PART II- OFFERING CIRCULAR

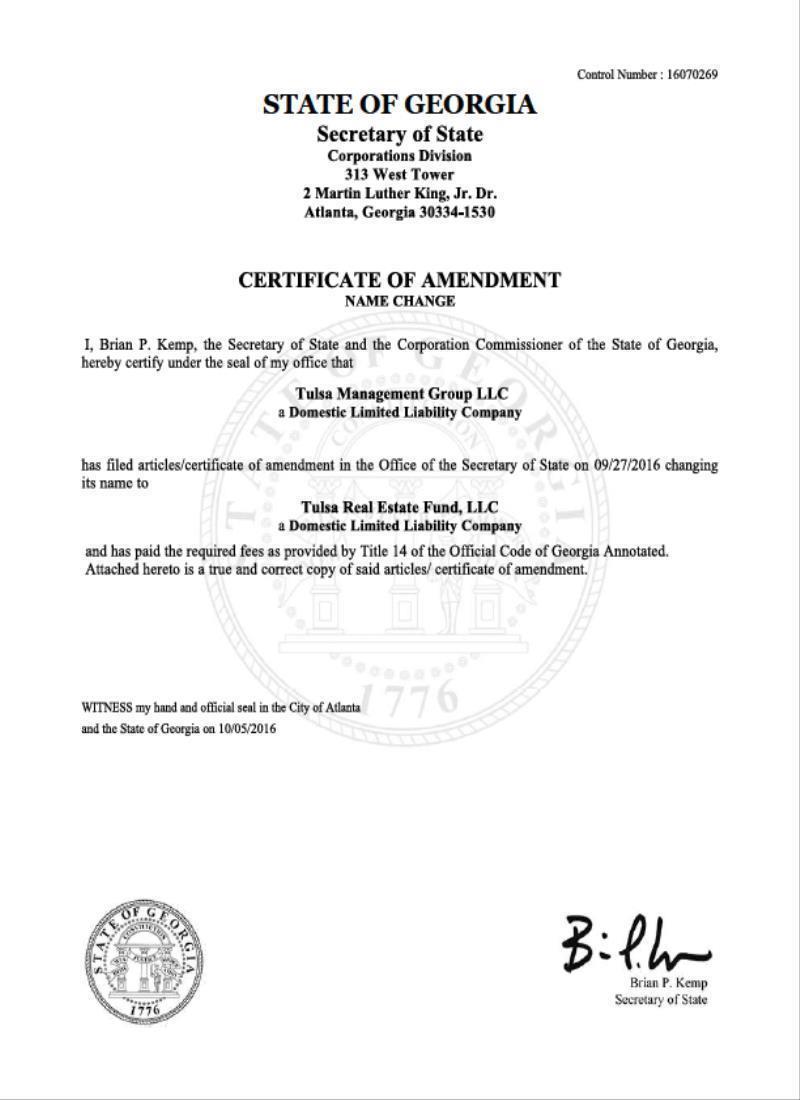

Tulsa Real Estate Fund, LLC

(the “Company”)

Preliminary Prospectus dated___________________________

The Company is hereby providing the information required by Part I of Form S-11 (17 9 CFR 239.18 and are following the requirements for a smaller reporting company as it meets the definition of that term in Rule 405 (17 CFR 230.405).

An offering statement pursuant to Regulation A relating to these securities has been filed with the Securities and Exchange Commission. Information contained in this Preliminary Offering Circular is subject to completion or amendment. These securities may not be sold nor may offers to buy be accepted before the offering statement filed with the Commission is qualified. This Preliminary Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy nor there any sales of these securities in any state in which such offer, solicitation or sale would be unlawful before registration or qualification under the laws of any such state. The Company may elect to satisfy its obligation to deliver a Final Offering Circular by sending you a notice within two business days after the completion of our sale that contains the URL where the Final Offering Circular or the offering statement in which such Final Offering Circular was filed may be obtained.

We are offering 1,000,000 Class A Interests (“Preferred Interests” or “Interests” or “Class Interests”) at $50 per Interest through our Manager (the “Offering.”) Purchasers shall become Class A Members in the Company. Funds will be made immediately available to the Company once the Company raise a minimum of $100,000 (“Minimum Offering”) in a designated escrow account in the Company’s name for the purposes of acquiring assets or working capital. This Offering terminates in 365 days after commencement of this Offering. There are no provisions for the return of funds once the minimum of 2,000 Interests are sold. No commissions will be paid for the sale of the Interests offered by the Company.

|

Class A Interests (Unit) |

|

Price to Investors |

|

|

Sellers’ Commissions |

|

|

Proceeds to the Company |

||||

|

Per Unit or Interest |

$ | 50 | $ | 0.00 | $ | 50 | ||||||

|

Minimum Dollar Amount |

$ | 100,000 | $ | 0.00 | $ | 100,000 | ||||||

|

Maximum Dollar Amount |

$ | 50,000,000 | $ | 0.00 | $ | 50,000,000 | ||||||

No public market currently exists for our Interests. The Company will be managed by Tulsa Founders, LLC which is managed by Jay Morrison (the “Manager.”) The Company has set a minimum investment requirement of $500. Subscribers may start funding their investment account with as little as $50, but their funds will not be invested and they will not become a Member until their individual account has a minimum balance of $500. We do intend to place the funds into a segregated account up to $100,000 that will be in the Company’s name. Subscribers may place as little as $50 into the Company’s segregated account. Such Subscriber funds shall remain in the Company’s segregated account until such time the balance reaches a minimum of $500. At any time prior to reaching the minimum of $500, a Subscriber may ask for a return of funds. Subscription funds may remain in the Company’s segregated account for up to 180 days from the first date of deposit. This will not be an escrow account. Purchasers of our Interests qualified hereunder may be unable to sell their securities, because there may not be a public market for our securities. Any purchaser of our securities should be in a financial position to bear the risks of losing their entire investment.

The transfer of Interests is limited. A Member may assign, his, her or its Interests only if only if certain conditions set forth in the Operating Agreement are satisfied. Please see those conditions on page 35 under “Withdrawal and Redemption Policy”

The Company has been formed to acquire various real estate related assets such single family, multifamily and commercial properties in urban neighborhoods throughout United States.

The Company is considered an “emerging growth company” under Section 101(a) of the Jumpstart Our Business Startups Act as it is an issuer that had total annual gross revenues of less than $1 billion during its most recently completed fiscal year.

Our independent auditors included an explanatory paragraph in the report on our 2016 financial statements related to the uncertainty in our ability to continue as a going concern.

| 1 |

Some of our Risk Factors include:

|

|

· |

We are an emerging growth company with a limited operating history. |

|

|

· |

Subscribers will have limited control in our company with limited voting rights. The Managing Members will manage the day to day operations of the Company. |

|

|

· |

We may require additional financing, such as bank loans, outside of this offering in order for our operations to be successful. |

|

|

· |

We have not conducted any revenue-generating activities and as such have not generated any revenue since inception. |

|

|

· |

Our offering price is arbitrary and does not reflect the book value of our Class A Interests. |

|

|

· |

Investments in real estate and real estate related assets are speculative and we will be highly dependent on the performance of the real estate market. |

|

|

· |

Our independent auditors have expressed substantial doubt about our ability to continue as a going concern in the independent auditors’ report to the financial statements included in the Offering. |

|

|

· |

The Company does not currently own any assets. |

See the section entitled “RISK FACTORS” beginning on page 7 for a more comprehensive discussion of risks to consider before purchasing our Class A Interests.

