Table of Contents

PRELIMINARY OFFERING CIRCULAR, DATED FEBRUARY 8, 2018

INSTITUTE FOR WEALTH HOLDINGS, INC.

Maximum offering of $20,000,000

Up to 2,000,000 shares of Series D Convertible Preferred Stock

And up to 2,000,000 shares of Common Stock into which the Series D Convertible Preferred Stock May Convert

Offering Circular Date February 8, 2018

Two Galleria Tower

13455 Noel Road, Suite 100

Dallas, Texas 75240

(972) 450-6000

www.iwhinc.com

The Institute for Wealth Holdings, Inc., a Delaware corporation, (the “Company,” “we” or “our”) is offering a maximum of 2,000,000 shares of Series D Convertible Preferred Stock, par value $0.001. The Series D Convertible Preferred Stock may be converted into shares of Common Stock of the Company at the discretion of the investor. As a result, the Company is qualifying up to 2,000,000 shares of Series D Convertible Preferred Stock and up to 2,000,000 shares of Common Stock under this offering statement, of which this offering circular is a part. See “Description of Capital - Offered Securities” on Page 56 for additional information.

This best efforts offering does not have a minimum number of securities which must be sold. Since there is no minimum amount of securities that must be purchased in this offering, all accepted and approved subscription proceeds will be available to us after release from escrow and no investor funds will be reimbursed if the proceeds of this offering are insufficient to cover the costs of the offering. The offering will continue until the earlier of twelve (12) months from the date of this offering is qualified for sale or the date when all offered securities have been sold.

| Price to Public | Discounts or Commissions |

Proceeds to Issuer per share* |

Proceeds to other persons |

|||||||||||||

| Per Share |

$ | 10.00 | 7% or $0.70 | ^ | $ | 9.30 | $ | 0 | ||||||||

| Maximum offering amount |

$ | 20,000,000 | $ | 1,400,000 | $ | 18,600,000 | $ | 0 | ||||||||

| * | For anticipated expenses, See “Use of Proceeds.” This does not include legal or accounting expenses. |

| ^ | This is a 7% commission to our placement agent, Lanier Securities, LLC. Please refer to “Plan of Distribution” on Page 18 for a description of the compensation arrangements with Lanier Securities, LLC in connection with this offering. |

Prior to this offering, there has been no trading market for our shares.

These are speculative securities. Investing in our shares involves significant risks. You should purchase these securities only if you can afford a complete loss of your investment. See “Risk Factors” beginning on Page 9.

Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

Table of Contents

THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OF OR GIVE ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SOLICITATION MATERIALS. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION.

AN OFFERING STATEMENT PURSUANT TO REGULATION A RELATING TO THESE SECURITIES HAS BEEN FILED WITH THE SECURITIES AND EXCHANGE COMMISSION. INFORMATION CONTAINED IN THIS PRELIMINARY OFFERING CIRCULAR IS SUBJECT TO COMPLETION OR AMENDMENT. THESE SECURITIES MAY NOT BE SOLD NOR MAY OFFERS TO BUY BE ACCEPTED BEFORE THE OFFERING STATEMENT FILED WITH THE COMMISSION IS QUALIFIED. THIS PRELIMINARY OFFERING CIRCULAR SHALL NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY NOR MAY THERE BE ANY SALES OF THESE SECURITIES IN ANY STATE IN WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE UNLAWFUL BEFORE REGISTRATION OR QUALIFICATION UNDER THE LAWS OF SUCH STATE. WE MAY ELECT TO SATISFY OUR OBLIGATION TO DELIVER A FINAL OFFERING CIRCULAR BY SENDING YOU A NOTICE WITHIN TWO BUSINESS DAYS AFTER THE COMPLETION OF OUR SALE TO YOU THAT CONTAINS THE URL WHERE THE FINAL OFFERING CIRCULAR OR THE OFFERING STATEMENT IN WHICH SUCH FINAL OFFERING CIRCULAR WAS FILED MAY BE OBTAINED.

This offering circular is following the offering circular format described in Part II (a)(1)(ii) of Form 1-A.

2

Table of Contents

| 4 | ||||

| 9 | ||||

| 17 | ||||

| 18 | ||||

| 19 | ||||

| 21 | ||||

| 39 | ||||

| MANAGEMENT AND FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

40 | |||

| 47 | ||||

| 52 | ||||

| SECURITY OWNERSHIP OF MANAGEMENT AND CERTAIN SECURITYHOLDERS |

54 | |||

| 55 | ||||

| 56 | ||||

| 59 | ||||

No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this offering circular. You must not rely on any unauthorized information or representations. This offering circular is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this offering circular is current only as of its date.

3

Table of Contents

The following summary highlights selected information contained in this offering circular. This summary does not contain all the information that may be important to your investment in the offered securities. You should read this entire offering circular carefully, including the “Risk Factors” section, our audited, consolidated financial statements and the related notes included elsewhere in this offering circular, before making an investment decision. Unless the context otherwise requires, the terms “Institute for Wealth,” “IWH,” “the Company,” “we,” “us” and “our” in this offering circular refers to Institute for Wealth Holdings, Inc., a Delaware corporation.

Our Company

Background

Our company is the result of a successful business combination in 2016 of two companies, the Institute for Wealth Management, LLC, a Delaware limited liability company (“IWM”), which was founded by Matthew D. Medeiros in 2003, and Institute for Wealth Holdings, Inc., formerly Cherry, Inc., which was founded in 2008 by Dewey M. “Rusty” Moore, Jr. Both of our founders are experienced investment professionals who have demonstrated proven leadership skills and excellence in the development of innovative products and services, and superior team building capabilities in launching successful companies.

All of our operations are conducted by our four subsidiaries, IWM, Institute for Wealth Advisors, Inc., a Delaware corporation (“IWA”), Institute for Wealth Consultants, Inc., a Delaware corporation (“IWC”), and Institute for Wealth Partners, Inc., a Delaware corporation (“IWP”). IWM, IWA and IWC operate a dual investment advisory and investment management platform for our investment advisory representatives (“IARs”) and clients through our various subsidiaries. We provide high quality investment management and advice to clients by enrolling, supporting and supervising qualified investment advisors. Our mission statement clearly articulates our business model: Empowering Trusted Advisors to succeed financially by providing quality and value in wealth management, financial planning, financial tools and investment advisory services based on proven principles and the highest standards of trust. We operate under this combined platform by utilizing our proven management team to recruit and train associate investment advisers and IARs to gather AUM under a successful, client-centric national brand. We provide, through multiple custodians, a single client interface for the administration, execution and reporting for client accounts, and offer advisers online access to fee tracking and payments. This approach allows for higher productivity by granting our advisors and IARs time to focus on existing clients and prospective new clients.

We believe ours is the “Ideal Business Model,” one that derives recurring income from an asset-based revenue model. We function much like a bank, in that client assets are deposited at one or more of our custodians through which we provide our client services for a fee. Our subsidiaries operate investment management, wealth management and investment advisory platforms, which derive fee based compensation based on the amount of assets under management (“AUM”). This is the fiduciary, or investment advisor, model where an increase in total assets is in the client’s and advisor’s best interests, a “win-win” relationship. Our company enjoys an excellent business reputation. Since their inception, neither IWM, IWA nor their affiliates have had an unresolved customer complaint.

