PART II — INFORMATION REQUIRED IN OFFERING CIRCULAR

An offering statement pursuant to Regulation A relating to these securities has been filed with the Securities and Exchange Commission. Information contained in this Preliminary Offering Circular is subject to completion or amendment. These securities may not be sold nor may offers to buy be accepted before the Offering Statement filed with the Commission is qualified. This Preliminary Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy nor may there be any sales of these securities in any state in which such offer, solicitation or sale would be unlawful before registration or qualification under the laws of any such state. We may elect to satisfy our obligation to deliver a Final Offering Circular by sending you a notice within two business days after the completion of our sale to you that contains the URL where the Final Offering Circular or the Offering Statement in which such Final Offering Circular was filed may be obtained.

Subject to Completion, dated August 16, 2019

Preliminary Offering Circular

![]()

FAT Brands Inc.

1,200,000 shares of 8.25% Series B Cumulative Preferred Stock

(Liquidation Preference $25 Per Share)

Warrants to Purchase 720,000 Shares of Common Stock

We are offering up to 1,200,000 shares of our 8.25% Series B Cumulative Preferred Stock (which we refer to as the “Series B Preferred Stock”) and warrants (which we refer to as the “Warrants”) initially exercisable to purchase up to an aggregate of 720,000 shares of our common stock, par value $0.0001 per share (which we refer to as the “Common Stock”), and the shares of Common Stock issuable upon exercise of the Warrants. Each share of Series B Preferred Stock that we sell in this Offering will be accompanied by a Warrant to purchase 0.60 shares of Common Stock at an exercise price of $8.50 per share of Common Stock. Each share of Series B Preferred Stock and accompanying Warrant is being offered at a price of $25.00, for an aggregate offering amount of up to $30,000,000. The shares of Series B Preferred Stock and Warrants will be issued separately but can only be purchased together in this Offering. Each Warrant will be immediately exercisable and will expire on the five year anniversary of the date of issuance.

We will pay cumulative dividends on the Series B Preferred Stock from and including the date of original issuance in the amount of $2.0625 per share each year, which is equivalent to 8.25% of the $25.00 liquidation preference per share. Dividends on the Series B Preferred Stock will be payable quarterly in arrears based on the Company’s fiscal quarters, beginning with the fiscal quarter ended September 29, 2019.

We may not redeem the Series B Preferred Stock before the first anniversary of the initial issuance date, or , 2020. After the first anniversary of the initial issuance date we may, at our option, redeem the Series B Preferred Stock, in whole or in part, by paying $25.00 per share, plus any accrued and unpaid dividends to the date of redemption, and plus a redemption premium equal to 10% of liquidation preference prior to the second anniversary ( , 2021) or 5% of liquidation preference after the second anniversary and prior to the third anniversary ( , 2022). The Series B Preferred Stock will mature on the five-year anniversary of the initial issuance date ( , 2024) or the earlier liquidation, dissolution or winding-up of the Company. Upon maturity, the holders of Series B Preferred Stock will be entitled to receive cash redemption of their shares in an amount equal to $25.00 per share plus any accrued and unpaid dividends.

Holders of Series B Preferred Stock may optionally cause the Company to redeem all or any portion of their Series B Preferred Stock following the first anniversary of the initial issuance date, or , 2021, for an amount equal to $25.00 per share, plus any accrued and unpaid dividends, minus an early redemption fee equal to 12% of liquidation preference prior to the second anniversary ( , 2021), 10% of liquidation preference after the second anniversary and prior to the third anniversary ( , 2022), or 8% of liquidation preference after the third anniversary and prior to the fourth anniversary ( , 2023). There will be no redemption premium charged after the fourth anniversary of the initial issuance date.

Our Common Stock is traded on NASDAQ under the symbol “FAT.” There is no established public trading market for the Series B Preferred Stock or the Warrants, and we do not expect a market to develop for the Series B Preferred Stock or the Warrants. We do not intend to apply for listing of the Series B Preferred Stock or Warrants on any securities exchange, and we do not expect that the Series B Preferred Stock or the Warrants will be quoted on NASDAQ. On July 29, 2019, the last reported sale price of our Common Stock was $3.70 per share.

The Offering will terminate at the earlier of: (1) the date at which $30,000,000 of Series B Preferred Stock and Warrants has been sold, (2) the date which is one year after this Offering being qualified by the U.S. Securities and Exchange Commission (which we refer to as the “SEC” or the “Commission”), or (3) the date on which this Offering is earlier terminated by the Company in its sole discretion (which we refer to as the “Termination Date”).

This Offering is being conducted on a “best efforts” basis pursuant to Regulation A of Section 3(6) of the Securities Act of 1933, as amended (the “Securities Act”), for Tier 2 offerings. The Company may undertake one or more closings on a rolling basis. Until we complete a closing, the proceeds for the Offering will be kept in an escrow account. At a closing, the proceeds will be distributed to the Company and the associated Series B Preferred Stock will be issued to investors. If there are no closings or if funds remain in the escrow account upon termination of this Offering without any corresponding closing, the investments for this Offering will be promptly returned to investors, without deduction and generally without interest. Wilmington Trust, N.A. will serve as the escrow agent. There is a minimum purchase requirement for an investor of $500 of Series B Preferred Stock in order to participate in the Offering.

TriPoint Global Equities, LLC and Digital Offering, LLC have agreed to act as our exclusive selling agents (which we refer to as the “Selling Agents”) to offer the Series B Preferred Stock to prospective investors on a “best efforts” basis. In addition, the Selling Agents may engage one or more sub-Selling Agents or selected dealers. The Selling Agents are not purchasing the Series B Preferred Stock offered by us, and are not required to sell any specific number or dollar amount of the Series B Preferred Stock in the Offering. We expect to commence the offer and sale of the Series B Preferred Stock as of the date on which the Offering Statement of which this Offering Circular is a part (the “Offering Statement”) is qualified by the SEC.

Investing in the Series B Preferred Stock involves risks. See “Risk Factors” beginning on page 11 of this Offering Circular to read about important factors you should consider before buying the Series B Preferred Stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities or determined if this Offering Circular is accurate or complete. Any representation to the contrary is a criminal offense.

| Per Share (1) | Total | |||||||

| Public Offering Price | $ | 25.00 | $ | 30,000,000 | ||||

| Selling Agents’ Commissions (2) | $ | 1.82 | $ | 2,184,000 | ||||

| Proceeds to FAT Brands Inc. (before expenses) (3) | $ | 23.18 | $ | 27,816,000 | ||||

| (1) | Per share price represents the offering price for one share of Series B Preferred Stock and a Warrant to purchase 0.60 shares of Common Stock at $8.50 per share. |

| (2) | We have agreed to pay the Selling Agents a fee of 7.28% of the gross proceeds received by the Company in the Offering, and to issue to the Selling Agents a warrant to purchase units equal to 1.25% of the total securities sold in the Offering (the “Unit Purchase Warrant”), each unit consisting of one share of Series B Preferred Stock and one Warrant to purchase 0.60 shares of Common Stock at $8.50 per share. The Selling Agents’ Unit Purchase Warrant is exercisable at a price per unit of $25.00, commencing one year after the date of the applicable closing, and will be exercisable for five years after the effective date of the offering. We have also agreed to reimburse certain expenses to our Selling Agents. Please refer to the section entitled “Plan of Distribution” in this Offering Circular for additional information regarding total Selling Agents compensation. |

| (3) | We estimate that our total expenses for the Offering will be approximately $266,000, in addition to Selling Agents’ commissions. |

NO SALE MAY BE MADE TO YOU IN THIS OFFERING IF THE AGGREGATE PURCHASE PRICE YOU PAY IS MORE THAN 10% OF THE GREATER OF YOUR ANNUAL INCOME OR NET WORTH. DIFFERENT RULES APPLY TO ACCREDITED INVESTORS AND NON-NATURAL PERSONS. BEFORE MAKING ANY REPRESENTATION THAT YOUR INVESTMENT DOES NOT EXCEED APPLICABLE THRESHOLDS, WE ENCOURAGE YOU TO REVIEW RULE 251(d)(2)(i)(C) OF REGULATION A. FOR GENERAL INFORMATION ON INVESTING, WE ENCOURAGE YOU TO REFER TO www.investor.gov.

THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OF OR GIVE ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SOLICITATION MATERIALS. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE SEC HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION.

For more information concerning the procedures of the Offering, please refer to “Plan of Distribution” beginning on page 58, including the sections “— Investment Limitations” and “— Procedures for Subscribing.”

This Offering Circular follows the disclosure format of Part I of Form S-1 pursuant to the general instructions of Part II(a)(1)(ii) of Form 1-A.

Book-Running Manager

Tripoint Global Equities

Co-Manager

Digital Offering

The date of this Offering Circular is 2019.

TABLE OF CONTENTS

We include cross references in this Offering Circular to captions elsewhere in these materials where you can find further related discussions. The following table of contents tells you where to find these captions:

INCORPORATION OF DOCUMENTS BY REFERENCE

The SEC allows us to incorporate by reference the information we file with it, which means that we can disclose important information to you by referring you to another document that we have filed separately with the SEC. We hereby incorporate by reference the following information or documents into this Offering Circular:

| ● | the following sections of our Annual Report on Form 10-K for the fiscal year ended December 30, 2018, filed with the SEC on March 29, 2019: |

Any information in any of the foregoing documents will automatically be deemed to be modified or superseded to the extent that information in this Offering Circular or in a later filed document that is incorporated or deemed to be incorporated herein by reference modifies or replaces such information.

We urge you to carefully read this Offering Circular and the documents incorporated by reference herein, before buying any of the securities being offered under this Offering Circular. This Offering Circular may add or update information contained in the documents incorporated by reference herein. To the extent that any statement that we make in this Offering Circular is inconsistent with statements made in the documents incorporated by reference herein, you should rely on the information in this Offering Circular and the statements made in this Offering Circular will be deemed to modify or supersede those made in the documents incorporated by reference herein.

You should rely only on the information contained in this Offering Circular or incorporated herein by reference. We have not authorized anyone to provide you with different information. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this Offering Circular or incorporated herein by reference. You should not rely on any unauthorized information or representation. This Offering Circular is an offer to sell only the securities offered hereby, and only under circumstances and in jurisdictions where it is lawful to do so. You should assume that the information in this Offering Circular is accurate only as of the date on the front of the applicable document and that any information we have incorporated by reference is accurate only as of the date of the document incorporated by reference, regardless of the time of delivery of this Offering Circular, or any sale of a security.

We further note that the representations, warranties and covenants made by us in any agreement that is filed as an exhibit to any document that is incorporated by reference in this Offering Circular were made solely for the benefit of the parties to such agreement, including, in some cases, for the purpose of allocating risk among the parties to such agreements, and should not be deemed to be a representation, warranty or covenant to you. Moreover, such representations, warranties or covenants were accurate only as of the date when made. Accordingly, such representations, warranties and covenants should not be relied on as accurately representing the current state of our affairs.

Unless otherwise mentioned or unless the context requires otherwise, all references in this Offering Circular to “FAT Brands,” “the Company,” “we,” “us,” and “our” refer to FAT Brands Inc., a Delaware corporation, and its subsidiaries.

Upon written or oral request, we will provide you without charge a copy of any or all of the documents that are incorporated by reference into this Offering Circular, including exhibits which are specifically incorporated by reference into such documents. Requests should be directed to: FAT Brands Inc., Attention: Investor Relations, 9720 Wilshire Blvd., Suite 500, Beverly Hills, CA 90212, telephone (310) 319-1850.

| i |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained in this Offering Circular may not be based on historical facts and are “Forward-Looking Statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements other than statements of historical facts contained in this Offering Circular may be forward-looking statements. Statements regarding our future results of operations and financial position, business strategy and plans and objectives of management for future operations, including, among others, statements regarding expected new franchisees, brands, store openings and future capital expenditures are forward-looking statements. In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “could,” “intends,” “targets,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “potential” or “continue” or the negative of these terms or other similar expressions.

Forward-looking statements are subject to significant business, economic and competitive risks, uncertainties and contingencies, many of which are difficult to predict and beyond our control, which could cause our actual results to differ materially from the results expressed or implied in such forward-looking statements. These and other risks, uncertainties and contingencies are described elsewhere in this Offering Circular, including under “Risk Factors,” and in the documents incorporated by reference herein, and include the following factors:

| ● | our inability to manage our growth; | |

| ● | the actions of our franchisees; | |

| ● | our inability to maintain good relationships with our franchisees; | |

| ● | our inability to successfully add franchisees, brands and new stores, and timely develop and expand our operations; | |

| ● | our inability to protect our brands and reputation; | |

| ● | our ability to adequately protect our intellectual property; | |

| ● | success of our advertising and marketing campaigns; | |

| ● | our inability to protect against security breaches of confidential guest information; | |

| ● | our business model being susceptible to litigation; | |

| ● | competition from other restaurants; | |

| ● | shortages or interruptions in the supply or delivery of food products; | |

| ● | our vulnerability to increased food commodity costs; | |

| ● | our failure to prevent food safety and food-borne illness incidents; | |

| ● | changes in consumer tastes and nutritional and dietary trends; | |

| ● | our dependence on key executive management; | |

| ● | our inability to identify qualified individuals for our workforce; | |

| ● | our vulnerability to labor costs; | |

| ● | our inability to comply with governmental regulation; | |

| ● | violations of the U.S. Foreign Corrupt Practices Act and similar worldwide anti-bribery and anti-kickback laws; | |

| ● | our inability to maintain sufficient levels of cash flow, or access to capital, to meet growth expectations; | |

| ● | control of our Company by Fog Cutter Capital Group, Inc.; and | |

| ● | the additional risks referred to in the section entitled “Risk Factors.” |

You should not put undue reliance on any forward-looking statements. Forward-looking statements speak only as of the date they are made, and we undertake no obligation to update them in light of new information or future events except to the extent required by Federal securities laws.

| ii |

This summary highlights selected information about us, this Offering and information appearing elsewhere in this Offering Circular and in the documents incorporated by reference herein. This summary is not complete and does not contain all of the information that you should consider before investing in the securities offered by this Offering Circular. You should read this summary together with the entire Offering Circular, including our financial statements, the notes to those financial statements and the other documents that we include in and/or have incorporated by reference in this Offering Circular, before making an investment decision. See the Risk Factors section of this Offering Circular beginning on page 11 and risk factors discussed in documents that we incorporate by reference in this Offering Circular, for a discussion of the risks involved in investing in our securities.

FAT Brands Inc.

FAT Brands Inc., formed in March 2017, is a leading multi-brand restaurant franchising company that develops, markets, and acquires predominantly fast casual restaurant concepts around the world. As a franchisor, we generally do not own or operate restaurant locations, but rather generate revenue by charging franchisees initial up-front fees as well as ongoing royalties. This asset light franchisor model provides the opportunity for strong profit margins and an attractive free cash flow profile while minimizing restaurant operating company risk, such as long-term real estate commitments or capital investments. Our scalable management platform enables us to add new stores and restaurant concepts to our portfolio with minimal incremental corporate overhead cost, while taking advantage of significant corporate overhead synergies. The acquisition of additional brands and restaurant concepts as well as expansion of our existing brands are key elements of our growth strategy.

As of the date of this Offering Circular, we were the owner and franchisor of the following restaurant brands:

Fatburger. Founded in Los Angeles, California in 1947, Fatburger (The Last Great Hamburger StandTM) has, throughout its history, maintained its reputation as an iconic, all-American, Hollywood favorite hamburger restaurant serving a variety of freshly made-to-order, customizable, big, juicy, and tasty Fatburgers, Turkeyburgers, Chicken Sandwiches, Impossible™ Burgers, Veggieburgers, French fries, onion rings, soft-drinks and milkshakes. With a legacy spanning over 70 years, Fatburger’s dedication to superior quality inspires robust loyalty amongst its customer base and has long appealed to American cultural and social leaders. We have counted many celebrities and athletes as past franchisees and customers, and we believe this prestige has been a principal driver of the brand’s strong growth. Fatburger offers a premier dining experience, demonstrating the same dedication to serving gourmet, homemade, custom-built burgers as it has since 1947. As of June 30, 2019, there were 164 franchised and sub-franchised Fatburger locations across 6 states and 18 countries.

