IROQUOIS VALLEY FARMLAND REIT, PBC

An offering of up to $65,000,000 in Common Stock

| Per Share | Total Maximum | |||||||

| Public Offering Price (1) | $ | 108.06 | $ | 65,000,000 | (2) | |||

| Underwriting Discounts and Commissions (3) | $ | – | $ | – | ||||

| Proceeds to Us from this Offering to the Public (Before Expenses) | $ | 108.06 | $ | 65,000,000 | ||||

| (1) | The price per share of common stock shown was determined by our board of directors based on the net asset value (NAV) of the Company and will apply until an alternate price is approved by the board of directors. Details of our valuation policy are contained in this offering circular. We expect to update our share price at least twice per year, typically in the winter and the summer. This is a “best-efforts” offering. | |

| (2) | Of this total, $1,000,000 of these shares are reserved for our Dividend Reinvestment Program, with the remainder allocated to this continuous offering of our shares to the public, subject to the limitations herein. Through this offering under SEC Regulation A, Tier 2 (this “Offering”), we are offering up to $65,000,000 in shares of our common stock, which represents the value of the shares available to be offered as of the date of this offering circular out of the rolling 12-month maximum offering amount of $75,000,000. | |

| (3) | There are no underwriting fees associated with this Offering. The Company has and will continue to sell its common stock directly, on a “best-efforts” basis. Our officers will not receive any commission or any other remuneration for these sales however we have previously engaged a placement agent to support sales efforts directed at institutional and other large investors and may engage similar commission-based sales support in the future. See the section of this Offering Circular titled “Plan of Distribution.” |

Generally, no sale may be made to you in this Offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

There is no public market for our securities. Investment in our shares is subject to substantial risks. See the section of this Offering Circular titled “Risk Factors.”

This Offering Circular follows the Form-S11 disclosure format.

The date of this offering circular is May 12, 2026.

The Securities and Exchange Commission (“SEC”) does not pass upon the merits of or give its approval to any securities offered or the terms of the Offering, nor does it pass upon the accuracy or completeness of any Offering Circular or other solicitation materials. These securities are offered pursuant to an exemption from registration with the SEC; however, the SEC has not made an independent determination that the securities offered are exempt from registration.

Neither the SEC nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this Offering Circular. Any representation to the contrary is a criminal offense.

The mailing address of our principal executive office is:

Iroquois Valley Farmland REIT, PBC

314 N. Main Street #200F

Roanoke, IN 46783

Our telephone number is (847) 859-6645 and our website is www.iroquoisvalley.com.

The mailing address and telephone number of our agent for service of process is:

Registered Agent Solutions, Inc.

838 Walker Road Suite 21-2

Dover, Delaware 19904

888-716-7274

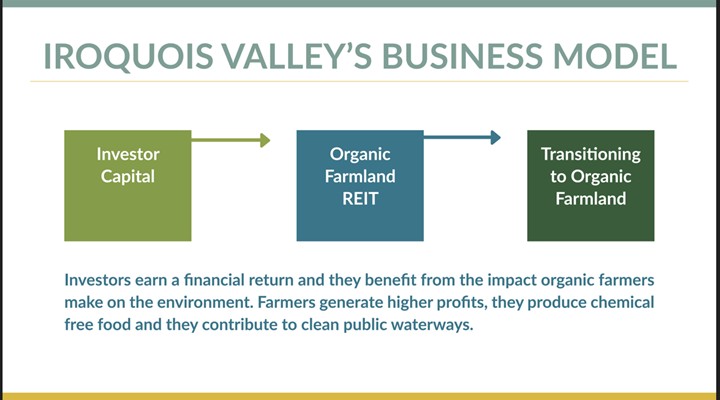

Iroquois Valley Farmland REIT, PBC, a Delaware public benefit corporation (“Iroquois Valley REIT”), is one of the first private enterprises in North America to offer investors direct exposure to a diversified portfolio of certified organic farmland.

We are offering up to $65,000,000 in our common shares to the public at an initial price of $108.06 per share. The initial minimum investment in shares of our common stock is $10,000 based on the current price per share.

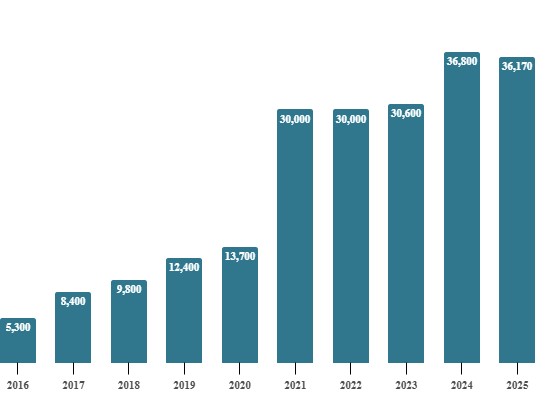

This is our third successive multi-year offering of common stock pursuant to SEC Regulation A. Since we first began offering shares for sale in this manner, beginning on May 3, 2019, we have raised nearly $67,219,367 and have issued over 752,354 shares as of the date of this offering circular. In the 12 months prior to the date of this Offering Circular, we have raised total gross offering proceeds of approximately $9,917,723 and have issued 158,643 shares of our common stock. Our total offering amount at this time is $65,000,000, representing the value of the shares available to be offered as of the date of this Offering Circular out of the rolling 12-month maximum Offering amount of $75,000,000 permitted by the SEC under Regulation A.

We expect to offer common stock in this Offering until the earlier of June 13, 2028, which is 3 years from the initial qualification date of this Offering (i.e., June 3, 2025), or the date on which we raise the maximum amount being offered, unless terminated earlier by our board of directors. In no event will we extend this Offering beyond 180 days after the third anniversary of the initial qualification date (i.e., November 30, 2028). This is a “best-efforts” offering, which means that we will use our best efforts to sell shares of common stock, but there is no obligation to purchase or sell any specific number of shares. Our shares of common stock are not being underwritten by an underwriter.

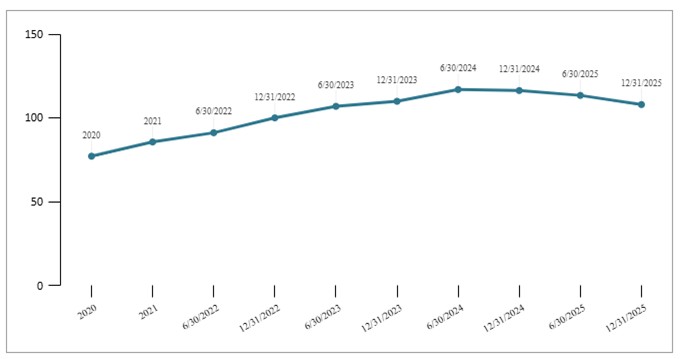

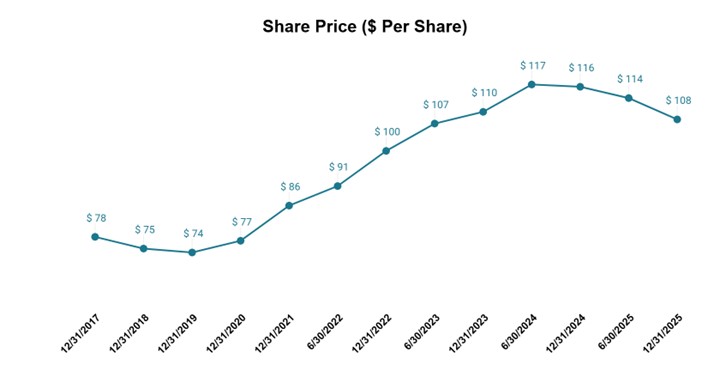

As of the date of this Offering Circular, the offering price per share of our common stock is $108.06/share. This price was determined by our board of directors and will apply until an alternate price is approved by the board of directors based on, among other factors, the appraised value of our owned farmland. We expect to update our share price at least twice per year, typically in the winter and the summer. Investors in this Offering will pay the most recent publicly announced offering price as of the date of their subscription. Our website, www.iroquoisvalley.com, will identify the current offering price per share, as will any supplements to this Offering Circular filed with the SEC. The price per share pursuant to our dividend reinvestment plan (the “DRIP”) will equal our most recently announced offering price per share. Please refer to “Policies with Regards to Certain Activities—Dividend Reinvestment Program” hereunder, and the copy of the DRIP filed with the SEC as an exhibit to our offering statement, for more details.