Our subsidiaries provide our investment advisory, wealth management and portfolio managements services, client services and multiple custodial relationships through our subsidiary, IWM founded in 2003, which is headquartered in Denver, Colorado. (See “Description of Business” on Page 21). In addition, we provide investment advisory support services to our IARs through another subsidiary, IWA,

4

Table of Contents

headquartered in Dallas, Texas. The Institute for Life & Annuity, Inc., a Texas corporation (“ILA”), our affiliated corporate life insurance agency, complements our IARs’ risk management services to clients. We also have recently added IWC, which provides IAR support services, and access to life insurance and annuity products and comprehensive fee-based financial planning at ILA. (See “Structure of Institute of Wealth Holdings” on Page 25).

The combined Institute for Wealth family of companies offers a robust platform to support our IARs and capture client AUM. We are growing rapidly, with over $819.4 million AUM through approximately forty IARs. Since December 31, 2015, on a pro forma basis, our total revenue has grown at a compound annual growth rate (“CAGR”) of 113% and AUM has grown at a CAGR of 82%. We expect to grow the number of IARs to over 100 and for AUM to grow to over $5 billion in the next 3 to 5 years if we successfully implement our growth strategy. The capital raised in this offering is expected to facilitate and enhance our growth strategy.

Executive Committee

The Company is led by a veteran leadership team with extensive business and investment management experience. D. M. “Rusty” Moore and Matthew D. Medeiros are our principal executives. Mr. Moore has worked as an executive in the financial management sector since the early 1990s and led Rushmore Financial Group, Inc., through its initial public offering in 1998, and over the following fifteen years as CEO he led his company through a number of public and private offerings, merger and acquisition transactions. Mr. Medeiros has significant investment management experience in the United States and abroad, and has been frequently cited and interviewed by media outlets, universities and professional organizations with respect to this experience. For more information about Mr. Moore, Mr. Medeiros and other vital members of our management team. (See “Directors, Officers and Significant Employees” on Page 47).

The Offering

Overview

We are offering 2,000,000 shares of Series D Convertible Preferred Stock, par value of $0.001 for $10.00 a share. The Series D Convertible Preferred Stock may be converted into shares of our Common Stock at the discretion of each investor. As such, we are qualifying up to 2,000,000 shares of Series D Convertible Preferred Stock and up to 2,000,000 shares of Common Stock under this offering statement, of which this offering circular is a part.

The Series D Convertible Preferred Stock: (i) is entitled to 7% annual dividends, payable quarterly in cash as declared by the Board of Directors; (ii) is convertible into shares of our common stock at the option of the stockholder for $10.00 per share; (iii) ranks pari-pasu with other preferred stock with respect to liquidation, but maintains a liquidation preference equal to 1.65 times the price of the offered securities; and (iv) is entitled to vote on an as-converted basis with common stock on any matter presented to the stockholders and separately as a class for matters relating to the offered securities. (See “Description of Capital – Offered Securities” for a description of the Series D Convertible Preferred Stock and the Common Stock on Page 56) .

There can be no assurance that all or any of the offered securities will be sold. To facilitate the offering, we have engaged Lanier Securities, LLC (“Lanier”) to act as our placement agent for the sale of the offered securities.

5

Table of Contents

Opportunities

IWH’s current business structure was created in September 2016 when we, as Cherry, Inc., merged with IWM’s parent company. As a result of this merger, we now appeal to a broader base of successful “break-away” brokers and independent investment advisors and provide expansive investment management and financial planning strategies nationwide. We anticipate that due to market conditions and recent consolidation trends there are significant opportunities to acquire smaller registered investment advisers (“RIAs”) and independent IARs who cannot afford the increased complexity and compliance costs associated with the investment management industry. We are now seeking approximately $20,000,000 to facilitate growth through the acquisition of additional IARs and RIAs, improve our technological infrastructure, reduce our outstanding debt, simplify our capital structure through the redemption or exchange of shares of our outstanding Series B Convertible Preferred stock, and to reserve a portion of the proceeds for the payment of quarterly dividends on the Series D Convertible Preferred Stock and accumulated but unpaid dividends on our Series B Convertible Preferred Stock.

We operate an investment management and investment advisory platform, which receives fee based compensation for our portfolio management services based on the total AUM at IWM, IAR support services at IWA and IWC, and life insurance and annuity overrides from ILA. This is the fiduciary, or investment advisor, model where an increase in total assets is in the client’s and advisor’s best interest. We believe that by increasing the number of IARs and RIAs we work with, we can significantly increase our AUM and profitability.

Current Stock

Our authorized capital stock consists of 50,000,000 shares of Common Stock, par value $0.001 and 10,000,000 shares of Preferred Stock, par value of $0.001 (“Preferred Stock”). The Preferred Stock currently consists of 70,000 authorized shares of Series B Convertible Preferred Stock, 1,925,000 authorized shares of Series C Convertible Preferred Stock and 2,500,000 authorized shares of Series D Convertible Preferred Stock. We previously issued a class of Series A preferred stock, which has been redeemed and may not be reissued. As a result, 5,500,000 shares of Preferred Stock remain undesignated.

These undesignated shares of Preferred Stock may be issued from time to time in one or more series pursuant to a resolution or resolutions providing for such issue duly adopted by the Board of Directors. The Board is further authorized, subject to limitations prescribed by law, to fix by resolution or resolutions the designations, powers, preferences and rights, and the qualifications, limitations or restrictions thereof, of any wholly unissued series of Preferred Stock, including without limitation authority to fix by resolution or resolutions the dividend rights, dividend rate, conversion rights, voting rights, rights and terms of redemption (including sinking fund provisions), redemption price or prices, and liquidation preferences of any such series, and the number of shares constituting any such series and the designation thereof, or any of the foregoing.

6

Table of Contents

Prior to this offering, our current capitalization consists of the following classes of securities:

| Class of Stock |

Authorized Shares | Outstanding | ||||||

| Common Stock |

50,000,000 | 2,700,710 | ||||||

| Preferred Stock |

10,000,000 | 1,963,584 | ||||||

| 1. Series B Convertible Preferred Stock |

70,000 | 42,750 | ||||||

| 2. Series C Convertible Preferred Stock |

1,925,000 | 1,904,404 | ||||||

| 3. Series D Convertible Preferred Stock |

2,500,000 | 267,300 | ||||||

7

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

We make forward-looking statements in this offering circular, including, without limitation, in the sections captioned “Summary,” “Risk Factors,” “Description of Business” and various other sections. In some cases, you can identify these statements by forward-looking words such as “may,” “might,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential” or “continue,” and the negative of these terms and other comparable terminology. These forward-looking statements, which are subject to known and unknown risks, uncertainties and assumptions about us, may include projections of our future financial performance based on our growth strategies and anticipated trends in our business. These statements are only predictions based on our current expectations and projections about future events. There are important factors that could cause our actual results, level of activity, performance or achievements to differ materially from the results, level of activity, performance or achievements expressed or implied by the forward-looking statements. In particular, you should consider the numerous risks and uncertainties described under “Risk Factors.”

While we believe we have identified material risks, these risks and uncertainties are not exhaustive. Other sections of this offering circular describe additional factors that could adversely impact our business and financial performance. Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time, and it is not possible to predict all risks and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

Although we believe the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, level of activity, performance or achievements. Moreover, neither we nor any other person assumes responsibility for the accuracy or completeness of any of these forward-looking statements. You should not rely upon forward-looking statements as predictions of future events. We are under no duty to update any of these forward-looking statements after the date of this offering circular to conform our prior statements to actual results or revised expectations, and we do not intend to do so.