Buffalo’s Cafe. Established in Roswell, Georgia in 1985, Buffalo’s Cafe (Where Everyone is FamilyTM) is a family-themed casual dining concept known for its chicken wings and 13 distinctive homemade wing sauces, burgers, wraps, steaks, salads and other classic American cuisine. Featuring a full bar and table service, Buffalo’s Cafe offers a distinctive dining experience affording friends and family the flexibility to share an intimate dinner together or to casually watch sporting events while enjoying extensive menu offerings. Beginning in 2011, Buffalo’s Express was developed and launched within the Buffalo’s Cafe brand as a fast-casual, smaller footprint variant of Buffalo’s Café, offering a limited version of the full menu with an emphasis on chicken wings, wraps and salads. Current Buffalo’s Express outlets are co-branded with Fatburger locations, providing our franchisees with complementary concepts that share kitchen space and result in a higher average unit volume (compared to stand-alone Fatburger locations). As of June 30, 2019, there were 17 franchised Buffalo’s Cafe and 92 co-branded Fatburger / Buffalo’s Express locations globally.

Ponderosa & Bonanza Steakhouse. Ponderosa Steakhouse, founded in 1965, and Bonanza Steakhouse, founded in 1963 (collectively, “Ponderosa”), offer the quintessential American steakhouse experience, for which there is strong and growing demand in international markets, particularly in Asia and the Middle East. Ponderosa and Bonanza Steakhouses offer guests a high-quality buffet and broad array of great tasting, affordably-priced steak, chicken and seafood entrées. Buffets at Ponderosa and Bonanza Steakhouses feature a large variety of all you can eat salads, soups, appetizers, vegetables, breads, hot main courses and desserts. An additional variation of the brand, Bonanza Steak & BBQ, offers a full-service steakhouse with fresh farm-to-table salad bar and a menu showcase of USDA flame-grilled steaks and house-smoked BBQ, with contemporized interpretations of traditional American classics. As of June 30, 2019, there were 83 Ponderosa and 14 Bonanza restaurants operating under franchise and sub-franchise agreements in 16 states and 5 countries.

Hurricane Grill & Wings. Founded in Fort Pierce, Florida in 1995, Hurricane Grill & Wings is a tropical beach themed casual dining restaurant known for its fresh, jumbo, chicken wings, 35 signature sauces, burgers, bowls, tacos, salads and sides. Featuring a full bar and table service, Hurricane Grill & Wings laid-back, casual, atmosphere affords family and friends the flexibility to enjoy dining experiences together regardless of the occasion. The acquisition of Hurricane Grill & Wings has been complementary to FAT Brands existing portfolio chicken wing brands, Buffalo’s Cafe and Buffalo’s Express. As of June 30, 2019, there were 55 franchised Hurricane Grill & Wings and 3 franchised Hurricane BTWs (Hurricane’s fast-casual burgers, tacos & wings concept), across 8 states.

| 1 |

Yalla Mediterranean. Founded in 2014, Yalla Mediterranean is a Los Angeles-based restaurant chain specializing in authentic, healthful, Mediterranean cuisine with an environmentally conscience and focus on sustainability. The word “yalla” which means “let’s go” is embraced in every aspect of Yalla Mediterranean’s culture and is a key component of our concept. Yalla Mediterranean offers a healthful Mediterranean menu of wraps, plates, and bowls in a fast-casual setting, with cuisine prepared fresh daily using, GMO-free, local ingredients for a menu that includes vegetarian, vegan, gluten-free and dairy-free options accommodating customers with a wide variety of dietary needs and preferences. The brand demonstrates its commitment to the environment by using responsibly-sourced proteins and utensils, bowls and serving trays made from compostable materials. Each of Yalla’s seven locations across California also feature on-tap selections of craft beers and fine wines. We intend to sell all of the existing Yalla locations to franchisees and expand the business through additional franchising.

Elevation Burger. Established in Northern Virginia in 2002, Elevation Burger is a fast-casual burger, fries, and shakes chain that provides its customers with healthier, “elevated” food options. Serving grass-fed beef, organic chicken, and French fries cooked using a proprietary olive oil-based frying method, Elevation maintains environmentally-friendly operating practices including responsible sourcing of ingredients, robust recycling programs intended to reduce carbon footprint, and store décor constructed of eco-friendly materials. The acquisition of Elevation Burger in June 2019 aligns with our corporate mission of providing fresh, authentic and tasty products to the customers of our franchisees and complements our existing burger brand, Fatburger. As of June 30, 2019, there were 43 franchised Elevation Burger stores located in 8 states plus the District of Columbia and 4 countries.

Systemwide, across all of the Company’s brands, store level sales approximated $100 million in the second quarter of 2019.

Beyond our current brand portfolio, we intend to acquire other restaurant franchise concepts that will allow us to offer additional food categories and expand our geographic footprint. In evaluating potential acquisitions, we specifically seek concepts with the following characteristics:

| ● | established, widely-recognized brands; | |

| ● | steady cash flows; | |

| ● | track records of long-term, sustainable operating performance; | |

| ● | good relationships with franchisees; | |

| ● | sustainable operating performance; | |

| ● | geographic diversification; and | |

| ● | growth potential, both geographically and through co-branding initiatives across our portfolio. |

Leveraging our scalable management platform, we expect to achieve cost synergies post-acquisition by reducing the corporate overhead of the acquired company – most notably in the legal, accounting and finance functions. We also plan to grow the top line revenues of newly acquired brands through support from our management and systems platform, including public relations, marketing and advertising, supply chain assistance, site selection analysis, staff training and operational oversight and support.

Our franchisee base consisted of 194 franchisees as of June 30, 2019. Of these franchisees, 157 operate in North America and 46 own multiple restaurant locations. Our franchisees operated a total of 381 restaurants as of June 30, 2019, 295 of which were located in North America. As of June 30, 2019, we had commitments for development of over 200 new stores which remain to be completed.

The FAT Brands Difference – Fresh. Authentic. Tasty.

Our name represents the values that we embrace as a company and the food that we provide to customers – Fresh. Authentic. Tasty (which we refer to as “FAT”). The success of our franchisor model is tied to consistent delivery by our restaurant operators of freshly prepared, made-to-order food that our customers desire. With the input of our customers and franchisees, we continually strive to keep a fresh perspective on our brands by enhancing our existing menu offerings and introducing appealing new menu items. When enhancing our offerings, we ensure that any changes are consistent with the core identity and attributes of our brands, although we do not intend to adapt our brands to be all things to all people. In conjunction with our restaurant operators (which means the individuals who manage and/or own our franchised restaurants), we are committed to delivering authentic, consistent brand experiences that have strong brand identity with customers. Ultimately, we understand that we are only as good as the last meal served, and we are dedicated to having our franchisees consistently deliver tasty, high-quality food and positive guest experiences in their restaurants.