INVESTMENT IN SMALL BUSINESSES INVOLVES A HIGH DEGREE OF RISK, AND INVESTORS SHOULD NOT INVEST ANY FUNDS IN THIS OFFERING UNLESS THEY CAN AFFORD TO LOSE THEIR ENTIRE INVESTMENT. SEE THE SECTION ENTITLED “RISK FACTORS.”

IN MAKING AN INVESTMENT DECISION INVESTORS MUST RELY ON THEIR OWN EXAMINATION OF THE ISSUER AND THE TERMS OF THE OFFERING, INCLUDING THE MERITS AND RISKS INVOLVED. THESE SECURITIES HAVE NOT BEEN RECOMMENDED OR APPROVED BY ANY FEDERAL OR STATE SECURITIES COMMISSION OR REGULATORY AUTHORITY. FURTHERMORE, THESE AUTHORITIES HAVE NOT PASSED UPON THE ACCURACY OR ADEQUACY OF THIS DOCUMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

THE U.S. SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OF ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR SELLING LITERATURE. THESE SECURITIES ARE OFFERED UNDER AN EXEMPTION FROM REGISTRATION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THESE SECURITIES ARE EXEMPT FROM REGISTRATION.

GENERALLY, NO SALE MAY BE MADE TO YOU IN THIS OFFERING IF THE AGGREGATE PURCHASE PRICE YOU PAY IS MORE THAN 10% OF THE GREATER OF YOUR ANNUAL INCOME OR NET WORTH. DIFFERENT RULES APPLY TO ACCREDITED INVESTORS AND NON-NATURAL PERSONS. BEFORE MAKING ANY REPRESENTATION THAT YOUR INVESTMENT DOES NOT EXCEED APPLICABLE THRESHOLDS, WE ENCOURAGE YOU TO REVIEW RULE 251(D)(2)(I)(C) OF REGULATION A. FOR GENERAL INFORMATION ON INVESTING, WE ENCOURAGE YOU TO REFER TO WWW.INVESTOR.GOV.

| 2 |

|

|

|

4 |

| |

|

|

|

6 |

| |

|

|

|

7 |

| |

|

|

|

16 |

| |

|

|

|

16 |

| |

|

|

|

17 |

| |

|

|

|

19 |

| |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION. |

|

|

20 |

|

|

|

|

23 |

| |

|

|

|

24 |

| |

|

|

|

31 |

| |

|

|

|

32 |

| |

|

|

|

36 |

| |

|

|

|

36 |

| |

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT. |

|

|

36 |

|

|

DIRECTOR, EXECUTIVE OFFICERS, PROMOTERS AND CONTROL PERSONS. |

|

|

36 |

|

|

|

|

38 |

| |

|

|

|

38 |

| |

|

|

|

39 |

| |

|

|

|

39 |

| |

|

|

|

F-1 |

| |

|

|

|

40 |

|

| 3 |

| Table of Contents |

This summary contains basic information about us and the Offering. Because it is a summary, it does not contain all the information that you should consider before investing. You should read the entire Prospectus carefully, including the risk factors and our financial statements and the related notes to those statements included in this prospectus. Except as otherwise required by the context, references in this prospectus to "we," "our," "us," “the Company,” “Tulsa Real Estate Fund,” and "TMG," refer to Tulsa Real Estate Fund, LLC

We were formed on July 20, 2016 and have not yet commenced operations.

We are not a blank check company and do not consider ourselves to be a blank check company as we:

|

|

· |

Have a specific business plan. We have provided a detailed plan for the next twelve (12) months throughout our Prospectus. |

|

|

· |

Have no intention of entering into a reverse merger with any entity in an unrelated industry in the future. |

Since our inception through December 31, 2016, we have not generated any revenues and have incurred a net loss of $0. We anticipate the commencement of generating revenues in the next twelve months. The capital raised in this offering has been budgeted to cover the costs associated with beginning to operate our company, marketing expense, and acquisition related costs. We intend on using the majority of the proceeds from this Offering for the acquisition of properties. However, closing and other acquisition related costs such as title insurance, professional, fees and taxes will likely require cash. We do not have the ability to quantify any of the expenses as they will all depend on size of deal, price, and place versus procuring new financing, due diligence performed (such as appraisal, environmental, property condition reports), legal and accounting, etc. There is no way to predict or otherwise detail expenses.

We intend on engaging in the following activities:

|

|

1. | Purchase single, multi-family, and commercial properties that have potential to be or are cash flow positive, meaning properties that have a positive monthly income after all expenses (mortgages, operating expenses, taxes) and maintenance reserves are paid. In order to determine if a property is “cash flow positive” our Manager will review the total gross rent, income, or receipts from the property and subtract any and all expenses including utilities, taxes, maintenance, and other reserve expenses. If this number is a positive number, the Company will deem the property “cash flow positive.” Depending on how positive the cash flow is will determine whether the management will purchase the property or not on behalf of the Company: there must be a comfortable cash flow potential which our officer is comfortable with. |

|

|

|

|

|

|

2. | Invest in any opportunity our Manager sees fit within the confines of the market, marketplace and economy so long as those investments are real estate related and within the investment objectives of the Company. To this end, at some time in the future, but not within the first 12 months of the Company, the Company may also purchase additional properties or make other real estate investments that relate to varying property types including office, retail and industrial properties. Such property types may include operating properties, properties under and development. It is expected that the Company will only use the proceeds in this Offering to purchase single family, multi-family and commercial properties. |

| 4 |

| Table of Contents |

In all cases, the debt on any given property must be such that it fits with the Investment Policies of the Company. We intend on leveraging our properties with up to 85% of their value.

The Company does not currently own any assets. Please see our “DESCRIPTION OF BUSINESS” on page 24. We believe we will need at least $100,000 to provide working capital and $25,000 for professional fees for the next 12 months.

As of the date of this Offering, we have three principals of our Manager who we anticipate will be devoting half of their working hours to the Company going forward if we are not able to raise a sufficient amount of capital. Jay Morrison through our Manager, will be in charge of our day to day operations until such time we are able to hire other personnel. If we are sufficiently financed, the members of the Manager intend to devote approximately 50% of his working hours to the Company which we believe to be approximately 20 hours, but may be less. Even if we sell all the securities offered, the majority of the proceeds of the offering will be spent for ongoing operational and property acquisition costs. Investors should realize that following this Offering we will be required to raise additional capital to cover the costs associated with our plans of operation.

Some of our Risk Factors include:

|

|

· | We are an emerging growth company with a limited operating history. |

|

|

|

|

|

|

· | Subscribers will have limited control in our company with limited voting rights. The Managing Members will manage the day to day operations of the Company. |

|

|

|

|

|

|

· | We may require additional financing, such as bank loans, outside of this offering in order for our operations to be successful. |

|

|

|

|

|

|

· | We have not conducted any revenue-generating activities and as such have not generated any revenue since inception. |

|

|

|

|

|

|

· | Our offering price is arbitrary and does not reflect the book value of our Class A Interests. |

|

|

|

|

|

|

· | Investments in real estate and real estate related assets are speculative and we will be highly dependent on the performance of the real estate market. |

|

|

|

|

|

|

· | Our independent auditors have expressed substantial doubt about our ability to continue as a going concern in the independent auditors’ report to the financial statements included in the Offering. |

|

|

|

|

|

|

· | The Company does not currently own any assets. |

| 5 |

| Table of Contents |

EXEMPTIONS UNDER JUMPSTART OUR BUSINESS STARTUPS ACT

We are an emerging growth company. An emerging growth company is one that had total annual gross revenues of less than $1,000,000,000 (as such amount is indexed for inflation every 5 years by the Commission to reflect the change in the Consumer Price Index for All Urban Consumers published by the Bureau of Labor Statistics, setting the threshold to the nearest 1,000,000) during its most recently completed fiscal year. We would lose our emerging growth status if we were to exceed $1,000,000,000 in gross revenues. We are not sure this will ever take place.