Forward-looking statements include, but are not limited to, statements about:

| • | our business’ strategies and investment policies; |

| • | our business’ financing plans and the availability of capital; |

| • | our ability to attract and retain IARs and RIAs; |

| • | the risks associated with potential acquisitions we might make; |

| • | the recruitment and retention of our officers and independent contractors; |

| • | our expected levels of compensation; |

| • | the effects of competition on our business; and |

| • | the impact of future legislation and regulatory changes on our business. |

We caution you not to place undue reliance on the forward-looking statements, which speak only as of the date of this offering circular.

8

Table of Contents

Investing in the offered securities involves a high degree of risk. You should carefully consider each of the following risks, together with all other information set forth in this offering circular, including the consolidated financial statements and the related notes, before making a decision to buy the offered securities. The risks described below are not the only risks that we face, but the following is a description of what we consider the key challenges and material risks to our business and an investment in our securities. Our company is still subject to the same risks as all other operating companies in the economy.

Inadequacy of Funds

There is no assurance that the proceeds of this offering will capitalize and sustain the Company sufficiently to allow for working and expansion capital, debt repayment, growth acquisition capital, technology development and investment. If only a fraction of this offering is sold, we may have inadequate funds to fully develop our business and may need debt financing or other capital investment to fully implement our business plans.

Dependence On Management

The growth plan proposed by management will be significantly dependent on our management team. Our success will be particularly dependent on Dewey M. “Rusty” Moore, Jr. and Matthew D. Medeiros. The loss of either of these individuals could have a material adverse effect on the Company. We do not currently maintain a “key man” life insurance policy for either Mr. Moore or Mr. Medeiros. See “Directors, Officers and Significant Employees” section.

We have a limited operating history

Since the merger between the Company and the Institute for Wealth Management Holdings, Inc., we have had a limited operating history. There can be no assurance we will ever operate profitably. The likelihood of our success should be considered in the light of the problems, expenses, difficulties, complications and delays usually encountered by companies in their early stages of development. We may not successfully attain the objectives necessary to overcome these risks and uncertainties.

Placement Agent

We have retained Lanier Securities, LLC (“Lanier”), a broker-dealer registered with the Financial Industry Regulatory Authority (FINRA), as placement agent. A portion of the capital contributions from this offering will be paid to Lanier as commission for its services. Lanier has the ability to assemble selling groups to facilitate this offering. The objectives of Lanier and any selling group may differ from those of the Company, management team, shareholders and investors. As such, Lanier’s and the selling group’s participation in this offering may be influenced by their own interests in current or future fees and commissions that are not necessarily in the best interest of the Company or prospective investors.

9

Table of Contents

Preferred Stock has a liquidation preference over Common Stock

Our preferred stock may be converted into shares of common stock at the discretion of the shareholder. As a general matter, outstanding shares of our preferred stock carry a liquidation preference over shares of our common stock. If an investor chooses to convert its preferred stock into common stock, the holders of the remaining preferred stock would be entitled to a preference over the common stock upon any liquidation of the Company, including the payment of any accrued but unpaid dividends.

Lack of dividends for Common Stock

Our preferred stock may be converted into shares of common stock at the discretion of the shareholder. We do not anticipate paying any cash dividends on common stock in the foreseeable future and intend to retain profits, if any, to finance growth and expansion.

Reservation of proceeds to pay dividends

We currently anticipate reserving a portion of the proceeds of this offering for the payment of quarterly dividends starting the first full calendar quarter following the closing of this offering. The holders of Series B Convertible Preferred Stock are entitled to any accrued but unpaid dividends prior to any other dividend distributions. The reservation of proceeds for dividend distribution to holders of Series B Convertible Preferred Stock and Series D Convertible Preferred Stock will reduce the amount of capital used to finance growth and expansion.

No public trading market for the securities

There is no active trading market for the securities being offered and no market may develop in the foreseeable future for any such securities. If no subsequent market develops, investors may end up with an illiquid investment and not be able to sell or otherwise monetize its stock.

Anti-Takeover Provisions

Our Certificate of Incorporation and Bylaws may make it difficult to effect a change of control and replace incumbent management. Our directors are elected for three-year terms. Advance notice of stockholder nominations for the election of directors must be at least ninety (90) days in advance of the date in which the next annual meeting of stockholders is held. In addition, directors may be removed only for “cause” as defined in the our Certificate of Incorporation, and then only through an action approved by at least two-thirds of the voting power of all of the shares of the Company entitled to vote generally in the election of directors, voting together as a single class. A similar vote is required for stockholders to call a special meeting or to amend the Certificate of Incorporation to amend or repeal any provision related to the Board of Directors. Our Certificate of Incorporation authorizes the Board of Directors to issue preferred stock in classes or series, and to determine voting, redemption and conversion rights and other rights related to such class or series of preferred stock that, in some circumstances, could have the effect of preventing a merger, tender offer or other takeover attempt which the Company’s Board of Directors opposes. Such provisions could also exert a negative influence on the value of our common stock and of a stockholder’s ability to receive the highest value for the common stock in a transaction that may be hindered by the operation of these provisions.

Risks associated with expansion

We plan on expanding our core business through the deployment of capital invested in this offering. Any expansion of operations we undertake will entail risks, and during our expansion we may have inadequate

10

Table of Contents

capital to operate our established business operations. Consequently, investors should assume that (i) such expansion may ultimately involve expenditures of funds beyond the resources available to us at that time, and (ii) management of such expanded operations may divert management’s attention and resources away from our existing operations. These factors may have a material adverse effect on our present and prospective business activities. There can be no assurances our current management team will have the ability to effectively manage our expanded operations, and we may need additional operating capital to hire managers, compliance officers and other administrative persons to manage any expanded operations.

We may need additional capital, which may not be available

We may require funds in excess of our existing cash resources to fund operating deficits, develop new products or services, establish and expand our marketing capabilities, and finance general and administrative activities. Due to market conditions at the time we may need additional funding, or due to our financial conditions at that time, it is possible we will be unable to obtain additional funding as and when we need it. If we are unable to obtain additional funding, we may not be able to repay debts when they are due and payable. If we are able to obtain capital, it may be on unfavorable terms or terms which excessively dilute then-existing equity holders. If we are unable to obtain additional funding as and when needed, we could be forced to delay our development, marketing and expansion efforts and, if we continue to experience losses, potentially cease operations.

Put Agreement for Previously Issued Stock

In connection with a previous private offering of Series D Convertible Preferred Stock, certain investors, that hold 76,637 shares, entered into put option agreements which afford the investors the opportunity, from January 1, 2021 through January 10, 2021 (“Put Exercise Period”), to cause the Company to purchase all or a portion of the applicable Series D Convertible Preferred Stock at approximately $600,000, plus any accrued but unpaid dividends. If, prior to the Put Exercise Period, we are unable to generate sufficient revenue and multiple shareholders exercise their put options, we could face significant financial hardship and may need to incur debt financing, on potentially unfavorable terms, to meet our obligations under these agreements.

In addition, the Company had previously entered into a Put Call Agreement with a holder of 343,136 shares of Series C Convertible Preferred Stock. This Put Call Agreement gave the shareholder the option to require the Company to purchase all, but not less than all, of such Series C Convertible Preferred Stock for $350,000 if the shareholder provided notice of exercise prior to January 11, 2018. On December 18, 2017, the Company received a notice of exercise from the shareholder under the Put Call Agreement which would require the Company to purchase the shares of Series C Convertible Preferred Stock. The Company and the shareholder subsequently entered into an amendment to this Put Call Agreement which extended the deadline for the Company to purchase all of such shares of Series C Convertible Preferred Stock to April 18, 2018. The Company expects to explore potential alternatives to purchasing such shares with the shareholder. If the Company is unable to purchase such shares or secure a negotiated alternative to purchasing the shares, it could adversely affect the Company’s financial results and divert resources from operations.