In pursuing acquisitions and entering new restaurant brands, we are committed to instilling our FAT Brands values into new restaurant concepts. As our restaurant portfolio continues to grow, we believe that both our franchisees and diners will recognize and value this ongoing commitment as they enjoy a wider concept offering.

| 2 |

Competitive Strengths

We believe that our competitive strengths include:

| ● | Management Platform Built for Growth. We have developed a robust and comprehensive management and systems platform designed to support the expansion of our existing brands while enabling the accretive and efficient acquisition and integration of additional restaurant concepts. We dedicate our considerable resources and industry knowledge to promote the success of our franchisees, offering them multiple support services such as public relations, marketing and advertising, supply chain assistance, site selection analysis, staff training and operational oversight and support. Furthermore, our platform is scalable and adaptable, allowing us to incorporate new concepts into the FAT Brands family with minimal incremental corporate costs. We intend to grow our existing brands as well as make strategic and opportunistic acquisitions that complement our existing portfolio of concepts providing an entrance into targeted restaurant segments. We believe that our platform is a key differentiator in pursuing this strategy. | |

| ● | Asset Light Business Model Driving High Free Cash Flow Conversion. We maintain an asset light business model requiring minimal capital expenditures by franchising our restaurant concepts to our owner/operators. The multi-brand franchisor model also enables us to efficiently scale the number of restaurant locations with very limited incremental corporate overhead and minimal exposure to store-level risk, such as long-term real estate commitments and increases in employee wage costs. Our multi-brand approach also gives us the organizational depth to provide a host of services to our franchisees, which we believe enhances their financial and operational performance. As a result, new store growth and accelerating financial performance of the FAT Brands network drive increases in our initial up-front fee and royalty revenue streams while expanding profit and free cash flow margins. | |

| ● | Strong Brands Aligned with FAT Brands Vision. We have an enviable track record of delivering Fresh, Authentic, and Tasty meals across our franchise system. Our Fatburger and Buffalo’s concepts have built distinctive brand identities within their respective segments, providing made-to-order, high-quality food at competitive prices. The Ponderosa and Bonanza brands deliver an authentic American steakhouse experience with which customers identify. Hurricane Grill & Wings offer customers fresh, jumbo chicken wings with an assortment of sauces and rubs in a casual dining atmosphere, while Yalla Mediterranean offers a healthful Mediterranean menu of wraps, plates, and bowls in a fast-casual setting. By maintaining alignment with the FAT Brands vision across an expanding platform, we believe that our concepts will appeal to a broad base of domestic and global consumers. | |

| ● | Experienced and Diverse Global Franchisee Network. We have new restaurant commitments of over 200 locations across our brands. We anticipate that our current franchisees will open more than 30 new restaurants annually for at least the next five years. The acquisition of additional restaurant franchisors will also increase the number of restaurants operated by our existing franchisee network. Additionally, our franchise development team has built an attractive pipeline of new potential franchisees, with many experienced restaurant operators and new entrepreneurs eager to join the FAT Brands family. | |

| ● | Ability to Cross-Sell Existing Franchisees Concepts from the FAT Brands Portfolio. Our ability to easily, and efficiently, cross-sell our existing franchisees new brands from our FAT Brands portfolio affords us the ability to grow more quickly and satisfy our existing franchisees’ demands to expand their organizations. By having the ability to offer our franchisees a variety of concepts (i.e., a fast-casual better-burger concept, a fast-casual chicken wing concept, a casual dining concept, a healthful Mediterranean menu concept and steakhouse concepts) from the FAT Brands portfolio, our existing franchisees are able to acquire the rights to, and develop, their respective markets with a well-rounded portfolio of FAT Brands concept offerings affording them the ability to strategically satisfy their respective market demands by developing our various concepts where opportunities are available. | |

| ● | Seasoned and Passionate Management Team. Our management team and employees are critical to our success. Our senior leadership team has more than 200 years of combined experience in the restaurant industry, and many have been a part of our team since the acquisition of the Fatburger brand in 2003. We believe that our management team has the track record and vision to leverage the FAT Brands platform to achieve significant future growth. In addition, through their holdings in Fog Cutter Capital Group, Inc., or “FCCG”), our senior executives own a significant equity interest in the company, ensuring long-term commitment and alignment with our public shareholders. Our management team is complemented by an accomplished Board of Directors. |

| 3 |

Growth Strategy

The principal elements of our growth strategy include:

| ● | Opportunistically Acquire New Brands. Our management platform was developed to cost-effectively and seamlessly scale with new restaurant concept acquisitions. Our recent acquisitions of the Hurricane Grill & Wings, Yalla Mediterranean and Elevation Burger brands are a continuation of this growth strategy. We have identified food categories that appeal to a broad international base of customers, targeting the burgers, chicken, pizza, steak, coffee, sandwich and dessert segments for future growth. We have developed a strong and actionable pipeline of potential acquisition opportunities to achieve our objectives. We seek concepts with established, widely-recognized brands; steady cash flows; track records of long-term, good relationships with franchisees; sustainable operating performance; geographic diversification; and growth potential, both geographically and through co-branding initiatives across our portfolio. We approach acquisitions from a value perspective, targeting modest multiples of franchise-level cash flow valuations to ensure that acquisitions are immediately accretive to our earnings prior to anticipated synergies. | |

| ● | Optimize Capital Structure to Enable Profitable Growth through Acquisitions. While we believe our existing business can be funded through cash generated from current operations, we intend to finance future acquisitions of restaurant brands through the issuance of debt and equity financing placed with investors and issued directly to sellers of restaurant brands. We are actively pursuing various financing alternatives, with the goal of reducing and optimizing our all-in cost of capital and providing us with the means to pursue larger and more profitable acquisitions. | |

| ● | Accelerate Same-Store Sales Growth. Same-store sales growth reflects the change in year-over-year of sales for the comparable store base, which we define as the number of stores open for at least one full fiscal year. To optimize restaurant performance, we have embraced a multi-faceted same-store sales growth strategy. We utilize customer feedback and closely analyze sales data to introduce, test and perfect existing and new menu items. In addition, we regularly utilize public relations and experiential marketing, which we leverage via social media and targeted digital advertising to expand the reach of our brands and to drive traffic to our stores. Furthermore, we have embraced emerging technology to develop our own brand-specific mobile applications, allowing guests to find restaurants, order online, earn rewards and join our e-marketing providers. We have also partnered with third-party delivery service providers, including UberEATS, Grub Hub, Amazon Restaurants and Postmates, which provide online and app-based delivery services and constitute a new sales channel for our existing locations. Finally, many of our franchisees are pursuing a robust capital expenditure program to remodel legacy restaurants and to opportunistically co-brand them with our Buffalo’s Express and / or Fat Bar concepts (serving beer, wine, spirits and cocktails). | |

| ● | Drive Store Growth through Co-Branding, Virtual Restaurants, and Cloud Kitchens. We franchise co-branded Fatburger / Buffalo’s Express locations, giving franchisees the flexibility of offering multiple concepts, while sharing kitchen space, resulting in a higher average check (compared to stand-alone Fatburger locations). Franchisees benefit by serving a broader customer base, and we estimate that co-branding results in a 20%-30% increase in average unit volume compared to stand-alone locations with minimal incremental cost to franchisees. Our acquisition strategy reinforces the importance of co-branding, as we expect to offer each of the complementary brands that we acquire to our existing franchisees on a co-branded basis. | |

| In addition to driving growth through co-branding opportunities, we are leveraging the current industry trend of virtual restaurants, whereby one (or more) of our brands serves its food out of the kitchen of another brand for online delivery only, and cloud kitchens, whereby restaurants open without a customer-facing store-front solely for the purpose of servicing delivery or virtual kitchens. Virtual restaurants and cloud kitchens allow us to introduce our brands in geographic areas where previously unknown such as introducing selected menu items from Hurricane Grill & Wings to the southern California market through the preparation in and delivery from Fatburger franchised restaurants via a program with UberEats. | ||

| ● | Extend Brands into New Segments. We have a strong track record of extending our brands into new segments, and we believe that we have a significant opportunity to capture new markets by strategically adapting our concepts while reinforcing the brand identity. In addition to dramatically expanding the traditional Buffalo’s Cafe customer base through Fatburger / Buffalo’s Express co-branding, we have also begun evaluating opportunities to leverage the Buffalo’s brand by promoting Buffalo’s Express on a stand-alone basis. Furthermore, we have also begun the roll-out of Fat Bars (serving beer, wine, spirits and cocktails), which we are opportunistically introducing to select existing Fatburger locations on a modular basis. Similarly, we plan to create smaller-scale, fast casual Ponderosa and Bonanza concepts, to drive new store growth, particularly internationally. |

| 4 |

| ● | Continue Expanding FAT Brands Internationally. We have a significant global presence, with international franchised stores in Canada, China, Qatar, Taiwan, Iraq, the United Kingdom, Indonesia, Tunisia, Singapore, Philippines, Panama, the United Arab Emirates, Kuwait, Saudi Arabia, Malaysia, Japan, Pakistan, and Egypt. We believe that the appeal of our Fresh, Authentic, and Tasty concepts is global, and we are targeting further penetration of Middle Eastern and Asian markets, particularly through leveraging the Buffalo’s, Ponderosa and Hurricane brands. | |

