AN OFFERING STATEMENT PURSUANT

TO REGULATION A RELATING TO THESE SECURITIES HAS BEEN FILED WITH

THE SECURITIES AND EXCHANGE COMMISSION. INFORMATION CONTAINED IN

THIS PRELIMINARY OFFERING CIRCULAR IS SUBJECT TO COMPLETION OR

AMENDMENT. THESE SECURITIES MAY NOT BE SOLD NOR MAY OFFERS TO BUY

BE ACCEPTED BEFORE THE OFFERING STATEMENT FILED WITH THE COMMISSION

IS QUALIFIED. THIS PRELIMINARY OFFERING CIRCULAR SHALL NOT

CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY

NOR MAY THERE BE ANY SALES OF THESE SECURITIES IN ANY STATE IN

WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE UNLAWFUL BEFORE

REGISTRATION OR QUALIFICATION UNDER THE LAWS OF SUCH STATE. THE

COMPANY MAY ELECT TO SATISFY ITS OBLIGATION TO DELIVER A FINAL

OFFERING CIRCULAR BY SENDING YOU A NOTICE WITHIN TWO BUSINESS DAYS

AFTER THE COMPLETION OF THE COMPANY’S SALE TO YOU THAT

CONTAINS THE URL WHERE THE FINAL OFFERING CIRCULAR OR THE OFFERING

STATEMENT IN WHICH SUCH FINAL OFFERING CIRCULAR WAS FILED MAY BE

OBTAINED.

PRELIMINARY OFFERING CIRCULAR DATED JANUARY 19,

2018

Bitzumi, Inc.

55 5th Avenue, Suite

1702

New York, NY 10003

646-741-9600

4,000,000 shares

of Common Stock, par value $0.0001

SEE “DESCRIPTION OF CAPITAL STOCK” AT PAGE

58

|

|

Price to Public

|

Broker-Dealer discount and commissions

|

Proceeds to issuer

|

Proceeds to other persons

|

|

Per share/unit

|

$ 2.50

|

0.5%

|

$ 2.25

|

$ 0

|

|

Total Minimum

|

$1,000,000

|

$13,000

|

$900,000

|

$ 0

|

|

Total Maximum

|

$10,000,000

|

$58,000

|

$9,000,000

|

$ 0

|

The issuer will pay the expenses of the offering; which it

estimates to be $120,000. See “Plan of

Distribution.”

The company has engaged Sageworks Capital, LLC, member FINRA/SIPC

(the “Broker-Dealer” or “Broker”) to assist

in the placement of its securities. See “Plan of

Distribution; Selling Security Holders” for details of

compensation paid to the Broker.

$1,000,000 MINIMUM OFFERING AMOUNT (400,000 SHARES OF COMMON

STOCK).

$10,000,000 MAXIMUM OFFERING AMOUNT (4,000,000 SHARES OF COMMON

STOCK).

The company has engaged Prime Trust LLC as an escrow agent (the

“Escrow Agent”) to hold funds tendered by investors

in compliance with SEC Rules 15c2-4 and 10b-9. The

offering is being conducted on a best-efforts basis with a minimum

offering amount of $1,000,000. The offering will terminate at the

earlier of: (1) the date at which the maximum offering amount has

been sold, (2) the date which is one year from this offering being

qualified by the Commission, or (3) the date at which the offering

is earlier terminated by us in our sole discretion.

After the Offering Statement has been qualified by the Securities

and Exchange Commission, we will accept tenders of funds to

purchase the shares. The funds tendered by potential investors will

be held by Prime Trust LLC. If the minimum of $1,000,000 is not

raised, the Escrow Agent will return the funds to the investors.

See “Plan of Distribution; Investors’ Tender of

Funds.”

THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS

UPON THE MERITS OR GIVE ITS APPROVAL OF ANY SECURITIES OFFERED OR

THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR

COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SOLICITATION

MATERIALS. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION

FROM REGISTRATION WITH THE COMMISSION; HOWEVER THE COMMISSION HAS

NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED

ARE EXEMPT FROM REGISTRATION

GENERALLY NO SALE MAY BE MADE TO YOU IN THIS OFFERING IF THE

AGGREGATE PURCHASE PRICE YOU PAY IS MORE THAN 10% OF THE GREATER OF

YOUR ANNUAL INCOME OR NET WORTH. DIFFERENT RULES APPLY TO

ACCREDITED INVESTORS AND NON-NATURAL PERSONS. BEFORE MAKING ANY

REPRESENTATION THAT YOUR INVESTMENT DOES NOT EXCEED APPLICABLE

THRESHOLDS, WE ENCOURAGE YOU TO REVIEW RULE 251(d)(2)(i)(C) OF

REGULATION A. FOR GENERAL INFORMATION ON INVESTING, WE ENCOURAGE

YOU TO REFER TO www.investor.gov.

This offering is inherently risky. See “Risk Factors”

on page 9.

Sales of these securities will commence on approximately _________,

2018.

The company is following the Form S-1 format of disclosure under

Regulation A.

TABLE OF CONTENTS

|

Page

|

|

|

|

|

|

2

|

|

|

|

|

|

9

|

|

|

|

|

|

28

|

|

|

|

|

|

30

|

|

|

|

|

|

32

|

|

|

|

|

|

34

|

|

|

|

|

|

47

|

|

|

|

|

|

53

|

|

|

|

|

|

54

|

|

|

|

|

|

55

|

|

|

|

|

|

56

|

|

|

|

|

|

57

|

|

|

|

|

|

61

|

|

|

|

|

|

62

|

|

|

|

|

|

63

|

|

|

|

|

|

66

|

|

|

|

|

|

66

|

|

|

|

|

|

67

|

In this Offering Circular, the term “Bitzumi” or

“the company” refers to Bitzumi, Inc. and its

subsidiaries.

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

THIS

OFFERING CIRCULAR MAY CONTAIN FORWARD-LOOKING STATEMENTS AND

INFORMATION RELATING TO, AMONG OTHER THINGS, THE COMPANY, ITS

BUSINESS PLAN AND STRATEGY, AND ITS INDUSTRY. THESE FORWARD-LOOKING

STATEMENTS ARE BASED ON THE BELIEFS OF, ASSUMPTIONS MADE BY, AND

INFORMATION CURRENTLY AVAILABLE TO THE COMPANY’S MANAGEMENT.

WHEN USED IN THE OFFERING MATERIALS, THE WORDS

“ESTIMATE,” “PROJECT,”

“BELIEVE,” “ANTICIPATE,”

“INTEND,” “EXPECT” AND SIMILAR EXPRESSIONS

ARE INTENDED TO IDENTIFY FORWARD-LOOKING STATEMENTS, WHICH

CONSTITUTE FORWARD LOOKING STATEMENTS. THESE STATEMENTS REFLECT

MANAGEMENT’S CURRENT VIEWS WITH RESPECT TO FUTURE EVENTS AND

ARE SUBJECT TO RISKS AND UNCERTAINTIES THAT COULD CAUSE THE

COMPANY’S ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE

CONTAINED IN THE FORWARD-LOOKING STATEMENTS. INVESTORS ARE

CAUTIONED NOT TO PLACE UNDUE RELIANCE ON THESE FORWARD-LOOKING

STATEMENTS, WHICH SPEAK ONLY AS OF THE DATE ON WHICH THEY ARE MADE.