Because we are an emerging growth company, we have the exemption from Section 404(b) of Sarbanes-Oxley Act of 2002 and Section 14A(a) and (b) of the Securities Exchange Act of 1934. Under Section 404(b), we are now exempt from the internal control assessment required by subsection (a) that requires each independent auditor that prepares or issues the audit report for the issuer shall attest to, and report on, the assessment made by the management of the issuer. We are also not required to receive a separate resolution regarding either executive compensation or for any golden parachutes for our executives so long as we continue to operate as an emerging growth company.

We hereby elect to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(1).

We will lose our status as an emerging growth company in the following circumstances:

|

|

· |

The end of the fiscal year in which our annual revenues exceed $1 billion. |

|

|

|

|

|

|

· |

The end of the fiscal year in which the fifth anniversary of our IPO occurred. |

|

|

|

|

|

|

· |

The date on which we have, during the previous three-year period, issued more than $1 billion in non-convertible debt. |

|

|

|

|

|

|

· |

The date on which we qualify as a large accelerated filer. |

| 6 |

| Table of Contents |

Investors in the Company should be particularly aware of the inherent risks associated with our business. As of the date of this filing our management is aware of the following material risks.

General Risks Related to Our Business

We are an emerging growth company organized in July 2016 and have recently commenced operations, which makes an evaluation of us extremely difficult. At this stage of our business operations, even with our good faith efforts, we may never become profitable or generate any significant amount of revenues, thus potential investors have a high probability of losing their investment.

We were organized in July 2016 and have not yet started operations. As a result of our start-up operations we have; (i) generated no revenues, (ii) will accumulate deficits due to organizational and start-up activities, business plan development, and professional fees since we organized. There is nothing at this time on which to base an assumption that our business operations will prove to be successful or that we will ever be able to operate profitably. Our future operating results will depend on many factors, including our ability to raise adequate working capital, availability of properties for purchase, the level of our competition and our ability to attract and maintain key management and employees.

We are significantly dependent on Jay Morrison. The loss or unavailability of hisservices would have an adverse effect on our business, operations and prospects in that we may not be able to obtain new management under the same financial arrangements, which could result in a loss of your investment.

Our business plan is significantly dependent upon the abilities and continued participation of Jay Morrison. It would be difficult to replace Jay Morrison at such an early stage of development of the Company. The loss by or unavailability of his services would have an adverse effect on our business, operations and prospects, in that our inability to replace Jay Morrison could result in the loss of one's investment. There can be no assurance that we would be able to locate or employ personnel to replace Mr. Morrison should his services be discontinued. In the event that we are unable to locate or employ personnel to replace Mr. Morrison we would be required to cease pursuing our business opportunity, which could result in a loss of your investment

Our independent auditors have expressed in their report substantial doubt about our ability to continue as a going concern.

The Company's ability to continue as a going concern is dependent upon its ability to generate future profitable operations and/or obtain the necessary financing to meet its obligations and repay its liabilities arising from normal business operations when they become due.

You may not have the opportunity to evaluate our investments before we make them, which makes your investment more speculative.

You will be unable to evaluate the economic merit of our note investments before we invest in them and will be entirely relying on the ability of Tulsa Founders, LLC, our Manager, to select our investments. Furthermore, our Manager will have broad discretion in implementing policies regarding tenant or mortgagor creditworthiness, and you will not have the opportunity to evaluate potential tenants, managers or borrowers. These factors increase the risk that your investment may not generate returns comparable to our competitors.

| 7 |

| Table of Contents |

Our Manager will have complete control over the Company and will therefore make all decisions of which Members will have no control.

Tulsa Founders, LLC, our Manager, shall make certain decisions without input by the Members. Such decisions may pertain to employment decisions, including our Manager’s compensation arrangements, the appointment of other officers and managers, and whether to enter into material transactions with related parties.

An investment in the Interests is highly illiquid. You may never be able to sell or otherwise dispose of your Interests.

Since there is no public trading market for our Interests, you may never be able to liquidate your investment or otherwise dispose of your Interests. The Company does currently have a redemption program, but there is no guarantee that the Company will ever redeem or "buy back" your Interests. Further, no one is allowed to redeem their Interests until twelve (12) months after the Interests were purchased. The Company will only redeem Interests up to 5.0% of the value of the assets as calculated on December 31 of the prior year.

Risks Related to the Real Estate Business in General

The profitability of attempted acquisitions is uncertain.

We intend to acquire properties selectively. Acquisition of properties entails risks that investments will fail to perform in accordance with expectations. In undertaking these acquisitions, we will incur certain risks, including the expenditure of funds on, and the devotion of management's time to, transactions that may not come to fruition. Additional risks inherent in acquisitions include risks that the properties will not achieve anticipated sales price or occupancy levels and that estimates of the costs of improvements to bring an acquired property up to standards established for the market position intended for that property may prove inaccurate. Expenses may be greater than anticipated.

Real estate investments are illiquid.

Because real estate investments are relatively illiquid, our ability to vary our portfolio promptly in response to economic or other conditions will be limited. The foregoing and any other factor or event that would impede our ability to respond to adverse changes in the performance of our investments could have an adverse effect on our financial condition and results of operations.

Rising expenses could reduce cash flow and funds available for future acquisitions.

Our properties will be subject to increases in tax rates, utility costs, operating expenses, insurance costs, repairs and maintenance, administrative and other expenses. If we are unable to lease properties on a basis requiring the tenants to pay all or some of the expenses, we would be required to pay those costs, which could adversely affect funds available for future acquisitions or cash available for distributions.

If we purchase assets at a time when the single family, multifamily, or commerial real estate market is experiencing substantial influxes of capital investment and competition for properties, the real estate we purchase may not appreciate or may decrease in value.

The multifamily real estate markets are currently experiencing a substantial influx of capital from investors worldwide. This substantial flow of capital, combined with significant competition for real estate, may result in inflated purchase prices for such assets. To the extent we purchase real estate in such an environment, we are subject to the risk that if the real estate market ceases to attract the same level of capital investment in the future as it is currently attracting, or if the number of companies seeking to acquire such assets decreases, our returns will be lower and the value of our assets may not appreciate or may decrease significantly below the amount we paid for such assets.

A single family, multifamily, or commercial property's income and value may be adversely affected by national and regional economic conditions, local real estate conditions such as an oversupply of properties or a reduction in demand for properties, availability of "for sale" properties, competition from other similar properties, our ability to provide adequate maintenance, insurance and management services, increased operating costs (including real estate taxes), the attractiveness and location of the property and changes in market rental rates. Our income will be adversely affected if a significant number of tenants are unable to pay rent or if our properties cannot be rented on favorable terms. Our performance is linked to economic conditions in the regions where our properties will be located and in the market for multifamily space generally. Therefore, to the extent that there are adverse economic conditions in those regions, and in these markets generally, that impact the applicable market rents, such conditions could result in a reduction of our income and cash available for distributions and thus affect the amount of distributions we can make to you.

| 8 |

| Table of Contents |

We may depend on tenants for some of our revenue and therefore our revenue may depend on the success and economic viability of our tenants.

We will be highly dependent on income from either tenants. Our financial results will depend in part on leasing space in the properties or the full properties we acquire to tenants on economically favorable terms.