| ii |

There is no public trading market in which our common stock can be sold, including on any national securities exchange. It may be difficult to sell your shares. While we will look to develop secondary and internal market options, you are not guaranteed the ability to sell or trade our common stock. Transfers of our common stock will be subject to the transfer restrictions in our Certificate of Incorporation and Bylaws, each as amended, and may only be made in full compliance with applicable federal and state securities laws. We have, however, adopted and have subsequently amended a stock redemption program (the “Stock Redemption Program”) designed to provide our stockholders with limited liquidity approximately four times a year, but eligibility for this program is subject to a 5-year holding period, with caps on the number of shares that can be redeemed each period, and other restrictions. Any repurchases of shares made pursuant to our Stock Redemption Program will be made at the most recently announced offering price per share. Please refer to the “Policies with Regards to Certain Activities—Stock Redemption Program” section hereunder, and the copy of the Stock Redemption Program filed with the SEC as an exhibit to our offering statement, for more details.

We conduct our business and own our farmland investments through our “operating company,” Iroquois Valley Farms LLC, an Illinois limited liability company (“Iroquois Valley LLC”), which was formed on June 5, 2007. Iroquois Valley REIT owns 99% and is the sole manager of Iroquois Valley LLC. Iroquois Valley Farmland TRS, Inc. (“Iroquois Valley TRS” or our “TRS”), a taxable REIT subsidiary of Iroquois Valley REIT, owns the remaining 1% of Iroquois Valley LLC.

References to “Iroquois Valley,” “we,” “our,” “us” or “Company” refer to the entire Iroquois Valley corporate family, namely Iroquois Valley REIT together with its consolidated subsidiaries, including our operating company, Iroquois Valley LLC (as well as any subsidiaries thereof) and Iroquois Valley TRS.

While the nature of business to be conducted or promoted by us must always be to engage in any lawful act or activity for which corporations may be organized under the General Corporation Law of Delaware, as a public benefit corporation, Iroquois Valley REIT and its board of directors will consider our public benefit objectives in addition to the financial interests of shareholders when making decisions. We manage our business in a manner that balances our stockholders’ pecuniary interests, the interests of those materially affected by our conduct, and the public benefit described in our Certificate of Incorporation. Our specific public benefit purpose is enabling healthy food production, soil restoration, and water quality improvement through the establishment of secure and sustainable farmland access tenures.

Historically, fee-only and fee-based financial advisors have provided a significant portion of our funds raised. We intend to continue to focus on these types of financial advisors in marketing and selling our shares. No commission or other remuneration will be paid to any member of our board of directors or executive officers in connection with the sale of common stock pursuant to this Offering. In addition, we have engaged Michael E. Tobin of Access Securities to support sales efforts directed at institutional and other large investors. Mr. Tobin shall receive commissions of 0.35% of the amount of capital raised from investors introduced by him, payable in cash or equivalent value of our Company shares, at our discretion. Once earned, to the extent we pay such commissions in cash, they would reduce proceeds to us from this Offering. We reserve the right in the future and without notice to engage additional placement agents or broker-dealers (or both) to assist in selling our common stock offered here. In the event that we do engage such placement agent or broker-dealer (or both), the resulting professional fees will further reduce our proceeds from this Offering by the amount of the total of such fees and commissions.

| iii |

This investment involves a high degree of risk. You should purchase these securities only if you can afford the complete loss of your investment. Potential investors are urged to consult their tax advisors regarding the tax consequences to them, in light of their particular circumstances, of acquiring, holding, and disposing of our common stock. See “Risk Factors” for risks to consider before buying shares of our common stock, including the following:

| · | Our prior performance, as well as that of our affiliated entities, may not predict our future results. Therefore, there is no assurance that we will achieve our investment objectives. | |

| · | Iroquois Valley REIT is a public benefit corporation, and as such may make decisions or pursue strategies that do not maximize financial gain, and consequently, could reduce the value of shares of our common stock offered hereby or the amount of distributions we make to holders of our shares. | |

| · | Although you can review information about our current portfolio within this Offering Circular, you will not be able to evaluate a significant number of our future farmland investments to be acquired while you are a shareholder prior to purchasing shares of our common stock, especially given that you should expect to hold your shares for at least five years. Our management team, which reports to our board of directors, analyzes investments. Please refer to the section titled “Policies with Regards to Certain Activities—Management’s Investment Authority Policy”. | |

| · | This Offering is being made pursuant to rules and regulations under Tier 2 of Regulation A of the Securities Act of 1933, as amended (the “Securities Act”). The legal and compliance requirements of these rules and regulations, including ongoing reporting requirements related thereto, are still relatively untested and subject to change. | |

| · | We may not acquire a sufficiently diverse portfolio of investments to offset certain geographic, market, and other risks, and the value of your shares may vary more widely with the performance of specific assets. | |

| · | We may change our investment guidelines without shareholder consent, which could result in investments that are different from those described in this Offering Circular. | |

| · | Although our distribution policy is to use our cash flow from operations to make distributions, our organizational documents permit us to pay distributions from any source, including offering proceeds, borrowings, or sales of assets. We have not established a limit on the amount of proceeds we may use to fund distributions. If we pay distributions from sources other than our cash flow from operations, we will have less funds available for investments, and your overall return may be reduced. In any event, we intend to make annual distributions as required to comply with REIT distribution requirements and avoid U.S. federal income and excise taxes on retained income. |

| · | Our shares are illiquid. Our Stock Redemption Program requires a minimum 5-year holding period for eligibility, and even then you may not be able to redeem your shares exactly when you request. There is no public market for our shares, nor a specific deadline by which one will be created, if ever. There is no requirement that our operating company liquidate our portfolio by a specific date, and in fact it is generally our intent to work with our farmers to hold and steward land for organic farming on a long-term basis. Until shares of our common stock are listed, if ever, you may not be able to sell any shares of our common stock purchased hereunder. If you can sell your shares of our common stock, you may have to sell them at a substantial loss. | |

| · | If we lose our status as a REIT (currently or with respect to any tax years for which the statute of limitations has not expired) and no relief provisions apply, we would be subject to entity-level U.S. federal income tax and, as a result, our cash available for distribution to our shareholders and the value of the shares of our common stock could materially decrease, as well as other material financial consequences. | |

| · | Real estate investments are subject to general industry downturns as well as downturns in specific geographic areas. We cannot predict what the operations will yield on our farmland investments or that any tenant or mortgage or other real estate-related loan borrower will remain solvent. Global pandemics, such as the COVID-19 pandemic, and tariffs or government cut-backs may affect our farmers directly, and/or impact their supply chains, access to markets, or availability of labor. We also cannot predict the future value of our properties. Accordingly, we cannot guarantee that you will receive cash distributions or appreciation of your shares. | |

| · | Our farmland investments are subject to risks relating to the volatility in the value of the underlying real estate, default on underlying income streams, fluctuations in interest rates, and other risks associated with debt and real estate investments generally. These investments are only suitable for sophisticated investors with a high-risk investment profile. | |

| · | Investors that are (i) an employee benefit plan subject to Title I of ERISA, (ii) a plan that is subject to Section 4975 of the Code (including an IRA and Keogh plan), or (iii) an entity whose underlying assets are deemed to include “plan assets” by reason of one or more retirement plan investors’ investments in that entity are subject to additional fiduciary duties under ERISA, as discussed further under “ERISA Considerations.” Such investors must consider whether an investment in our securities is appropriate when considering such fiduciary duties. |

| iv |

| v |

Please carefully read the information in this Offering Circular and any accompanying Offering Circular supplements, which we refer to collectively as the Offering Circular. You should rely only on the information contained in this Offering Circular. We have not authorized anyone to provide you with different information. This Offering Circular may only be used where it is legal to sell shares of the common stock securities offered hereunder. You should not assume that the information contained in this Offering Circular is accurate as of any date later than the date hereof or such other dates as are stated herein or as of the respective dates of any documents or other information incorporated herein by reference.