| ● | Enhance Footprint in Existing Markets through Current Franchisee Networks. We had 194 franchisees who collectively operated more than 380 restaurants as of June 30, 2019. As noted, our existing and new franchisees have made new store commitments of over 200 locations across our brands, and we anticipate that our new and existing franchisees will open more than 30 new stores annually for at least the next four years. Beyond these existing commitments, we have found that many of our franchisees have grown their businesses over time, increasing the number of stores operated in their organizations and expanding their concept offerings across the FAT Brands portfolio of concepts. | |

| ● | Attract New Franchisees in Existing and Unpenetrated Markets. In addition to the large pipeline of new store commitments from current franchisees, we believe the existing markets for Fatburger, Elevation Burger, Buffalo’s Cafe, Buffalo’s Express, Ponderosa, Bonanza, Hurricane, and Yalla locations are far from saturated and can support a significant increase in units. Furthermore, new franchisee relationships represent the optimal way for our brands to penetrate geographic markets where we do not currently operate. In many cases, prospective franchisees have experience in and knowledge of markets where we are not currently active, facilitating a smoother brand introduction than we or our existing franchisees could achieve independently. We generate franchisee leads through various channels, including franchisee referrals, traditional and non-traditional franchise brokers and broker networks, franchise development advertising, and franchise trade shows and conventions. |

Summary Risk Factors

We are subject to a number of risks, including risks that may prevent us from achieving our business objectives or that may adversely affect our business, financial condition, results of operations, cash flows and prospects. You should carefully consider the risks discussed in the section entitled “Risk Factors,” including the following risks, before investing in our Series B Preferred Stock:

| ● | Our operating results and growth strategies are closely tied to the success and cooperation of our franchisees, and we have experienced volatility in unit economics of our franchisees in recent years. | |

| ● | Our franchisees could take actions that could harm our business, and may not accurately report sales which drives our royalties. | |

| ● | We may not open new domestic and international franchisee-owned restaurants on a timely basis. | |

| ● | We may not successfully identify, recruit and contract with a sufficient number of qualified franchisees. | |

| ● | We may not achieve our target development goals, aggressive development could cannibalize existing sales and new restaurants and acquisitions of new brands may not be successful or profitable. | |

| ● | Food safety and foodborne illness concerns may have an adverse effect on our business. | |

| ● | Our business may be adversely impacted by changes in consumer discretionary spending and general economic conditions in our franchisee markets. | |

| ● | Our international operations subject us to operating and geographic risks and foreign currency risks that could negatively affect our business and financial results. | |

| ● | We depend on key executive management. | |

| ● | We expect that FCCG will remain a significant stockholder, whose interests may differ from those of our public stockholders. | |

| ● | Given our market capitalization, there is limited trading liquidity in our Common Stock. | |

| ● | We are a “controlled company” within the meaning of the NASDAQ listing standards and, as a result, will qualify for exemptions from certain corporate governance requirements. You may not have the same protections afforded to stockholders of companies that are subject to such requirements. |

| 5 |

| ● | We may issue additional shares of preferred stock in the future, which could make it difficult for another company to acquire us or could otherwise adversely affect holders of our Common Stock and the Series B Preferred Stock. | |

| ● | Our ability to pay regular dividends to our stockholders is subject to the discretion of our Board of Directors and may be limited by our holding company structure and applicable provisions of Delaware law. |

Our Corporate Information

FAT Brands Inc., the issuer of the Series B Preferred Stock in this Offering, was incorporated as a Delaware corporation on March 21, 2017. Our corporate headquarters are located at 9720 Wilshire Blvd., Suite 500, Beverly Hills, California 90212. Our main telephone number is (310) 319-1850. Our principal Internet website address is www.fatbrands.com. The information on our website is not incorporated by reference into, or a part of, this Offering Circular.

Implications of Being an Emerging Growth Company

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other requirements that are otherwise applicable generally to public companies. These provisions include the following:

| ● | we are required to have only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations disclosure; | |

| ● | we are not required to engage an auditor to report on our internal controls over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002 (which we refer to as the “Sarbanes-Oxley Act”); | |

| ● | we are not required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board (which we refer to as the “PCAOB”) regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements (i.e., an auditor discussion and analysis); | |

| ● | we are not required to submit certain executive compensation matters to stockholder advisory votes, such as “say-on-pay,” “say-on-frequency” and “say-on-golden parachutes;” and | |

| ● | we are not required to disclose certain executive compensation related items such as the correlation between executive compensation and performance and comparisons of the chief executive officer’s compensation to median employee compensation. |

We may take advantage of these provisions until the last day of our fiscal year following the fifth anniversary of the consummation of our initial public offering or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company if we have more than $1.07 billion in annual revenue, have more than $700 million in market value of our Common Stock held by non-affiliates, or issue more than $1.0 billion of non-convertible debt over a three-year period (as such amounts may be adjusted from time-to-time). We may choose to take advantage of some but not all of these reduced burdens. We have elected to adopt the reduced disclosure with respect to financial statements and the related Management’s Discussion and Analysis of Financial Condition and Results of Operations disclosure. As a result of this election, the information that we provide stockholders may be different than you might get from other public companies in which you hold equity.

The JOBS Act permits an emerging growth company like us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We are choosing to “opt out” of this provision and, as a result, we will comply with new or revised accounting standards as required when they are adopted. This decision to opt out of the extended transition period is irrevocable.

| 6 |

The following is a brief summary of certain terms of this offering. For a more complete description of the terms of the Series B Preferred Stock and Warrants, see “Description of the Securities We Are Offering–Series B Cumulative Preferred Stock” and “Description of the Securities We Are Offering–Warrants” in this Offering Circular.

| Issuer | FAT Brands Inc. | |

| Securities Offered | We are offering up to 1,200,000 shares of 8.25% Series B Cumulative Preferred Stock, and Warrants initially exercisable to purchase up to an aggregate of 720,000 shares of Common Stock at an exercise price of $8.50 per share.

Each share of Series B Preferred Stock that we sell in this Offering will be accompanied by a Warrant to purchase 0.60 shares of Common Stock at an exercise price of $8.50 per share of Common Stock. | |

| Price | Each share of Series B Preferred Stock and accompanying Warrant is being offered at a price of $25.00. | |

| Warrants | We are offering Warrants to purchase up to an aggregate of 720,000 shares of common stock that will be exercisable for five years from the date of initial issuance ( , 2019) at an exercise price of $8.50 per share, subject to adjustment. This Offering Circular also relates to the offering of the shares of Common Stock issuable upon exercise of the Warrants. There is presently no public market for the Warrants and it is not anticipated that a public market for the Warrants will develop in the future.

| |

| The Warrants will be governed by the laws of the State of New York, and any disputes against the Company arising from the Warrants must be brought and enforced in the State and Federal courts in the State of New York. However, we do not intend that the foregoing provisions would apply to actions arising under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended | ||

| Liquidation preference of Series B Preferred Stock | If we liquidate, dissolve or wind up, holders of the Series B Preferred Stock will have the right to receive $25.00 per share, plus all accumulated, accrued and unpaid dividends (whether or not earned or declared) to and including the date of payment, before any payments are made to the holders of our Common Stock or to the holders of equity securities the terms of which provide that such equity securities will rank junior to the Series B Preferred Stock. The rights of holders of Series B Preferred Stock to receive their liquidation preference also will be subject to the proportionate rights of our Series A Fixed Rate Cumulative Preferred Stock and any other class or series of our capital stock ranking in parity with the Series B Preferred Stock as to liquidation. | |