THE COMPANY DOES NOT UNDERTAKE ANY OBLIGATION TO REVISE OR UPDATE

THESE FORWARD-LOOKING STATEMENTS TO REFLECT EVENTS OR CIRCUMSTANCES

AFTER SUCH DATE OR TO REFLECT THE OCCURRENCE OF UNANTICIPATED

EVENTS.

Industry and Market Data

Although

we are responsible for all disclosure contained in this Offering

Circular, in some cases we have relied on certain market and

industry data obtained from third-party sources that we believe to

be reliable. Market estimates are calculated by using independent

industry publications in conjunction with our assumptions regarding

the Bitcoin industry and market. While we are not aware of any

misstatements regarding any market, industry or similar data

presented herein, such data involves risks and uncertainties and is

subject to change based on various factors, including those

discussed under the headings “Statement Regarding

Forward Looking Statements” and “Risk

Factors” in this Offering Circular.

This summary highlights selected information contained elsewhere in

this Offering Circular. This summary is not complete and does not

contain all the information that you should consider before

deciding whether to invest in our Common Stock. You should

carefully read the entire Offering Circular, including the risks

associated with an investment in the company discussed in the "Risk

Factors" section of this Offering Circular, before making an

investment decision. Some of the statements in this Offering

Circular are forward looking statements. See the section

entitled "Statement Regarding Forward Looking

Statements."

Company Information

The

company was organized on June 13, 2017 under the laws of the State

of Delaware. Our principal executive office is located at 55 Fifth

Avenue, New York, NY 10003, and our telephone number is

646-741-9600. Our website address is www.bitzumi.com.

We do not incorporate the information on or accessible through our

website into this Offering Circular, and you should not consider

any information on, or that can be accessed through, our website or

that of Ebit News a part of this Offering Circular.

On July

24, 2017, we launched a beta version 1.1 of www.bitzumi.com to test our

exchange and wallet on a limited basis. On September 22, 2017, we

registered with FinCen as a money services business and are in the

process of obtaining licenses as a money transmitter business in

each of the 50 states. We anticipate having a public launch of

www.bitzumi.com by

early 2018.

On July

24, 2017, we launched a beta version of www.ebitnews.com to develop a

cryptocurrency publication business.

Our Business

Bitzumi

is a vertically-integrated Bitcoin exchange and marketplace. Our

mission is to drive growth to the cryptocurrency industry. We

plan to launch our business divisions with a phased approach.

Initially, our primary focus will be to develop a publishing and

marketing company to educate potential Bitzumi exchange/wallet

consumers, and to gain name recognition. We intend to deliver users

to Bitzumi’s and affiliates’ crypto-related offerings

and products. Ultimately, we intend for our primary product to be

our cryptocurrency exchange and digital storage on www.bitzumi.com.

We also plan to develop various educational and information

products and newsletters focusing on the cryptocurrency

industry.

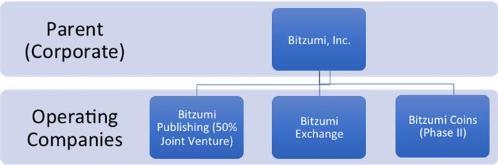

Below

is an overview of the Bitzumi’s corporate

structure.

We

anticipate implementing a two-phased approach to our business

model. Phase I is to focus on developing an online presence to

direct users and traffic to our targeted crypto-related

products. In Phase II

(following the public launch of our exchange), we plan to evaluate

blockchain technologies and other growth initiatives, including

developing our Bitzumi Coins division. Since we believe the most

prominent use case for blockchain technologies is digital

currencies, we expect to create special purpose coins for

particular industries as our focus in Phase II. We anticipate

continuing to evaluate other blockchain technology opportunities,

as well as technologies that are complementary to our business

strategy in an effort to minimize risks and enhance shareholder

value. This will include evaluating opportunities that diversify

our revenue streams, provide other consumer services and provide

on-ramps for new users.

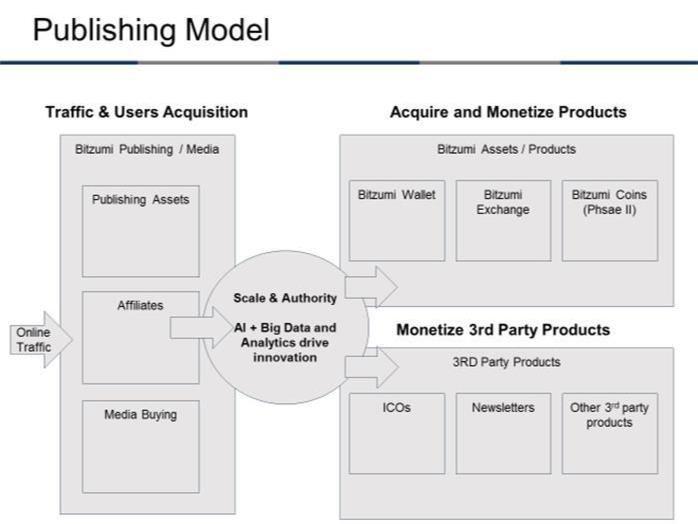

Below

is an illustration our business model:

Our Products

Phase I: Publication / News Portal

Our

publication business is intended to educate consumers on

cryptocurrency and blockchain technology. It is expected to

function as a news aggregation site as well as publishing original

content. On June 27, 2017, we launched beta version of the site at

www.ebitnews.com.

We plan to acquire and/or partner with other news portals to become

the leading news and information publisher for the cryptocurrency

industry. Our business model anticipates initially deriving revenue

from subscriptions and to later generate revenue from marketing as

well.

On

October 4, 2017, we entered into a 50% joint venture with Ibis

Venture Partners, LLC (“Ibis Venture”) and formed

Bitzumi Publishing, LLC, a New York limited liability company

(“Bitzumi Publishing”), with the intention to market

and sell various cryptocurrency newsletters and related

informational and educational products.

On

October 9, 2017, Bitzumi Publishing partnered with Agora Financial,

LLC to market and sell a newsletter created by James Altucher, one

of our co-founders. Bitzumi Publishing’s goal is to dominate

search engine traffic in the cryptocurrency industry and drive

traffic to both our Bitzumi exchange and other product offerings,

such as subscription-based newsletters.

On January 10, 2018, Bitzumi entered into a joint venture and

servicing agreement with Acacia Research Corporation

(“Acacia”) to create a patent registration platform

using Blockchain technology. In addition, Acacia and Bitzumi have

agreed to a strategic investment by Acacia. See

“Management’s Discussion and

Analysis.”

Phase II: Exchange and Wallet

We

intend Bitzumi to be a cryptocurrency exchange that provides a

reliable and secure way to buy, sell, store, and trade to and from

the following fiat and digital currencies: US dollars

(“USD”), Bitcoin (“BTC”), Litecoin

(“LTC”), and Ethereum (“ETH”). Bitzumi is

expected to provide 24/7 access to customers’ digital wallets

as well as liquidity into USD through integration with customer

debit cards.

We

intend that Bitzumi will focus on four key elements to distinguish

itself from its competitors: security, customer support, a mix of

advanced and simple trading tools, and most importantly, liquidity.

We plan for our business model to focus on growth through customer

acquisitions and marketing of our platform.

Payment Processing and Escrow

We plan

to develop processing and escrow technology to facilitate the use

of cryptocurrency in various industries. The platform is under

development and we anticipate that it will be launched in

2018.

Market Overview

Bitcoin, Ethereum, and Litecoin

Bitcoins,

Ethereum, and Litecoins are cryptocurrency, or digital commodities

that are based on an open source protocol. Cryptocurrency is not

issued by any government, bank, or central organization, but

instead exists on an online, peer-to-peer computer network.

