a fraction, the numerator of which is the cash flow generated by an investment for that year minus the total amount invested as of that year (not counting borrowed money). For example, if the investment generates $9 for 2015 and the total cash investment as of 2015 was $100, the CoC for 2015 was 9%. The average annual CoC simply takes the average over the life of the investment.

Project-Level vs. Investor-Level Calculations

We have calculated IRR, ROI, and MOIC in two ways: first from the perspective of the project as a whole, and then from the perspective of investors. For example, suppose a property cost $100, all funded by investors, and were sold after one year for $120, with investors receiving a return of their $100 of capital plus 70% of the $20 profit, or $14, for a total of $114, and the sponsor receiving 30% of the $20 profit, or $6. The project would have an IRR of 20%, while investors would have an IRR of 14%.

Acquisitions of Properties Within Last Three Years

During the last three years, Casoro Group has purchased seven properties, with 2,090 rental units and an aggregate cost of over $260 million. For more detailed information, see Table VI of the prior performance tables.

For more information about all the Programs please refer to Appendix A– Results of Prior Programs, below. The information in Appendix A is presented as of December 31, 2022.

The Company is currently treated as a Real Estate Investment Trust, or “REIT,” and intends to remain so.

Until January 2, 2022, the Company did not qualify as a REIT because too few people owned too much of its stock. However, the failure of the Company to qualify as a REIT did not harm the Company or its investors.

A REIT is just a tax concept: an entity that is treated as a corporation for federal income tax purposes and satisfies a long list of requirements listed in section 856 of the Internal Revenue Code. These requirements include:

| ● | The kinds of assets it owns |

| ● | The kind of income it generates |

| ● | Who owns it |

| ● | How much of its income it distributes to its owners |

A REIT is not a function of securities laws. Thus, many REITs have “gone public” by offering their securities in offerings that are registered under the Securities Act of 1933, while many other REITs are still private. Some “public” REITs have registered their shares on a national securities exchange, allowing the shares to be publicly traded, while the shares of other “public” REITs are traded privately. There are very large REITs and very small REITs, and everything in between. Some REITs invest in one class of real estate assets, others invest in completely different classes of real estate assets (e.g., only mortgages), and still others invest in multiple classes of real estate assets. The only thing all these companies have in common, being REITs, is that they all satisfy the requirement in section 856 of the Code.

The benefit of a REIT is just taxes:

| ● | If the Company were a regular limited liability company, not a REIT, then the income of the Company would be reported to Investors on Form K-1. Transferring the information from Form K-1 to his or her own personal tax return can be difficult and time-consuming. |

Page | 16

| ● | Conversely, if the Company were a corporation and did not qualify as a REIT, it would be subject to tax on its income at the corporate level, and investors would then be subject to tax again when the Company distributed its income, resulting in two levels of tax on the same income. |

| ● | As a REIT, the Company will not itself be subject to tax, and Investors will receive only a Form 1099 to report their income from the Company. |

If you are interested, you can read much more detailed information about the tax treatment of REITs in “Federal Income Tax Consequences.”

The Company is a limited liability for purposes of state law but has elected to be treated as a corporation for federal income tax purposes. That’s what allows the Company to be treated as a REIT.

| Name | Age | Position | Term of Office | Approximate Hours Per Week If Not Full Time | ||||

| Monte Lee-Wen | 46 | Chief Executive Officer | 08/01/2006 Indefinite |

Full Time | ||||

| Nalie Lee-Wen | 46 | Chief Financial Officer | 08/01/2006 Indefinite |

Full Time | ||||

Mehul Chavada

|

39 | Chief Investment Officer | Started 01/16/2023 At Will |

Full Time | ||||

| Dustin Gabriel | 38 | Director of Investor Relations | Started 03/06/2023 At Will |

Full Time | ||||

| Lea Allen | 35 | Controller | Started 02/22/2022 At Will |

Full Time |

NOTE: All these individuals are employed by Casoro Capital Partners, LLC, the Sponsor, not by the Company directly. Each works full time for the Sponsor, but that doesn’t mean they spend all their time on the Company’s business.

Monte K. Lee-Wen

CEO

As CEO, Monte is responsible for the overall leadership, growth, and business development. Monte Wen is a Principal of the Manager and an owner of the Sponsor. Monte has executed over $600 million in transactions, acquiring, managing, and repositioning commercial property across the United States. He is the Chairman of Casoro Group, LLC, a multi-housing real estate investment company which merged with The PPA Group in 2019. Casoro Group is headquartered in Austin, Texas and also serves as a holding company for Casoro Group family of companies. He has a unique investment philosophy which involves evaluating and taking advantage of opportunities where superior risk-adjusted returns can be realized.