Dividends on Series B Preferred Stock |

Holders of the Series B Preferred Stock will be entitled to receive, when, as and if declared by our Board of Directors, cumulative cash dividends payable quarterly in an amount per share of Series B Preferred Stock equal to $2.0625 per share each year, which is equivalent to 8.25% of the $25.00 liquidation preference per share. Dividends on the Series B Preferred Stock will be payable quarterly in arrears based on the Company’s fiscal quarters, beginning with the fiscal quarter ended September 29, 2019. To the extent declared by our Board of Directors, dividends will be payable not later than twenty (20) days after the end of each quarter. Dividends on the Series B Preferred Stock will accumulate whether or not we have earnings, whether or not there are funds legally available for the payment of such dividends and whether or not such dividends are declared by our Board of Directors. Dividends on the Series B Preferred Stock will increase to $2.50 per share each year, which is equivalent to 10% of the $25.00 liquidation preference per share, to the extent the Company fails to make a cash dividend payment of four or more consecutive or non-consecutive quarterly dividends. | |

| Maturity of Series B Preferred Stock | The Series B Preferred Stock will mature on the five-year anniversary of the initial issuance date ( , 2024) or the earlier liquidation, dissolution or winding-up of the Company. Upon maturity, the holders of Series B Preferred Stock will be entitled to receive cash redemption of their shares in an amount equal to $25.00 per share plus any accrued and unpaid dividends. | |

Call Feature of Series B Preferred Stock |

We may not redeem the Series B Preferred Stock before the first anniversary of the initial issuance date, or , 2020. After the first anniversary of the initial issuance date we may, at our option, redeem the Series B Preferred Stock, in whole or in part, by paying $25.00 per share, plus any accrued and unpaid dividends to the date of redemption and a redemption premium equal to 10% of liquidation preference prior to the second anniversary ( , 2021) or 5% of liquidation preference after the second anniversary and prior to the third anniversary ( , 2022). | |

| Early redemption by holder | Holders of Series B Preferred Stock may optionally cause the Company to redeem all or any portion of their Series B Preferred Stock following the first anniversary of the initial issuance date, or , 2021, for an amount equal to $25.00 per share, plus any accrued and unpaid dividends, minus an early redemption fee equal to 12% of liquidation preference prior to the second anniversary ( , 2021), 10% of liquidation preference after the second anniversary and prior to the third anniversary ( , 2022), or 8% of liquidation preference after the third anniversary and prior to the fourth anniversary ( , 2023). There will be no redemption premium charged after the fourth anniversary of the initial issuance date. |

| 7 |

| Information rights | During any period in which we are not subject to the reporting requirements of Section 13 or 15(d) of the Exchange Act and any shares of our Series B Preferred Stock are outstanding, we will (i) transmit by mail to all holders of the Series B Preferred Stock, copies of the annual reports and quarterly reports that we would have been required to file with the SEC pursuant to Section 13 or 15(d) of the Exchange Act if we were subject to those sections (other than any exhibits that would have been required) and (ii) promptly upon written request, make available copies of such reports to any prospective holder of Series B Preferred Stock. We will mail the reports to the holders of Series B Preferred Stock within 15 days after the respective dates by which we would have been required to file the reports with the SEC if we were subject to Section 13 or 15(d) of the Exchange Act. | |

| Form | The Series B Preferred Stock and Warrants will be maintained in book-entry form registered in the name of the nominee of The Depository Trust Company, except under limited circumstances where certificated shares may be issued. | |

| Ranking | The Series B Preferred Stock, with respect to dividend rights and rights upon our voluntary or involuntary liquidation, dissolution or winding up, will rank: |

| ● | senior to our Common Stock, our Series A-1 Preferred Stock, and any other class of equity securities the terms of which provide that such equity securities will rank junior to the Series B Preferred Stock; | |

| ● | on a parity (pari passu) with our Series A Preferred Stock, and any other equity securities the terms of which provide that such equity securities will rank without preference or priority over the other; and | |

| ● | junior to any equity securities the terms of which provide that such equity securities will rank senior to the Series B Preferred Stock, and to all of our existing and future debt, including, prior to conversion of such debt, any debt convertible into our equity securities. |

| Voting rights | The Series B Preferred Stock will not vote with the Common Stock, but will have voting rights as required by law and majority consent rights to (i) merger, consolidation or share exchange that materially and adversely affects the rights, preferences or privileges of the Series B Preferred Stock, unless full redemption price is paid in cash; (ii) amending the certificate of incorporation to materially and adversely affect the Series B Preferred Stock; and (iii) declaring or paying any junior dividends or repurchasing any junior securities during any time that all dividends on the Series B Preferred Stock have not been paid in full in cash. | |

| Absence of a trading market | The Series B Preferred Stock and Warrants are new issues of securities with no established trading market. Accordingly, we cannot provide any assurance as to the development or liquidity of any market for the Series B Preferred Stock or Warrants. | |

| Listing | We do not intend to apply for listing of the Series B Preferred Stock or Warrants on any securities exchange, and we do not expect that the Series B Preferred Stock or the Warrants will be quoted on NASDAQ. | |

| Use of proceeds | We intend to use the net proceeds for general corporate purposes and possible future acquisitions and growth opportunities. See “Use of Proceeds.” | |

| Settlement date | We expect that the shares of Series B Preferred Stock and Warrants to be issued in this Offering will initially be ready for delivery to purchasers on or about , 2019 and thereafter at each closing, on a rolling basis, until the Termination Date. | |

| Risk factors | Investing in our Series B Preferred Stock and Warrants involves a number of risks. See “Risk Factors” beginning on page 11 of this Offering Circular and in our Annual Report on Form 10-K for the year ended December 30, 2018 for information about important risks you should consider before making an investment decision regarding the Series B Preferred Stock. | |

| Selling Agents | TriPoint Global Equities, LLC and Digital Offering, LLC have agreed to act as our exclusive, lead managing selling agents (which we refer to as the “Selling Agents”) to offer the Series B Preferred Stock and Warrants to prospective investors on a “best efforts” basis. In addition, the Selling Agents may engage one or more sub-Selling Agents or selected dealers. The Selling Agents are not purchasing the Series B Preferred Stock or Warrants offered by us, and is not required to sell any specific number or dollar amount of the Series B Preferred Stock and Warrants in the Offering. |

| 8 |

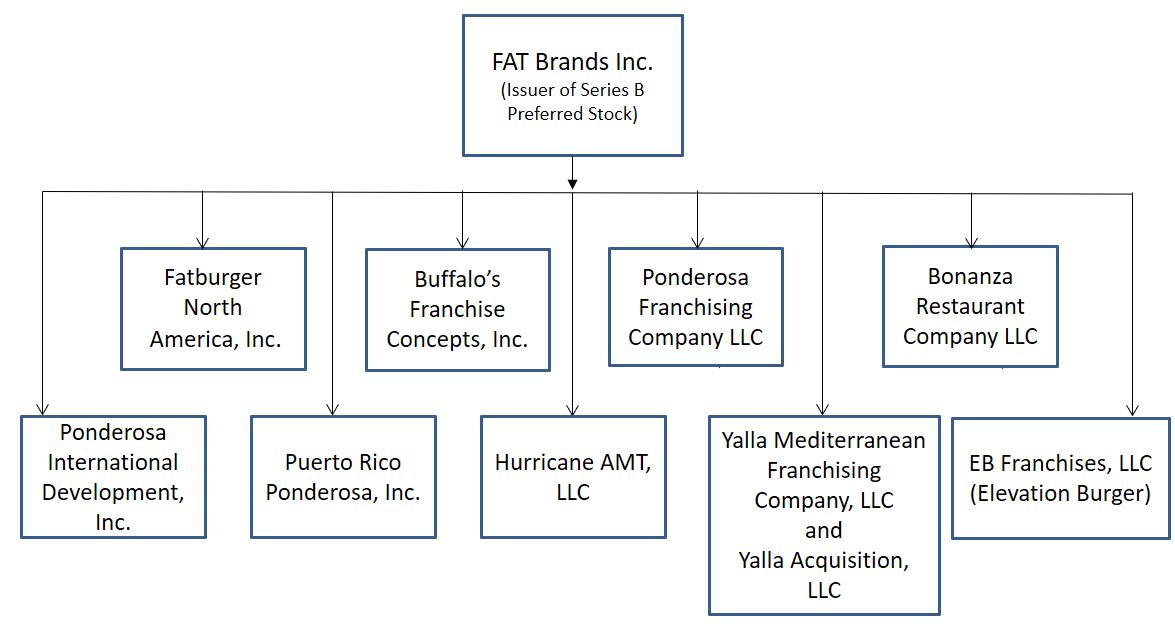

Existing Structure

The following diagram shows our organizational structure at the time of this Offering Circular:

| 9 |

SUMMARY HISTORICAL AND PRO FORMA CONSOLIDATED FINANCIAL AND OTHER DATA

The following tables summarize the consolidated historical financial data for FAT Brands Inc.