This Offering Circular is part of an offering statement filed with the SEC, using a continuous offering process. Periodically, as we make material investments, or have other material developments, we will provide an Offering Circular supplement that may add, update, or change information contained in this Offering Circular. Any statement that we make in this Offering Circular will be modified or superseded by any inconsistent statement made by us in a subsequent Offering Circular supplement. The offering statement we filed with the SEC includes exhibits that provide more detailed descriptions of the matters discussed in this Offering Circular. You should read this Offering Circular and the related exhibits filed with the SEC and any Offering Circular supplement, together with additional information contained in our annual reports, semiannual reports and other reports and information statements that we will file periodically with the SEC.

We expect this Offering to be open until the earlier of June 13, 2028 (3 years from the initial qualification date) or the date on which we raise the maximum amount being offered, unless terminated earlier by our board of directors.

The offering statement and all supplements and reports that we have filed or will file in the future can be read at the SEC website, www.sec.gov. Also, a copy of our Offering Circular and all supplements will be posted on our website, www.iroquoisvalley.com. The contents of our website (other than the Offering Circular and supplements thereto) are not incorporated by reference in or otherwise a part of this Offering Circular.

Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

| 1 |

STATE LAW EXEMPTION AND PURCHASE RESTRICTIONS

Shares of our common stock are being offered and sold only to “qualified purchasers” (as defined in Regulation A under the Securities Act). As a Tier 2 offering pursuant to Regulation A under the Securities Act, this Offering is exempt from state “Blue Sky” law review, subject to meeting certain state filing requirements and complying with certain antifraud provisions, to the extent that our common shares offered hereby are offered and sold only to “qualified purchasers” or at a time when our common shares are listed on a national securities exchange.

“Qualified purchasers” include:

| 1. | “accredited investors” under Rule 501(a) of Regulation D, which for natural persons means, among other things, an individual whose: |

| a. | Net worth, or joint net worth with their spouse, exceeds $1,000,000 at the time of the purchase, excluding the value of their primary residence; OR | |

| b. | Earned income exceeded $200,000 in each of the 2 most recent years, or joint income with their spouse exceeded $300,000 for those years, and in either case with a reasonable expectation of the same income level in the current year. |

There are other ways natural persons can meet the definition of accredited investor, and if the investor is not a natural person, different standards apply. See Rule 501 of Regulation D for more details.

| 2. | all other investors besides “accredited investors,” so long as their investment in our common shares does not represent more than: |

| a. | 10% of the greater of their annual income or net worth (for natural persons); OR | |

| b. | 10% of the greater of annual revenue or net assets at fiscal year-end (for non-natural persons). |

Annual income and net worth should be calculated as provided in the “accredited investor” definition under Rule 501 of Regulation D. In particular, net worth in all cases should be calculated excluding the value of an investor’s home, home furnishings and automobiles.

We reserve the right to reject any investor’s subscription in whole or in part for any reason, including if we determine in our sole and absolute discretion that such investor is not a “qualified purchaser” for purposes of Regulation A.

Foreign (non-U.S.) investors may participate in this Offering only in accordance with applicable investment standards of the foreign investor’s residence and SEC Regulation S. However, such foreign purchasers may not be permitted to re-sell common stock purchased in this Offering to a U.S. person or for the account or benefit of a U.S. person for a period of 6 months from the date of purchase from us, except to qualified institutional buyers, as defined in SEC Rule 144A, or accredited investors that are institutions, as defined in SEC Rule 501(a).

| 2 |

This offering summary highlights key information regarding Iroquois Valley and this Offering of our common stock. This summary is intended solely for reference and does not contain all of the information necessary to fully evaluate this Offering. Before deciding to invest in Iroquois Valley through this Offering, you should read this complete Offering Circular carefully, including the “Risk Factors” section, and consult your own advisors.

IROQUOIS VALLEY

Iroquois Valley is an organic farmland finance company. We select, value, and manage farmland investments across the United States. Farmland investments include the acquisition of farmland, mortgage financings secured by farmland, and extending operating lines of credit to farmers, all centered around organic farming. We are one of the original private companies in North America to offer investors direct exposure to a diversified portfolio of certified organic farmland.

OUR VISION

An agricultural system transformed through land stewardship, rooted in organic farmland, for the health of people, communities, and our planet.

Embodied in this vision are the following guiding principles:

| · | Enable the next generation of young farmers to positively impact world health. |

| · | Farm with healthy, humane, and organic practices | |

| Without GMOs, toxic pesticides, herbicides, fungicides, synthetic fertilizers or other harmful chemicals. |

| · | Keep farmers on the land | |

| By indefinitely renewing their leases and preferentially selling to the farm lessee. Investor exits should not affect the ability for farmers to stay on the land. |

| · | Grow a broad-based membership | |

| Reaching thousands of like-minded investors concerned about the health of people, the planet, and financial stability. |

| · | Transition of traditional investment capital | |

| From conventional trading and extractive practices to renewable and regenerative uses. |

| · | Maintain a fair-valued, democratically-governed enterprise | |

| Enabling both investors and farmers to enjoy a stable and profitable return on their farming investment. |

| · | Protect farmland |

See “Our Business and Properties— Section 4: Our Portfolio” and “Section 6: Impact” for more about how we further this vision through our work.

We seek to achieve our vision steadily over time; however, there is no assurance that we will meet our social and environmental or portfolio objectives. See “Risk Factors.”

| 3 |

OUR STRATEGY

We intend to provide investors access to a diversified portfolio of certified organic farmland in line with our portfolio objectives and public benefit commitment. We expect to use substantially all the net proceeds of this Offering to invest in farmland investments throughout the United States. Farmland investments may include direct acquisitions of farmland, offering intermediate farm mortgage loans to farmers, or occasionally, financing organic farm stability and expansion through operating lines of credit. We may invest in farmland investments through one or more joint ventures or subsidiaries. See “Estimated Use of Proceeds.”

In selecting farmland investments, we prioritize those which will provide financial returns and further our social and environmental objectives. For real estate investments, we acquire and manage farmland properties that generate leasing revenue from tenants. A few of our legacy leases provide for both fixed rent and variable rent which is based on the farmers revenue, but we are phasing out our variable rent program and no longer include it on new leases. We directly structure, underwrite, and originate our debt investments (i.e., mortgage investments), allowing us to approach our underwriting in partnership with the farmer. Our focus with these debt instruments is to lend to farmers with a low risk of default based on due diligence supervised by our management team, Farm Impact & Stewardship Committee, and board of directors. In structuring our loan transactions, we aim to receive an acceptable risk-adjusted return and to provide the farmer with a realistic and manageable payment schedule. In addition to more quantitative underwriting criteria, we also use certain qualitative criteria in our underwriting practices to approach our portfolio building in a more mindful way, consistent with our public benefit goals.

We also seek to acquire farmland investments that reflect the diversity of activities occurring on certified organic farmland throughout the United States, with a focus on the Midwestern States. We seek to invest across a variety of operators that vary in terms of size, generational history, crop and production mixes, business plans, and supply chain practices.

MARKET OPPORTUNITIES

Our income stream from farmland investments depends in large part on organic farmers’ revenue and profitability. Demand for organic food continues to grow, largely driven by consumers’ concern for the quality, source, and nutrition of the food they eat and feed their families. Organic farmers earn a price premium for their crops at market. Studies show that, as a result, over time organic farms can be more profitable than conventional farms of a similar size, scope, and crop variety. The growing demand for organic food, coupled with the price premium for certified organic products, is fundamental to our business model. Ultimately, we believe that our farmland investments will allow us to create income for periodic dividend payments to our stockholders, in addition to social and environmental impact.