Through founding The PPA Group, Monte has been able to combine his investment experience and philosophy with the creative talent required to renovate and reposition properties. Monte brings an extensive knowledge in property assessment and transaction due diligence. He has created a standardized internal analysis system to effectively evaluate investment properties which has enabled Casoro Group to streamline the process of acquiring profitable real estate investments.

In 2008, Monte formed a subsidiary company called PPA Real Estate Management (“REM”) to serve as the property management company for The PPA Group’s real estate holdings and to conduct third-party fee management business. REM currently manages a diverse portfolio of multi-housing properties. Monte takes pride in investing not only in properties, but also in the communities and families that reside at the company’s properties.

Monte is a seasoned entrepreneur having started and run several companies:

| ● | CLEAR Property Management, LLC - January 2008 |

| ● | United Equity Ventures, LLC - 2009 |

| ● | Ingenium Construction Company, LLC - November 2011 |

| ● | Performance Utility Management & Billing, LLC - February 2013 |

| ● | Casoro Capital, LLC - May 2015 |

Page | 17

His networking and speaking skills have propelled the company forward very quickly. He is actively involved in board positions and guidance committees of many private and public initiatives nationwide. During the last five years, Monte has held Board/Committee positions on the following organizations:

| ● | Athletes for Change - a Glenn Heights, Texas organization focused on guiding and mentoring kids through interactions and relationships with professional athletes |

| ● | Thinkery - a children’s museum located in Austin, Texas |

| ● | IronShore Properties, LLC - a commercial real estate investment company. |

Nalie Lee-Wen

Chief Financial Officer

As CFO, Nalie Lee-Wen heads Casoro Group’s internal finance department. She specializes in developing profitable relationships with capital partners and coordinating seamless transactions during the funding and closing phase of Casoro’s acquisitions.

Nalie oversees the team of accounting professionals for Casoro Group and its family of companies, including CLEAR Property Management. Her experience in commercial financing and lender relationships contributes significant value to the company’s operational management. She also plays a pivotal role in the asset management and property management departments.

Starting as a family office alongside Monte Lee-Wen, they have grown Casoro Group into a vertically integrated owner / operator and private equity investor on behalf of institutions. The company serves as a holding company for the Casoro Group family of companies, including CLEAR Property Management, Performance Utilities and Billing, Ingenium Construction, and Upside Avenue, a public non-traded multifamily REIT.

Prior to founding the company, Nalie served as the Chief Executive Officer of a commercial real estate funding group. Nalie has more than 10 years of experience in real estate financing, asset management, and portfolio management. Her strong background in real estate and finance has afforded Nalie with a singular talent for anticipating potential problems and creating effective solutions that stop asset acquisitions issues in their tracks — before they can derail a deal.

Nalie’s high level of expertise in working with state and local governments, surveyors, vendors, lenders, and legal professionals further empowers her to resolve title issues and move acquisitions over the finish line.

Nalie currently sits on the board of Casoro Group Education Foundation.

Mehul Chavada

Chief Investment Officer

Mehul joined the team at Casoro Group in January 2023. He is responsible for strategizing and executing the firm’s growth strategy in investing in real assets that meet or exceed performance thresholds. Mehul specializes in identifying and acquiring multifamily investments throughout the United States for Casoro Group’s institutional, family office, and high-net-worth clients, as well as its discretionary non-traded multifamily income REIT, Upside Avenue.

With more than 15 years of commercial transaction experience, Mehul brings deep expertise in the acquisition and asset management of multiple asset types, including multifamily, student housing, industrial, office, and retail. Mehul has also built close relationships with some of the world’s largest sovereign wealth funds, pension funds and family offices. Most recently during 2020 through 2022, he was Head of Investments at Nitya Capital in Houston, a firm with over $2.5 billion of assets under management in multifamily, office and retail assets. Previously, as Director – Fund Management at Hines from 2015 through 2020, one of the largest privately held global real estate investors and managers, he managed several funds including opportunistic, value-added and sustainable income fund strategies. Prior to joining Hines, Mehul led a real estate development business which focused on residential and mixed-use projects. He has contributed to the investment and development of more than 17 million square feet of commercial real estate across Americas, Europe and Asia. At Casoro Group, Mehul plays a crucial role in developing the firm’s market presence, uncovering profitable opportunities, leading the underwriting, structuring, negotiation, and closing of new acquisitions. Mehul also oversees the company’s equity and debt capital raising activities.