In the event of a tenant default prior to stabilization, we may experience delays in enforcing our rights as landlord and may incur substantial costs in protecting our investment and re-letting our property. A default, of a substantial tenant or number of tenants at any one time, on lease payments to us would cause us to lose the revenue associated with such lease(s) and cause us to have to find an alternative source of revenue to meet mortgage payments and prevent a foreclosure if the property is subject to a mortgage. Therefore, lease payment defaults by tenant(s) could cause us to lose our investment or reduce the amount of distributions to Members.

We may not make a profit if we sell a property.

The prices that we can obtain when we determine to sell a property will depend on many factors that are presently unknown, including the operating history, tax treatment of real estate investments, demographic trends in the area and available financing. There is a risk that we will not realize any significant appreciation on our investment in a property. Accordingly, your ability to recover all or any portion of your investment under such circumstances will depend on the amount of funds so realized and claims to be satisfied therefrom.

This offering is a blind pool offering, and therefore, Members will not have the opportunity to evaluate some of our investments before we make them, which makes investments more speculative.

We will seek to invest substantially all of the net offering proceeds from this Offering, after the payment of fees and expenses, in the acquisition of or investment in interests in assets. However, because, as of the date of this prospectus, we have not identified the assets we expect to acquire and because our Members will be unable to evaluate the economic merit of assets before we invest in them, they will have to rely on the ability of our Manager to select suitable and successful investment opportunities. These factors increase the risk that our Members’ investment may not generate returns comparable to our competitors.

Our properties may not be diversified.

Our potential profitability and our ability to diversify our investments may be limited, both geographically and by type of properties purchased. We will be able to purchase additional properties only as additional funds are raised and only if owners of real estate accept our Class A Interests in exchange for an interest in the target property or title to the property. Our properties may not be well diversified and their economic performance could be affected by changes in local economic conditions.

Our performance is therefore linked to economic conditions in the regions in which we will acquire properties and in the market for real estate properties generally. Therefore, to the extent that there are adverse economic conditions in the regions in which our properties are located and in the market for real estate properties, such conditions could result in a reduction of our income and cash to return capital and thus affect the amount of distributions we can make to you.

| 9 |

| Table of Contents |

Competition with third parties in acquiring and operating properties may reduce our profitability and the return on your investment.

We compete with many other entities engaged in real estate investment activities, many of which have greater resources than we do. Specifically, there are numerous commercial developers, real estate companies, and foreign investors that operate in the markets in which we may operate, that will compete with us in acquiring residential, commercial, and other properties that will be seeking investments and tenants for these properties.

Many of these entities have significant financial and other resources, including operating experience, allowing them to compete effectively with us. Competitors with substantially greater financial resources than us may generally be able to accept more risk than we can prudently manage, including risks with respect to the creditworthiness of entities in which investments may be made or risks attendant to a geographic concentration of investments. Demand from third parties for properties that meet our investment objectives could result in an increase of the price of such properties. If we pay higher prices for properties, our profitability may be reduced and you may experience a lower return on your investment. In addition, our properties may be located in close proximity to other properties that will compete against our properties for tenants. Many of these competing properties may be better located and/or appointed than the properties that we will acquire, giving these properties a competitive advantage over our properties, and we may, in the future, face additional competition from properties not yet constructed or even planned. This competition could adversely affect our business. The number of competitive properties could have a material effect on our ability to rent space at our properties and the amount of rents charged. We could be adversely affected if additional competitive properties are built in locations competitive with our properties, causing increased competition for residential renters. In addition, our ability to charge premium rental rates to tenants may be negatively impacted. This increased competition may increase our costs of acquisitions or lower the occupancies and the rent we may charge tenants. This could result in decreased cash flow from tenants and may require us to make capital improvements to properties which we would not have otherwise made, thus affecting cash available for distributions to you.

We may not have control over costs arising from rehabilitation or ground up construction of properties.

We may elect to acquire properties which may require rehabilitation or even be from the “ground up,” meaning that we purchase the land and implement a plan to construct a multifamily building, single family residence or commercial building on the land. In particular, we may acquire affordable properties that we will rehabilitate and convert to market rate properties. We may also purchase land, entitle the land for a multifamily building, single family residence or commercial building (if that is not already provided), architect a multifamily building, single family residence, or commercial building and build a brand new multifamily building, single family residence, or commercial building. Consequently, we intend to retain independent general contractors to perform the actual physical rehabilitation and/or construction work and will be subject to risks in connection with a contractor's ability to control rehabilitation and/or construction costs, the timing of completion of rehabilitation and/or construction, and a contractor's ability to build in conformity with plans and specification.

Inventory or available properties might not be sufficient to realize our investment goals.

We may not be successful in identifying suitable real estate properties or other assets that meet our acquisition criteria, or consummating acquisitions or investments on satisfactory terms. Failures in identifying or consummating acquisitions would impair the pursuit of our business plan. Members ultimately may not like the location, lease terms or other relevant economic and financial data of any real properties, other assets or other companies that we may acquire in the future. Moreover, our acquisition strategy could involve significant risks that could inhibit our growth and negatively impact our operating results, including the following: increases in asking prices by acquisition candidates to levels beyond our financial capability or to levels that would not result in the returns required by our acquisition criteria; diversion of management’s attention to expansion efforts; unanticipated costs and contingent or undisclosed liabilities associated with acquisitions; failure of acquired businesses to achieve expected results; and difficulties entering markets in which we have no or limited experience.

| 10 |

| Table of Contents |

The consideration paid for our target acquisition may exceed fair market value, which may harm our financial condition and operating results.

The consideration that we pay will be based upon numerous factors, and the target acquisition may be purchased in a negotiated transaction rather than through a competitive bidding process. We cannot assure anyone that the purchase price that we pay for a target acquisition or its appraised value will be a fair price, that we will be able to generate an acceptable return on such target acquisition, or that the location, lease terms or other relevant economic and financial data of any properties that we acquire will meet acceptable risk profiles. We may also be unable to lease vacant space or renegotiate existing leases at market rates, which would adversely affect our returns on a target acquisition. As a result, our investments in our target acquisition may fail to perform in accordance with our expectations, which may substantially harm our operating results and financial condition.

The failure of our properties to generate positive cash flow or to appreciate in value would most likely preclude our Members from realizing a return on their Interest ownership.

There is no assurance that our real estate investments will appreciate in value or will ever be sold at a profit. The marketability and value of the properties will depend upon many factors beyond the control of our management. There is no assurance that there will be a ready market for the properties, since investments in real property are generally non-liquid. The real estate market is affected by many factors, such as general economic conditions, availability of financing, interest rates and other factors, including supply and demand, that are beyond our control. We cannot predict whether we will be able to sell any property for the price or on the terms set by it, or whether any price or other terms offered by a prospective purchaser would be acceptable to us. We also cannot predict the length of time needed to find a willing purchaser and to close the sale of a property. Moreover, we may be required to expend funds to correct defects or to make improvements before a property can be sold. We cannot assure any person that we will have funds available to correct those defects or to make those improvements. In acquiring a property, we may agree to lockout provisions that materially restrict us from selling that property for a period of time or impose other restrictions, such as a limitation on the amount of debt that can be placed or repaid on that property. These lockout provisions would restrict our ability to sell a property. These factors and any others that would impede our ability to respond to adverse changes in the performance of our properties could significantly harm our financial condition and operating results.

Illiquidity of real estate investments could significantly impede our ability to respond to adverse changes in the performance of our properties and harm our financial condition.