Each cryptocurrency has its own network (such as the Bitcoin

Network, the Ethereum Network, and the Litecoin Network), which

hosts a public transaction ledger where its respective

cryptocurrency (respectively, Bitcoin, Ether, and Litecoin)

transfers are recorded (the “Blockchain”). The

Blockchain is a public record of the creation, custody, and flow of

funds of cryptocurrency, and shows every transaction effected on

the Blockchain among users’ online “digital

wallets.” Digital wallets store cryptocurrency, and

cryptocurrency may be sent or received through users’ digital

wallets by using public and private keys that are part of the

particular cryptocurrency’s network’s cryptographic

security mechanism.

Software

is used to access the cryptocurrency networks, and to create, move,

and own cyrptocurrency. Bitcoins, Ether, and Litecoins have no

physical existence beyond the record of transactions on the

Blockchain.

Bitcoin History

The

first decentralized cryptocurrency was Bitcoin, which was created

in 2009. Bitcoin is still the most prominent cryptocurrency today.

The Bitcoin Network is a recent technological innovation, and the

Bitcoins that are created, transferred, used, and stored by

entities and individuals have certain features associated with

several types of assets, most notably commodities, securities, and

currencies. Many U.S. regulators, including the Financial Crimes

Enforcement Network of the U.S. Department of the Treasury

(“FinCEN”), the U.S. Securities and Exchange Commission

(“SEC”), the U.S. Commodity Futures Trading Commission

(“CFTC”), the U.S. Internal Revenue Service

(“IRS”), and state regulators, including the New York

Department of Financial Services (“NYDFS”), have made

official pronouncements or issued guidance or rules regarding the

treatment of Bitcoins and other digital currencies, and may offer

additional guidance or rules in the future. Other U.S. and state

agencies have not made official pronouncements or issued guidance

or rules regarding the treatment of Bitcoins. The treatment of

Bitcoins and other digital currencies is often uncertain or

contradictory in other countries. The regulatory uncertainty

surrounding the treatment of Bitcoins and similar cryptocurrencies

creates risks for the company. See “Risk Factors Related to

Regulation.”

The Offering

|

Issuer:

|

Bitzumi,

Inc.

|

|

Securities offered by the company:

|

Common

Stock, par value $0.0001

|

|

Securities offered by selling stockholders:

|

None

|

|

Number of shares of Common Stock outstanding before the

offering:

|

111,076,211

|

|

Number of shares of Common Stock to be outstanding after the

offering:

|

115,076,211

|

|

Price per share:

|

$2.50

|

|

Minimum offering amount:

|

$1,000,000

|

|

Maximum offering amount:

|

$10,000,000

|

|

Use of proceeds:

|

We

intend to use the proceeds towards offering expenses, software

development, marketing and advertising, licensing and regulatory

compliance, operational and customer support, public company and

corporate costs, research and development and other application

development, and working capital.

|

Risk factors

Risk Factors Related to the company

●

We have an evolving

business model.

●

We have a limited

operating history and a history of operating losses, and expect to

incur significant additional operating losses.

●

We may need to

secure additional financing.

●

Any valuation at

this stage is difficult to assess.

●

Any inability to

attract and retain additional personnel could affect our ability to

successfully grow our business.

●

Loss of employees

or contractors could affect our ability to successfully grow our

business.

●

State licensing

procedures are lengthy and expensive.

●

We may need to

implement additional finance and accounting systems, procedures and

controls as we grow our business and organization and to satisfy

new reporting requirements.

●

Our auditors have

issued a “going concern” audit opinion.

●

We have not

conducted an evaluation of the effectiveness of our internal

control over financial reporting and will not be required to do so

until we are a public company. If we are unable to implement and

maintain effective internal control over financial reporting

investors may lose confidence in the accuracy and completeness of

our financial reports and the market price of our Common Stock may

be negatively affected.

●

Conflicts of

interest may occur.

●

Our stock price may

be volatile.

●

We have not paid

cash dividends in the past and do not expect to pay dividends in

the future. Any return on investment may be limited to the value of

our Common Stock.

●

There is currently

no trading market for our Common Stock and we cannot ensure that

one will ever develop or be sustained.

●

You will experience

future dilution as a result of future equity

offerings.

●

We may be unable to

protect our proprietary technology or keep up with that of our

competitors.

●

We may not be able

to obtain trademark protection for our marks, which could impede

our efforts to build brand identity.

●

We may be accused

of infringing intellectual property rights of third

parties.

●

Implications of

Being an Emerging Growth Company As an emerging growth company, we

intend to take advantage of all of reduced reporting requirements

and exemptions, including the longer phase-in periods for the

adoption of new or revised financial accounting standards under the

JOBS Act. Our election to use the phase-in periods may make it

difficult to compare our financial statements to those of

non-emerging growth companies and other emerging growth companies

that have opted out of the phase-in periods.

Risk Factors Related to Cryptocurrency Networks and

Cryptocurrency

●

The value of

cryptocurrency and fluctuations in the price of cryptocurrency

could materially and adversely affect the business and investment

in the company.

●

The loss or

destruction of a private key required to access cryptocurrency may

be irreversible. Our loss of access to our private keys or our

experience of a data loss relating to the cryptocurrency we hold

could adversely affect an investment in our company.

●

We depend on third

parties to provide execution of our trading platform, Internet,

telecommunication and fiber optic network connectivity to the

customers in our data centers, and any delays or disruptions in

service could adversely affect an investment in us.

●

Power outages,

limited availability of electrical resources, and increased energy

costs could adversely affect our business.

●

The further

development and acceptance of cryptocurrency networks, which

represents a new and rapidly changing industry, are subject to a

variety of factors that are difficult to evaluate. The slowing or

stopping of the development or acceptance of digital currency

systems may adversely affect our business.

●

Currently, there is

relatively small use of cryptocurrency in the retail and commercial

marketplace in comparison to relatively large use by speculators,

thus contributing to price volatility that could adversely affect

an investment in us.

●

The acceptance of

Bitcoin network, Ethereum network, or Litecoin network software

patches or upgrades by a significant, but not overwhelming,

percentage of the users and miners in the respective networks could

result in a “fork” in the Blockchain, resulting in the

operation of two separate networks until such time as the forked

Blockchains are merged. The temporary or permanent existence of

forked Blockchains could adversely impact an investment in

us.

●

The open-source

structure of cryptocurrency network protocol means that the Core

Developers and other contributors to the protocol are generally not

directly compensated for their contributions in maintaining and

developing the protocol. A failure to properly monitor and upgrade

the protocol could damage the cryptocurrency network and an

investment in us.

●

If the awards of

cryptocurrency for solving blocks and transaction fees for

recording transactions are not sufficiently high to incentivize

miners, miners may respond in a way that reduces confidence in the

cryptocurrency networks, which could adversely affect an investment

in our company.

●

To the extent that

any miners cease to record transactions in solved blocks,

transactions that do not include the payment of a transaction fee

will not be recorded on the Blockchain until a block is solved by a

miner who does not require the payment of transaction fees. Any

widespread delays in the recording of transactions could result in

a loss of confidence in the cryptocurrency networks, which could

adversely impact an investment in us.

●

Intellectual

property rights claims may adversely affect the operation of

cryptocurrency networks.