The summary statements of operations data for each of the twenty-six weeks ended June 30, 2019 and July 1, 2018 are derived from the unaudited financial statements of FAT Brands Inc. filed on the Company’s Form 10-Q with the SEC on August 14, 2019. The summary statement of operations data for each of the years in the two-year period ended December 30, 2018 and December 31, 2017 are derived from the audited financial statements of FAT Brands Inc. filed on the Company’s Form 10-K with the SEC on March 29, 2019. We completed our initial public offering on October 20, 2017, and the statement of operations data for 2017 represents the period from our inception (March 21, 2017) through December 31, 2017.

The results of operations for the periods presented below are not necessarily indicative of the results to be expected for any future periods and the results for any interim period are not necessarily indicative of the results that may be expected for a full fiscal year. The information set forth below should be read together with the “Selected Historical Financial and Other Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the financial statements and the accompanying notes appearing elsewhere in this Offering Circular.

In thousands, except net income (loss) per share data

| 26 weeks ended | Fiscal Year ended | |||||||||||||||

| June 30, 2019 | July 1, 2018 | December 30, 2018 | December 31, 2017 | |||||||||||||

| (unaudited) | (unaudited) | (audited) | (audited) | |||||||||||||

| Statements of operations data: | ||||||||||||||||

| Revenues | ||||||||||||||||

| Royalties | $ | 7,127 | $ | 5,432 | $ | 12,097 | $ | 2,023 | ||||||||

| Franchise fees | 1,306 | 698 | 2,136 | 140 | ||||||||||||

| Store opening fees | 289 | 105 | 352 | - | ||||||||||||

| Advertising fees | 2,008 | 1,226 | 3,182 | - | ||||||||||||

| Management fees and other revenue | 38 | 32 | 600 | 10 | ||||||||||||

| Total revenues | 10,768 | 7,493 | 18,367 | 2,173 | ||||||||||||

| Costs and expenses | ||||||||||||||||

| General and administrative | 5,542 | 4,499 | 10,949 | 2,123 | ||||||||||||

| Advertising expenses | 2,008 | 1,226 | 3,182 | - | ||||||||||||

| Refranchising restaurant costs and expense, net of revenue | 1,021 | - | - | - | ||||||||||||

| Costs and expenses | 8,571 | 5,725 | 14,131 | 2,123 | ||||||||||||

| Income from operations | 2,197 | 1,768 | 4,236 | 50 | ||||||||||||

| Other expense, net | (2,790 | ) | (590 | ) | (6,309 | ) | (256 | ) | ||||||||

| Income (loss) before income tax expense | (593 | ) | 1,178 | (2,073 | ) | (206 | ) | |||||||||

| Income tax expense (benefit) | 625 | 296 | (275 | ) | 407 | |||||||||||

| Net income (loss) | $ | (1,218 | ) | $ | 882 | $ | (1,798 | ) | $ | (613 | ) | |||||

| EBITDA (1) | $ | 3,067 | $ | 1,765 | $ | 3,055 | $ | 22 | ||||||||

| Adjusted EBITDA (2) | $ | 3,598 | $ | 2,010 | $ | 4,902 | $ | 111 | ||||||||

| Basic (loss) income per common share | $ | (0.10 | ) | $ | 0.09 | $ | (0.16 | ) | $ | (0.07 | ) | |||||

| Basic weighted average shares outstanding | 11,726 | 10,304 | 10,971 | 8,686 | ||||||||||||

| Diluted (loss) income per common share | $ | (0.10 | ) | $ | 0.09 | $ | (0.16 | ) | $ | (0.07 | ) | |||||

| Diluted weighted average shares outstanding | 11,726 | 10,304 | 10,971 | 8,686 | ||||||||||||

| (1) | EBITDA is defined as earnings before interest, taxes, depreciation and amortization. We use the term EBITDA, as opposed to income from operations, as it is widely used by analysts, investors and other interested parties to evaluate companies in our industry. We believe that EBITDA is an appropriate measure of operating performance because it eliminates the impact of expenses that do not relate to business performance. EBITDA is not a measure of our financial performance or liquidity that is determined in accordance with generally accepted accounting principles (“GAAP”), and should not be considered as an alternative to net income (loss) as a measure of financial performance or cash flows from operations as measures of liquidity, or any other performance measure derived in accordance with GAAP. | |

| (2) | Adjusted EBITDA is defined as EBITDA (as defined above), excluding expenses related to acquisitions, refranchising restaurant costs and expenses, net of revenue, and certain non-recurring or non-cash items that the Company does not believe directly reflect its core operations and may not be indicative of the Company’s recurring business operations. |

A reconciliation of net income to EBITDA is set forth below:

| 26 weeks ended | Fiscal Year ended | |||||||||||||||

| June 30, 2019 | July 1, 2018 | December 30, 2018 | December 31, 2017 | |||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||

| Net income (loss) | $ | (1,218 | ) | $ | 882 | $ | (1,798 | ) | $ | (613 | ) | |||||

| Depreciation expense | 278 | 73 | 358 | 23 | ||||||||||||

| Interest expense, net | 3,382 | 514 | 4,770 | 205 | ||||||||||||

| Income tax expense (benefit) | 625 | 296 | (275 | ) | 407 | |||||||||||

| EBITDA | $ | 3,067 | $ | 1,765 | $ | 3,055 | $ | 22 | ||||||||

| Share-based compensation expenses | 159 | 245 | 439 | 89 | ||||||||||||

| Non-cash lease expenses | 124 | - | - | - | ||||||||||||

| Acquisition costs and non-recurring legal costs | 197 | - | 1,408 | - | ||||||||||||

| Refranchising restaurant costs and expenses, net of revenue | 1,021 | - | - | - | ||||||||||||

| Gain on sale of refranchised restaurants | (970 | ) | - | - | - | |||||||||||

| Adjusted EBITDA | $ | 3,598 | $ | 2,010 | $ | 4,902 | $ | 111 | ||||||||

| 10 |

An investment in the Series B Preferred Stock is subject to various risks that may adversely affect the value of the Series B Preferred Stock. Before making an investment decision, you should carefully consider the risks described below together with the risks described in our Annual Report on Form 10-K for the year ended December 30, 2018, in particular under the caption “Risk Factors”, and in other documents that we subsequently file with the SEC, all of which are incorporated by reference into this Offering Circular. Additional risks and uncertainties not presently known to us or that we currently deem insignificant or remote also may adversely affect our business, financial condition and results of operations, perhaps materially.

Risks Related to the Series B Preferred Stock and this Offering

We may not be able to generate sufficient cash to service our obligations, including our obligations under the Series B Preferred Stock.

Our ability to make dividend payments on our outstanding shares of preferred stock, including the Series B Preferred Stock, and outstanding indebtedness will depend on our financial and operating performance, which is subject to prevailing economic and competitive conditions and to certain financial, business and other factors beyond our control. We may be unable to maintain a level of cash flows from operating activities sufficient to permit us to pay the liquidation preference, premium, if any, and dividends on our preferred stock, including the Series B Preferred Stock, as well as principal and interest on our outstanding indebtedness, including our senior secured credit facility.

We may need to refinance our redeemable preferred stock prior to the maturity of the Series B Preferred Stock.