OUR COMMITMENT TO IMPACT

As a Delaware public benefit corporation, Iroquois Valley REIT and its board of directors will consider our public benefit objective in addition to the financial interests of shareholders when making decisions. In doing so, we intend to operate in a responsible and sustainable manner. Pursuant to our Certificate of Incorporation, our public benefit purpose is enabling healthy food production, soil restoration and water quality improvement through the establishment of secure and sustainable farmland access tenures.

We have taken several steps to further affirm our commitment to social and environmental impact. We first applied for and received B Corp certification in 2012 and have undergone regular assessments of our impact efforts and re-certification as a B Corp.

B Corp certification is managed by B Lab, a non-profit that measures companies against rigorous impact metrics. The B Impact Assessment is updated every 3 years to reflect feedback and best practices. In 2025, Iroquois Valley received its fourth recertification.

Iroquois Valley has been selected to the ImpactAssets IA50 each year since 2012. The IA50 is a listing of experienced private debt and equity impact investment managers that is updated annually by ImpactAssets, a non-profit organization that promotes a capital ecosystem for optimal social, environmental, and financial impact. Our tenure on this list led to special recognition as an Emeritus Manager in 2025.

| 4 |

OUR STRUCTURE

This is an Offering of the common stock of Iroquois Valley REIT. We make our farmland investments through our operating subsidiary, Iroquois Valley LLC. Iroquois Valley REIT is the manager of and owns (directly and indirectly) 100% of Iroquois Valley LLC.

See “Our Business and Properties—Section 1: Corporate Structure” and “Summary of Iroquois Valley LLC’s Operating Agreement” for more information about our corporate structure.

DIRECTORS AND OFFICERS

Iroquois Valley REIT is led by a board of directors elected by our shareholders. The board has full authority to manage the business and affairs of the Company. Several of our directors, including our Chairperson, are either active farmers or involved with farming and gardening operations. In 2023, the Company adopted a policy that the percentage of portfolio farmers represented on the board shall not exceed 33% of the total number of Directors on the board at the time of appointment or nomination. Our board has created and delegated certain authority to certain committees. See “Policies with Regards to Certain Activities—Committees of the Board of Directors.”

The board of directors appoints corporate officers to both Iroquois Valley REIT and Iroquois Valley LLC. We compensate our officers and other employees, typically through salaries and performance-based bonuses. Non-employee directors are compensated in accordance with our Non-Employee Director Compensation Policy.

For additional detail, including biographies of directors and officers, see “Directors and Officers” and “Management Compensation.”

TABLE SUMMARY OF KEY INFORMATION ABOUT THIS OFFERING OF COMMON STOCK

The table below provides a summary of key additional features of this Offering of common stock. The table below is intended to serve as a reference only and is qualified in its entirety by reference to the Offering Circular.

| The Offering |

We are offering up to $65,000,000 in shares of common stock of Iroquois Valley REIT at $108.06 per share. The initial minimum investment in shares of our common stock is $10,000. We are making this Offering available to U.S. investors subject to SEC Regulation A and to non-U.S. investors subject to SEC Regulation S and local securities laws. For additional detail on eligibility for participation in this Offering and related matters, see “Plan of Distribution.”

This Offering is our third successive Regulation A Offering. From the start of our initial offering on May 3, 2019, through the date of this offering circular, we have raised total aggregate gross offering proceeds of nearly $67,219,367 and have issued over 752,354 shares of our common stock. In the past 12 months, we have raised total aggregate gross offering proceeds of approximately $9,917,723 and have issued 158,643 shares of our common stock.

We expect to offer common stock through this Offering until the earlier of June 13, 2028, which is 3 years from the initial qualification date of this Offering, or the date on which we raise the maximum amount being offered, unless our board terminates the Offering at an earlier time. In no event will we extend this Offering beyond 180 days after the 3rd anniversary of the initial qualification date of this Offering (i.e., November 30, 2028). We reserve the right to terminate this Offering for any reason at any time.

|

| Voting Rights | Each common stockholder is entitled to one vote per share on all matters voted on by stockholders, including election of our board of directors. See the sections of this Offering Circular titled “Description of Common Stock” and “Certain Provisions of Delaware Law and our Charter Documents.” |

| 5 |

| Summary of Risk Factors |

Investing in shares of our common stock is subject to many risks. These risks include, without limitation:

· risks related to our business model and the farms in which we invest; · risks related to compliance with securities laws and other laws and regulations; · risks related to real estate and real estate-related assets; · risks related to our use of leverage; and · risks related to our REIT status and other tax risks.

You should carefully review the “Risk Factors” section of this Offering Circular, which contains a detailed discussion of material risks that you should consider before you invest in us.

|

|

Conflicts of

|

We are subject to various conflicts of interest arising out of our activities with respect to certain relationships between the Company, our directors and officers, stockholders, and farm operators. See “Conflicts of Interest.”

|

|

Distributions

|

We have operated, and intend to continue to operate, in a manner that allows us to qualify Iroquois Valley REIT as a real estate investment trust (“REIT”) for U.S. federal income tax purposes. Among other requirements, REITs are generally required to distribute to shareholders at least 90% of their annual REIT taxable income (computed without regard to the dividends paid deduction and excluding net capital gain).

We expect that our board will consider and, where appropriate, declare and pay distributions annually, typically in December of each year. In some cases, we may declare and pay a spillover dividend in late spring/summer of each year, consistent with our requirements as a REIT. Distributions will be at the discretion of our board and will be based on, among other factors, our present and reasonably projected future cash flow and the REIT distribution requirements. We expect that our board will set the rate of distributions at a level that will be reasonably consistent and sustainable over time, which will be fully dependent on the yields generated by our assets.

Our goal is to provide a reasonably predictable and stable level of current income, through annual distributions, while at the same time maintaining a fair level of consistency in our net asset value. Distributions will directly impact our net asset value by reducing the amount of our assets. Over the course of your investment, your distributions plus the change in your shares’ value (either positive or negative) will produce your total return. See “Description of Common Stock.”

|

| Stock Redemption Program |

Our Stock Redemption Program is intended to provide some limited liquidity for our stockholders. Subject to certain conditions, shares become eligible for redemption following a minimum 5-year holding period. A copy of our Stock Redemption Program is attached as an exhibit to our offering statement filed with the SEC. See also “Policies with Regards to Certain Activities—Stock Redemption Program.”

|

|

How to Subscribe

|

After reviewing and considering this Offering Circular and all exhibits, you may request to purchase stock electronically through iroquoisvalley.com, or by submitting the subscription agreement attached as an exhibit to this Offering Circular. See “How to Subscribe.”

|

|

Additional

|

Our office is located at 314 N. Main Street #200F, Roanoke, IN 46783. Our telephone number is (847) 859-6645. Information regarding the Company is also available on our website at www.iroquoisvalley.com.

If you have questions about making an investment in Iroquois Valley REIT, you may reach the investor relations team at (847) 859-6645 ext. 1 or invest@iroquoisvalleyfarms.com. |

| 6 |

QUESTIONS AND ANSWERS ABOUT THIS OFFERING

The following questions and answers highlight material information regarding us and this Offering. You should read this entire Offering Circular, including the section entitled “Risk Factors,” before deciding to purchase any shares of our common stock.

Q: What is Iroquois Valley?

A: We are one of the first private REITs to offer investors direct exposure to a diversified portfolio of certified organic farmland. Iroquois Valley is a certified B Corp and our REIT is incorporated as a Delaware Public Benefit Corporation (“PBC”). As a PBC, we conduct business that balances the interests of the shareholders with our public benefits. Our specific beneficial purpose contained in our charter is to enable healthy food production, restoring soil, and improving water quality through the establishment of secure and sustainable farmland tenures.

Q: What is Iroquois Valley’s legal structure?

A: We conduct our business and own our farmland investments through our operating company, Iroquois Valley LLC, which was formed on June 5, 2007. Effective as of December 31, 2016, to simplify tax reporting and provide opportunities to efficiently raise growth capital, the members and managers of our operating company approved and implemented a conversion: from a limited liability company owned by multiple equity owners to a three-entity operating structure.