Reliance on Assets Under Management to Produce Revenue

Our subsidiaries operate investment management, wealth management and investment advisory platforms, which derive fee based compensation based on the amount of assets under management (“AUM”). As a result, we derive a substantial portion of our revenue from fees collected based on the amount of AUM. As a general proposition, if the amount of AUM increases, our revenue increases and vice versa.

AUM is typically a product of the number of investment advisors and managers our subsidiaries are able to recruit and retain and the skill and success of those groups. While we have limited AUM turnover, the concentration of the source of our revenue could disproportionately expose us if our subsidiaries are unable to recruit and retain investment advisors and managers and thus AUM. Market conditions, regulatory exposure and the loss of advisors could cause a reduction in AUM. Although we do not believe we are substantially dependent on any particular advisor, the departure of an advisor responsible for a significant amount of AUM could have detrimental effects on our revenue and the value of an investor’s stock. We believe our compensation system, regulatory expertise, back office support, established succession plan and portfolio management products significantly reduce the risk of losing advisors. However, any loss of AUM would reduce our revenue and potentially inhibit our ability to adequately implement our business growth plans if the loss or losses were significant.

11

Table of Contents

Customer Base and Market Acceptance

While we believe we can develop a customer base through the marketing and promotion of our products and services, our inability to further develop such a customer base could have a material adverse effect on our operations. Although we believe our product and services offer advantages over competitive companies, no assurance can be given that our products and services will attain a degree of market acceptance on a sustained basis or that it will generate revenues sufficient for sustained profitable operations.

Competition

The securities and financial services industries are highly competitive, with many large, diversified, well-capitalized brokerage firms, financial institutions, and other organizations. Competition within the financial services industry is intense, with prospective clients solicited by established Wall Street brokerage and investment management firms offering similar services to prospective clients. Many of these competitors spend significant amounts on advertising to attract the investing public. Many Wall Street firms are better capitalized, have more established reputations, greater marketing experience and prowess, better relationships with investment product suppliers or have other competitive advantages. We expect our competitors to continue to improve the performance of their current products, reduce their prices and introduce new services and technologies that may offer greater performance and improved pricing, any of which could cause a decline in revenue or loss of market acceptance of our products. In addition, our competitors may develop enhancements to, or future generations of, competitive products that may render our services or technologies obsolete or uncompetitive. Competitive pressures may adversely affect us and our prospects.

Regulatory Risks

Our subsidiaries are subject to extensive regulation in the United States, primarily at the federal level, including regulation by the SEC under the Investment Advisers Act of 1940, as amended (the “Advisers Act”) and by the U.S. Department of Labor under the Employee Retirement Income Security Act of 1974 (“ERISA”). The Advisers Act imposes numerous obligations on our subsidiaries including advertising, recordkeeping and operating requirements, disclosure obligations and prohibitions on fraudulent activities.

Accordingly, we face the risk of significant intervention by regulatory authorities, including extended investigation and surveillance activity, adoption of costly or restrictive new regulations and judicial or administrative proceedings that may result in substantial penalties. Among other things, our subsidiaries could be fined or be prohibited from engaging in some of our business activities. The requirements imposed by regulators are generally designed to ensure the integrity of the financial markets and to protect clients and other third parties who deal with us, and are generally not designed to protect our stockholders. Consequently, these regulations often serve to limit our activities, including through net capital, customer protection and market conduct requirements. Moreover, volatility in the U.S. equities markets have led to heightened scrutiny of sophisticated trading technology and execution methods.

Our emphasis on growth coupled with the challenges of managing our business could result in increased exposure to regulatory violations. Although we have implemented, and continue to develop, various internal controls and procedures to prevent violation of applicable rules and regulations, there can be no assurance these controls will be sufficient.

12

Table of Contents

Changes in the Regulatory Environment

The legislative and regulatory environment in which our subsidiaries operate has undergone significant changes in the recent past, including additional filings with the SEC required for investment advisors, which have resulted in increased compliance costs. New laws or regulations, or changes in the enforcement of existing laws or regulations, applicable to us and our clients may adversely affect our business. Our ability to function in this environment will depend on our ability to monitor and promptly react to legislative and regulatory changes. There have been a number of highly publicized regulatory inquiries that have focused on the investment management industry. These inquiries already have resulted in increased scrutiny of the industry and new rules and regulations for investment advisers. This regulatory scrutiny may limit our ability to engage in certain activities that might be beneficial to our stockholders.

The SEC recently announced the formation of a Retail Strategy Task Force (the “Task Force”) to develop effective strategies to address harm to retail investors. The Task Force will work closely with the SEC’s examination staff, as well as the Office of Investor Education and Advocacy and use data analytics to identify areas of risk to retail investors. The Task Force will focus on vigorously pursuing cases against financial institutions and intermediaries. During fiscal year 2017, the SEC obtained orders and judgments totaling $3.7 billion in disgorgement and penalties, brought 754 enforcement actions and barred or suspended more than 625 individuals. The failure of our subsidiaries or their RIAs or IARs to comply with applicable laws or regulations could result in fines, suspensions of individual employees or other sanctions. Even if an investigation or proceeding did not result in a fine or sanction or the fine or sanction imposed against us or our employees by a regulator were small in monetary amount, the adverse publicity relating to an investigation, proceeding or imposition of these fines or sanctions could harm our reputation and cause our subsidiaries to lose existing clients existing accounts, or fail to attract new investors or accounts.

Changes in fiduciary definition

The Department of Labor expanded the “fiduciary” definition under the Employee Retirement Income Security Act of 1974 (“ERISA”) to include persons or entities who provide nondiscretionary investment advice to benefit plans and individual retirement accounts. Changes to ERISA’s fiduciary standards could increase compliance costs and potentially cause significant personal and corporate liability. The practical effects of this change are yet to be determined; however, it could have an impact on our daily operations.

General economic conditions effect on investable income

Our business activities and earnings will be affected by the behavior of individual investors within the United States. General business conditions in the United States, such as short-term and long-term interest rates, inflation, unemployment levels, monetary supply, fluctuations in both debt and equity capital markets, the strength of the United States economy and the local economy in which we operate, global financial market instability, and the risks of a recession and/or prolonged periods of stock market volatility, may reduce the amount of investable income of potential clients and may also influence investors’ behavior in ways we cannot predict, which may be particularly detrimental to our business model.

Possible fluctuations in operating results

Our operating results may fluctuate significantly from period to period as a result of a variety of factors, including investing patterns of customers, competitive pricing, debt service and principal reduction payments, and general economic conditions. Our operating cash flow may vary by quarter due to these fluctuations, which could restrict our ability to pay dividends to shareholders.

13

Table of Contents

Unanticipated obstacles to execution of the business plan

Our business plans may change significantly. Many of our potential business endeavors are capital intensive and may be subject to statutory or regulatory requirements. Management believes our chosen activities and strategies are achievable in light of current economic and legal conditions with the skills, background, and knowledge of our principals and advisors. Management reserves the right to make significant modifications to our stated strategies depending on future events. Investors will not have direct voting control regarding potential changes our business plan.

Management discretion as to use of proceeds

The net proceeds from this offering will be used for the purposes described in “Use of Proceeds.” We reserve the right, however, to use the funds obtained from this offering for other similar purposes not presently contemplated which we deem to be in the best interests of the Company and our shareholders in order to address changed circumstances or opportunities. As a result of the foregoing, our success will be substantially dependent upon the discretion and judgment of management with respect to application and allocation of the net proceeds of this offering. Investors in the offered securities will be entrusting their funds to our management, upon whose judgment and discretion the investors must depend.