He holds a M.S. in Civil Engineering from Virginia Tech, and an M.S. in Real Estate from Massachusetts Institute of Technology. Mehul is also an adjunct professor teaching Real Estate Private Equity at Rice University’s Jones Graduate School of Business.

Page | 18

Dustin Gabriel

Director of Investor Relations

Dustin will be focused on investor communication, experience and capital raising for Upside Avenue as well as assisting with broader capital markets activities. He has a diversified background from sponsorship, investment, finance and management perspectives. He joins from a structured finance company owned by Apollo and Bank OZK’s Real Estate Specialties Group. He also has a background syndicating CRE deals and he raised the capital to co-sponsor in the acquisition and development of suburban class A office buildings, land assemblage and a multifamily rehab.

Dustin holds a Bachelor of Science and MPA with Finance Emphasis from Brigham Young University.

Lea Allen

Controller

Lea Allen joined the team at Casoro Group in February 2022. She serves as the Corporate Controller for Upside Avenue where she is responsible for all accounting matters related to corporate, property asset management and fund level functions. With over a decade of experience in the field, Lea provides expertise in accounting and strong knowledge of financial reporting.

Prior to joining Casoro Group, Lea served as Controller for Secured Investment Corp, a top peer to peer real estate lending company and private equity fund manager. During this time, Lea was responsible for leading the accounting and reporting functions for the corporate family of companies as well as for the private equity funds managed by the company. Her tenure at Secured Investment Corp spanned from 2012 through 2022 where she held multiple accounting positions. During her time there she worked on both funds they had since inception, totaling in millions of loans originated and hundreds of SFR assets purchases and fixed. Her private equity fund experience spans both Regulation D and Regulation A+ funds and her investment fund experience includes a portfolio of first trust deeds (mortgages) and single-family residences.

Lea holds a BBA in Accountancy from Gonzaga University.

The Sponsor owns 70% of Casoro Investment Advisory Firm, LLC, the Manager of the Company. The PPA Group LLC owns 100% of the Sponsor.

Nalie Lee-Wen is the CFO of the Casoro Group, and wife of Monte Lee-Wen. Monte Lee-Wen is the majority owner of our sponsor Casoro Investment Advisory Firm, LLC.

Within the last five years, no Executive Officer or Significant Employee of the Company has been convicted of, or pleaded guilty or no contest to, any criminal matter, excluding traffic violations and other minor offenses.

Within the last five years, no Executive Officer or Significant Employee of the Company, no partnership of which an Executive Officer or Significant Employee was a general partner, and no corporation or other business association of which an Executive Officer or Significant Employee was an executive officer, has been a debtor in bankruptcy or any similar proceedings.

Within the last five years, no Executive Officer or Significant Employee of the Company, no partnership of which an Executive Officer or Significant Employee was a general partner, and no corporation or other business association of which an Executive Officer or Significant Employee was an executive officer, has been involved as a defendant in a lawsuit arising from real estate transactions.

Page | 19

SUMMARY OF MANAGEMENT AGREEMENT

The Company entered into an agreement captioned “Management Services Agreement” with the Manager effective on May 1, 2022 (the “Management Agreement”). The following summarizes some of the key terms of the Management Agreement. However, this summary is qualified by the Management Agreement itself, a copy of which is attached as Exhibit 1A-6A.

Duties of Manager

The duties of the Manager fall into several categories:

| ● | Investment Management: The Manager is responsible for all aspects of the Company’s investing activities, including developing investment guidelines, evaluating possible investments, conducting due diligence, arranging financing, and evaluating possible sales. |

| ● | Capital Formation: The Manager is responsible for managing and supervising one or more offerings of securities on behalf of the Company, including this Offering. |

| ● | Asset Management: The Manager is responsible for managing and monitoring the assets of the Company. |

| ● | Accounting and Administrative: The Manager is responsible for maintaining the books and records of the Company. |

| ● | Member Services: The Manager is responsible for shall managing and coordinating distributions and payments to Members; distributing reports, updates, and other information to Members; handling redemption requests from Members; and provide services in the nature of investor relations. |

Compensation of Manager

As compensation for its services under the Management Agreement, the Manager is entitled to a fee equal to one-half of one percent (0.5%) of the Company’s net asset value as of the last day of the previous quarter.

Term of Management Agreement

The Management Agreement will remain in effect for as long as the Manager is the manager of the Company.

Page | 20

The people who run the Company make money from the Company in (only) two ways:

| ● | They receive fees |

| ● | They invest alongside Investors and receive the same distributions as Investors |

Both forms of compensation are discussed below.