Today, more than 900 shareholders own common stock of Iroquois Valley REIT, with no shareholder owning greater than 7.5%. In turn, Iroquois Valley REIT owns (i) 100% of Iroquois Valley TRS and (ii) 99% of Iroquois Valley LLC (with Iroquois Valley TRS owning the remaining 1% of Iroquois Valley LLC). We are offering shares of common stock of Iroquois Valley REIT in this Offering.

Iroquois Valley LLC remains our operating company, holding and managing the majority of our properties, and employing our staff and management. Iroquois Valley REIT is the sole manager of Iroquois Valley LLC. We have formed (and may again in the future form) subsidiaries to acquire certain properties. Examples of reasons to do so include to secure certain financing, to engage a joint venture partner (or partners), or for general liability protection.

Q: What is a real estate investment trust, or REIT?

A: In general, a REIT is an entity that:

| · | Combines the capital of many investors to acquire or provide financing for a diversified portfolio of real estate investments under professional management; | |

| · | Is able to qualify as a “real estate investment trust” under the Code for U.S. federal income tax purposes and is therefore generally entitled to a deduction for the dividends it pays and not subject to U.S. federal corporate income taxes on its net income that is distributed to its shareholders. This treatment substantially eliminates the “double taxation” (i.e., taxation at both the corporate and shareholder levels) that generally results from investments in a corporation; and | |

| · | Generally, pays distributions to investors of at least 90% of its annual taxable income. |

In this Offering Circular, we refer to an entity that qualifies to be taxed as a real estate investment trust for U.S. federal income tax purposes as a REIT. We elected to be treated as a REIT for U.S. federal income tax purposes commencing with our taxable year ended December 31, 2016.

| 7 |

Q: Who chooses which investments we make?

A: Subject to certain limitations established and overseen by our board of directors, our management team has authority to make farmland investments. The board has also established a Farm Impact & Stewardship Committee that, among other things, (a) considers the alignment of investment of company resources with its stated mission and public benefit statement by the establishment and periodic review of criteria/parameters for the purchase and sale of farmland investments delegated to management; (b) reviews investments or sales opportunities that fall outside the parameters delegated to management, and makes recommendations to the board; (c) evaluates whether portfolio farms and pipeline diversification, size, and practices align with the current strategic plan goals; and (d) reviews and evaluates potential new investment products for their approval and adoption by the full board. See “Policies with Regards to Certain Activities.”

Our board of directors at all times has ultimate oversight and policy-making authority, including responsibility for governance, financial controls, compliance, and disclosure with respect to our operating company, as well as the authority to make decisions related to the management of our operating company’s assets, including sourcing, evaluating, and monitoring our investment opportunities, and making decisions related to the acquisition, management, financing, and disposition of our assets, in accordance with our investment objectives, guidelines, policies, and limitations. Our board receives regular updates from management and through the Farm Impact & Stewardship Committee on potential investments, periodic introductions to Iroquois Valley farmers, and regular reports on compliance with the board’s guidance.

Q: What kind of offering is this?

A: This Offering is being conducted as a continuous offering pursuant to Rule 251(d)(3) of Regulation A, meaning that while the offering of securities is continuous, active sales of securities may happen sporadically over the term of the Offering. For administrative reasons, we typically only accept subscriptions on the 1st and 15th of every month.

Q: How does a “best efforts” offering work?

A: When our common shares are offered to the public on a “best efforts” basis, we are only required to use our best efforts to sell our common shares. No party, such as an underwriter, has a firm commitment or obligation to purchase any of our common shares.

We intend to sell up to the maximum number of shares authorized for sale by our board. However, if we raise substantially less than the maximum offering amount, it may raise material risks to our success (and your investment). For example, we may not be able to acquire a diverse portfolio of investments, and the value of shares may vary more widely with the performance of specific assets.

Q: What is the purchase price for your common shares?

A: Our current offering price is set at $108.06 per share. This price was determined by our board of directors based on the net asset value of Iroquois Valley REIT. We expect to update our share price at least twice per year, typically in the summer and the winter. Investors in this Offering will pay the most recently publicly announced offering price as of the date of their subscription.

Q: Is there any minimum investment required?

A: Yes, the minimum investment is $10,000.

| 8 |

Q: May I make an investment through my IRA or other tax-deferred retirement account?

A: Generally, yes. We currently accept investments through IRAs maintained with certain custodians. You should also understand that in making such an investment you will be required to bear the risk as to whether the investment is a non-exempt prohibited transaction under the Code or ERISA and whether such investment complies with all fiduciary duties and other obligations under ERISA. You should not consider any information in this Offering Circular to be legal, business, ERISA, or tax advice. You are urged to consider the tax, legal, and financial implications of such an investment with your own professional advisors before investing.

Q: How is an investment in your common shares different from investing in shares of other real estate investment opportunities offered on online investment platforms?

A: There are a few differences. We are one of the few non-exchange traded REITs offered directly to accredited and non-accredited investors over the internet, at a relatively low investment minimum. Although we do and may continue from time to time to hire brokers or other placement agents to help find larger investors in exchange for a commission, many of our investors come to us directly, which means we’re not paying platform fees to generate investments and can direct more money towards farmland investments. We’re also strategic in our marketing and outreach, so a very large number of our shareholders identify with or are aligned with our impact and vision, in addition to our merits as a real estate investment company.

Q: How is an investment in shares of Iroquois Valley REIT’s common stock different from investing in shares of a listed REIT?

A: Shares of a “listed REIT” are listed on a public trading market. Therefore, the fundamental difference between our common shares and those of a listed REIT is the daily liquidity available with a listed REIT. For investors with a short-term investment horizon or other reasons to desire a more liquid investment, a listed REIT may be a better alternative than investing in our shares. While we believe our shares are an alternative way for investors to deploy capital into a diversified pool of real estate assets with a lower correlation to the general stock market than listed REITs, and although we may eventually seek to list our shares on an exchange sometime in the future, currently and for the foreseeable future an investment in this Offering is highly illiquid.

Additionally, listed REITs are subject to more demanding public disclosure and corporate governance requirements than we are. While we are subject to the scaled reporting requirements of Regulation A, such periodic reports are substantially less than what typically would be required for a listed REIT.

Q: Will I have the opportunity to redeem my common shares?

A: Yes. Our Stock Redemption Program provides some limited liquidity for stockholders.

Stock redemption under this program is subject to certain restrictions and limitations, including a 5-year hold period before shares are eligible for redemption. Please refer to the copy of our Stock Redemption Program filed as an exhibit to our offering statement filed with the SEC and “Policies with Regards to Certain Activities—Stock Redemption Program.”

Q: Who pays your organization and offering costs?

A: Organization and offering costs may be paid from a variety of sources, including but not limited to cash flow from operations, proceeds of this Offering and/or securities offerings by our subsidiaries, interest or dividend income received from our investments, financing, or lines of credit from institutional lenders, the sale of farmland investments, or loan proceeds. Generally, we have few or no limitations on the amounts we may pay from such sources.

| 9 |

Q: Will I be charged upfront selling commissions?

A: Generally, no. Most investors (and all of our investors to date) do not pay upfront selling commissions as part of the price per share purchased in this Offering. Our executive officers will use commercially reasonable efforts in an attempt to offer and sell the shares, and do not receive any commission or any other remuneration for these sales. Additionally, there is no dealer-manager fee in connection with the offering and sale of our common shares through our website.

We have engaged Michael E. Tobin of Access Securities to support sales efforts directed at institutional and other large investors. As we seek to scale our impact, we believe we can present a strong investment case to mission aligned foundations, family offices, and other institutional investors, and are working with Mr. Tobin to identify and pursue these opportunities. Mr. Tobin shall receive commissions of 0.35% of the amount of capital raised from investors introduced by him, payable in cash or equivalent value of our Company shares, at the Company’s discretion. No such sales have yet to occur. Although Mr. Tobin will not receive commissions for most investments in Iroquois Valley, in the future he may facilitate such an investment, and the commission to him, if paid in cash, will reduce proceeds from that sale to the Company. See the section of this Offering Circular titled “Plan of Distribution.”