●

The cryptocurrency

exchanges on which cryptocurrency trade are relatively new and, in

most cases, largely unregulated and may therefore be more exposed

to fraud and failure than established, regulated exchanges for

other products. To the extent that the cryptocurrency exchanges

representing a substantial portion of the volume in cryptocurrency

trading are involved in fraud or experience security failures or

other operational issues, such cryptocurrency exchanges’

failures may result in a reduction in the price of cryptocurrency

and can adversely affect an investment in us.

●

Our ability to

adopt technology in response to changing security needs or trends

poses a challenge to the safekeeping of our

cryptocurrency.

●

Security threats to

us could result in a loss of company’s cryptocurrency, or

damage to our reputation and our brand, each of which could

adversely affect an investment in us.

●

Cryptocurrency

transactions are irrevocable and stolen or incorrectly transferred

cryptocurrency may be irretrievable. As a result, any incorrectly

executed cryptocurrency transactions could render company liable to

lawsuits or criminal charges to the extent company facilitates bad

transactions, and thus, adversely affect an investment in

us.

●

Our cryptocurrency

may be subject to loss, damage, theft, or restriction on

access.

●

A loss of

confidence in our security system, or a breach of our security

system, may adversely affect us and the value of an investment in

us.

●

The limited rights

of legal recourse against us, and our lack of insurance protection

expose us and our shareholders to the risk of loss of our

cryptocurrency for which no person is liable.

●

Cryptocurrency held

by us are not subject to FDIC or SIPC protections.

●

We may not have

adequate sources of recovery if our cryptocurrency is lost, stolen,

or destroyed.

●

Political or

economic crises may motivate large-scale sales of cryptocurrency,

which could result in a reduction in cryptocurrency value and

adversely affect an investment in us.

●

The sale of our

cryptocurrency to pay expenses at a time of low cryptocurrency

prices could adversely affect an investment in us.

Risk Factors

Related to Publication Business

●

The further

development and acceptance of cryptocurrency, which represent a new

and rapidly changing industry, are subject to a variety of factors

that are difficult to evaluate. The slowing or stopping of the

development or acceptance of cryptocurrencies may adversely

affect our newsletter and an investment in our

company.

●

We face significant

competition across the media landscape, including from magazine

publishers, digital publishers, social media platforms, search

platforms, portals and digital marketing services, among others,

which we expect will continue, and as a result we may not be able

to maintain or improve our operating results.

●

Service disruptions

or failures of our or our vendors’ information systems and

networks as a result of computer viruses, misappropriation of data

or other malfeasance, natural disasters (including extreme

weather), accidental releases of information or other similar

events, may disrupt our business, damage our reputation or have a

negative impact on our results of operations.

●

Our business may

suffer if we cannot protect our intellectual

property.

●

Technology in the

media industry continues to evolve rapidly.

●

We face significant

competition. Many of our competitors and potential competitors have

larger customer bases, more established brand recognition and

greater financial, marketing, technological, and personnel

resources than we do, which could put us at a competitive

disadvantage. Additionally, some of our competitors and potential

competitors are better capitalized than we are and able to obtain

capital more easily, which could put us at a competitive

disadvantage.

●

Failure to maintain

our reputation for trustworthiness may harm our

business.

●

We rely heavily on

joint ventures for the success of our publication business, thus,

any problem with our joint venture relationships could have an

adverse impact on our business.

Risk Factors Related to Regulation

●

U.S. and

international regulatory changes or actions may restrict the use of

or impose heightened regulatory burdens on cryptocurrency or the

operation of cryptocurrency network based on currency, securities,

or commodities regulations in a manner that adversely affects an

investment in us.

●

It may be illegal

now, or in the future, to acquire, own, hold, sell or use

cryptocurrency in one or more countries, and ownership of, holding

or trading in or company’s securities may also be considered

illegal and subject to sanction.

●

Our business of

converting cryptocurrencies to US dollars and vice versa require

our registration as a “money services business” under

the regulations promulgated by FinCEN under the authority of the US

Bank Secrecy Act, and require the licensing or other registration

as a money transmitter (or equivalent designation) under state law

in any state in which we plan to operate. This process is lengthy

and expensive, and any delays could delay commencing operations and

cost additional money, which may have an adverse impact on the

operation of our company and investment in our

company.

●

If federal or state

legislatures or agencies initiate or release tax determinations

that change the classification of cryptocurrency as property for

tax purposes, such determination could have a negative tax

consequence on our company, and adversely affect investment in

us.

●

Legislative and

regulatory developments, including with respect to privacy, could

adversely affect our business.

Summary Financial Information

The

following table summarizes the relevant financial data for our

business and should be read with our financial statements, which

are included in this prospectus. We have not had any significant

operations to date, so only balance sheet data is

presented.

|

|

September

30, 2017

|

|

|

|

Actual

|

As Adjusted(5)

|

|

Balance

Sheet Data:

|

|

|

|

Working capital

(1)

|

$384,249

|

$10,326,249

|

|

Total

assets(2)

|

401,332

|

10,401,332

|

|

Total

liabilities(3)

|

-

|

58,000

|

|

Shareholders’

equity(4)

|

401,332

|

10,343,332

|

(1)

The “as

adjusted” calculation includes $10,000,000 cash from the

proceeds of this offering if the maximum amount is raised, plus

$401,332 of actual shareholders’ equity as of September 30,

2017, less $58,000 of deferred underwriting

commissions.

(2)

The “as

adjusted” calculation includes $10,000,000 net cash from the

proceeds of this offering, plus $401,332 of actual

shareholders’ equity as of September 30, 2017.

(3)

The “as

adjusted” calculation includes $58,000 of deferred

underwriting commissions.

(4)

The “as

adjusted” calculation.

(5)

The “as

adjusted” column gives effect to the “maximum offering

amount” of $10,000,000.

The SEC

requires the company to identify risks that are specific to its

business and its financial condition. The company is still subject

to all the same risks that all companies in its business, and all

companies in the economy, are exposed to. These include risks

relating to economic downturns, political and economic events and

technological developments. Additionally, early-stage companies are

inherently riskier than more developed companies. You should

consider general risks as well as specific risks when deciding

whether to invest.

Risk Factors Related to the Company

We have an evolving business model.

As

digital currencies and blockchain technologies evolve, so will our

business model. We may continue to try to offer additional types of

products or services, and we cannot offer any assurance that any of

them will be successful. From time to time we may also modify

aspects of our business model relating to our product mix and

service offerings. We cannot offer any assurance that these or any

other modifications will be successful or will not result in harm

to the business. We may not be able to manage growth effectively,

which could damage our reputation, limit our growth, and negatively

affect our operating results.

We have a limited operating history and a history of operating

losses, and expect to incur significant additional operating

losses.

We have

a limited operating history. Therefore, there is no historical

financial information on which to base an evaluation of our

performance. Our prospects must be considered in light of the

uncertainties, risks, expenses, and difficulties frequently

encountered by companies in their early stages of operations. We

have generated net losses of $51,167 for the period from June 13,

2017 (inception) through September 30, 2017. We expect to incur

significant additional losses over the next 12 months as we

continue to maintain and expand our existing operations. The amount

of future losses and when, if ever, we will achieve profitability

are uncertain. If we are unsuccessful at executing on our business

plan, our business, prospects, and results of operations may be

materially adversely affected.

We

are likely to need to secure additional financing.