Control by Management

As of the commencement of this offering, our executive officers and directors own more than 50% of the outstanding voting securities. Each share of the Series D Convertible Preferred Stock offered hereby will have one vote per share for all actions that require common stockholder approval and as such may have the ability to vote to remove any member of the Board of Directors. However, if only a portion of this offering is purchased, the executive officers and directors may maintain voting control of the Company. Accordingly, and because there is no cumulative voting for directors, our executive officers and directors may be in a position to control the election of the directors of the Company and to control our business and operations through their stock ownership, positions on the Board of Directors and management roles.

Dividend Policy

A holder of the Series D Convertible Preferred Stock offered hereby will be entitled to receive dividends only when, as, and if declared by the Board of Directors out of funds legally available. Our Board of Directors will determine the dividend policy based upon our results of operations, financial condition, capital requirements, and other circumstances. Additionally, prior to distributing dividends to holders of the offered securities, we must pay all accrued but unpaid dividends to holders of Series B Convertible Preferred Stock. As of December 31, 2017, the accumulated but unpaid dividends on the outstanding Series B Convertible Preferred Stock was $226,970. Although we anticipate a large amount of the Series B Convertible Preferred Stock will be exchanged for Series D Convertible Preferred Stock, there can be no assurances that such exchanges will occur and based on the financial position of the Company prior to this offering, without giving effect to any proceeds to be received from this offering, we may be undercapitalized and unable to pay dividends until our financial position is improved.

No assurances of protection for proprietary rights; Reliance on trade secrets

In certain cases, we may rely on trade secrets to protect proprietary technology and processes which we have developed or may develop in the future. There can be no assurances that secrecy obligations will be honored or that others will not independently develop similar or superior technology. The protection of proprietary technology through claims of trade secret status has been the subject of increasing claims and litigation by various companies both in order to protect proprietary rights as well as for competitive reasons

14

Table of Contents

even where proprietary claims are unsubstantiated. The prosecution of proprietary claims or the defense of such claims is costly and uncertain given the rapid development of the principles of law pertaining to this area. We may, like other firms, also be subject to claims by other parties with regard to the use of technology information and data which may be deemed proprietary to others.

Cybersecurity

We are, and our service providers are, susceptible to operational, information security and other cybersecurity risks, both directly and indirectly through their certain third parties. Similar types of cybersecurity risks are also present for issuers of securities in which our IARs invest, which could result in material adverse consequences for such issuers and may cause clients’ investment in such portfolio companies to lose value. These risks may not be covered by insurance. In general, cybersecurity incidents can result from deliberate attacks or unintentional events. Cyber-attacks include, but are not limited to, gaining unauthorized access to digital systems (e.g., through hacking or use of malicious software coding) for purposes of misappropriating assets or sensitive information, corrupting data, or causing operational disruption. Cyber-attacks may also be carried out without ever obtaining direct access to the targeted systems, such as through a denial-of-service attack which could result in the target’s network services becoming unavailable to its intended users. Cybersecurity failures by, or breaches of, the systems of the Company, IARs and other service providers (including, but not limited to, data providers, accountants, custodians, transfer agents and attorneys), market makers or the issuers of securities in which the IARs invest, could cause disruptions and impact business operations, potentially resulting in one or more of the following: material financial losses, unintended disclosure of confidential trading information, material impediments to trading, submission of erroneous trades or redemption orders, the inability of the Company or its service providers to transact business, violations of applicable privacy and other laws, regulatory fines, penalties, reputational damage, reimbursement or other compensation costs, or additional compliance costs. In addition, cyber-attacks may render inaccessible, inaccurate or incomplete any or all of the records of our assets, transactions, ownership of offered securities, and other data integral to our functioning. We may have to incur substantial costs in order to prevent or address cyber-incidents in the future. We have established a cybersecurity policy and business continuity procedures to address and mitigate these cybersecurity risks. Despite these efforts, certain risks may not yet have been identified and it is possible that prevention and remediation efforts will be inadequate or unsuccessful. Additionally, because techniques used to obtain unauthorized access or to sabotage systems change frequently and generally are not recognized until launched against a company, we may be unable to anticipate these techniques or to implement adequate preventive measures. Furthermore, we are unable to directly control the cybersecurity procedures and systems of any service providers, and the shareholders could be materially and adversely impacted as a result.

Litigation

There is no pending or threatened litigation against us at this time. We expect that, from time to time in the future, we may be engaged in routine litigation incidental to operating a business. Legal proceedings, even frivolous proceedings, can be costly and time consuming. The cost of any litigation would reduce the amount of expansion capital available to us and may materially impact the value of the offered securities.

Terrorist attacks or other acts of violence or war may affect our industry, operations and profitability

Terrorist attacks, whether local, national or international, may harm our results of operations and an investor’s investment as a result of fluctuations in the investing environment. There can be no assurance there will not be more terrorist attacks against the United States, U.S. businesses or key U.S. allies. These attacks or armed conflicts may directly or indirectly impact the value of our stock. Moreover, any of these

15

Table of Contents

events could cause consumer confidence and spending to decrease or result in increased volatility in the United States and worldwide financial markets and economy. They could also result in economic uncertainty in the United States or abroad. Any uncertainty in the U.S. markets may affect the amount of investable income of potential clients and may also influence investors’ behavior in ways we cannot predict, which may be particularly detrimental to our business model.

16

Table of Contents

Private Offering

Prior to this offering’s effective date, the Company conducted an offering relying on the exemption provided in Regulation D 506(c) to sell shares of Series D Convertible Preferred Stock to accredited investors. During the prior private offering, 76,637 shares of our Series D Convertible Preferred Stock were acquired for a discounted purchase price under two scenarios: (i) clients of RIAs purchased the offered securities for a seven percent (7%) discount for their client’s accounts; and (ii) clients of broker-dealers purchased the offered securities for a fifteen percent (15%) discount.

Future Dilution

We, for business purposes, may from time to time issue additional shares, which may result in dilution of existing shareholders. Dilution is a reduction in the percentage of a stock caused by the issuance of new stock. Dilution can also occur when holders of stock options (such as company employees) or holders of other convertible securities, such as warrants, exercise these convertible securities. When the number of shares outstanding increases, each existing stockholder will own a smaller, or diluted, percentage of a company, making each share less valuable. Dilution may also reduce the value of existing shares by reducing the stock’s earnings per share. There is no guarantee that dilution of the offered securities will not occur in the future.

17

Table of Contents

We are offering shares of our Series D Convertible Preferred Stock to investors in this offering. The Series D Convertible Preferred Stock may be converted into shares of our Common Stock at the discretion of each investor. As such, we are qualifying up to 2,000,000 shares of Series D Convertible Preferred Stock and up to 2,000,000 shares of Common Stock under this offering statement, of which this offering circular is a part.

The Company has engaged Lanier Securities, LLC as a placement agent (the “Placement Agent” or “Lanier”). The Company entered into an engagement letter with the Placement Agent, which defined the terms and conditions of its association with this offering. We will pay Lanier seven percent (7%) of the gross proceeds of the offering and one percent (1%) of gross proceeds of the sale for unaccountable expenses. We also paid Lanier $25,000, payable in five monthly installments, upon the execution of the engagement letter related to early stage due diligence. Lanier will provide financial advice related to the offering, and establish a selling group and marketing plan to sell the offered securities.