Q: What fees and expenses do you pay to any of your affiliates?

A: No commission or other remuneration will be paid to any member of our board of directors or executive officers in connection with the sale of common stock pursuant to this Offering. We compensate our executive officers and other employees, typically through salaries and performance-based bonuses. We compensate our non-employee directors in accordance with our Non-Employee Director Compensation Policy. The Company may receive reasonable market-based acquisition or closing fees associated with loan origination. We may use certain offering proceeds to reimburse expenses related to the Offering, including but not limited to legal, accounting, and filing fees. See “Management Compensation.”

Q: Does Iroquois Valley intend to use leverage?

A: Yes. We do and will continue to use leverage in making our investments. Our targeted portfolio-wide leverage is between 25-40% of the cost basis of our assets. As we continue to grow our portfolio, we may employ greater leverage on individual assets (that will also result in greater leverage of the interim portfolio) in order to quickly build a diversified portfolio of properties and assets.

Q: How often will I receive distributions?

A: We expect that our board will continue to declare and pay distributions annually in arrears; however, our board may declare other periodic distributions as circumstances dictate. Any distributions we make will be at the discretion of our board and will be based on, among other factors, our present and reasonably projected future cash flow and our requirements as a REIT. We expect that our board will set the rate of distributions at a level that will be reasonably consistent and sustainable over time, which will be fully dependent on the yields generated by our assets.

In addition, our board of directors’ discretion as to the payment of distributions is impacted by the REIT distribution requirements, which generally require that we make aggregate annual distributions to our shareholders of at least 90% of our REIT taxable income, computed without regard to the dividends paid deduction and excluding net capital gain. Moreover, even if we make the required minimum distributions under the REIT rules, we are subject to U.S. federal income and excise taxes on our undistributed taxable income and gains. As a result, our board will make such additional distributions, beyond the minimum REIT distribution, to avoid such taxes. Distributions will directly impact our net asset value by reducing the amount of our assets.

| 10 |

Q: What is the source of your distributions?

A: We may pay distributions from a variety of sources, including but not limited to cash flow from operations, proceeds of this Offering and/or securities offerings by our subsidiaries, interest or dividend income from our investments, financing or lines of credit from institutional lenders, the sale of farmland investments, or loan proceeds. Generally, we have few or no limitations on the amounts we may pay from such sources.

Q: Will the distributions I receive be taxable as ordinary income?

A: Unless your investment is held in a qualified tax-exempt account or we designate certain distributions as capital gain dividends, distributions that you receive generally will be taxed as ordinary income to the extent they are from current or accumulated earnings and profits. The portion of your distribution in excess of current and accumulated earnings and profits is considered a return of capital for U.S. federal income tax purposes and will reduce the tax basis of your investment, rather than result in current tax, until your basis is reduced to zero. Return of capital distributions made to you in excess of your tax basis in our common shares will be treated as sales proceeds from the sale of our common shares for U.S. federal income tax purposes. Distributions we designate as capital gain dividends are generally taxable at long-term capital gains rates for U.S. federal income tax purposes.

However, because each investor’s tax considerations are different, you should consult with your tax advisor prior to making an investment. You also should review the section of this Offering Circular entitled “U.S. Federal Income Tax Considerations,” including for a discussion of the special rules applicable to distributions in redemption of shares and liquidating distributions.

Q: May I reinvest my cash distributions in additional shares?

A: Generally, yes, provided that you are an accredited investor and your investment in shares of our common stock is permitted pursuant to the limitations imposed under Regulation A as well as other restrictions on ownership and transfer of the stock in Iroquois Valley REIT’s Bylaws.

Under the terms of our dividend reinvestment plan (“DRIP”), accredited investors may elect to have their cash distributions automatically reinvested into the Company in exchange for additional shares at the then current offering price. Participation in the DRIP does not relieve participants of any taxes that may be payable as a result of distributions, however, even if distributions are paid in the form of shares rather than cash.

Please refer to the copy of our DRIP filed as an exhibit to our offering statement filed with the SEC and see “Policies with Regards to Certain Activities—Dividend Reinvestment Program.”

Q: Who might be interested in making an investment in your shares?

A: An investment in our shares may be of interest to you if you seek to diversify your personal portfolio with a real estate investment vehicle focused on organic farmland properties and other select real estate-related assets, seek to receive current income, or seek to preserve capital and are able to hold your investment for a time period consistent with our liquidity strategy. On the other hand, we caution prospective investors who require immediate liquidity or guaranteed income, or who seek a short-term investment, that an investment in our shares will not meet those needs.

Any investment in Iroquois Valley is subject to substantial risks and should not be taken lightly. No assurance can be given that a shareholder will receive dividends, will be repaid his/her/its investment, or that an investor will not lose the entire investment. You should consult with your tax, financial, and legal advisors before making an investment.

| 11 |

Q: Are there any risks involved in buying your shares?

A: Yes. Investing in our common shares involves a high degree of risk. If we are unable to effectively manage the impact of these risks, we may not meet our investment objectives. You should purchase these securities only if you can afford a complete loss of your investment. See “Risk Factors” for a description of the risks relating to this Offering and an investment in our shares.

Q: What will you do with the proceeds from the Offering?

A: We have used, and intend to continue to use, substantially all of the net proceeds from this Offering (after paying or reimbursing organization and offering expenses) to invest in and manage a diverse portfolio of assets primarily consisting of organic farmland properties. However, our management team, led and overseen by our board of directors, will have considerable discretion in using offering proceeds consistent with our business and beneficial impact goals. For example, we may use offering proceeds to reduce outstanding debt, provide cash for working capital purposes, or pay a dividend to stockholders.

We may not be able to promptly invest the net proceeds of this Offering in commercial real estate and other select real estate-related assets such as mortgage loans. For example, our deal flow may affect our ability to deploy available capital quickly as we conduct due diligence and evaluate prospective investments considering our business strategy and impact goals. In the interim, we may invest in short-term, highly liquid or other authorized investments. Such short-term investments will not earn as high of a return as we expect to earn on our real estate-related investments.

Q: How long will this Offering last?

We expect to offer common stock through this Offering until the earlier of June 13, 2028, which is 3 years from the initial qualification date of this Offering, or the date on which we raise the maximum amount being offered, unless our board terminates the Offering at an earlier time. In no event will we extend this Offering beyond 180 days after the 3rd anniversary of the initial qualification date (i.e., November 30, 2028). We reserve the right to terminate this Offering for any reason at any time.

Q: Will I be notified of how my investment is doing?

A: Yes, we will provide you with periodic updates on the performance of your investment, including:

| · | an annual report; | |

| · | a semi-annual report; | |

| · | current event reports for specified material events within 4 business days of their occurrence; | |

| · | supplements to the offering circular, if we have material information to disclose to you; and | |

| · | other reports that we may file or furnish to the SEC from time to time. |

We will provide this information to you by posting such information on the SEC’s website at www.sec.gov.

In addition, we send a monthly newsletter in which we highlight various news and projects at Iroquois Valley and our portfolio of farms. All investors are added to the newsletter distribution list upon investment, and anyone can sign up on our website at www.iroquoisvalley.com. We also seek to host quarterly updates and webinars for investors, as well as an annual shareholders meeting, so that you will be able to hear from Iroquois Valley staff, board members, farmers, and other partners.

The SEC requires certain material information to be contained in the filings listed above. Typically, the monthly newsletter will highlight some of that material information, but may also include more information like farmer profiles, impact success stories, team updates, and so on.

| 12 |

Q: When will I get my detailed tax information?

A: Your IRS Form 1099-DIV tax information, if required, will be provided by January 31 of the year following each taxable year.

Q: How do I buy shares?