We anticipate that we will incur operating losses for the

foreseeable future. Our historical cash burn rate for the period

from June 13, 2017 (inception) through September 30, 2017 was on

average approximately $14,000 per month, which included costs

associated with the build out of our exchange platform. As a

result, we expect that the cash we currently have on hand will fund

our operations through April 2018. As of September 30, 2017, we had

a cash position equal to $259,249. We are likely to require

additional funds for our anticipated operations and further

expansion and if we are not successful in securing additional

financing, we may be required to delay significantly, reduce the

scope of or eliminate one or more of our business activities,

downsize our general and administrative infrastructure, or seek

alternative measures to avoid insolvency. It is possible that

future offerings will be at a different valuation, especially if an

investor is a strategic investor and/or is willing to invest a

significant amount of funds.

Any valuation at this stage is difficult to assess.

The

valuation for the offering was established by the company. Unlike

listed companies that are valued publicly through market-driven

stock prices, the valuation of private companies, especially

startups, is difficult to assess and you may risk overpaying for

your investment.

Any inability to attract and retain additional personnel could

affect our ability to successfully grow our business.

Our

future success depends on our ability to identify, attract, hire,

train, retain and motivate other highly-skilled technical,

managerial, editorial, marketing and customer service personnel.

Competition for such personnel is intense. Our failure to retain

and attract the necessary technical, managerial, editorial,

marketing, and customer service personnel could harm our

business.

Loss of employees or contractors could affect our ability to

successfully grow our business.

Our

future success depends on our ability to retain certain key

employees and contractors related to software and blockchain

technology and development of proprietary content and newsletters

for our publications. Our failure to retain these relationships, or

adequately replace them in a timely manner, could harm our

business.

State licensing procedures are lengthy and expensive.

We are

required to obtain approval from federal and states regulatory

authorities to operate as a money servicer. The cost to do so may

exceed $1,000,000 and take 12-18 months to complete. We cannot

fully operate until we obtain these licenses, and any delay in

obtaining licenses could harm our business.

We may need to implement additional finance and accounting systems,

procedures and controls as we grow our business and organization

and to satisfy new reporting requirements.

We are

required to comply with a variety of reporting, accounting, and

other rules and regulations. Compliance with existing requirements

is expensive. Further requirements may increase our costs and

require additional management time and resources. We may need to

implement additional finance and accounting systems, procedures and

controls to satisfy our reporting requirements. If our internal

controls over financial reporting are determined to be ineffective,

such failure could cause investors to lose confidence in our

reported financial information, negatively affect the market price

of our Common Stock, subject us to regulatory investigations and

penalties, and adversely impact our business and financial

condition.

Our auditors have issued a “going concern” audit

opinion.

Our independent

auditors have indicated in their report on our September 30, 2017

financial statements that the company’s ability to continue

as a going concern is dependent on our ability to implement the

business plan, generate sufficient revenues, and to control

operating expenses. A “going concern” opinion indicates

that the financial statements have been prepared assuming we will

continue as a going concern and do not include any adjustments to

reflect the possible future effects on the recoverability and

classification of assets, or the amounts and classification of

liabilities that may result if we do not continue as a going

concern. Therefore, you should not rely on our balance sheet as an

indication of the amount of proceeds that would be available to

satisfy claims of creditors, and potentially be available for

distribution to stockholders, in the event of

liquidation.

We have not conducted an evaluation of the effectiveness of our

internal control over financial reporting and will not be required

to do so until we are a public company. If we are unable to

implement and maintain effective internal control over financial

reporting investors may lose confidence in the accuracy and

completeness of our financial reports and the market price of our

Common Stock may be negatively affected.

We hope

to list as a public company eventually, and at that time various

accounting rules applicable to public companies will apply to us.

We are uncertain that we have the procedures in place to make sure

we meet those requirements, and compliance will be a burden. If and

when required, our independent registered public accounting firm is

unable to express an opinion as to the effectiveness of our

internal control over financial reporting, at that time, investors

may lose confidence in the accuracy and completeness of our

financial reports and the market price of our Common Stock could be

negatively affected, and we could become subject to investigations

by the stock exchange on which our securities are listed, the SEC,

or other regulatory authorities, which could require additional

financial and management resources.

Conflicts of interest may occur.

Our

chief executive officer, Scot Cohen, is involved in oil and gas and

other companies including being the executive chairman of both

Petro River Oil Corp and Wrap Technologies. He is also the managing

member of various oil and gas related special purpose entities and

a member of the Board of Directors of True Drinks,

Inc. In the event such positions and interest results in

a conflict of interest between us and any of these other entities,

he could potentially make decisions that are not in the best

interest of the shareholders of the company.

To the

extent that such other companies may participate in ventures in

which we may desire to participate or the amount of time and

attention we require overlaps with the needs of such other

companies, Mr. Cohen may have a conflict of interest. Our

Board of Directors and Mr. Cohen will attempt to minimize such

conflicts. In determining whether or not our interests

conflict with those of Mr. Cohen, our disinterested directors will

primarily consider the potential benefits to us, the degree of risk

to which we may be exposed and its financial position at that time.

Other than as indicated, the company has no other procedures

or mechanisms to deal with conflicts of interest. It is possible

that the existence of potential conflicts or decisions made in

connection with such conflicts could adversely affect the price of

our Common Stock and could cause the price to be less than it might

have been if the conflicts did not exist or were avoided. Mr. Cohen

will split his time equally between Bitzumi and his other business

interests.

Our stock price may be volatile.

The

market price of our Common Stock, if and when trading begins, is

likely to be highly volatile and could fluctuate widely in price in

response to various factors, many of which are beyond our control,

including the following:

●

Changes to the

Bitcoin industry, including value of Bitcoin and demand for

Bitcoin;

●

We may not be able

to compete successfully against current and future

competitors;

●

Competitive pricing

pressures;

●

Our ability to

obtain working capital financing;

●

Additions or

departures of key personnel;

●

Sales of our Common

Stock;

●

Our ability to

execute our business plan;

●

Operating results

that fall below expectations;

●

Loss of any

strategic relationship, including our joint venture partner in

Bitzumi Publishing;

●

Regulatory

developments, particularly those affecting cryptocurrency;

and

●

Economic and other

external factors.

In

addition, the securities markets have from time to time experienced

significant price and volume fluctuations that are unrelated to the

operating performance of particular companies. These market

fluctuations may also materially and adversely affect the market

price of our Common Stock. As a result, you may be unable to resell

your shares at a desired price.

We have not paid cash dividends in the past and do not expect to

pay dividends in the future. Any return on investment may be

limited to the value of our Common Stock.

We have

never paid cash dividends on our Common Stock and do not anticipate

doing so in the foreseeable future. The payment of dividends on our

Common Stock will depend on earnings, financial condition and other

business and economic factors affecting us at such time as our

board of directors may consider relevant. If we do not pay

dividends, our Common Stock may be less valuable because a return

on your investment will only occur if our stock price

appreciates.

There is currently no trading market for our Common Stock and we

cannot ensure that one will ever develop or be

sustained.

There

is no current market for any of our shares of stock and a market

may not develop. We hope to list our Common Stock on the Nasdaq

Capital Market (“NASDAQ”) if we raise enough money in

this offering, but there is no guarantee that we will be able to do

so. See “Implications of being an emerging growth

company.” If not listed on NASDAQ, shares of Common Stock,

when issued, may be traded on the over-the-counter market to the

extent any demand exists. Even if listed on NASDAQ, a liquid

trading market may not develop. Investors should assume that they

may not be able to liquidate their investment for some time, or be

able to pledge their shares as collateral.

You will experience future dilution as a result of future equity

offerings.