Dewey M. Moore, Jr., our Chief Executive Officer, is a registered representative and compliance officer for Lanier. As a registered representative of Lanier, Mr. Moore may receive commissions for any sale of Series D Convertible Preferred Stock through Lanier; however, Mr. Moore has no intention to sell Series D Convertible Preferred Stock as a registered representative of Lanier.

We have engaged Prime Trust Federal Credit Union as an escrow agent. All proceeds from the sale of Series D Convertible Preferred Stock will be deposited in an escrow account for further transfer to us upon acceptance of the subscription agreement. Since there is no minimum amount of securities that must be purchased in this offering, all accepted and approved subscription proceeds will be available to us after release from escrow and no investor funds will be reimbursed if the proceeds of this offering are insufficient to cover the costs of the offering.

We have obtained a Committee on Uniform Security Identification Procedures (CUSIP) number and anticipate applying for Depository Trust Company (DTC) eligibility; however, a trading market for the Series D Convertible Preferred Stock may never develop.

18

Table of Contents

The following section is based on estimates by management. Our actual use of the proceeds may differ depending on the exact amount invested in the offering and any foreseen or unforeseen changes to our operating landscape.

SALE OF EQUITY

| Category |

Max Proceeds | |||

| Proceeds from Sale of Shares |

$ | 20,000,000 | ||

OFFERING EXPENSES & COMMISSIONS

| Category |

Max Proceeds | |||

| Expenses1 |

$ | 350,000 | ||

| Brokerage Commissions2 |

$ | 1,400,000 | ||

| TOTAL OFFERING FEES |

$ | 1,750,000 | ||

CORPORATE APPLICATION OF PROCEEDS

| Category |

Max Proceeds | |||

| Repay or Exchange Senior Debt3 |

$ | 625,000 | ||

| Other Debt Repayment |

$ | 1,500,000 | ||

| Redeem or Exchange Series B and Series C Convertible Preferred Stock4 |

$ | 1,150,000 | ||

| Reservation of Proceeds for Dividend Payments5 |

$ | 1,400,000 | ||

| Technology Development & Investment |

$ | 2,000,000 | ||

| Acquisition & Growth Capital |

$ | 11,350,000 | ||

| Legal & Accounting |

$ | 225,000 | ||

| TOTAL CORPORATE USE |

$ | 18,250,000 | ||

| 1 | Includes estimated offering circular preparation, filing, printing, investor portal, web development, marketing and other fees and expenses related to the offering. |

| 2 | Registered broker or dealers who are members of the FINRA and who enter into a participating dealer agreement with the Company may sell offered securities. Such brokers or dealers may receive commissions up to seven percent (7%) of the price of the offered securities sold. Offered securities purchased by an RIA for clients will have the purchase price reduced by 7%, as no commissions may be paid to investment advisors. |

| 3 | Affiliates of our Company hold approximately $150,000 of our outstanding Senior Secured Notes. |

| 4 | If we are unable to negotiate an alternative to the requirement to purchase certain shares of Series C Convertible Preferred Stock pursuant to the Put Call Agreement, as amended, we anticipate using $350,000 to purchase the 343,136 shares required by such agreement. |

| 5 | Includes the reservation of dividends for one-year on the Series D Convertible Preferred Stock and potential accrued but unpaid dividends on any unexchanged Series B Convertible Preferred Stock. |

19

Table of Contents

TOTAL USE OF PROCEEDS

| Category |

Max Proceeds | |||

| Offering Expenses & Commissions |

$ | 1,750,000 | ||

| Corporate Application of Proceeds |

$ | 18,250,000 | ||

| TOTAL PROCEEDS |

$ | 20,000,000 | ||

OUR ACTUAL USE OF PROCEEDS MAY DIFFER DEPENDING ON THE BUSINESS AND REGULATORY LANDSCAPE.

Exchange or Repay Senior Secured Notes. We expect the holders of a significant amount of our 8% Senior Secured Notes will exchange their Notes for shares of the Series D Convertible Preferred Stock. Notes that are not exchanged will be paid off as a portion of the use of proceeds in this section. Management expects to negotiate discounted settlements with other debts and liabilities of the Company. Affiliates of the Company hold approximately $150,000 of our outstanding Senior Secured Notes.

Holders of our Series B Convertible Preferred Stock will also have an opportunity to exchange their Series B Convertible Preferred Stock for shares of Series D Convertible Preferred Stock. We expect a significant portion of the Series B Convertible Preferred Stock to exchange into the Series D Convertible Preferred Stock.

Technology Investment & Development. We intend to make investments in technology to put us on the “cutting edge” with other nationally recognized RIA and wealth management firms.

Dividend Reserve Account. We intend to keep segregated in a separate account the funds necessary for the payment of dividends on the Series D Convertible Preferred Stock and any outstanding Series B Convertible Preferred Stock for the first year, which we believe will provide ample time for us to reach a sustainable level of profitability to service the dividend payments from profits of the Company.

Acquisition & Working Capital. Our sales and business development team at IWA has a pipeline of prospective new recruits and acquisition candidates. The Board of Directors is also considering the purchase of ILA from Mr. Moore after a fair market analysis is competed. In addition, we have developed a growth and acquisition plan for the next four years that allocates a portion of the proceeds to acquisition and aggregation of other smaller RIAs and IARs into IWM and IWA. We believe this will accelerate our growth and acquisition program, thus expanding our footprint from a regional mini-aggregator into a $5-10 billion-plus national super-aggregator.

If this offering is fully subscribed, the capital will serve to accelerate our growth plans. Additionally, we have the internal money management expertise to safely invest the excess funds at favorable risk-adjusted returns until additional acquisition opportunities are realized.

Potential Interested Transaction.

The Company has considered and will consider acquiring the ILA from Dewey M. Moore, Jr. Any transaction will be conducted on an arms-length basis for a price determined by an independent third-party evaluation and must be unanimously approved by the independent members of the Board of Directors.

20

Table of Contents

Institute for Wealth Holdings, Inc.

Summary:

Our company is the result of a successful merger in 2016 of the Institute for Wealth Management, LLC, which was founded by Matthew D. Medeiros in 2003, and Institute for Wealth Holdings, Inc., formerly Cherry, Inc., which was founded in 2008 by Dewey M. “Rusty” Moore, Jr. Both of our founders are experienced investment professionals who have demonstrated proven skills, excellence in leadership in the development of innovative products and services, and superior team building capabilities in launching successful companies.

IWM, IWA and IWC operate a dual RIA platform utilizing our proven management team to recruit and train associate investment advisers and IARs to gather AUM under a successful, client-centric national brand. We provide, through multiple custodians, a single client interface for the administration, execution and reporting for client accounts, and offer advisers online access to fee tracking and payments. Our business model separates the money management functions from the advisor marketing functions with added degrees of separation from clients’ AUM, reducing compliance risk and allowing for higher productivity by providing our advisors and IARs more time to focus on existing client relationships and prospective new clients. Our company enjoys an excellent business reputation. Since their inception, neither IWM, IWA nor their affiliates have had an unresolved customer complaint.

Our training process for advisers is structured to provide templates, support, resources, coaching and guidance for greater client retention and growth. When each new advisor joins us, the advisor receives an overview of IWM’s wealth management portfolios, policies and procedures, advertising and marketing guidelines, client enrollment materials and other information to support the advisor’s client development efforts.

Our Growth:

Our 2016 merger was our first major step to expand our national brand and increase our AUM. The merger with IWM provided us with an expansive platform, proprietary wealth management strategies, experienced leadership team, an improved technological infrastructure and a proven portfolio management philosophy.