A: You may purchase shares of our common stock in this Offering by filling out a subscription agreement like the one attached as an exhibit to this Offering Circular. This process can be completed electronically through our investor portal or submitted by mail as per the instructions on the subscription agreement. Please request access to the portal by visiting our website, www.iroquoisvalley.com. As part of the subscription process, you will need to select an investment amount and pay for the shares at the time you subscribe. If you have questions, you may reach an investor relations team member at (847) 859-6645 ext. 1. See “How to Subscribe.”

Q: Who can help answer my questions about the Offering?

A: If you have more questions about the Offering, or if you would like additional copies of this Offering Circular, you should contact us by writing, emailing, or telephoning us at:

Iroquois Valley Farmland REIT, PBC

314 N Main St.

Ste. 200 F, Roanoke, IN 46783

Investor Relations Department

invest@iroquoisvalleyfarms.com

(847) 859-6645 ext. 1

| 13 |

An investment in shares of our common stock involves risks. You should specifically consider the following material risks in addition to the other information contained in this Offering Circular before you decide to purchase shares of our common stock. The occurrence of any of the following risks might cause you to lose all or a significant part of your investment. The risks and uncertainties discussed below are not the only ones we face but represent those we believe are most significant to our business, operating results, financial condition, prospects, and forward-looking statements. In addition, some statements in this Offering Circular, including statements in the following risk factors, constitute forward-looking statements. See “Cautionary Note Regarding Forward-Looking Information.”

RISKS RELATED TO OUR BUSINESS AND FARMS

The geographic concentration of our portfolio could cause us to be more susceptible to adverse weather, economic or regulatory changes or developments in the markets in which our farms are located than if we owned a more geographically diverse portfolio, which could materially adversely affect the value of our farms and our ability to lease our farms on favorable terms or at all.

We are susceptible to developments or conditions in the states and/or the specific counties in which our farms are located, including adverse weather conditions (such as drought, windstorms, tornadoes, floods, hail and temperature extremes), transportation conditions (including conditions relating to truck and rail transportation and the navigation of the Mississippi River), crop disease, pests and other adverse growing conditions, health crises and pandemics, and unfavorable or uncertain political, economic, business or regulatory conditions (such as changes in price supports, subsidies and environmental regulations). Any such developments or conditions could materially adversely affect the value of our farms and our ability to lease our farms on favorable terms or at all, which could materially adversely affect our financial condition, results of operations, cash flow, and ability to make distributions to our stockholders.

Our portfolio is concentrated in a limited number of farms, which subjects us to an increased risk of significant loss if any farm declines in value or if we are unable to lease a farm.

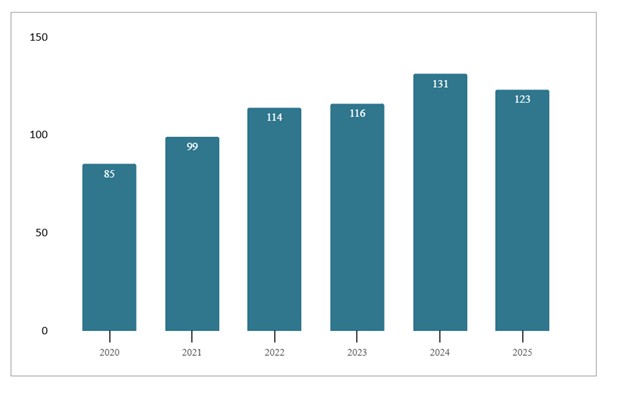

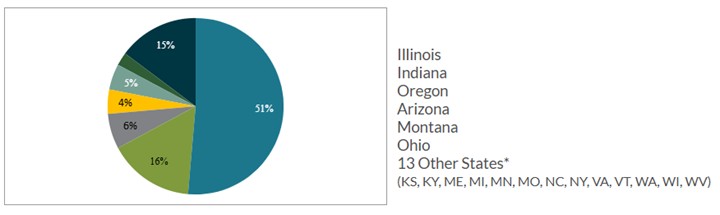

Our current portfolio includes 123 individual farmland investments (including farms, mortgages, and lines of credit) relating to farms in 19 states across the U.S. However, in many cases, we have made multiple investments in a single farm or farmer, and nearly half of our farms are located in the state of Illinois. (See “Our Business and Properties—Section 5: Our Portfolio”). The aggregate returns we realize may be substantially adversely affected by the unfavorable performance of a small number of farm operations or a significant decline in the value or success of any single property. Lack of diversification will increase the potential that a single underperforming investment could have a material adverse effect on our cash flows and the price we could realize from the sale of our farms.

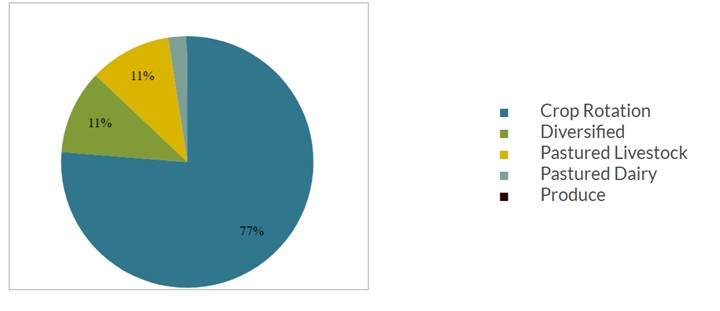

Our investments in pastured livestock and dairy farms have additional capital risks compared to our commodity and specialty/vegetable row crop farms because if diseased or damaged, it requires multiple years and substantial capital to redevelop the revenue producing assets, which could materially adversely affect our results of operations and ability to make distributions to our stockholders.

A number of our farms are focused on pastured livestock for either dairy or meat production. See “Our Business and Properties” for additional details on our current portfolio. And in the future, we most likely will add to our investments in farmland used for pastured livestock and, under limited circumstances, dairy production. Such investments would increase our concentration of livestock-based investments. Livestock production involves more risk than annual vegetable and commodity row crops because it requires more time and a greater capital investment. If a farmer loses part of its herd to flooding, fire, or disease, there would generally be significant time and capital needed to replace the animals and it may take years to resume production.

| 14 |

We currently lease many of our farms to small and medium-sized independent farming operations, and younger farmers, which may have limited financial and personnel resources and, therefore, may be less stable than larger companies or agribusinesses, which could impact our ability to generate rental revenue.

We lease many of our farms to small- and medium-sized farming operations, which will expose us to several unique risks. For example, small- and medium-sized agricultural businesses may be less able than larger farming operations to make lease payments when they experience adverse events. In addition, our target tenants for our organic grain farms may face intense competition, including competition from companies with greater financial resources, which could lead to price pressure on crops that could lower our tenants’ income, which in turn could impact our ability to generate rental revenue. Furthermore, the success of f small- and medium-sized farming businesses may also depend on the management talents and efforts of one or a small group of persons. The death, disability, or resignation of one or more of these persons could have a material adverse impact on our farmers and, in turn, on us.

In addition, our tenants and borrowers are frequently younger farmers. Young farmers may have less experience overall, particularly regarding the business planning associated with taking on substantial lease and mortgage obligations. At the same time, the young farmers we work with are generally more experienced given what are typically strong family farming backgrounds. These “multi-generational” farmers have often established or expanded their businesses after growing up farming with parents and grandparents. Thus, they likely have multi-generational and community support structures to offer guidance. Nevertheless, it is a fact that these young farmers have less years of experience than an older farmer would generally have.

Our business is dependent in part upon the profitability of our tenants’ and borrowers’ farming operations, and any downturn in the profitability of their farming operations could have a material adverse effect on the amount of rent we can collect and, consequently, our cash flow and ability to make distributions to our stockholders.

We depend on our tenants and borrowers to operate the farms in a manner that generates sufficient revenue to allow them to meet their obligations to us, including their obligations to pay rent or interest, as well as pay real estate taxes, maintain certain insurance coverage and maintain the farms generally. These obligations depend, in part, upon the overall profitability of their farming operations, which could be adversely impacted by, among other things, adverse weather conditions, crop prices, global supply of arable farmland, crop disease, pests, contaminants, and unfavorable or uncertain political, global health, economic, business, or regulatory conditions. We can provide no assurances that, if a tenant defaults on its obligations to us under a lease, we will be able to lease or re-lease that property on economically favorable terms in a timely manner, or at all. In addition, we may experience delays in enforcing our rights as a landlord and may incur substantial costs in protecting our investment.