Because real estate investments are relatively illiquid, our ability to promptly sell one or more properties or investments in our portfolio in response to changing economic, financial and investment conditions may be limited. In particular, these risks could arise from weakness in or even the lack of an established market for a property, changes in the financial condition or prospects of prospective purchasers, changes in national or international economic conditions, and changes in laws, regulations or fiscal policies of jurisdictions in which the property is located. We may be unable to realize our investment objectives by sale, other disposition or refinance at attractive prices within any given period of time or may otherwise be unable to complete any exit strategy. An exit event is not guaranteed and is subject to the Manager’s discretion.

Risks Related to Financing

We might obtain lines of credit and other borrowings, which increases our risk of loss due to potential foreclosure.

We may obtain lines of credit and long-term financing that may be secured by our assets. As with any liability, there is a risk that we may be unable to repay our obligations from the cash flow of our assets. Therefore, when borrowing and securing such borrowing with our assets, we risk losing such assets in the event we are unable to repay such obligations or meet such demands.

| 11 |

| Table of Contents |

We have broad authority to incur debt and high debt levels could hinder our ability to make distributions and decrease the value of our investors’ investments.

Our policies do not limit us from incurring debt until our total liabilities would be at 85% of the value of the assets of the Company. We intend to borrow as much as 85% of the value of our properties. We do not currently own any properties. High debt levels would cause us to incur higher interest charges and higher debt service payments and may also be accompanied by restrictive covenants. These factors could limit the amount of cash we have available to distribute and could result in a decline in the value of our investors’ investments.

Risks Related to Our Corporate Structure

We do not set aside funds in a sinking fund to pay distributions or redeem the Interests, so you must rely on our revenues from operations and other sources of funding for distributions and withdrawal requests. These sources may not be sufficient to meet these obligations.

We do not contribute funds on a regular basis to a separate account, commonly known as a sinking fund, to pay distributions on or redeem the Interests at the end of the applicable non-withdrawal period. Accordingly, you will have to rely on our cash from operations and other sources of liquidity, such as borrowed funds and proceeds from future offerings of securities, for distributions payments and payments upon withdrawal. Our ability to generate revenues from operations in the future is subject to general economic, financial, competitive, legislative, statutory and other factors that are beyond our control. Moreover, we cannot assure you that we will have access to additional sources of liquidity if our cash from operations are not sufficient to fund distributions to you. Our need for such additional sources may come at undesirable times, such as during poor market or credit conditions when the costs of funds are high and/or other terms are not as favorable as they would be during good market or credit conditions. The cost of financing will directly impact our results of operations, and financing on less than favorable terms may hinder our ability to make a profit. Your right to receive distributions on your Interests is junior to the right of our general creditors to receive payments from us. If we do not have sufficient funds to meet our anticipated future operating expenditures and debt repayment obligations as they become due, then you could lose all or part of your investment. We currently do not have any revenues.

You will have limited control over changes in our policies and operations, which increases the uncertainty and risks you face as a Member.

Our Manager determines our major policies, including our policies regarding financing, growth and debt capitalization. Our Manager may amend or revise these and other policies without a vote of the Members. Our Manager’s broad discretion in setting policies and our Members’ inability to exert control over those policies increases the uncertainty and risks you face as a Member. In addition, our Manager may change our investment objectives without seeking Member approval. Although our board has fiduciary duties to our Members and intends only to change our investment objectives when the board determines that a change is in the best interests of our Members, a change in our investment objectives could cause a decline in the value of your investment in our company.

Our ability to make distributions to our Members is subject to fluctuations in our financial performance, operating results and capital improvement requirements.

Currently, our strategy includes paying a preferred return to investors under this Offering that would result in a return of approximately 8% annualized return on investment, of which there is no guarantee. In the event of downturns in our operating results, unanticipated capital improvements to our properties, or other factors, we may be unable to declare or pay distributions to our Members. The timing and amount of distributions are the sole discretion of our Manager who will consider, among other factors, our financial performance, any debt service obligations, any debt covenants, our taxable income and capital expenditure requirements. We cannot assure you that we will generate sufficient cash in order to fund distributions.

| 12 |

| Table of Contents |

Investors will not receive the benefit of the regulations provided to real estate investment trusts or investment companies.

We are not a real estate investment trust and enjoy a broader range of permissible activities. Under the Investment Company Act of 1940, an “investment company” is defined as an issuer which is or holds itself out as being engaged primarily, or proposes to engage primarily, in the business of investing, reinvesting, or trading in securities; is engaged or proposes to engage in the business of issuing face-amount certificates of the installment type, or has been engaged in such business and has any such certificate outstanding; or is engaged or proposes to engage in the business of investing, reinvesting, owning, holding, or trading in securities, and owns or proposes to acquire investment securities having a value exceeding 40 per centum of the value of such issuer’s total assets (exclusive of Government securities and cash items) on an unconsolidated basis.

We intend to operate in such manner as not to be classified as an "investment company" within the meaning of the Investment Company Act of 1940 as we intend on primarily holding real estate. The management and the investment practices and policies of ours are not supervised or regulated by any federal or state authority. As a result, investors will be exposed to certain risks that would not be present if we were subjected to a more restrictive regulatory situation.

If we are deemed to be an investment company, we may be required to institute burdensome compliance requirements and our activities may be restricted

If we are ever deemed to be an investment company under the Investment Company Act of 1940, we may be subject to certain restrictions including:

|

|

· |

restrictions on the nature of our investments; and |

|

|

|

|

|

|

· |

restrictions on the issuance of securities. |

In addition, we may have imposed upon us certain burdensome requirements, including:

|

|

· |

registration as an investment company; |

|

|

|

|

|

|

· |

adoption of a specific form of corporate structure; and |

|

|

|

|

|

|

· |

reporting, record keeping, voting, proxy, compliance policies and procedures and disclosure requirements and other rules and regulations. |

The exemption from the Investment Company Act of 1940 may restrict our operating flexibility. Failure to maintain this exemption may adversely affect our profitability.

We do not believe that at any time we will be deemed an “investment company” under the Investment Company Act of 1940 as we do not intend on trading or selling securities. Rather, we intend to hold and manage real estate. However, if at any time we may be deemed an “investment company,” we believe we will be afforded an exemption under Section 3(c)(5)(C) of the Investment Company Act of 1940, as amended (referred to in this Offering as the “1940 Act”). (If you are going to abbreviate this, this comment should go where the first mention of the Act is which is the first paragraph of this page) Section 3(c)(5)(C) of the 1940 Act excludes from regulation as an “investment company” any entity that is primarily engaged in the business of purchasing or otherwise acquiring “mortgages and other liens on and interests in real estate”. To qualify for this exemption, we must ensure our asset composition meets certain criteria. Generally, 55% of our assets must consist of qualifying mortgages and other liens on and interests in real estate and the remaining 45% must consist of other qualifying real estate-type interests. Maintaining this exemption may adversely impact our ability to acquire or hold investments, to engage in future business activities that we believe could be profitable, or could require us to dispose of investments that we might prefer to retain. If we are required to register as an “investment company” under the 1940 Act, then the additional expenses and operational requirements associated with such registration may materially and adversely impact our financial condition and results of operations in future periods.

| 13 |

| Table of Contents |

Insurance Risks

We may suffer losses that are not covered by insurance.

The geographic areas in which we invest in notes may be at risk for damage to property due to certain weather-related and environmental events, including such things as severe thunderstorms, hurricanes, flooding, tornadoes, snowstorm, sinkholes, and earthquakes. To the extent possible, the Manager may but is not required to attempt to acquire insurance against fire or environmental hazards. However, such insurance may not be available in all areas, nor are all hazards insurable as some may be deemed acts of God or be subject to other policy exclusions.