We may in the future offer additional shares of our Common Stock or

other securities convertible into or exchangeable for our Common

Stock. Although no assurances can be given that we will consummate

a financing, in the event we do, or in the event we sell shares of

Common Stock or other securities convertible into shares of our

Common Stock in the future, additional and substantial dilution

will occur. In addition, current investors or investors purchasing

shares or other securities in the future could have rights superior

to investors in this offering. Subsequent offerings at a lower

price (a “down round”) or securities convertible into

or exchangeable for our Common Stock at a lower price (including

the securities held by Acacia) could result in additional

dilution.

We may be unable to protect our proprietary technology or keep up

with that of our competitors.

Our

success depends to a significant degree upon the protection of our

software and other proprietary intellectual property rights. We may

be unable to deter misappropriation of our proprietary information,

detect unauthorized use, or take appropriate steps to enforce our

intellectual property rights. In addition, our competitors may now

have or may in the future develop technologies that are as good as

or better than our technology without violating our proprietary

rights. Our failure to protect our software and other proprietary

intellectual property rights or to utilize technologies that are as

good as our competitors’ could put us at a disadvantage to

our competitors.

We may not be able to obtain trademark protection for our marks,

which could impede our efforts to build brand

identity.

We have

filed a trademark application with the Patent and Trademark Office

seeking registration of the trademark, BITZUMI and EBIT NEWS. There

can be no assurance that our application will be successful or that

we will be able to secure significant protection for our trademark

in the United States or elsewhere as we expand internationally. Our

competitors or others could adopt product or service marks similar

to our mark, or try to prevent us from using our mark, thereby

impeding our ability to build brand identity and possibly leading

to customer confusion. Any claim by another party against us or

customer confusion related to our trademark, or our failure to

obtain trademark registration, could harm our

business.

We may be accused of infringing intellectual property rights of

third parties.

Other

parties may claim that we infringe their intellectual property

rights. In the future we may be subject to legal claims of alleged

infringement of the intellectual property rights of third parties.

The ready availability of damages, royalties, and the potential for

injunctive relief has increased the defense litigation costs of

patent infringement claims, especially those asserted by third

parties whose sole or primary business is to assert such claims.

Such claims, even if not meritorious, may result in significant

expenditure of financial and managerial resources, and the payment

of damages or settlement amounts. Additionally, we may become

subject to injunctions prohibiting us from using software or

business processes we currently use or may need to use in the

future, or requiring us to obtain licenses from third parties when

such licenses may not be available on financially feasible terms or

terms acceptable to us or at all. In addition, we may not be able

to obtain on favorable terms, or at all, licenses or other rights

with respect to intellectual property we do not own.

Implications of being an “emerging growth

company”

As an issuer with less than $1 billion in total annual gross

revenues during our last fiscal year, we will qualify as an

“emerging growth company” under the Jumpstart Our

Business Startups Act of 2012 (the “JOBS Act”) if and

when we become a public company. An emerging growth company may

take advantage of certain reduced reporting requirements and is

relieved of certain other significant requirements that are

otherwise generally applicable to public companies. In particular,

as an emerging growth company we:

|

●

|

Would not be required to obtain an auditor attestation on our

internal controls over financial reporting pursuant to the

Sarbanes-Oxley Act of 2002;

|

|

●

|

Would not be required to provide a detailed narrative disclosure

discussing our compensation principles, objectives and elements and

analyzing how those elements fit with our principles and objectives

(commonly referred to as “compensation discussion and

analysis”);

|

|

●

|

Would not be required to obtain a non-binding advisory vote from

our stockholders on executive compensation or golden parachute

arrangements (commonly referred to as the “say-on-pay,”

“say-on-frequency” and

“say-on-golden-parachute” votes);

|

|

●

|

Would be exempt from certain executive compensation disclosure

provisions requiring a pay-for-performance graph and CEO pay ratio

disclosure;

|

|

●

|

May present only two years of audited financial statements and only

two years of related Management’s Discussion and Analysis of

Financial Condition and Results of Operations; and

|

|

●

|

Would be eligible to claim longer phase-in periods for the adoption

of new or revised financial accounting standards.

|

We

intend to take advantage of all of these reduced reporting

requirements and exemptions, including the longer phase-in periods

for the adoption of new or revised financial accounting standards

under §107 of the JOBS Act. Our election to use the phase-in

periods may make it difficult to compare our financial statements

to those of non-emerging growth companies and other emerging growth

companies that have opted out of the phase-in periods under

§107 of the JOBS Act.

Under

the JOBS Act, we may take advantage of the above-described reduced

reporting requirements and exemptions for up to five years after

our initial sale of common equity pursuant to a registration

statement declared effective under the Securities Act of 1933, as

amended (“Securities Act”), or such earlier time that

we no longer meet the definition of an emerging growth company.

Note that this offering, while a public offering, is not a sale of

common equity pursuant to a registration statement, since the

offering is conducted pursuant to an exemption from the

registration requirements. In this regard, the JOBS Act provides

that we would cease to be an “emerging growth company”

if we have more than $1 billion in annual revenues, have more than

$700 million in market value of our Common Stock held by

non-affiliates, or issue more than $1 billion in principal amount

of non-convertible debt over a three-year period.

Risk Factors Related to Cryptocurrency Networks and

Cryptocurrency

The value of cryptocurrency and fluctuations in the price of

cryptocurrency could materially and adversely affect the business

and investment in the company.

Several

factors may affect the value of cryptocurrency, including, but not

limited to:

●

Total

cryptocurrency in existence;

●

Global

cryptocurrency demand, which is influenced by the growth of retail

merchants’ and commercial businesses’ acceptance of

cryptocurrency as payment for goods and services, the security of

online cryptocurrency exchanges and digital wallets that hold

cryptocurrency, the perception that the use and holding of

cryptocurrency is safe and secure, the lack of regulatory

restrictions on their use and the reputation of cryptocurrency for

illicit use;

●

Global

cryptocurrency supply, which is influenced by similar factors as

global cryptocurrency demand, in addition to fiat currency needs by

miners (for example, to invest in equipment or pay electricity

bills) and taxpayers who may liquidate cryptocurrency holdings

around tax deadlines to meet tax obligations;

●

Investors’

expectations with respect to the rate of inflation or deflation of

fiat currencies or cryptocurrency;

●

Interest

rates;

●

Currency exchange

rates, including the rates at which cryptocurrency may be exchanged

for fiat currencies;

●

Fiat currency

withdrawal and deposit policies of cryptocurrency exchanges and

liquidity of such cryptocurrency exchanges;

●

Interruptions in

service from or failures of major cryptocurrency

exchanges;

●

Cyber theft of

cryptocurrency from online cryptocurrency wallet providers, or news

of such theft from such providers, or from individuals’

cryptocurrency wallets;

●

Investment and

trading activities of large investors, including private and

registered funds, that may directly or indirectly invest in

cryptocurrency;

●

Monetary policies

of governments, trade restrictions, currency devaluations and

revaluations;

●

Regulatory

measures, if any, that restrict the use of cryptocurrency as a form

of payment or the purchase of cryptocurrency on the cryptocurrency

market;

●

The availability

and popularity of businesses that provide cryptocurrency

related services;

●

The maintenance and

development of the opensource software protocol of certain

cryptocurrency networks;

●

Increased

competition from other forms of cryptocurrency or payments

services;

●

Global or regional

political, economic, or financial events and

situations;

●

Expectations among

cryptocurrency economy participants that the value of

cryptocurrency will soon change; and

●

Fees associated

with processing a cryptocurrency transaction.