The merger also provided us with a broader platform from which we can acquire independent IARs and smaller RIAs, and “on-board” each new advisor efficiently and effectively. The growth capital sought by this offering is intended to, in part, accelerate our management team’s ability to execute our growth plans to expand from a regional mini-aggregator, to a national $10 billion-plus super-aggregator of AUM supporting over 200 IARs and tens of thousands of clients.

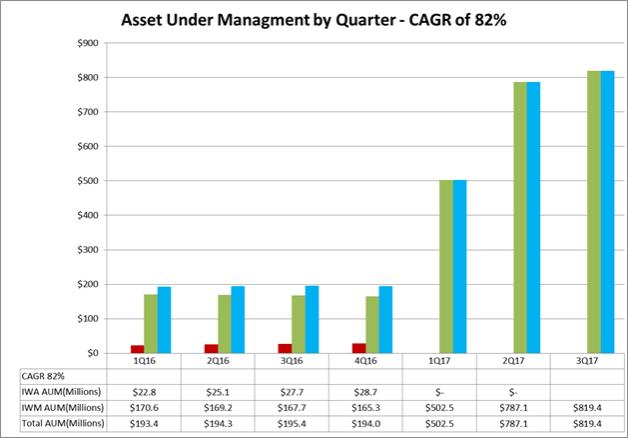

Our leadership is focused on implementing this growth strategy and we have added twenty new investment advisory professionals over the first half of 2017 alone. Our AUM has increased from under $200 million on December 31, 2016, to approximately $500 million by March 2017, over $750 million at the end of June 2017, and $819.4 million as of the end of September 2017. Since December 31, 2015, on a pro forma basis, our total revenue has increased at a CAGR of 113% and AUM has grown at a CAGR of 82%. Although this indicates robust economic growth, our management team anticipates continued rapid development and growth if we are able to obtain the expansion capital necessary to acquire new advisors and AUM.

21

Table of Contents

Our future marketing and growth plans focus on five primary distribution channels, as aligned to our own core competencies and anticipated market opportunity:

| 1. | Organic AUM Growth – We grow our AUM organically through the application of our portfolio management strategies for our clients. We grow as our clients’ assets grow. There are three phases of clients’ wealth management: (1) accumulation phase, (2) preservation phase and (3) distribution phase. Most of our clients are in the accumulation and preservation phases. We also gain AUM as we consolidate more of a client’s assets held at other firms and from inter-generational transfers, as clients receive inheritances from their parents. |

| 2. | Third-Party Broker/Dealer & RIA Network – The IWM business model has historically been to target market existing broker/dealers and independent RIAs. This strategy has been successful as IWM currently has selling agreements with more than 100 firms which offer IWM’s portfolio management services as a third-party money manager to their representatives, constituting more than 20,000 representatives. Approximately $200 million in AUM is currently a result of this network channel. IWM expects to expand its marketing efforts to this channel by hiring of additional internal wholesalers and sales representatives. |

| 3. | Robo-Advisor Portal – The proprietary software development of this proposed Robo-Advisor portal for self-directed clients began in 2010 and postponed until adequate funding could be secured for its completion. A portion of the proceeds from this offering are to be allocated to the completion of its development. When completed, this portal will allow subscribers to screen stocks for inclusion in their customized portfolios, with access to news, research and other features automatically generating risk-based profiles and suitable IWH investment program solutions according to each client’s objectives. This may provide opportunities for advisors with smaller clientele, and smaller accounts size in AUM as well as draw new direct clients to the firm who are self-directed online investors. The Company will also use this technology internally as proprietary stock screening tool in the research and selection of stocks for inclusion in various portfolios. |

| 4. | Recruiting and Business Development – IWA’s business model is primarily focused on expanding distribution by recruiting new IARs and onboarding them onto our platform and into our organizational culture. Everyone in the IWH organization, from the CEO to the IARs, are incentivized to recruit quality IARs. IWA also uses internal as well as external recruiters to execute its plan. Proceeds from this offering with enhance and expand IWA’s opportunity to recruit new IARs and onboard them and their clients into our business organization. |

| 5. | Mergers & Acquisitions – We intend to acquire smaller to medium sized RIAs and independent IARs by merging them into IWM and IWA. Many aging advisors planning for retirement are seeking a succession plan for their firms and for their clients. (See “Seasoned Advisors Aging-Out” on Page 35). IWM and IWA are well positioned to assist in the planning and transition for these professionals. A significant portion of the use of the proceeds from this offering will enhance and expand our ability to acquire and onboard them and their clients into our business organization. |

22

Table of Contents

Our Products:

We have competitive advantages as a result of our management philosophy, proven leadership, our proprietary wealth management products and technologies and our scalable investment architecture. All of our wealth management strategies are developed and managed internally, and we are therefore not dependent on using “outside” or third-party money managers. This adds to IWM’s profit center and also provides our IARs a cost effective advantage, as most independent RIAs and IARs must either hire outside money managers for a portion of the fees they charge, which cuts into their profitability, or they attempt to manage client account assets themselves. Very few independent RIAs and IARs are successful with this approach.

Through selective recruiting of advisors, we believe we are in a position to optimally manage and support the activities of our prospective advisors, providing them with our proprietary wealth management portfolios and advisor support platform as compared to smaller to mid-sized traditional RIAs that are faced with the challenges of trying to do it all themselves. The merger with IWM provided us with the brand, the advisor support platform and proprietary wealth management products to recruit or to acquire less profitable advisors and reform them into successful advisors. Our operations are dependent on the ability of our management team to recruit, manage and train enthusiastic investment advisers.

Our technology allows us to manage each of our proprietary portfolio strategies through the management of a single model for each portfolio strategy. We are then able to allocate those efficiently and cost effectively as Separately Managed Accounts (“SMAs”) across hundreds or thousands of our client accounts. These SMAs function like mutual funds, but without the costs, fees and constraints required by the mutual fund industry, thus giving our clients a lower cost, more efficient actively managed account, presumably with a greater upside potential. Our proprietary wealth management products and SMAs offer a differential advantage for our IARs and clients. These products include the following:

| • | IWM MoneyPlus: The IWM MoneyPlus strategy invests solely in cash, fixed income mutual funds and ETFs. While seeking a lower duration than traditional bond benchmarks, this strategy may incorporate cash, U.S. treasuries, government-related debts, corporate bonds, securitized bonds, derivatives and global fixed income securities. |

| • | Guaranteed Income Edge Portfolios: Our Guaranteed Income Edge Portfolios offer an optional 4 or 5% guaranteed income benefit for life (combined with an insurance certificate from a financial institution). |

| • | Signature 5 Series Portfolios with Partial Downside Protection: Our Signature 5 Series Portfolios are “Partially Protected” portfolios (backed by issuing bank). The unique component of the protected portfolios is that a portion of each portfolio has a buffer of protection of up to 20% on either 50% or 75% of the portfolio. The remainder of the portfolio remains diversified to offer an additional safety net against potential losses. These portfolios are intended to be held until maturity (currently 3 to 4 years). |

| • | Aspire Portfolios: Our Aspire Portfolios provide global allocations with downside protection. These portfolios feature the same best ideas, factor exposures and oversight as our Global Tactical Asset Allocation program, including allocations suitable across the goals and objectives spectrum. The portfolios are built around our proprietary dynamic selection models for growth versus value stocks and fixed income, designed to perform well in both bull and bear markets. |

23

Table of Contents

| • | Cherry Value: Our Large Cap Domestic Equity Stock portfolio consisting of stocks selectively managed based on a value investing philosophy and processes with the belief that quality, high yielding companies when acquired at a discount with a margin of safety to their intrinsic values offer investors superior risk-adjusted returns over the long term. The Cherry Value SMA benchmark is the S&P 500. |

| • | Cherry International: Our Mid to Large Cap International Equity Stock portfolio managed by investing abroad in stocks of quality foreign companies, selectively managed based on a value investing philosophy and processes with the belief that quality, high yielding foreign companies when acquired at a discount with a margin of safety to their intrinsic values offer investors superior risk-adjusted returns over the long term. The Cherry International SMA benchmark is the Morgan Stanley’s MSCI EAFE Index. |

| • | Cherry Dividend & Income: Our Large Cap Global Equity Stock portfolio consisting of stocks selected and managed for capital preservation and long term yield from quality blue chip companies based on a value investing philosophy and processes with the belief that quality, high yielding companies when acquired at a discount with a margin of safety to their intrinsic values offer investors superior risk-adjusted returns over the long term. The Cherry Dividend & Income SMA benchmark is the Dow Jones Global Dividend Index. |

Our investments strategies have significant track records of producing meaningful risk-adjusted returns, remaining focused on the overall strategy of managing a client’s risk first and returns second. Our various strategies include the following:

| • | Global Strategic: These are passive, strategic asset allocation portfolios constructed from the Vanguard family of mutual funds and ETFs, managed on a discretionary basis by a portfolio manager who determines the asset allocation and selects Vanguard funds for each investment style component of the portfolios based on proprietary modeling strategies. |

| • | Global Tactical Asset Allocation (GTAA): Our GTAA portfolios are managed using a research-driven process that analyzes prospective managers and their research in order to select a blend of best-of-class research partners that produce above-average, long-term returns while also reducing the likelihood of uncomfortable, short-term surprises. Concurrently, the GTAA strategy, similar to the objectives of many large endowments, manages risk first and pursues returns second. |

| • | Sector Rotation: Our active, tactical management strategy designed to capture a proportionate share of S&P 500 upside in bull markets while also seeking to reduce participation in bear markets by holding above-average cash or money market balances. Proprietary quant-based entry and exit criteria are used to manage risk, determine sector weightings and determine when to increase or decrease cash/money market balances. |

| • | Unconstrained Long/Short: This is an active, tactical management strategy that uses technical analysis to pursue above-average, risk-adjusted returns with lower volatility relative to the market. |

| • | Socially Responsible Investor (SRI): Our SRI models provide a solution for investors interested in socially responsible equities. IWM uses its institutional style investing to provide a socially responsible solution through an investment universe selected by Morningstar (a leading expert in socially responsible investments). |

24

Table of Contents

Structure of Institute of Wealth Holdings

|

|

The Institute for Wealth Holdings, Inc. |

Our core competencies align with our mission to provide a comprehensive suite of premier client and advisor-centric services. Our diversified services platform and our multiple channels of distribution also

25

Table of Contents

provide the opportunity for multiple revenue streams to IWH divided in four (4) major components. We derive revenues from: (1) IWM’s portfolio and wealth management services, (2) IWA’s advisor support in practice management, coaching & development, back-office services & technology, (3) financial planning, and (4) life insurance and annuity offerings, all more specifically described below.

Portfolio & Wealth Management. Our investment philosophy is based on managing risk first and returns second. Our investment management arm has over forty strategies with significant track records, providing the full spectrum of investment options necessary for any practice, some of these are outlined in the preceding paragraph. By offering these same solutions to various outside broker-dealer and third-party asset management platforms, we are also able to effectively leverage our intellectual property, generating revenue from assets held away from our direct platforms.

Practice Management, Coaching & Development. Each advisor is encouraged to work one-on-one with an experienced investment manager or coach to learn important aspects of the business, while focusing on the individual advisors’ strengths and weaknesses. By doing so, we are able to create a personalized plan to improve their overall practice management objectives. This hands-on management increases our appeal to break-away prospects, while simultaneously increasing current AUM for an advisor and the firm.

Back-Office Service & Technology. Through direct investments in technology and close partnerships with allied firms, our technology platform allows advisors to spend more time with their clients and less time administrating each account. Our back office team actively supports new advisors allowing them to focus on client development and asset management, as most independent advisors must spend approximately fifty percent (50%) of the time conducting back-office services. We also feature strong relationships with each of the major custodians to provide world-class client and advisor choice.

A Financial Planning Focus. We provide financial planning services to help advisors and IARs focus on providing a more comprehensive advisory service to clients, thereby enhancing their client relationships. Our financial planning division helps advisors perform at a higher level of service to clients, and ultimately gather more AUM, additional fee based income and uncover estate planning needs for life insurance and annuities. This capability and support for IARs and clients is available to advisors through a service support desk, a dedicated para-planner to enter the clients’ data as well as a customized and IWM branded software platform with a virtual cloud storage component.

Licensed Insurance Agency Solutions. Our IARs have access to ILA, our corporate insurance agency affiliate of IWH, to offer life insurance and annuity products to their clients. Having a breadth of non-investment solutions, such as expertise and access to diversified life insurance and annuity products, means helping clients with risk management, estate planning, retirement planning and other complex life and annuity strategies to complement their full wealth management and life planning goals. Additionally, our Agency offers additional revenues for the Company and for our advisors and IARs.

Why we believe IWH will continue to grow and thrive as a successful company:

We have clear, executable growth strategies that are focused on expanding our network of IARs and growing our AUM. Since our 2016 merger, we now appeal to a much broader base of successful advisors across the country. Further, because our RIA subsidiaries are registered with the U. S. Securities and Exchange Commission, (“SEC”) rather than on a state by state basis, we can enter a new state and recruit new IARs in that state with a simple notice filing in most cases.

26

Table of Contents

We believe we can continue our rapid growth and expansion over the next few years, due to the following:

| • | Advisors in the investment industry are moving from Broker/Dealer commissions to RIA fee based compensation models in which IWH already has an established market share. |

| • | Cerulli Associates forecasts that independent RIAs will control more assets than all brokerage firms by 2020. |

| • | The compliance costs and regulatory complexity (such as the recently implemented Department of Labor fiduciary rule) inhibits independent IARs and small RIA firms, and therefore presents us with merger and acquisition opportunities. |

| • | We are a fully integrated dual RIA and investment management platform that is well positioned to capitalize on these trends. |

| • | IWM’s multiple custodians; e.g.: TD Ameritrade, Schwab, Fidelity, Pershing, Folio Institutional, Kingdom Trust, and others provide easy avenues for IARs and clients to move to IWM. |

| • | We believe that with the growth and acquisition capital from this offering we have the ability to acquire small RIAs and independent IARs to grow our AUM to $5-10 billion. |

| • | We believe RIAs with under $100 million in AUM need to join affiliated organizations with a larger platform that can provide technology, compliance and systems required in an increasingly complex and competitive financial system. |

| • | We have begun an aggressive acquisition program, finding smaller RIAs eager to join an organization with superior technology and compliance capabilities. |

| • | We boast a 82% CAGR in combined AUM since December 31, 2015. |

| • | IWA’s succession plan program allows retiring IARs to sell their client relationships & AUM to IWH for cash plus an “earn-out” based on performance. |

| • | We will solicit break-away brokers and independent IARs who would prefer a fee-based advisory model to merge their firm into IWM, IWA or IWC. |

| • | IWA has an active recruitment program using third-party recruiting firms for which we pay a fee for the onboarding of qualified candidates. |

27

Table of Contents

As shown above, since our merger with IWM, we have been able to rapidly accumulate AUM.

28

Table of Contents

Consistent with our AUM growth, since the merger with IWM, we have seen an increase in revenue, as shown above.

29

Table of Contents