The Manager expects to obtain a lender’s title insurance policy and will require that owners of property securing its notes maintain hazard insurance naming the Company as the beneficiary. All decisions relating to the type, quality and amount of insurance to be placed on property securing its notes will be made exclusively by the Manager. Certain types of losses that may impact the security for the note could be of a catastrophic nature (due to such things as ice storms, tornadoes, wind damage, hurricanes, earthquakes, landslides, sinkholes, and floods), some of which may be uninsurable, not fully insured or not economically insurable. This may result in insurance coverage that, in the event of a substantial loss, would not be sufficient to pay the full prevailing market value or prevailing replacement cost of the underlying property. Inflation, changes in building codes and ordinances, environmental considerations, and other factors also might make it unfeasible to use insurance proceeds to replace the underlying property once it has been damaged or destroyed. Under such circumstances, the insurance proceeds received might not be adequate to restore the property, leaving the Company without security for its notes.

Furthermore, an insurance company may deny coverage for certain claims, and/or determine that the value of the claim is less than the cost to restore the property, and a lawsuit could have to be initiated to force them to provide coverage, resulting in further losses in income to the Company. Additionally, properties securing the notes may now contain or come to contain mold, which may not be covered by insurance and has been linked to health issues.

Further, when a borrower defaults on a Note, it is likely they will allow their hazard insurance to lapse. The Manager will attempt to obtain its own insurance policies on such properties, to the extent such lender’s policies are available, but it is possible that some of the properties securing the notes may be uninsured for a period of time or uninsurable. If damage occurred during a time when a property was uninsured, the Company may suffer a loss of its security for a loan.

Federal Income Tax Risks

The Internal Revenue Service may challenge our characterization of material tax aspects of your investment in the Interests.

An investment in Interests involves material income tax risks which are discussed in detail in the section of this offering entitled “

TAX TREATMENT OF COMPANY AND ITS SUBSIDIARIES” starting on page 31. You are urged to consult with your own tax advisor with respect to the federal, state, local and foreign tax considerations of an investment in our Interests. We may or may not seek any rulings from the Internal Revenue Service regarding any of the tax issues discussed herein. Accordingly, we cannot assure you that the tax conclusions discussed in this offering, if contested, would be sustained by the IRS or any court. In addition, our legal counsel is unable to form an opinion as to the probable outcome of the contest of certain material tax aspects of the transactions described in this offering, including whether we will be characterized as a “dealer” so that sales of our assets would give rise to ordinary income rather than capital gain and whether we are required to qualify as a tax shelter under the Internal Revenue Code. Our counsel also gives no opinion as to the tax considerations to you of tax issues that have an impact at the individual or partner level.

| 14 |

| Table of Contents |

You may realize taxable income without cash distributions, and you may have to use funds from other sources to fund tax liabilities.

As a Member of the Company, you will be required to report your allocable share of our taxable income on your personal income tax return regardless of whether you have received any cash distributions from us. It is possible that your Interests will be allocated taxable income in excess of your cash distributions. We cannot assure you that cash flow will be available for distribution in any year. As a result, you may have to use funds from other sources to pay your tax liability.

You may not be able to benefit from any tax losses that are allocated to your Interests.

Interests may be allocated their share of tax losses should any arise. Section 469 of the Internal Revenue Code limits the allowance of deductions for losses attributable to passive activities, which are defined generally as activities in which the taxpayer does not materially participate. Any tax losses allocated to investors will be characterized as passive losses, and, accordingly, the deductibility of such losses will be subject to these limitations. Losses from passive activities are generally deductible only to the extent of a taxpayer’s income or gains from passive activities and will not be allowed as an offset against other income, including salary or other compensation for personal services, active business income or “portfolio income”, which includes non-business income derived from dividends, interest, royalties, annuities and gains from the sale of property held for investment. Accordingly, you may receive no benefit from your share of tax losses unless you are concurrently being allocated passive income from other sources.

We may be audited which could subject you to additional tax, interest and penalties.

Our federal income tax returns may be audited by the Internal Revenue Service. Any audit of the Company could result in an audit of your tax return. The results of any such audit may require adjustments of items unrelated to your investment, in addition to adjustments to various Company items. In the event of any such audit or adjustments, you might incur attorneys’ fees, court costs and other expenses in contesting deficiencies asserted by the Internal Revenue Service. You may also be liable for interest on any underpayment and penalties from the date your tax was originally due. The tax treatment of all Company items will generally be determined at the Company level in a single proceeding rather than in separate proceedings with each Member, and our Manager is primarily responsible for contesting federal income tax adjustments proposed by the Internal Revenue Service. In such a contest, our Manger may choose to extend the statute of limitations as to all Members and, in certain circumstances, may bind the Members to a settlement with the Internal Revenue Service. Further, our Manager may cause us to elect to be treated as an electing large Company. If it does, we could take advantage of simplified flow-through reporting of Company items. Adjustments to Company items would continue to be determined at the Company level however, and any such adjustments would be accounted for in the year they take effect, rather than in the year to which such adjustments relate. Our Manager will have the discretion in such circumstances either to pass along any such adjustments to the Members or to bear such adjustments at the Company level.

State and local taxes and a requirement to withhold state taxes may apply, and if so, the amount of net cash from open payable to you would be reduced.

The state in which you reside may impose an income tax upon your share of our taxable income. Further, states in which we will own properties acquired through foreclosure may impose income taxes upon your share of our taxable income allocable to any Company property located in that state. Many states have implemented or are implementing programs to require companies to withhold and pay state income taxes owed by non-resident Members relating to income-producing properties located in their states, and we may be required to withhold state taxes from cash distributions otherwise payable to you. You may also be required to file income tax returns in some states and report your share of income attributable to ownership and operation by the Company of properties in those states. In the event we are required to withhold state taxes from your cash distributions, the amount of the net cash from operations otherwise payable to you would be reduced. In addition, such collection and filing requirements at the state level may result in increases in our administrative expenses that would have the effect of reducing cash available for distribution to you. You are urged to consult with your own tax advisors with respect to the impact of applicable state and local taxes and state tax withholding requirements on an investment in our Interests.

| 15 |

| Table of Contents |

Legislative or regulatory action could adversely affect investors.

In recent years, numerous legislative, judicial and administrative changes have been made in the provisions of the federal income tax laws applicable to investments similar to an investment in our Interests. Additional changes to the tax laws are likely to continue to occur, and we cannot assure you that any such changes will not adversely affect your taxation as a Member. Any such changes could have an adverse effect on an investment in our Interests or on the market value or the resale potential of our properties. You are urged to consult with your own tax advisor with respect to the impact of recent legislation on your investment in Interests and the status of legislative, regulatory or administrative developments and proposals and their potential effect on an investment in our Interests.

DETERMINATION OF OFFERING PRICE

Our Offering Price is arbitrary with no relation to value of the company. This Offering is a self-underwritten offering, which means that it does not involve the participation of an underwriter to market, distribute or sell the Class A Interests offered under this offering.

If the maximum amount of Class A Interests are sold under this Offering, the purchasers under this Offering will own 100% of the Class A Interests outstanding.

If the minimum amount of Class A Interests are sold under this Offering, the purchasers under this Offering will own 100% of the Class A Interests outstanding.

This Offering shall remain open for one year following the Qualification Date of this Offering.

The Class A Interests (Interests) are self-underwritten and are being offered and sold by the Company on a minimum/maximum basis. No compensation will be paid to any principal, the Manager, or any affiliated company or party with respect to the sale of the Class A Interests. This means that no compensation will be paid with respect to the sale of the Class A Interests to Mr. Morrison or affiliated companies. We are relying on Rule 3a4-1 of the Securities Exchange Act of 1934, Associated Persons of an Issuer Deemed not to be Brokers. The applicable portions of the rule state that associated persons (including companies) of an issuer shall not be deemed brokers if they a) perform substantial duties at the end of the offering for the issuer; b) are not broker dealers; and c) do not participate in selling securities more than once every 12 months, except for any of the following activities: i) preparing written communication, but no oral solicitation; or ii) responding to inquiries provided that the content is contained in the applicable registration statement; or iii) performing clerical work in effecting any transaction. Neither the Company, its Manager, nor any affiliates conduct any activities that fall outside of Rule 3a4-1 and are therefore not brokers nor are they dealers. All subscription funds which are accepted will be deposited directly into the Company’s account. This account is not held by an escrow agent. Subscription funds placed in the segregate, Company account may only be released if the Minimum Offering Amount is raised within the Offering Period. The purchase price for the Class A Interests is $50, with a minimum purchase of ten (10) Interests. The Company will raise a minimum of $100,000 prior to funds being released to the Company. If the Company does not raise the Offering Amount within the Offering Period, all proceeds raised to that point will be promptly returned to subscribers of Class A Interests pro-rata, with interest, if any. Subscription Agreements are irrevocable.

| 16 |

| Table of Contents |

The Company plans to primarily use the Tulsa Founders, LLC’s current network of real estate investors of which he already has a pre-existing relationship to solicit investments. The Company, subject to Rule 255 of the 33 Act and corresponding state regulations, is permitted to generally solicit investors by using advertising mediums, such as print, radio, TV, and the Internet. We will offer the securities as permitted by Rule 251 (d)(1)(iii) whereby offers may be made after this Offering has been qualified, but any written offers must be accompanied with or preceded by the most recent offering circular filed with the Commission for the Offering. The Company plans to solicit investors using the Internet through a variety of existing internet advertising mechanisms, such as search based advertising, search engine optimization, and the Company website. The Company website is in the process of being developed.

Please note that the Company will not communicate any information to prospective investors without providing access to the Offering. The Offering may be delivered through the website that is in the process of being developed, through email, or by hard paper copy.

However received or communicated, all of our communications will be Rule 255 compliant and not amount to a free writing prospectus. We will not orally solicit investors and no sales will be made prior to this offering statement being declared qualified and a final Offering is available.

Prior to the acceptance of any investment dollars or Subscription Agreements, the Company will determine which state the prospective investor resides. Investments will be processed on a first come, first served basis, up to the Offering Amount of $50,000,000.

Subscribers may start funding their investment account with as little as $50, but their funds will not be invested and they will not become a Member until their individual account has a minimum balance of $500. We do intend to place the funds into a segregated account up to $100,000 that will be in the Company’s name. Subscribers may place as little as $50 into the Company’s segregated account. Such Subscriber funds shall remain in the Company’s segregated account until such time the balance reaches a minimum of $500. At any time prior to reaching the minimum of $500, a Subscriber may ask for a return of funds. Subscription funds may remain in the Company’s segregated account for up to 180 days from the first date of deposit.

The Offering Period will commence upon the Offering Statement being declared qualified.

No sale will be made to a prospective investor if the aggregate purchase price payable is more than 10% of the greater of the prospective investor’s annual income or net worth. Different rules apply to accredited investors and non-natural persons.

Quarterly, the Manager will report to the Members and will supplement this Offering with material and/or fundamental changes to our operations. We will also provide updated financial statements to all Members and prospective Members.

In compliance with Rule 253(e) of Regulation A, the Manager shall revise this Offering Statement during the course of the Offering whenever information herein has become false or misleading in light of existing circumstances, material developments have occurred, or there has been a fundamental change in the information initially presented. Such updates will not only correct such misleading information but shall also provide update financial statements and shall be filed as an exhibit to the Offering Statement and be requalified under Rule 252.

The net proceeds to us from the sale of up to 1,000,000 Class A Interests offered at an offering price of $50 per Interest will vary depending upon the total number of Class A Interests sold. Regardless of the number of Class A Interests sold, we expect to incur Offering expenses estimated at approximately $60,000 for legal, accounting, and other costs in connection with this offering. The table below shows the intended net proceeds from this offering, indicating scenarios where we sell various amounts of the Class A Interests. There is no guarantee that we will be successful at selling any of the securities being offered in this Offering. Accordingly, the actual amount of proceeds we will raise in this offering, if any, may differ.

| 17 |

| Table of Contents |

The offering scenarios presented below are for illustrative purposes only and the actual amounts of proceeds, if any, may differ.

|

|

|

Minimum |

25% |

50% |

75% |

100% |

||||||||||||||

|

Interests Sold |

|

|

2,000 |

|

|

|

250,000 |

|

|

|

500,000 |

|

|

|

750,000 |

|

|

|

1,000,000 |

|

|

Gross Proceeds |

|

$ | 100,000 |

|

|

$ | 12,500,000 |

|

|

$ | 25,000,000 |

|

|

$ | 37,500,000 |

|

|

$ | 50,000,000 |

|

|

Offering Expenses1 |

|

$ | 0 |

|

|

$ | 60,000 |

|

|

$ | 60,000 |

|

|

$ | 60,000 |

|

|

$ | 60,000 |

|

|

Selling Commissions & Fees2 |

|

$ | 0 |

|

|

$ | 0 |

|

|

$ | 0 |

|

|

$ | 0 |

|

|

$ | 0 |

|

|

Net Proceeds |

|

$ | 100,000 |

|

|

$ | 12,440,000 |

|

|

$ | 24,940,000 |

|

|

$ | 37,440,000 |

|

|

$ | 49,940,000 |

|

|

Asset Management Fee3 |

|

$ | 0 |

|

|

$ | 0 |

|

|

$ | 0 |

|

|

$ | 0 |

|

|

$ | 0 |

|

|

Acquisition Fee4 |

|

$ | 850 |

|

|

$ | 110,740 |

|

|

$ | 222,200 |

|

|

$ | 335,000 |

|

|

$ | 450,000 |

|

|

Acquisitions5 |

|

$ | 85,000 |

|

|

$ | 11,074,000 |

|

|

$ | 22,220,000 |

|

|

$ | 33,500,000 |

|

|

$ | 45,000,000 |

|

|

Related Acquisition Costs6 |

|

$ | 4,675 |

|

|

$ | 609,070 |

|

|

$ | 1,222,100 |

|

|

$ | 1,842,500 |

|

|

$ | 2,475,000 |

|

|

Working Capital7 |

|

$ | 0 |

|

|

$ | 621,190 |

|

|

$ | 1,225,700 |

|

|

$ | 1,662,500 |

|

|

$ | 1,865,000 |

|

|

Legal and Accounting8 |

|

$ | 0 |

|

|

$ | 25,000 |

|

|

$ | 50,000 |

|

|

$ | 100,000 |

|

|

$ | 150,000 |

|

|

Total Use of Proceeds |

|

$ | 90,525 |

|

|

$ | 12,500,000 |

|

|

$ | 25,000,000 |

|

|

$ | 37,500,000 |

|

|

$ | 50,000,000 |

|

___________

|

(1) |

These costs assume the costs related with completing this Form 1-A as well as those costs related to the services of a transfer agent, listing fees, our interim financial statements, and our legal costs ($60,000). It is expected that the Company will reimburse these expenses to the Manager without interest. The Manager has received the Class B Interests in the Company in exchange for its services. The Company will only reimburse the Manager once it is has raised more than $250,000. |

|

|

|

|

(2) |

The Company does not intend on paying selling commissions or fees. In the event that the Company enters into an agreement with a licensed broker dealer, this Offering and Use of Proceeds table will be amended accordingly. |

|

|

|

|

(3) |

The Manager may receive a 5.0% annualized asset management fee paid monthly to the Manager for its services related to asset management. The Manager may receive between an estimated $416 per month as an Asset Management at the Minimum Amount or as much as $187,500 per month at the Maximum Amount. These amounts, however, are not calculated in the Use of Proceeds table because although they are calculated against the amount of capital invested in properties, it is expected that the Asset Management fee will actually be derived from the revenues of the properties purchased by the Company. |

|

| |

|

(4) |

The Manager may be paid up to 1% of the acquisition price of a property as an Acquisition Fee. The Manager may receive between $850 and $450,000 for this fee. |

|

|

|

|

(5) |

We plan to purchase multifamily properties, single family residences and commercial property with the proceeds from this Offering. |

|

|

|

|

(6) |

We believe acquisition related and closing costs could be between 3% and 8% of the value of the acquisition, with an average of 5.5%. These costs could include travel to states in which we purchase multifamily properties, single family residences, and commercial properties, research costs, closing costs, and other costs. Our ability to quantify any of the expenses is difficult as they will all depend on size of deal, price, due diligence performed (such as appraisal, environmental, property condition reports), legal and accounting, etc. We expect the related acquisition costs to be correlated with the price of the property. |

|

|

|

|

(7) |

Costs associated with our web development, marketing and working capital for the next 12 months. |

|

|

|

|

(8) |

Costs for accounting and legal fees associated with being a public company for the next 12 months. |

| 18 |

| Table of Contents |

The Use of Proceeds sets forth how we intend to use the funds under the various percentages of the related offering. All amounts listed are estimates.

The net proceeds will be used for ongoing legal and accounting professional fees (estimated to be between $25,000 and $35,000 depending on our money raise and acquisitions for the next 12 months), working capital for the creation of a website and due diligence costs incurred in locating suitable acquisitions for the Company for the next 12 months, and for the costs associated with acquiring properties, such as broker price opinions, closing costs, title reports, recording fees, accounting costs and legal fees. We determined estimates for ongoing professional fees based upon consultations with our accountants and lawyers, and operating expenses and due diligence costs based upon the Manager’s real estate industry experience.

As of December 31, 2016, the Manager has paid $15,350 to the Company for offering expenses and the balance will be paid by the Manager regardless of the number of Interests sold. Our Offering expenses are comprised of legal and accounting expenses, SEC and EDGAR filing fees, printing and transfer agent fees. Our Manager will not receive any compensation for their efforts in selling our Class A Interests.

The Manager will pay the offering expenses of $60,000 regardless of the amount of Class A Interests we sell and will only be reimbursed if the Company raises a minimum of $250,000. If we sell at least 2,000 Class A Interests, we believe that we will have sufficient funds to continue our filing obligations as a reporting company for the next 12 months. We intend to use the proceeds of this offering in the manner and in order of priority set forth above. We do not intend to use the proceeds to acquire assets or finance the acquisition of other businesses. At present, no material changes are contemplated. Should there be any material changes in the projected use of proceeds in connection with this Offering, we will issue an amended Offering reflecting the new uses.

In all instances, after the qualification of this Form 1-A, the Company will need some amount of working capital to maintain its general existence and comply with its reporting obligations. In addition to changing allocations because of the amount of proceeds received, we may change the use of proceeds because of required changes in our business plan. Investors should understand that we have wide discretion over the use of proceeds. Therefore, management decisions may not be in line with the initial objectives of investors who will have little ability to influence these decisions.

The following summary financial data should be read in conjunction with “MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION” and the Financial Statements and Notes thereto, included elsewhere in this Offering. The statement of operations and balance sheet data from inception through the period ended December 31, 2016 audited financial statements and for the period ended June 30, 2017 unaudited financial statements.

|

|

|

At June 30, 2017 |

|

|

At December 31, 2016 |

| ||

|

|

|

|

|

|

|

| ||

|

TOTAL ASSETS |

|

$ | 15,350 |

|

|

$ | 15,350 |

|

|

|

|

|

|

|

|

|

|

|

|

LIABILITIES AND MEMBERS’ EQUITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LIABILITIES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Current Liabilities |

|

|

15,350 |

|

|

|

15,350 |

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL LIABILITIES |

|

|

15,350 |

|

|

|

15,350 |

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL MEMBERS’ EQUITY |

|

|

- |

|

|

|

- |

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL LIABILITIES AND MEMBERS’ EQUITY |

|

$ | 15,350 |

|

|

$ | 15,350 |

|

| 19 |

| Table of Contents |

|

|

|

June 30, 2017 |

|

|

Inception (July 20, 2016) to December 31, 2016 |

| ||

|

|

|

|

|

|

|

| ||

|

Revenues |

|

$ | 0 |

|

|

$ | 0 |

|

|

|

|

|

|

|

|

|

|

|

|

Expenses |

|

$ | 0 |

|

|

$ | 0 |

|

|

|

|

|

|

|

|

|

|

|

|

Net Income (Loss) |

|

$ | 0 |

|

|

$ | 0 |

|

|

|

|

|

|

|

|

|

|

|

|

Earnings per Interest |

|

$ | .00 |

|

|

$ | .00 |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

The following discussion and analysis should be read in conjunction with our financial statements and the notes thereto contained elsewhere in this filing.

Critical Accounting Policies

Section 107 of the JOBS Act provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards that have different effective dates for public and private companies. We have elected to take advantage of this extended transition period, and thus, our financial statements may not be comparable to those of other reporting companies. Accordingly, until the date we are no longer an “emerging growth company” or affirmatively opt out of the exemption, upon the issuance of a new or revised accounting standard that applies to our financial statements and has a different effective date for public and private companies, we will disclose the date on which adoption is required for non-emerging growth companies and the date on which we will adopt the recently issued accounting standard.

Cautionary Statement Regarding Forward-Looking Statements

With the exception of historical matters, the matters discussed herein are forward-looking statements that involve risks and uncertainties. Forward-looking statements include, but are not limited to, statements concerning anticipated trends in revenues and net income, projections concerning operations and available cash flow. Our actual results could differ materially from the results discussed in such forward-looking statements. The following discussion of our financial condition and results of operations should be read in conjunction with our financial statements and the related notes thereto appearing elsewhere herein.

Background Overview

Tulsa Real Estate Fund, LLC was formed in the State of Georgia in July of 2016. We have no plans to change our business activities or to combine with another business, and we are not aware of any events or circumstances that might cause our plans to change. The Manager of the Company do not have any plans or arrangements to enter into a change of control, business combination or similar transaction or to change management.

TREF allows our communities to own an equity stake in assets in their own community. We call this "Participation Past Donation." People have a vested interest, dollars begin to circulate in our community, and there is a platform that allows us to unite around our common goals.

| 20 |

| Table of Contents |

The Company’s overall strategy is to purchase multifamily, single family, commercial property and raw land in urban communities to rehab, develop and lease or sell those properties for a profit. Some of our projects will be traditional real estate transactions. However, the vast majority will be community impacting projects focused on generating wealth in minority communities while making a profit for Members of the Company.

The Company will be owned by the Manager and have a Membership which may include, but is not limited to: individuals, individual retirement accounts, banks and other financial institutions, endowments, and pension funds.