The loss or destruction of a private key required to access

cryptocurrency may be irreversible. Our loss of access to our

private keys or our experience of a data loss relating to the

cryptocurrency we hold could adversely affect an investment in our

company.

Cryptocurrency

is controllable only by the possessor of both the unique public key

and private key relating to the local or online digital wallet in

which the cryptocurrency is held. We are required by the operation

of cryptocurrency networks to publish the public key relating to a

digital wallet in use by us when the cryptocurrency network first

verifies a spending transaction from that digital wallet, and

disseminates such information into the cryptocurrency network. We

safeguard and keep private the private keys relating to our

cryptocurrency by utilizing AlphaPoint, an offsite third-party

storage facility; to the extent a private key is lost, destroyed or

otherwise compromised and no backup of the private key is

accessible, we will be unable to access the cryptocurrency held by

the private key and the private key will not be capable of being

restored by the cryptocurrency network. Any loss of private keys

relating to digital wallets used to store our cryptocurrency could

adversely affect an investment in us.

We depend on third parties to provide execution of our trading

platform, Internet, telecommunication and fiber optic network

connectivity to the customers in our data centers, and any delays

or disruptions in service could adversely affect an investment in

us.

We rely

on third-party service providers. In particular, we will depend on

third parties to provide real time quotation and trading execution

with our trading platform, Internet, telecommunication, and fiber

optic network connectivity to our servers in our data center, and

we have no control over the reliability of the services provided by

these suppliers. We may in the future experience difficulties due

to service failures unrelated to our systems and services. Any

Internet, telecommunication, or fiber optic network failures may

result in significant loss of connectivity of our wallets to the

cryptocurrency exchanges, which could consequently impair our

ability to facilitate cryptocurrency transactions, which could

adversely impact an investment in us.

Power outages, limited availability of electrical resources, and

increased energy costs could adversely affect our

business.

Our

operations are subject to electrical power outages, regional

competition for available power, and increased energy costs. Any of

these could result in loss of connectivity to our wallets,

increased costs of operation, and/or damage to our servers and

electrical equipment, which could consequently impair our ability

to facilitate cryptocurrency transactions, which could adversely

impact an investment in us.

The further development and acceptance of cryptocurrency networks,

which represents a new and rapidly changing industry, are subject

to a variety of factors that are difficult to evaluate. The slowing

or stopping of the development or acceptance of digital currency

systems may adversely affect our business.

Digital

currencies may be used, among other things, to buy and sell goods

and services are a new and rapidly evolving industry. The growth of

the digital currency industry in general, and in particular the

Bitcoin industry, Ethereum industry, and Litecoin industry, are

subject to a high degree of uncertainty. The factors affecting the

further development of the digital currencies industry, as well as

the Bitcoin, Ethereum and Litecoin industries,

include:

●

Continued worldwide

growth in the adoption and use of Bitcoins, Ethereum, and

Litecoins, and other cryptocurrency;

●

Government and

quasi-government regulation of Bitcoin, Ethereum, and Litecoin, and

other cryptocurrency and their use, or restrictions on or

regulation of access to and operation of cryptocurrency networks

and system;

●

The maintenance and

development of the open-source software protocol of various

cryptocurrency networks;

●

The availability

and popularity of other forms or methods of buying and selling

goods and services, including new means of using fiat currencies;

and

●

General economic

conditions and the regulatory environment relating to digital

currencies.

A

decline in the popularity or acceptance of the Bitcoin Network,

Ethereum Network, or Litecoin Network could adversely affect an

investment in us.

Currently, there is relatively small use of cryptocurrency in the

retail and commercial marketplace in comparison to relatively large

use by speculators, thus contributing to price volatility that

could adversely affect an investment in us.

As

relatively new products and technologies, cryptocurrency has only

recently become widely accepted as a means of payment for goods and

services by many major retail and commercial outlets, and use of

cryptocurrency by consumers to pay such retail and commercial

outlets remains limited. Conversely, a significant portion of

cryptocurrency demand is generated by speculators and investors

seeking to profit from the short- or long-term holding of

cryptocurrency. A lack of expansion by cryptocurrency into retail

and commercial markets, or a contraction of such use, may result in

increased volatility or a reduction in the price of

cryptocurrencies, either of which could adversely impact an

investment in us.

The acceptance of Bitcoin Network, Ethereum Network, or Litecoin

Network software patches or upgrades by a significant, but not

overwhelming, percentage of the users and miners in the respective

networks could result in a “fork” in the Blockchain,

resulting in the operation of two separate networks until such time

as the forked Blockchains are merged. The temporary or permanent

existence of forked Blockchains could adversely impact an

investment in us.

Bitcoin, Ethereum, and Litecoin are open source projects and,

although there is an influential group of leaders in the

cryptocurrency community, there is no official developer or group

of developers that formally controls the Bitcoin, Ethereum, or

Litecoin Networks. Any individual can download the particular

cryptocurrency network software and make any desired modifications,

which are proposed to users and miners on the respective network

through software downloads and upgrades. A substantial majority of

miners and the particular cryptocurrency users must consent to

those software modifications by downloading the altered software or

upgrade that implements the changes; otherwise, the changes do not

become a part of the cryptocurrency network. Generally, changes to

various cryptocurrency networks have been accepted by the vast

majority of users and miners, ensuring that the cryptocurrency

networks remain coherent economic systems; however, a developer or

group of developers could potentially propose a modification to a

cryptocurrency network that is not accepted by avast majority of

miners and users, but that is nonetheless accepted by a substantial

population of participants in the respective cryptocurrency

network. In such a case, and if the modification is material and/or

not backwards compatible with the prior version of the respective

cryptocurrency network software, a “fork” in the

Blockchain could develop and two separate networks of the same

cryptocurrency could result, one running the pre-modification

software program and the other running the modified version (e.g.,

a second Bitcoin Network). Such a fork in the Blockchain typically

would be addressed by community-led efforts to merge the forked

Blockchains, and several prior forks have been so merged without

any material impact on the price of Bitcoin, although there can be

no assurance that this will always be the case upon a fork. This

kind of split in a Bitcoin, Ethereum, or Litecoin Network could

materially and adversely impact an investment in us and, in the

worst case scenario, harm the sustainability of the respective

network’s economy.

The open-source structure of cryptocurrency network protocol means

that the Core Developers and other contributors to the protocol are

generally not directly compensated for their contributions in

maintaining and developing the protocol. A failure to properly

monitor and upgrade the protocol could damage the cryptocurrency

network and an investment in us.

The

Bitcoin, Ethereum, and Litecoin Networks operate based on an

open-source protocol maintained by the Core Developers and other

contributors. The Core Developers are those developers employed by

MIT Media Lab’s Digital Currency Initiative who oversee the

Bitcoin Network. See “Crytpographic Security Used in the

Bitcoin Network—Modification to the Bitcoin Network.”

As these network protocols are not sold and the networks’ use

does not generate revenues for its development team, the Core

Developers and contributors are generally not compensated for

maintaining and updating the respective cryptocurrency network

protocol. To the extent that material issues arise with the

Bitcoin, Ethereum, or Litecoin Network protocols, and the Core

Developers and open-source contributor community are unable to

address the issues adequately or in a timely manner, the respective

cryptocurrency network and an investment in us may be adversely

affected.

If the awards of cryptocurrency for solving blocks and transaction

fees for recording transactions are not sufficiently high to

incentivize miners, miners may respond in a way that reduces

confidence in the cryptocurrency networks, which could adversely

affect an investment in our company.

If the

award of new cryptocurrency for solving blocks declines and

transaction fees are not sufficiently high, miners may not have an

adequate incentive to continue mining and may cease their mining

operations. See “Overview of the Bitcoin Network

Operations--Bitcoin Mining and Creation of New Bitcoins.”

Miners ceasing operations would reduce the collective processing

power on the cryptocurrency networks, which would adversely affect

the confirmation process for transactions (i.e., temporarily

decreasing the speed at which blocks are added to the Blockchain

until the next scheduled adjustment in difficulty for block

solutions) and make the cryptocurrency networks more vulnerable to

a malicious actor or botnet obtaining control in excess of 50

percent of the processing power on the cryptocurrency networks. Any

reduction in confidence in the confirmation process or processing

power of cryptocurrency networks may adversely impact an investment

in us.

In

addition, to the extent to which the value of cryptocurrency mined

by a professionalized mining operation exceeds the allocable

capital and operating costs determines the profit margin of such

operation. A professionalized mining operation may be more likely

to sell a higher percentage of its newly mined cryptocurrency

rapidly if it is operating at a low profit margin—and it may

partially or completely cease operations if its profit margin is

negative. In a low profit margin environment, a higher percentage

of the new cryptocurrency mined each day will be sold into the

cryptocurrency exchange markets more rapidly, thereby reducing

cryptocurrency prices. Lower cryptocurrency prices will result in

further tightening of profit margins, particularly for

professionalized mining operations with higher costs and more

limited capital reserves, creating a network effect that may

further reduce the price of cryptocurrency until mining operations

with higher operating costs become unprofitable and remove mining

power from the cryptocurrency networks. The network effect of

reduced profit margins resulting in greater sales of newly mined

cryptocurrency could result in a reduction in the price of

cryptocurrency that could adversely impact an investment in our

company.

To the extent that any miners cease to record transactions in

solved blocks, transactions that do not include the payment of a

transaction fee will not be recorded on the Blockchain until a

block is solved by a miner who does not require the payment of

transaction fees. Any widespread delays in the recording of

transactions could result in a loss of confidence in the

cryptocurrency networks, which could adversely impact an investment

in us.

To the

extent that any miners cease to record transactions in solved

blocks, such transactions will not be recorded on the Blockchain.

Currently, there are no known incentives for miners to elect to

exclude the recording of transactions in solved blocks; however, to

the extent that any such incentives arise (e.g., a collective

movement among miners or one or more mining pools forcing

cryptocurrency users to pay transaction fees as a substitute for or

in addition to the award of new cryptocurrency upon the solving of

a block), actions of miners solving a significant number of blocks

could delay the recording and confirmation of transactions on the

Blockchain. Any systemic delays in the recording and confirmation

of transactions on the Blockchain could result in greater exposure

to double-spending transactions and a loss of confidence in

cryptocurrency networks, which could adversely impact an investment

in our company.

Intellectual property rights claims may adversely affect the

operation of cryptocurrency networks.

Third

parties may assert intellectual property claims relating to the

holding and transfer of digital currencies and their source code.

Regardless of the merit of any intellectual property or other legal

action, any threatened action that reduces confidence in

cryptocurrency networks’ long-term viability or the ability

of end-users to hold and transfer cryptocurrency may adversely

affect an investment in us. Additionally, a meritorious

intellectual property claim could prevent us and other end-users

from accessing cryptocurrency networks or holding or transferring

their cryptocurrency. As a result, an intellectual property claim

against us or other large cryptocurrency network participants could

adversely affect an investment in us.

The cryptocurrency exchanges on which cryptocurrency trade are

relatively new and, in most cases, largely unregulated and may

therefore be more exposed to fraud and failure than established,

regulated exchanges for other products. To the extent that the

cryptocurrency exchanges representing a substantial portion of the

volume in cryptocurrency trading are involved in fraud or

experience security failures or other operational issues, such

cryptocurrency exchanges’ failures may result in a reduction

in the price of cryptocurrency and can adversely affect an

investment in us.

The

cryptocurrency exchanges on which cryptocurrency trade are new and,

in most cases, largely unregulated. Furthermore, many

cryptocurrency exchanges do not provide the public with significant

information regarding their ownership structure, management teams,

corporate practices, or regulatory compliance. As a result, the

marketplace may lose confidence in, or may experience problems

relating to, cryptocurrency exchanges, including prominent

exchanges handling a significant portion of the volume of

cryptocurrency trading. These potential consequences of a

cryptocurrency exchange’s failure could reduce the demand and

use of cryptocurrency, reduce the value of cryptocurrency, and/or

adversely affect an investment in us.

Over

the past four years, many cryptocurrency exchanges have been closed

due to fraud, failure, or security breaches. In many of these

instances, the customers of such cryptocurrency exchanges were not

compensated or made whole for the partial or complete losses of

their account balances in such cryptocurrency exchanges. While

smaller cryptocurrency exchanges are less likely to have the

infrastructure and capitalization that make larger cryptocurrency

exchanges more stable, larger cryptocurrency exchanges are more

likely to be appealing targets for hackers and

“malware” (i.e., software used or programmed by

attackers to disrupt computer operation, gather sensitive

information, or gain access to private computer

systems).

A lack of stability in the cryptocurrency exchange market and the

closure or temporary shutdown of cryptocurrency exchanges due to

fraud, business failure, hackers or malware, or government-mandated

regulation may reduce confidence in cryptocurrency networks and

result in greater volatility in cryptocurrency value. These

potential consequences of a cryptocurrency exchange’s failure

could reflect poorly on us even if we are not involved in that

failure, and adversely affect an investment in our

company.

Our ability to adopt technology in response to changing security

needs or trends poses a challenge to the safekeeping of our

cryptocurrency.

The history of the cryptocurrency exchange markets has shown that

cryptocurrency exchanges and large holders of cryptocurrency must

adapt to technological change in order to secure and safeguard

their cryptocurrency. We rely on AlphaPoint, a third-party off site

storage provider, to safeguard our cryptocurrency holdings from

theft, loss, destruction or other issues relating to hackers and

technological attack. We believe that it may become a more

appealing target of security threats as the size of our

cryptocurrency holdings grow. To the extent that either our

third-party storage sites or we are unable to identify and mitigate

or stop new security threats, our cryptocurrency holdings may be

subject to theft, loss, destruction or other attack, which could

adversely affect an investment in us.

Security threats to us could result in a loss of company’s

cryptocurrency, or damage to our reputation and our brand, each of

which could adversely affect an investment in us.

Security

breaches, computer malware, and computer hacking attacks have been

a prevalent concern in cryptocurrency exchange markets since the

launch of cryptocurrency networks. Any security breach caused by

hacking, which involves efforts to gain unauthorized access to

information or systems, or to cause intentional malfunctions or

loss or corruption of data, software, hardware or other computer

equipment, and the inadvertent transmission of computer viruses,

could harm our business operations or result in loss of our

cryptocurrency. Any breach of our infrastructure could result in

damage to our reputation which could adversely affect an investment

in us. Furthermore, we believe that, as our assets grow, we may

become a more appealing target for security threats such as hackers

and malware.

We

rely

solely on AlphaPoint to safeguard our cryptocurrency holdings from

theft, loss, destruction or other issues relating to hackers and

technological attack. Nevertheless, our third-party storage

provider security system may not be impenetrable and may not be

free from defect or immune to acts of God, and any loss due to a

security breach, software defect or act of God will be borne by