Due to the nature of crops as a commodity, there is a risk that crop prices could fall to levels that will not sustain an ongoing operation and may result in default or payment delays. Similarly, farming has historically been a marginally profitable business and, therefore, projected profits or variable rent payments, if any, may not materialize. Any downturn in the profitability of the farming operations of our tenants/borrowers, without insurance to make up the difference, or a downturn in the agricultural industry in general could have a material adverse effect on our financial condition, results of operations, cash flow, and ability to make distributions to our stockholders. Although we continue to seek means to reasonably diversify our portfolio, concentration in our portfolio may exacerbate any potential impacts.

Global health crises could negatively impact our farmland investments.

Global health crises, similar to the COVID-19 outbreak, could have a materially adverse effect on the financial condition of farms in our portfolio. Pandemics similar to COVID-19, or a resurgence of COVID-19, may cause market volatility in commodity prices and could result in other market uncertainties. Pandemics affect demand for certain products from the wholesalers, distributors, processors, cooperatives, and producers to whom our farmers sell, and it is likely that the outbreak of a similar pandemic will cause an economic slowdown. Our farmers’ ability to grow their businesses, contract for labor and supplies, sell crops, and access supply chains could be materially affected. Risks related to an epidemic, pandemic, or other health crisis such as COVID-19 could severely disrupt farmer operations and thus lower the lease and mortgage revenue from our farmland investments.

| 15 |

We may be subject to risks associated with our tenants’ and borrowers’ financial condition and liquidity position.

A majority of our leases do not require the full payment of rent in cash in advance of the planting season, which subjects us to credit risk exposure to our farm-operator tenants and the risks associated with farming operations, such as weather, commodity price fluctuations and other factors. We will also be exposed to these risks with respect to flexible leases for which a portion of the rent is based on a percentage of a tenant’s farming revenues and leases with terms greater than 1 year. We also may not become aware of a tenant’s financial distress until the tenant fails to make payments to us when due, which may significantly reduce the amount of time we have to evict the tenant and re-lease the property to a new tenant before the start of the spring planting season, should we choose to do so. These risk scenarios also apply to our borrowers—we may have limited efficient recourse upon borrower default.

We may be unable to collect balances due on our leases or mortgages from any tenants or borrowers in bankruptcy, which could materially adversely affect our financial condition, results of operations and cash flow.

We are subject to tenant and borrower credit risk. Our tenants, particularly those that may depend on debt and leverage, could be susceptible to bankruptcy if their cash flows are insufficient to satisfy their financial obligations, including meeting their obligations to us under their leases. A tenant in bankruptcy may be able to restrict our ability to collect unpaid rent and interest during the bankruptcy proceeding and may reject the lease. If a bankrupt tenant rejects a lease with us, any claim we might have for breach of the lease, excluding a claim against collateral securing the lease, would be treated as a general unsecured claim. Our claim would likely be capped at the amount the tenant owed us for unpaid rent prior to the bankruptcy unrelated to the termination, plus the greater of 1 year of lease payments or 15% of the remaining lease payments payable under the lease, but in no case more than 3 years of lease payments. In addition, a tenant may assert in a bankruptcy proceeding that its lease should be re-characterized as a financing agreement. If such a claim is successful, our rights and remedies as a lender, compared to a landlord, will generally be more limited. In the event of a tenant bankruptcy, we may also be required to fund certain expenses and obligations (e.g., real estate taxes, debt costs and maintenance expenses) to preserve the value of our farms, avoid the imposition of liens on our farms or transition our farms to a new tenant. Again, bankruptcy by borrowers presents certain similarities. Although our mortgage loans are typically secured by properties and our lines of credit are typically secured by other borrower assets, foreclosure may not be an efficient means to re-capture our investment in a bankruptcy context and may not be the recourse selected by our board considering our broader public benefit goals. In sum, our financial condition, results of operations, and ability to make distributions to our stockholders could be materially adversely affected if a tenant or borrower declares bankruptcy.

Our failure to identify and consummate acquisitions that meet our investment criteria would significantly impede our ability to achieve our business objectives, including growing our portfolio and diversifying by geography, crop type, and farmer, which could materially adversely affect our results of operations and ability to make distributions to our stockholders.

Our ability to expand through acquisitions is integral to our business strategy and requires that we identify and consummate suitable acquisition or investment opportunities that meet our investment criteria and are compatible with our growth strategy. While we continue to actively seek and evaluate farms for potential purchase as well as potential mortgage and occasionally operating line of credit borrowers, there is no guarantee that we will be able to continue to find and acquire such assets at attractive prices (or, in the case of our loan products, borrowers) or that any such acquisitions will not initially result in our portfolio being concentrated in a certain geography or crop type.

Additionally, we compete for the acquisition of farmland and related assets with many other entities engaged in agricultural and real estate investment activities, including individual and family operators of farming businesses, corporate agriculture companies, financial institutions, institutional pension funds, real estate companies, private equity funds and other private real estate investors. Our competitors may have greater resources than we do and may be willing to pay more for certain assets or may have a more compatible operating philosophy with our acquisition targets. In addition, the number of entities and the amount of funds competing for suitable investment farms may increase, resulting in increased demand and increased prices paid for these farms. Our failure to identify and consummate acquisitions that meet our investment criteria, including our target allocation ranges for crop type, would significantly impede our ability to achieve our business objectives, including growing our portfolio and diversifying by geography, crop type, and farmer, which could materially adversely affect our results of operations and ability to make distributions to our stockholders.

| 16 |

Some state laws prohibit or restrict the ownership of agricultural land by business entities, which could impede the growth of our portfolio and our ability to diversify geographically.

Certain states in which a substantial amount of farmland is located, including for example Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, Oklahoma, South Dakota, and Wisconsin have laws that prohibit or restrict to varying degrees the ownership of agricultural land by corporations or business entities like us. Additional states may, in the future, pass similar or more restrictive laws, and we may not be legally permitted, or it may become overly burdensome or expensive, to acquire farms in these states, which could impede the growth of our portfolio and our ability to diversify geographically in states that might otherwise offer compelling investment opportunities.

We are subject to state and local land use laws, including with respect to easements, and these issues may impact our ability to implement our business plan.

Pre-existing easements may impact the value of assets we purchase or the ability of our farmers to use that land for organic farming. For certain farmland investments, we have or may pursue the establishment of a conservation easement. If successful, we may be compensated for a portion of the development value that is contributed, but such an easement restricts the usage of the property and may affect its resale value. There is no guarantee that we will be able to resell a property at its new cost basis after a conservation easement is established.

Failure to succeed in new markets could have a material adverse effect on our results of operations and ability to make distributions to our stockholders.

Our portfolio is comprised of farms located in 19 different states. We may continue to expand our geographic footprint into new markets, but any expansion into new geographies creates potential risks. As we acquire assets located in new markets, we may face risks associated with a lack of market knowledge or understanding of the local market, including the availability and identity of quality tenant or borrower farmers, forging new business relationships in the area and unfamiliarity with local government requirements and procedures. The management team may not be able to evaluate the farmer or the opportunity properly or efficiently due to geographic nuances in the market or farmland. While diversification itself is a risk mitigator, our management team may have less experience with the regional or local production models.

Geographic expansion is not a priority for Iroquois Valley. We intend to continue to serve many farmers in the Midwest and certain other hubs where we have existing relationships, confidence in supporting infrastructure (including financing, processing and transportation), and experience to inform our due diligence and allow us to support promising farmers.

Our anticipated growth, expansion, and diversification may require additional corporate infrastructure or restructuring.

It is possible that certain structural changes may be necessary in the future to most effectively manage both the legacy buy-and-lease acquisitions and the mortgage and other loan business, or for example, management of companion funds or special purpose investment vehicles. Our platform for operating our business may not be as scalable as we anticipate or able to support significant growth without substantial new investment in personnel and infrastructure.