Upon the five-year anniversary of the initial issuance date of our Series A Preferred Stock (June 8, 2023), the holders of Series A Preferred Stock will be entitled to cash redemption of their shares in an amount equal to $25.00 per share, or an aggregate of $10,000,000, plus any accrued and unpaid dividends. In addition, upon the five-year anniversary of the initial issuance date (July 3, 2023) of our Series A-1 Preferred Stock, the holders of Series A-1 Preferred Stock will be entitled to cash redemption of their shares in an amount equal to $25.00 per share, or an aggregate of $4,500,000, plus any accrued and unpaid dividends. Although we expect to refinance or otherwise repay the holders of Series B Preferred Stock, we may not be able to refinance this amount on commercially reasonable terms or at all. The financial terms or covenants of any new credit facility, preferred stock or other indebtedness may not be as favorable as those under our existing Series A Preferred Stock and Series A-1 Preferred Stock. Our ability to complete a refinancing of our preferred stock will depend on our financial and operating performance, as well as a number of conditions beyond our control. For example, if disruptions in the financial markets were to exist at the time that we intended to refinance these amounts, we might be restricted in our ability to access the financial markets. If we are unable to refinance our preferred stock, our alternatives would include negotiating an extension of the maturities of our preferred stock with investors and seeking or raising new equity capital. If we were unsuccessful, the lenders under our senior secured credit facility and the holders of our existing Preferred Stock could demand repayment of the amounts owed to them on the relevant maturity date. As a result, our ability to pay the principal of and interest on the Series B Preferred Stock would be adversely affected.

We may incur additional indebtedness and obligations to pay cumulative dividends on preferred stock.

We and our subsidiaries may incur additional indebtedness and obligations to pay cumulative dividends on preferred stock in the future. The terms of the Series B Preferred Stock do not prohibit us or our subsidiaries from incurring additional indebtedness or issuing additional shares of preferred with cumulative dividends. Also, our subsidiaries could incur additional indebtedness that is structurally senior to the Series B Preferred Stock or we and our subsidiaries could incur indebtedness secured by a lien on assets that do not constitute collateral, including assets of ours and our subsidiaries, and the holders of such indebtedness will have the right to be paid first from the proceeds of such assets. If we issue any additional preferred stock that ranks equally with the Series B Preferred Stock, the holders of those shares will be entitled to share ratably with the holders of the Series B Preferred Stock in any proceeds distributed in connection with our insolvency, liquidation, reorganization or dissolution. This may have the effect of reducing the amount of proceeds paid to the holders of Series B Preferred Stock. If new indebtedness is added to our current debt levels, the related risks that we and our subsidiaries now face could materially increase.

Our ability to meet our obligations under the Series B Preferred Stock depends on the earnings and cash flows of our subsidiaries and the ability of our subsidiaries to pay dividends or advance or repay funds to us.

We conduct all of our business operations through our subsidiaries. In servicing dividend payments to be made on the Series B Preferred Stock, we will rely on cash flows from these subsidiaries, mainly dividend payments and other distributions. The ability of these subsidiaries to make dividend payments to us will be affected by, among other factors, the obligations of these entities to their creditors, requirements of corporate and other law, and restrictions contained in agreements entered into by or relating to these entities.

| 11 |

We may not be able to redeem the Series B Preferred Stock upon an early redemption request.

The holders of Series B Preferred Stock will be entitled to early redemption following the first anniversary of the initial issuance date, or , 2021, subject to an early redemption fee. We may not have sufficient funds available to redeem all of the Series B Preferred Stock tendered pursuant to any such early redemption.

The Series B Preferred Stock are a new issue and do not have an established trading market, which may, among several other factors, negatively affect their liquidity or market value.

The Series B Preferred Stock are a new issue of securities and there is no established trading market for the Series B Preferred Stock. We do not intend to apply for listing of the Series B Preferred Stock on NASDAQ, we cannot make any assurances as to the development or sustainability of an active trading market, the liquidity of any trading market that may develop, the ability of holders to sell their Preferred Stock in a timely manner or at all, or the price at which the holders might be able to sell their Preferred Stock.

If a trading market does develop for the Series B Preferred Stock, the future trading price of the Series B Preferred Stock will depend on many factors, including:

| ● | prevailing dividend rates being paid by other companies similar to us; | |

| ● | the market for preferred shares similar to the Series B Preferred Stock; | |

| ● | the total amount owed by us under our outstanding indebtedness and preferred stock, which could be affected by our future incurrence of additional debt or issuances of preferred stock; | |

| ● | our financial condition, results of operations and prospects; | |

| ● | general economic conditions in our markets; and | |

| ● | the overall condition of the financial markets, many of which have experienced substantial turbulence from time to time over the last several years. |

Risks Related to Our Business and Industry

Our operating and financial results and growth strategies are closely tied to the success of our franchisees.

Our restaurants are operated by our franchisees, which makes us dependent on the financial success and cooperation of our franchisees. We have limited control over how our franchisees’ businesses are run, and the inability of franchisees to operate successfully could adversely affect our operating and financial results through decreased royalty payments. If our franchisees incur too much debt, if their operating expenses or commodity prices increase or if economic or sales trends deteriorate such that they are unable to operate profitably or repay existing debt, it could result in their financial distress, including insolvency or bankruptcy. If a significant franchisee or a significant number of our franchisees become financially distressed, our operating and financial results could be impacted through reduced or delayed royalty payments. Our success also depends on the willingness and ability of our franchisees to implement major initiatives, which may include financial investment. Our franchisees may be unable to successfully implement strategies that we believe are necessary for their further growth, which in turn may harm the growth prospects and financial condition of the company. Additionally, the failure of our franchisees to focus on the fundamentals of restaurant operations, such as quality service and cleanliness (even if such failures do not rise to the level of breaching the related franchise documents), could have a negative impact on our business.

Our franchisees could take actions that could harm our business and may not accurately report sales.

Our franchisees are contractually obligated to operate their restaurants in accordance with the operations, safety, and health standards set forth in our agreements with them and applicable laws. However, although we will attempt to properly train and support all our franchisees, they are independent third parties whom we do not control. The franchisees own, operate, and oversee the daily operations of their restaurants, and their employees are not our employees. Accordingly, their actions are outside of our control. Although we have developed criteria to evaluate and screen prospective franchisees, we cannot be certain that our franchisees will have the business acumen or financial resources necessary to operate successful franchises at their approved locations, and state franchise laws may limit our ability to terminate or not renew these franchise agreements. Moreover, despite our training, support and monitoring, franchisees may not successfully operate restaurants in a manner consistent with our standards and requirements or may not hire and adequately train qualified managers and other restaurant personnel. The failure of our franchisees to operate their franchises in accordance with our standards or applicable law, actions taken by their employees or a negative publicity event at one of our franchised restaurants or involving one of our franchisees could have a material adverse effect on our reputation, our brands, our ability to attract prospective franchisees, our company-owned restaurants, and our business, financial condition or results of operations.

Franchisees typically use a point of sale, or POS, cash register system to record all sales transactions at the restaurant. We require franchisees to use a specific brand or model of hardware or software components for their restaurant system. Currently, franchisees report sales manually and electronically, but we do not have the ability to verify all sales data electronically by accessing their POS cash register systems. We have the right under our franchise agreement to audit franchisees to verify sales information provided to us, and we have the ability to indirectly verify sales based on purchasing information. However, franchisees may underreport sales, which would reduce royalty income otherwise payable to us and adversely affect our operating and financial results.

| 12 |

If we fail to identify, recruit and contract with a sufficient number of qualified franchisees, our ability to open new franchised restaurants and increase our revenues could be materially adversely affected.

The opening of additional franchised restaurants depends, in part, upon the availability of prospective franchisees who meet our criteria. Most of our franchisees open and operate multiple restaurants, and our growth strategy requires us to identify, recruit and contract with a significant number of new franchisees each year. We may not be able to identify, recruit or contract with suitable franchisees in our target markets on a timely basis or at all. In addition, our franchisees may not have access to the financial or management resources that they need to open the restaurants contemplated by their agreements with us, or they may elect to cease restaurant development for other reasons. If we are unable to recruit suitable franchisees or if franchisees are unable or unwilling to open new restaurants as planned, our growth may be slower than anticipated, which could materially adversely affect our ability to increase our revenues and materially adversely affect our business, financial condition and results of operations.

If we fail to open new domestic and international franchisee-owned restaurants on a timely basis, our ability to increase our revenues could be materially adversely affected.

A significant component of our growth strategy includes the opening of new domestic and international franchised restaurants. Our franchisees face many challenges associated with opening new restaurants, including: