ROCK FUND VII-A LLC

$50,000,000

of

Preferred Membership Interests

Minimum purchase: $1,000 in Membership Interests

We are offering a minimum of $5,000,000 of Preferred Membership Interests and a maximum of $50,000,000 of Preferred Membership Interests on a “best efforts” basis. If $5,000,000 in subscriptions for the membership interests (the “Minimum Offering”) are not deposited in escrow on or before December 31, 2017 (the “Minimum Offering Period”), all subscriptions will be refunded to subscribers without deduction or interest. Subscribers have no right to a return of their funds during the Minimum Offering Period. If this minimum offering amount has been deposited by December 31, 2017, the offering may continue until the earlier of December 31, 2018 (which date may be extended at our option) or the date when all membership interests have been sold. See “Plan of Distribution” and “Securities Being Offered” for a description of our equity structure. We intend to commence the offering immediately upon the qualification by the Securities & Exchange Commission of the Offering Statement of which this Offering Circular is a part.

Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

There is currently no trading market for our membership interests, and no trading market is likely to exist in the future.

These are speculative securities. Investing in our membership interests involves significant risks. You should purchase these securities only if you can afford a complete loss of your investment. See “Risk Factors” beginning on page 4.

| Amount of Membership Interests | Price to Public | Underwriting Discounts and Commissions | Proceeds to Issuer | |||||||||||||

| Per Dollar: | $ | 1.00 | $ | 1.00 | $ | 0 | $ | 1.00 | ||||||||

| Total Minimum: | $ | 5,000,000 | $ | 5,000,000 | $ | 0 | $ | 5,000,000 | ||||||||

| Total Maximum: | $ | 50,000,000 | $ | 50,000,000 | $ | 0 | $ | 50,000,000 | ||||||||

| (1) | We do not intend to use commissioned sales agents or underwriters. |

| (2) | Does not include expenses of the offering, including costs of blue sky compliance, and marketing expenses, estimated to be $200,000. See “Plan of Distribution”. |

The United States Securities and Exchange Commission does not pass upon the merits of or give its approval to any securities offered or the terms of the offering, nor does it pass upon the accuracy or completeness of any offering circular or other solicitation materials. These securities are offered pursuant to an exemption from registration with the Commission; however, the Commission has not made an independent determination that the securities offered are exempt from registration.

Investing in our Membership Interests is speculative and involves substantial risks. You should purchase these securities only if you can afford a complete loss of your investment. See “Risk Factors” beginning on page 4 to read about the more significant risks you should consider before buying our membership interests. These risks include, but are not limited to, the following:

| · | We have no prior operating history and there is no assurance that we will be able to achieve our investment objectives. |

| · | We may change our operational policies (including our investment guidelines, strategies and policies) without Member consent at any time. |

| · | Because this is a “blind pool” offering, you will not have the opportunity to evaluate our investments before we make them. We currently do not own any properties. |

| · | We depend on our Managing Member to select our investments and conduct our operations. We will pay fees and expenses to our Managing Member and its affiliates that were not determined on an arm’s length basis, and therefore we do not have the benefit of arm’s length negotiations of the type normally conducted between unrelated parties. These fees increase your risk of loss. |

| · | Our Managing Member’s managers and key real estate professionals are also managers and/or key professionals of various affiliates. As a result, they will face conflicts of interest, including time constraints, allocation of investment opportunities and significant conflicts created by our Managing Member’s compensation arrangements with us and other affiliates of our sponsor. |

| · | We may suffer from delays in locating suitable investment properties, which could limit our ability to make distributions and lower the overall return on your investment. |

| · | Real estate investment is inherently speculative. |

| · | There are various tax risks associated with purchasing and owning our membership interests. |

| · | If we raise substantially less than the maximum offering amount, we may not be able to acquire a diverse portfolio of investments and the value of your membership interests may vary more widely with the performance of specific assets. We may commence operations with as little as $5,000,000. |

180 Newport Center Drive, Suite 230

Newport Beach, CA 92660

(949) 640-0600

The date of this offering circular is January 13, 2017

TABLE OF CONTENTS

THIS OFFERING CIRCULAR MAY CONTAIN FORWARD-LOOKING STATEMENTS AND INFORMATION RELATING TO, AMONG OTHER THINGS, US, OUR BUSINESS PLAN AND STRATEGY, AND OUR INDUSTRY. THESE FORWARD-LOOKING STATEMENTS ARE BASED ON THE BELIEFS OF, ASSUMPTIONS MADE BY, AND INFORMATION CURRENTLY AVAILABLE TO OUR MANAGEMENT. WHEN USED IN THE OFFERING CIRCULAR, THE WORDS “ESTIMATE,” “PROJECT,” “BELIEVE,” “ANTICIPATE,” “INTEND,” “EXPECT” AND SIMILAR EXPRESSIONS ARE INTENDED TO IDENTIFY FORWARD-LOOKING STATEMENTS, WHICH CONSTITUTE FORWARD LOOKING STATEMENTS. THESE STATEMENTS REFLECT MANAGEMENT’S CURRENT VIEWS WITH RESPECT TO FUTURE EVENTS AND ARE SUBJECT TO RISKS AND UNCERTAINTIES THAT COULD CAUSE OUR ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE CONTAINED IN THE FORWARD-LOOKING STATEMENTS. INVESTORS ARE CAUTIONED NOT TO PLACE UNDUE RELIANCE ON THESE FORWARD-LOOKING STATEMENTS, WHICH SPEAK ONLY AS OF THE DATE ON WHICH THEY ARE MADE. WE DO NOT UNDERTAKE ANY OBLIGATION TO REVISE OR UPDATE THESE FORWARD-LOOKING STATEMENTS TO REFLECT EVENTS OR CIRCUMSTANCES AFTER SUCH DATE OR TO REFLECT THE OCCURRENCE OF UNANTICIPATED EVENTS.

| 2 |

The following summary highlights selected information contained in this Offering Circular. This summary does not contain all of the information that may be important to you. You should read the more detailed information contained in this offering circular, including, but not limited to, the risk factors beginning on page 4. References to “we,” “us,” “our,” or the “company” mean Rock Fund VII-A LLC.

Our Company

Rock Fund VII-A LLC (the “Company”), is a Delaware limited liability company, the managing member of which is TRP Management VII LLC, a Delaware limited liability company (the “Managing Member”). The net proceeds of this offering will be used primarily to source and acquire residential and commercial properties in Edmonton and Calgary, Canada, some of which may be distressed, and to renovate, lease, operate and maintain such properties. At the discretion of our Managing Member, however, we may invest in other types of properties and in properties in other geographic areas.

This Offering

| Securities offered: | Minimum of $5,000,000 of preferred membership interests. Maximum of $50,000,000 of preferred membership interests. | |

| Preferred Return: | A preferred return shall accrue on the members’ unreturned capital contributions at a rate of 8% per annum (cumulative, but not compounded), meaning that 8% shall accrue on members’ unreturned capital contributions, and that the Managing Member shall not receive any profit distributions, in the case of cash flow from operations, until the Members have received a return of the preferred return that has accrued on their contributed capital, and, in the case of cash flow from the sale of properties, until the Members have received a return of the preferred return that has accrued on their contributed capital, plus all of their contributed capital.

All accepted subscriptions shall be placed in a subscription holding account, and transferred to an operating account at such time as the funds are required to acquire or renovate properties, acquire other assets, or are otherwise required for operating capital. Preferred returns shall not commence accruing on subscription amounts until such time as the applicable funds are transferred to our operating account. The Managing Member may, in its sole discretion, determine which members’ capital contribution are transferred to the operating account and need not transfer funds on a pro rata or first in basis. The Managing Member may base such determination on the size of the capital contribution made by the applicable member, the timing of the member’s capital contribution or on any other factors. | |

| Carried Interest: | Our Managing Member holds a carried interest, which entitles it to receive 30% of the distributions, profits and losses of the Company, subject to the distribution provisions outlined below. See “Distributions”. | |

| Distributions: | Our Managing Member shall, at its discretion, determine the timing and amount of distributions. When made, distributions shall be made as follows:

Cash Flow from Operations. Any rental income and other cash flow from operations which is distributed, shall be distributed (1) first, 100% to our members until they have cumulatively received an amount equal to their preferred return that has accrued through the prior quarter; (2) second, 100% to our Managing Member, until our Managing Member has cumulatively received an amount equal to the sum of 30% of the aggregate preferred return that has been paid to our members; and (3) third, 70% to our members, and 30% to our Managing Member.

Cash Flow from Sales. Any cash from the sale or refinancing of any property which is distributed, shall be distributed or paid, (1) first, 100% to our members until they have cumulatively received an amount equal to their preferred return that has accrued through the prior quarter; (2) second, 100% to our members until they have cumulatively received an amount equal to their total capital contributions; (3) third, 100% to our Managing Member, until our Managing Member has cumulatively received an amount equal to the sum of 30% of the aggregate preferred return that has been paid to our members; and (4) fourth, 70% to our members, and 30% to our Managing Member.

| |

| Use of proceeds: | The net proceeds of this offering will be used primarily to source and acquire residential and commercial properties in Edmonton and Calgary, Canada, and to renovate, lease, operate and maintain such properties. At the discretion of our Managing Member, however, we may invest in other types of real property and in real property in other geographic areas. |

| 3 |

| Risk Factors: | Investing in our membership interests involves a high degree of risk. As an investor, you should be able to bear a complete loss of your investment. You should carefully consider the information set forth in the “Risk Factors” section of this offering circular. |

The Managing Member’s address is 180 Newport Center Drive, Suite 230, Newport Beach, CA. 92660, and telephone number is (949) 640-0600. Our Managing Member’s real estate professionals, including Mr. Alexander Philips and Mr. Michael M. Meyer, will be making investment decisions for the Company.

An investment in our membership interests involves substantial risks. You should carefully consider the following risk factors in addition to the other information contained in this offering circular before purchasing membership interests. The occurrence of any of the following risks might cause you to lose a significant part of your investment. The risks and uncertainties discussed below are not the only ones we face, but do represent those risks and uncertainties that we believe are most significant to our business, operating results, prospects and financial condition. Some statements in this offering circular, including statements in the following risk factors, constitute forward-looking statements.

Risks Related to an Investment in the Company

We have no prior operating history, and the prior performance of the principals of our Managing Member or other real estate investment opportunities entered into by our principals may not predict our future results.

We are a recently formed company and have no operating history. As of the date of this offering circular, we have not made any investments, and prior to our initial closing, our total assets will consist of a limited amount of cash advanced by our Managing Member or its affiliates to cover organizational costs, offering costs and other initial operating expenses. You should not assume that our performance will be similar to the past performance of TwinRock Partners, LLC and other affiliates of our Managing Member in other real estate investment opportunities engaged in by them. Our lack of an operating history significantly increases the risk and uncertainty you face in making an investment in our membership interests.

We have had no revenue to date and have incurred only losses since inception.

We have generated no revenues to date and we have cumulative net losses of approximately $2,976 since inception.

We have minimal operating capital, no significant assets and no revenue from operations.

We have minimal operating capital and for the foreseeable future will be dependent upon our ability to finance our operations from the sale of equity or other financing alternatives. There can be no assurance that we will be able to successfully raise operating capital. The failure to successfully raise operating capital could result in our bankruptcy or other events which would have a material adverse effect on us and our members. We have no significant assets or financial resources, so any such adverse event could put your investment dollars at significant risk.

Our projections and estimates are forward looking and may not be accurate.

Estimates, projections or our goals as to events that may occur in the future or with respect to our future operating or financial performance, including, but not limited to, our pro forma downside, static and base scenarios, and assumptions therein of average rents, effective rents, rent growth, and investor cash-on-cash return, and estimates with respect to our future operating or financial performance and estimated maintenance costs, are based upon the reasonable judgment of our Managing Member and are based on assumptions, data or methods that may be incorrect or imprecise. There is no assurance that actual results, rental and other income, expenses, costs and other items estimated or projected, will be the same, or similar, to those projected or estimated by us. Whether or not financial projections are attained will depend on our achieving our overall business objectives and numerous other factors.

| 4 |

If we are unable to find suitable investments, we may not be able to achieve our investment objectives.

Our ability to achieve our investment objectives depends upon the performance of our Managing Member in the acquisition of investment properties and other assets. In addition, you will have no opportunity to evaluate the economic merits or the terms of our investments before making a decision to invest in us. You must rely entirely on the management abilities of our Managing Member. We cannot assure you that our Managing Member will be successful in sourcing suitable investment properties and assets on financially attractive terms or that, if our Managing Member makes investments on our behalf, our objectives will be achieved. If we, through our Managing Member, are unable to find suitable investment properties promptly, we will hold the proceeds from this offering in an interest-bearing account. If we would continue to be unsuccessful in locating suitable investments, we may ultimately decide to liquidate. In the event we are unable to timely locate suitable investments, we may be unable or limited in our ability to pay distributions and we may not be able to meet our investment objectives.

We may suffer from delays in locating suitable investment properties, which could limit our ability to make distributions and lower the overall return on your investment.

We rely upon our Managing Member’s real estate professionals, including Mr. Alexander Philips and Mr. Michael M. Meyer, to identify suitable investment properties and assets. To the extent that our Managing Member’s real estate professionals face competing demands upon their time in instances when we have capital ready for investment, we may face delays in execution. Further, because we have no pre-selected assets, it may be difficult for us to invest the net offering proceeds promptly and on attractive terms. Delays we encounter in the selection and origination of real property transactions would likely limit our ability to pay distributions to our members and lower their overall returns.

The market in which we participate is competitive and, if we do not compete effectively, our operating results could be harmed.

We face competition from various entities for real estate investment opportunities, including REITs, pension funds, insurance companies, investment funds and developers. Many of these competitors have substantially greater financial resources than we have and may be able to accept more risks or may prove better able to diversify and reduce their risk exposure by investing in a larger number of assets and/or in a larger geographic area. In the future, competition from these entities may reduce the number of suitable investment opportunities available to us or increase the bargaining power of property owners seeking to sell. Further, market conditions might deteriorate to the point that the market offers significant rental concessions to attract tenants. These concessions could adversely affect our ability to maintain or raise rents and could adversely affect our ability to attract or retain tenants. Additionally, our ability to compete depends upon, among other factors, economic trends, investment alternatives, financial condition and operating results of current and prospective tenants, availability and cost of capital, construction and renovation costs, taxes, governmental regulations, legislation and population trends. See “Business - Competition”.

Risks related to Real Estate Investments

Real estate investments will be subject to risks inherent in ownership of real estate.

Real estate cash flows and values are affected by a number of factors, including competition from other available properties and our ability to provide adequate property maintenance and insurance and to control operating costs. Real estate cash flows and values are also affected by such factors as government regulations (including zoning, usage and tax laws), interest rate levels, the availability of financing, property tax rates, utility expenses, potential liability under environmental and other laws and changes in environmental and other laws. Commercial real estate equity investments that we make will be subject to such risks.

Real estate investment is inherently speculative.

Events and conditions that are beyond our control may decrease cash available for distribution and the value of our assets. These events include, but are not limited to:

| 5 |

| · | local oversupply, increased competition or reduced demand for residential or commercial space, |

| · | inability to collect rent from tenants, |

| · | vacancies or our inability to vacant units on favorable terms, |

| · | increased operating costs, including repairs and maintenance, insurance premiums, interest rates, utilities and real estate taxes, |

| · | the ongoing need for capital improvements, |

| · | costs of complying with changes in governmental regulations, including tax laws and city zoning laws, |

| · | the relative illiquidity of real estate investments, |

| · | changing submarket demographics, and |

| · | civil unrest, acts of war and natural disasters, including earthquakes, floods, tornados and fires, which may result in uninsured and underinsured losses, or |

In addition, we could experience a general decline in rents or an increased incidence of defaults under our leases if any of the following occur:

| · | periods of economic slowdown or recession, and other adverse economic conditions affecting property values, including, but not limited to, population decreases, household income decreases, foreclosures, mortgage and other credit availability and governmental policies, |

| · | rising interest rates, |

| · | declining demand for real estate, or |

| · | the public perception that any of these events may occur. |

Any of these events could adversely affect our financial condition, results of operations, cash flow, ability to satisfy our debt service obligations and ability to realize long term gains on our capital investments.

We may invest in distressed real estate.

We intend to invest in real estate in financially distressed areas, and may invest in distressed real estate. If there is no financial recovery in such areas, or we fail to estimate the viability of distressed property we purchase, the same could adversely affect our financial condition, results of operations, cash flow, ability to satisfy our debt service obligations and ability to realize long term gains on our capital investments.

Third party debt obligations expose us to increased risk.

We intend to use third party debt to finance a portion of the purchase price of some or all of the properties we purchase and may later refinance any or all such properties. The use of third party debt may have adverse consequences to us, including the following:

| · | Required payments of principal and interest may be greater than our cash flow from operations; |

| · | We may be forced to dispose of one or more properties, possibly on disadvantageous terms, to make payments on any then-outstanding debt; |

| · | If we default on our debt obligations, the lender or mortgagee may foreclose on one or more of our properties and we may incur recourse liability with respect to any deficiency resulting from such foreclosure; |

| 6 |

| · | A foreclosure on a property will be treated as a sale of such property for a purchase price equal to the outstanding balance of the secured debt on such property. If the outstanding balance of the secured debt exceeds our tax basis in such property, we and our members would recognize taxable income on foreclosure without realizing any accompanying cash proceeds to pay the tax; and |

| · | A default on a loan for one property may result in cross-defaults on loans we have on other properties. |

Uninsured and underinsured losses could adversely affect us.

We intend to carry general liability insurance, fire and extended coverage, covering our properties. We believe that the policy specifications and insured limits we will carry will be adequate given the relative risk of loss, cost of the coverage and standard industry practice. We may discontinue certain coverage, or may elect not to procure such coverage, in the future if the cost of the premiums for any of the policies exceeds, in our judgment, the value of the coverage discounted for the risk of loss. If we experience a loss that is uninsured or that exceeds policy limits, we could lose any capital invested in such properties as well as the anticipated future cash flows from such properties. In addition, if any property is subject to recourse indebtedness, we would continue to be liable for the indebtedness, even if the property is irreparably damaged.

Our investments are illiquid and we may not be able to vary our portfolio in response to changes in economic and other conditions.

The illiquidity of our investments may make it difficult for us to sell such investments if the need or desire arises. If we are required to liquidate all or a portion of our properties quickly, we may realize significantly less than the value at which we have previously purchased them and our ability to vary our portfolio in response to changes in economic and other conditions may be relatively limited, which could adversely affect our results of operations and financial condition.

Disruptions in the financial markets.

Uncertainty in the credit markets may negatively impact our ability to access additional debt financing or to refinance existing debt maturities on favorable terms (or at all), which may negatively affect our ability to maintain our properties. A prolonged downturn in the credit markets may cause us to seek alternative sources of potentially less attractive financing, and may require us to adjust our business plan accordingly.

Risks Related to Our Organization and Structure

Our members do not elect or vote on our Managing Member and have limited ability to influence decisions regarding our business.

Our operating agreement provides that our assets, affairs and business will be managed under the direction of our Managing Member. Our members do not elect or vote on our Managing Member, and, unlike the holders of shares in a corporation, have only limited voting rights on matters affecting our business, and therefore limited ability to influence decisions regarding our business.

Certain provisions of our operating agreement and Delaware law could hinder, delay or prevent a change of control of our company.

Certain provisions of our operating agreement and Delaware law could have the effect of discouraging, delaying or preventing transactions that involve an actual or threatened change of control of our company. See “Securities Being Offered - Certain Anti-Take Over Effects”.

| 7 |

Our operating agreement limits the personal liability of our Managing Member and its affiliates, and requires us to indemnify our Managing Member and its affiliates.

Our operating agreement provides that to the fullest extent permitted by applicable law, our Managing Member, and its managers, officers, and affiliates will not be liable to us. In addition, we have agreed to indemnify our Managing Member, its members, managers and their respective officers and employees, to the fullest extent permitted by law, against all expenses and liabilities (including judgments, fines, penalties, interest, amounts paid in settlement with the approval of the company and attorney’s fees and disbursements) arising from the performance of any of their obligations or duties in connection with their service to us or the operating agreement, including in connection with any civil, criminal, administrative, investigative or other action, suit or proceeding to which any such person may hereafter be made party by reason of being or having been our Managing Member or one of our Managing Member’s directors or officers. These limitations of liability and indemnity provisions are detrimental to you because they restrict the remedies available to you for actions that without those limitations might constitute breaches of duty, including fiduciary duties. By purchasing our membership interests, you will be treated as having consented to the provisions set forth in the operating agreement, which appears as Exhibit 2.2 to the Offering Statement of which this offering circular forms a part. See “Securities Being Offered - Liability and Indemnification of Managing Member and its Affiliates”.

By purchasing membership interests in this offering, you are bound by the arbitration provisions contained in our subscription agreement, which limits your ability to bring class action lawsuits or seek remedy on a class basis.

By purchasing membership interests in this offering, our members agree to be bound by the arbitration provisions contained in Section 7 of our subscription agreement which is Exhibit 2.2 to the Offering Statement of which this offering circular forms a part. Such arbitration provision applies to claims that may be made regarding this offering and, among other things, limits the ability of investors to bring class action lawsuits or similarly seek remedies on a class basis. The subscription agreement allows for either us or an investor to elect to enter into binding arbitration in the event of any claim in which we and the investor are adverse parties, including claims regarding this offering. If one or more investors file a claim against us and we elect to invoke the arbitration clause, the members would lose the ability to seek redress in court and would be required to submit the dispute to arbitration. These restrictions on the ability to bring a class action lawsuit is likely to result in increased costs, both in terms of time and money, to individual investors who wish to pursue claims against us.

Because no public trading market for membership interests currently exists, it will be difficult for you to sell your membership interests and, if you are able to sell your membership interests, you will likely sell them at a substantial discount to the price you paid for them.

Our operating agreement does not require our Managing Member to seek member approval to liquidate our assets by a specified date, nor does our operating agreement require our Managing Member to list our membership interests for trading on a national securities exchange by a specified date, or at all. There is no public market for our membership interests and we currently have no plans to list our membership interests on a stock exchange or other trading market. Until our membership interests are listed, if ever, you may not sell your membership interests unless the buyer meets the applicable suitability and minimum purchase standards. In addition, our operating agreement contains certain restrictions on the transferability of your membership interests. Therefore, it will be difficult for you to sell your membership interests promptly or at all. If you are able to sell your membership interests, you would likely have to sell them at a substantial discount to the price you paid for them. See “Securities Being Offered - Transferability of Membership Interests”.

Your interest in us will be diluted if we issue additional membership interests, which could reduce the overall value of your investment.

Potential investors in this offering do not have preemptive rights to acquire any membership interests we issue in the future. Under our operating agreement, we have authority to issue an unlimited number of additional membership interests or other securities. Depending upon the terms and pricing of any additional offerings and the value of our investments, you may experience dilution in the book value and fair value of your membership interests. See “Ownership and Dilution”.

| 8 |

The interests of our Managing Member, its principals and its other affiliates may conflict with your interests.

The interests of our Managing Member, its principals and its other affiliates may conflict with your interests. TwinRock Partners, LLC is the sole member and manager of our Managing Member. TwinRock Partners, through various affiliates, currently owns proprietary interests in and/or manages other investment properties and investment funds that acquire real estate. In addition, TwinRock Partners, LLC and its affiliates may directly or indirectly engage in future activities in which their interests or the interests of their clients may conflict with our interests, or which may include transactions in similar assets as those held by us and/or assets located in the same geographic areas as properties purchased by us.

In addition, TwinRock Partners, LLC and/or its affiliates may give advice or take action with respect to its existing or future properties in which it holds a proprietary interest, that may differ from the advice given, or may involve a different timing or nature of action taken, than is given or taken with respect to us. Because of different objectives or other factors, TwinRock Partners, LLC, or one of its affiliates may purchase, or advise third parties to purchase, real estate or other assets at a time when we are selling similar property or assets. They may also, in the ordinary course of business, possess, or come into possession of, information relevant to our investment activities that they may be prohibited from using in connection with us, or disclosing to us, or that they may elect not to disclose.

Neither TwinRock Partners, LLC, our Managing Member nor any of their affiliates will have any duty, responsibility or obligation to refrain from (a) engaging in the same or similar activities or lines of business as us; (b) doing business with any potential or actual tenant, lender, purchaser, supplier, customer or competitor of ours or any fund; or (c) engaging in, or refraining from, any other activities whatsoever relating to any of the potential or actual tenants, lenders, purchasers, suppliers or customers of us or any fund.

In addition, any decisions by our Managing Member to renew, extend, modify or terminate an agreement or arrangement, or enter into similar agreements or arrangements in the future, may benefit us, TwinRock Partners, LLC, or any affiliated entities more than another or limit or impair our ability or the ability of TwinRock Partners, LLC, or any other affiliated entity to pursue business opportunities. In addition, third parties may require as a condition to their arrangements or agreements with or related to TwinRock Partners, LLC, us or any one particular affiliated entity, that such arrangements or agreements include or not include us or another affiliated entity, as the case may be. Any of these decisions may benefit us, TwinRock Partners, LLC, or one of the other affiliated entities more than another.

Our Managing Member also has the right, in its sole discretion, to determine whether TwinRock Partners, LLC, or any of its affiliates, may co-invest with us with respect to any particular property investment. In addition, we may acquire properties, or an interest therein, from our affiliates or the affiliates of our Managing Member, from which our Managing Member or its affiliates may derive profit.

Our Managing Member has in the past, and expects to continue in the future, to establish and manage additional real estate funds, including offerings that may acquire or invest in commercial real estate equity investments and other select real estate-related assets. These additional funds may have investment criteria that compete with us. If a sale, financing, investment or other business opportunity would be suitable for more than one of the funds, our Managing Member will allocate it according to the policies and procedures adopted by our Managing Member.

Our Managing Member and its affiliates will receive substantial fees (such as property management fees, leasing commissions and disposition fees) and distribution allocations from us, some of which will not be negotiated at arm’s length. These fees could influence our Managing Member’s advice to us as well as the judgment of affiliates of our Managing Member. See “Management Compensation”.

By acquiring an interest in us, and executing the operating agreement which appears as Exhibit 2.2 to the Offering Statement of which this offering circular forms a part, you will be deemed to have (a) acknowledged the existence of the actual and potential conflicts of interest described herein and to have consented to and waived such conflicts of interest, and (b) waived any claims that our Managing Member’s or its affiliates’ activities described above, will violate the corporate opportunity doctrine, or any fiduciary duty to us or you, or any duty to our creditors. See “Interests of Management and Others in Certain Transactions”.

| 9 |

Preferred returns will not begin to accrue on subscription amounts until we make use of such subscription amounts.

All accepted subscriptions will be placed in a subscription holding account, and transferred to an operating account at such time as the funds are required to acquire or renovate properties, acquire other assets, or for operating capital. Preferred returns will not commence accruing on subscription amounts until such time as the applicable funds are transferred to our operating account. Therefore, the preferred return may not commence accruing on your invested capital for an indefinite period of time. In addition, the Managing Member may, in its sole discretion, determine which members’ capital contribution are transferred to the operating account and need not transfer funds on a pro rata or first in basis. The Managing Member may base such determination on the size of the capital contribution made by the applicable member, the timing of the member’s capital contribution or on any other factors.

If our Managing Member fails to retain its key personnel, we may not be able to achieve our anticipated level of growth and our business could suffer.

Our success depends in substantial part upon the skill and expertise of our Managing Member and its managing member, TwinRock Partners, LLC, and its principals, Alexander Philips and Michael M. Meyer, who would be difficult to replace. You will be relying entirely on our Managing Member and its managing members, and their employees, to manage our affairs. Therefore, you must rely on the ability of our Managing Member to make appropriate investment decisions and to manage our properties. In addition, our Managing Member is required to devote such time to our business and affairs as is necessary to carry out our Managing Member’s duties set forth our operating agreement, however, our Managing Member is not required to devote its full time efforts to us. Also, our members have very limited rights to remove our Managing Member. Therefore, you should not purchase our membership interests unless you are willing to entrust all aspects of our management to our Managing Member.

We may change our investment guidelines without seeking Member approval.

We may change our investment guidelines without Member notice or consent. Although our Managing Member has fiduciary duties to our Members and intends only to change our investment guidelines when it determines that a change is in the best interests of our Members, a change in our investment guidelines could reduce our payment of cash distributions to our Members or cause a decline in the value of our investments.

We may make distributions from any source.

We may pay distributions from any source, including, but not limited to, the proceeds of funds raised in this Offering and from borrowed debt. If we pay distributions from the proceeds of funds raised in this Offering, there would be a dilutive effect on your investment because there would be less capital to invest in properties.

Risks Related to Compliance and Regulation

We are offering our membership interests pursuant to recent amendments to Regulation A promulgated pursuant to the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, and we cannot be certain if the reduced disclosure requirements applicable to Tier 2 issuers will make our membership interests less attractive to investors as compared to a traditional initial public offering.

As a Tier 2 issuer, we will be subject to scaled disclosure and reporting requirements, as compared to a traditional initial public offering, which may make an investment in our membership interests less attractive to investors who are accustomed to enhanced disclosure and more frequent financial reporting. If our scaled disclosure and reporting requirements, or regulatory uncertainty regarding Regulation A, reduces the attractiveness of our membership interests, we may be unable to raise the funds necessary to commence operations, or to develop a diversified portfolio of real estate investments, which could severely affect the value of our membership interests.

Requirement to register under the Investment Company Act and Investment Adviser Act.

The SEC heavily regulates the manner in which “investment companies,” “investment advisors,” and “broker-dealers” are permitted to conduct their business activities. We believe we will conduct our business in a manner that does not result in us being characterized as an investment company, an investment advisor or a broker-dealer, as we do not believe that we will engage in any of the activities that require registration under the Investment Company Act of 1940, the Investment Advisor’s Act of 1940 or any similar provisions under state law. We intend to continue to conduct our business in such manner. If, however, we are deemed to be an investment company, an investment advisor, or a broker-dealer, we may be required to institute burdensome compliance requirements and our activities may be restricted, which would affect our business to a material degree. The loss or potential loss of our exclusion from regulation pursuant to the Investment Company Act, the Investment Advisors Act or any related state exemptions, could require us to restructure our operations, sell certain of our assets or abstain from the purchase of certain assets, which could have an adverse effect on our financial condition and results of operations.

| 10 |

Federal Income Tax Risks

The income tax aspects of an investment in us are complicated, and each investor should review them with his, her or its own professional advisors familiar with the investor’s personal income tax situation and with the income tax laws and regulations applicable to the investor and investment in limited liability companies. We expect to be treated as a partnership for federal income tax purposes, with the result that the investors, not the Company, will be taxed on our recognized income and gain. Investors will have this income tax liability even in the absence of cash distributions and thus may have taxable income and income tax liability arising from their investments in us in years when they receive no cash distributions from us. In addition to federal income taxes, each investor may incur income tax liabilities under the foreign, state or local income tax laws of certain jurisdictions in which we will operate, as well as in the jurisdiction of that investor’s residence or domicile. Foreign, state and local income tax laws vary from one location to another, and federal, state, local and foreign income tax laws are both complex and subject to change.

Tax uncertainty risks.

Because no ruling will be sought from the Internal Revenue Service (the “IRS”), nor will any opinion from tax advisers be obtained regarding the federal income tax consequences of any of the matters discussed in this Offering Circular or any other tax issues affecting us or the investors, there is a risk to investors that the IRS will not agree with our assessment of the tax treatment of an investment in membership interests in us.

Changes in legislation or court decisions.

The federal income tax treatment of an investment in a limited liability company, such as us, may be modified by legislative, judicial or administrative action at any time, and any such action may retroactively affect investments and commitments previously made. The rules dealing with federal income taxation of limited liability companies are constantly under review by the IRS, resulting in revisions of the Internal Revenue Code of 1986, as amended (the “Code”) and the regulations promulgated thereunder (the “Treasury Regulations”), and revised interpretations of established concepts. In evaluating an investment in us, you should consult with your personal tax adviser with respect to possible or pending legislative, judicial and administrative developments.

Risk of IRS determination of profits and losses.

Section 704(b) of the Code provides that allocations of items of income, gain, loss and deduction from a partnership will be respected for tax purposes if such allocations have “substantial economic effect.” Our Operating Agreement contains certain allocations of profits and losses that could be reallocated by the IRS if it were determined that the allocations did not have “substantial economic effect.” Any resulting reallocation of tax items by the IRS may have adverse tax and financial consequences for our investors.

Risk of audit.

Our income tax returns may be audited by the IRS. Any audit of us could result in an audit your tax return causing adjustments of items unrelated to your investment in us, in addition to adjustments to various Company items. In the event of any such adjustments, you may incur attorneys’ fees, court costs and other expenses contesting deficiencies asserted by the IRS. You may also be liable for interest on any underpayment and certain penalties from the date tax was originally due. The tax treatment of all Company items will generally be determined at the Company level in a single proceeding rather than in separate proceedings with each member, and the Managing Member is primarily responsible for contesting federal income tax adjustments proposed by the IRS. The Managing Member may extend the statute of limitations as to all members and, in certain circumstances, may bind the members to a settlement with the IRS.

| 11 |

Federal income tax.

As a limited liability company, we will not be subject to federal income tax. Instead, each member will be required to report on such investor’s federal income tax return its allocated share of our items of income, gain, loss and deduction substantially as if the items had been recognized directly by such member. Accordingly, you generally will be required to pay income tax on your allocable share of our net income or gain in the year recognized without regard to whether we make a corresponding cash distribution. Except as described herein, distributions (as opposed to allocations of taxable income or gain) received by any of our members, generally will not be subject to income tax.

No distributions for taxes.

Members will be required to report their distributive share of our taxable income. Although we may make distributions to the members for them to satisfy taxes imposed on them in respect of their distributive shares of our taxable income, the Managing Member will have full discretion whether or not to make any such distributions. The Operating Agreement does not require the Managing Member to make mandatory tax distributions.

Sale or exchange of interests.

The sale or exchange of membership interests by you generally will result in the recognition of capital gain or loss equal to the difference between your tax basis in the membership interests sold and the amount of consideration received (including any liability relief under Section 752 of the Code). However, a portion of such gain or loss may be recharacterized as ordinary income or loss to the extent attributable to your indirect share of certain Company assets (“unrealized receivables” and “inventory items,” each as specifically defined) described in Section 751 of the Code.

Inability to deduct Company losses.

If we incur operating losses, you may not be able to deduct your share of those losses for federal income tax purposes. Several limitations on the deductibility of such losses exist, including your basis in your membership interest, whether you are considered to be “at risk” with respect to your investment in us, and whether your investment is considered to be “passive” and thus subject to the “passive activity loss” rules.

Filings and information returns.

The Managing Member will use reasonable commercial efforts to cause all tax filings to be made in a timely manner (taking permitted extensions into account); however, investment in us may require the filing of tax return extensions and filing in multiple jurisdictions by members if composite state returns are not filed by us. You may have to file one or more tax filing extensions if we do not deliver Schedule K-1 by the due date of your returns.

Foreign, state and local taxes.

The country or state in which you reside may impose an income tax upon your share of our taxable income. Further, countries or states in which we will invest in properties may impose income taxes upon your share of our taxable income allocable to any Company property located in that state. Many countries and states have also implemented or are implementing programs to require limited liability companies to withhold and pay state or foreign income taxes owed by non-resident members relating to income-producing properties located in their countries or states, and we may be required to withhold state or foreign taxes from distributions otherwise payable to you. In the event we are required to withhold foreign or state taxes from an investor’s distributions, the amount of the distributions otherwise payable to you may be reduced. In addition, such collection and filing requirements at the country or state level may result in increases in our administrative expenses that would have the effect of reducing cash available for distribution to members. You are urged to consult with your own tax advisors with respect to the impact of applicable foreign, state and local taxes and foreign and state tax withholding requirements on an investment in the membership interests.

| 12 |

Certain income directly or indirectly received by us from sources within Canada may be subject to withholding taxes imposed by Canada, and we also may be subject to capital gains taxes in Canada on a sale of real property situated in Canada. The members generally will be entitled to claim either a credit or, if they itemize their deductions, a deduction (subject to the limitations generally applicable to deductions) for their share of such foreign taxes in computing their federal income taxes. However, a member that is tax-exempt ordinarily will not benefit from such a credit or deduction, and a credit for foreign taxes may not exceed your federal tax (before the credit) attributable to your total foreign source taxable income. Because of these limitations, you may be unable to claim a credit for the full amount of your proportionate share of foreign taxes paid by us. As the availability of foreign tax credits depends on each member’s circumstances, each prospective investor should consult with his, her or its own tax advisor regarding the availability of foreign tax credits.

Foreign investors.

Foreign investors should be aware that our income and gain (as well as gain from the sale of the membership interests) may be treated as effectively connected with the conduct of a U.S. trade or business and, thus, be subject to tax (at the federal and possibly state and local levels) at regular U.S. rates even though such investor has no other contacts with the U.S. As a result, the Managing Member anticipates that it will withhold tax from substantially all the income allocable to a foreign investor. Notwithstanding that some of such taxes may be collected by withholding, foreign investors will be required to file appropriate federal (and possibly state and local) tax returns.

Unrelated Business Taxable Income (“UBTI”) risks.

Certain entities, including trusts under plans qualifying under Section 401(a) of the Code, individual retirement accounts, and certain charitable and other organizations described in Section 501(c) of the Code, generally are exempt from federal income tax, but are subject to federal income tax on their UBTI. It is likely that a portion of our gains will constitute UBTI to investors who are tax-exempt owners. If we use leverage in our portfolio investments, we will generate UBTI. If the tax-exempt entity borrows in order to purchase its membership interest, an allocable portion of the income it derives from its investment will be treated as UBTI. Any income earned by us that constitutes UBTI will be allocated to our investors. Each tax-exempt investor should consult its personal tax advisors to determine the effect of any UBTI on its specific tax situation.

Jeopardizing tax-exempt status.

The purchase of the membership interests by certain tax-exempt organizations may, under certain circumstances, adversely affect their tax-exempt status. Each tax-exempt investor should consult its personal tax advisors to obtain advice concerning the effect of an investment in the membership interests on such investor’s tax-exempt status.

| 13 |

The net proceeds of this offering will be used primarily to source and acquire residential and commercial properties in Edmonton and Calgary, Canada, and to renovate, lease, operate and maintain such properties. At the discretion of our Managing Member, however, we may invest in other types of properties and in properties in other geographic areas.

Accordingly, we expect to use the net proceeds as follows:

| Minimum Offering | Maximum Offering | |||||||||||||||

| Amount | Percentage | Amount | Percentage | |||||||||||||

| Real estate investment | $ | 4,200,000 | 84.00 | % | $ | 48,000,000 | 96.00 | % | ||||||||

| Offering and Organizational Expenses | $ | 250,000 | 5.00 | % | $ | 1,000,000 | 2.00 | % | ||||||||

| Due Diligence Fees | $ | 500,000 | 10.00 | % | $ | 500,000 | 1.00 | % | ||||||||

| Working capital | $ | 50,000 | 1.00 | % | $ | 500,000 | 1.00 | % | ||||||||

| TOTAL | $ | 5,000,000 | 100.00 | % | $ | 50,000,000 | 100.00 | % | ||||||||

The foregoing information is an estimate based on our current business plan. We may find it necessary or advisable to re-allocate portions of the net proceeds reserved for one category to another, and we will have broad discretion in doing so. Pending these uses, we intend to invest the net proceeds of this offering in short-term, interest-bearing securities. The foregoing excludes an acquisition fee equal to 1.0% of the purchase price and budgeted capital improvements of any properties we purchase, which shall be paid at the closing of such acquisition to the Managing Member.

The proceeds of this offering will not be used to compensate or otherwise make payments to our Managing Member or any officer, employee or manager of the issuer or any of its subsidiaries, except for the reimbursement of offering expenses and other operating expenses paid for by our Managing Member or its affiliates, and a due diligence fee in the amount of $500,000 to be paid to our Managing Member. See “Management Compensation”.

We intend to use debt, together with the proceeds of this offering, to finance some or all of the properties and assets we purchase, in order to provide more funds available for investment. The material portion of the net proceeds of this Offering is not committed to any specific properties.

To date, the Company has incurred $27,976 in offering and organizational expenses.

| 14 |

Our Company

We were organized as a Delaware limited liability company on March 21, 2016. We were established for the purpose of investing in office, industrial and multi-family properties primarily in Calgary and Edmonton, Alberta, Canada, however, we may invest in other types of properties or properties in other geographic areas. Our Managing Member is TRP Management VII LLC, a Delaware limited liability company. TRP Management VII LLC, is wholly owned and managed by TwinRock Partners, LLC, a Delaware limited liability company. See “Management”.

Market Overview and Opportunity

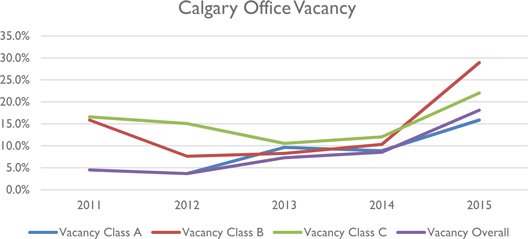

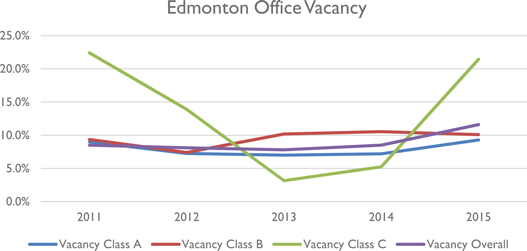

We believe that the near and intermediate-term market for investment in select commercial real estate properties, commercial real estate equity investments, joint venture equity investments, and other real-estate related assets, including, distressed properties, in Canada, and especially Calgary and Edmonton Canada, is compelling from a risk-return perspective. We believe that the following market conditions create a favorable investment environment:

| • | According to a 2012 OECD survey, Canada is the most educated country in the world, with approximately 51% of Canadian adults having attained at least an undergraduate or university degree. |

| • | Calgary and Edmonton are two of the six most populated cities in Canada. |

| • | The Canadian dollar compared to the U.S. dollar has recently been at its weakest value in the last 10 years. |

US v. Canadian Dollar

Google, https://www.google.com/finance?q=usdcad&ei=wDDzVtj3FOPCigLn9I_4Cw

| • | Canada is the world’s 11th largest economy and one of a few developed nations that is a net exporter of energy. Approximately three-quarters of Calgary’s downtown office space is leased by the energy sector. |

| • | Oil has recently hit its lowest price in the last 12 years resulting in a contraction of the Canadian economy. The dip in the energy sector has reduced jobs, which has resulted in an increase in office vacancies. To further complicate matters there is a significant amount of office buildings under construction that will add to the softer market. |

| • | As of December 2015, Alberta’s unemployment rate was 7.0%, the highest since April 2010. |

| • | Alberta has low corporate tax rates and no provincial sales taxes, which is expected to positively impact growth. |

| • | The Alberta government is planning to spend approximately $34B over the next five years on infrastructure and job creation to help boost economic activity. |

| • | Edmonton is building a new arena for the Edmonton Oilers hockey team, which is projected to be completed before the 2016-2017 season. This new arena is the centerpiece around the “Ice District” which has helped boost economic activity in Edmonton. |

Investment Strategy

We intend to use substantially all of the proceeds of this offering to originate, acquire, manage, operate, selectively leverage, hold and opportunistically sell multifamily and mixed use properties, office properties, retail properties, industrial properties and/or commercial real estate in Calgary and Edmonton, Alberta, Canada.

| 15 |

Our investment strategy is to take advantage of the recent downturn in oil prices, the weak Canadian dollar and to capitalize on what we believe are currently under-valued and distressed areas in Alberta, Canada. As a result of these and other economic conditions, vacancies are high and rents are low.

We believe that by purchasing property while vacancies are high and rents are low, we can acquire properties at opportunistic prices. With our proactive management, aggressive marketing and leasing, and by strategically lowering operational expenses, we believe we can maintain and improve the performance of the properties we purchase, and fully capitalize on future rent and pricing growth. We anticipate holding our properties for between 5 and 7 years from acquisition.

In addition to purchasing properties in fee simple, we may enter into joint ventures, partnerships, tenant-in-common investments or other co-ownership arrangements with third parties as well as entities affiliated with our Managing Member, for the acquisition, development or improvement of properties.

We are not limited in the number or size of properties we may acquire or the percentage of net proceeds of this offering that we may invest in a single property. The number and mix of properties we acquire will depend upon real estate and market conditions and other circumstances existing at the time we acquire our properties and the amount of proceeds we raise in this offering. In addition, while we intend to initially focus on acquiring properties in Edmonton and Calgary, Canada, we may acquire properties in other geographical areas.

| 16 |

We believe that our investment strategy, combined with the experience and expertise of our Managing Member’s principals, will provide opportunities to originate investments with attractive long-term equity returns and strong structural features, thereby taking advantage of changing market conditions in order to seek the best risk-return dynamic for our members.

Investment Process

We will follow investment guidelines adopted by our Managing Member. Our Managing Member has the authority to make all decisions regarding our investments, and may change our investment objectives at any time without the approval of our members.

Our Managing Member will focus on the sourcing, acquisition and management of real estate. It will source our investments from new or existing customers, former and current financing and investment partners, third party intermediaries, and competitors looking to share risk and investment.

In selecting investments for us, our Managing Member will utilize our Managing Member’s established investment and underwriting process, which focuses on ensuring that each prospective investment is being evaluated appropriately. The criteria that our Managing Member will consider when evaluating prospective investment opportunities include, but are not limited to:

| • | macroeconomic conditions that may influence operating performance; |

| • | real estate market factors that may influence real estate valuations, real estate lending and/or economic performance of real estate generally; |

| • | analysis of the real estate, including tenant rosters, lease terms, zoning, operating costs and the asset’s overall competitive position in its market; |

| • | real estate and leasing market conditions affecting the real estate; |

| • | existing and potential cash flow; |

| • | estimated costs and timing of required capital improvements; |

| • | review of third-party reports, including appraisals, engineering and environmental reports; |

| • | physical inspections; and |

| • | the overall structure of the investment. |

Borrowing Policy

We intend to use debt to partially finance some or all of the properties we purchase, in order to provide more funds available for investment. We believe use of structured leverage will help us achieve our diversification goals and potentially enhance the returns on our investment. The Company expects that the maximum debt leverage used by the Company for any property will be 75% and for the entire portfolio, will be 75%.

| 17 |

Competition

Our success depends, in large part, on our ability to source, acquire and manage attractive investments. We compete with many other entities engaged in real estate investment activities, including individuals, corporations, bank and insurance company investment accounts, REITs, private real estate funds, and other entities engaged in real estate investment activities, many of which have greater financial resources and lower costs of capital available to them than we have. Many of these competitors have acquisition objectives similar to ours, and others may be organized in the future, which may increase competition for the investments suitable for us. Competitive variables include market presence and visibility, amount of capital to be invested per project and underwriting standards. To the extent that a competitor is willing to risk larger amounts of capital in a particular transaction or to employ more liberal underwriting standards when evaluating potential investments than we are, our investment volume and profit margins for our investment portfolio could be impacted. Our competitors may also be willing to accept lower returns on their investments and may succeed in buying the assets that we have targeted for acquisition. Although we believe that we are well positioned to compete effectively in each facet of our business, there is enormous competition in our market sector and there can be no assurance that we will compete effectively or that we will not encounter increased competition in the future that could limit our ability to conduct our business effectively.

Investment Company Act Considerations

We intend to conduct our operations so that we are not required to register as investment company under the Investment Company Act.

Section 3(a)(1)(A) of the Investment Company Act defines an investment company as any issuer that is or holds itself out as being engaged primarily in the business of investing, reinvesting or trading in securities. Section 3(a)(1)(C) of the Investment Company Act defines an investment company as any issuer that is engaged or proposes to engage in the business of investing, reinvesting, owning, holding or trading in securities and owns or proposes to acquire investment securities having a value exceeding 40% of the value of the issuer’s total assets (exclusive of U.S. Government securities and cash items) on an unconsolidated basis, which we refer to as the 40% test. Excluded from the term “investment securities,” among other things, are U.S. Government securities and securities issued by majority-owned subsidiaries that are not themselves investment companies and are not relying on the exception from the definition of investment company set forth in Section 3(c)(1) or Section 3(c)(7) of the Investment Company Act.

We intend, directly or through our subsidiaries, to originate, invest in and manage a diversified portfolio of commercial real estate investments. We anticipate that we will acquire and hold real estate and real estate-related assets (i) directly, (ii) through wholly-owned subsidiaries, (iii) through majority-owned joint venture subsidiaries, and, (iv) to a lesser extent, through minority-owned joint venture subsidiaries. We may also invest, to a limited extent, in commercial real estate loans, as well as commercial real estate-related debt securities and other real estate-related assets.

We will monitor our compliance with the 40% test and the holdings of our subsidiaries to ensure that we are in compliance with an applicable exemption or exclusion from registration as an investment company under the Investment Company Act. In addition, we believe that neither we nor certain of our subsidiaries will be considered investment companies under Section 3(a)(1)(A) of the Investment Company Act because we and they will not engage primarily or hold themselves out as being engaged primarily in the business of investing, reinvesting or trading in securities. Rather, we and such subsidiaries will be primarily engaged in non-investment company businesses related to real estate. Consequently, we and our subsidiaries expect to be able to conduct our operations such that none will be required to register as an investment company under the Investment Company Act.

The loss or potential loss of our exclusion from regulation pursuant to the Investment Company Act could require us to restructure our operations, sell certain of our assets or abstain from the purchase of certain assets, which could have an adverse effect on our financial condition and results of operations.

Other Government Regulations

Our business will be subject to many laws and governmental regulations. Changes in these laws and regulations, or their interpretation by agencies and courts, occur frequently. Under various environmental laws, a current or previous owner or operator of any real property we purchase may be held liable for the costs of removing or remediating hazardous or toxic substances. These laws may impose clean-up responsibility and liability without regard to whether the owner or operator was responsible for, or even knew of, the presence of the hazardous or toxic substances. In addition, the properties we acquire will likely be subject to various regulatory requirements, such as zoning and fire and life safety requirements. Failure to comply with these requirements could result in the imposition of fines by governmental authorities or awards of damages to private litigants. We intend to acquire properties that are in material compliance with all such regulatory requirements. However, we cannot assure you that these requirements will not be changed or that new requirements will not be imposed which would require significant unanticipated expenditures by us and could have an adverse effect on our financial condition and results of operations.

| 18 |

Legal Proceedings

There are no legal proceedings material to our business or financial condition pending and, to the best of our knowledge, there are no such legal proceedings contemplated or threatened.

Properties

Our principal office is located at 180 Newport Center Drive, Suite 230, Newport Beach, California. We lease office space, free of charge, from TwinRock Partners, LLC, the managing member of our Managing Member. We have not yet purchased any investment properties.

Employees

As of June 1, 2016, we had no employees. Our Managing Member handles all of our operations and management.

| 19 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION

General

As of the date of this offering circular, we have not yet commenced active operations. Offering proceeds will be applied to investment in properties, the payment of third party real estate sales and broker’s commissions and other third party fees and expenses related to the purchase and sale of properties we acquire, the reimbursement to the Managing Member of organizational and offering expenses, the payment of future organizational and offering expenses, the payment of certain other fees due or to become due to the Managing Member (See Management Compensation), and the other uses as described throughout this offering circular. We will experience a relative increase in liquidity as we receive additional proceeds from the sale of membership interests and a relative decrease in liquidity as we spend net offering proceeds in connection with the acquisition and operation of our properties or other investments.

Further, we have not entered into any arrangements creating a reasonable probability that we will acquire a specific property or other asset. The number of properties and other assets that we will acquire will depend upon the amount of membership interests sold and the resulting amount of the net proceeds available for investment in properties and other assets. All accepted subscriptions shall be placed in a subscription holding account, and transferred to an operating account at such time as the funds are required to acquire or renovate properties, acquire other assets, or are otherwise required for operating capital. Preferred returns shall not commence accruing on subscription amounts until such time as the applicable funds are transferred to our operating account.

We intend to make reserve allocations as necessary to aid our objective of preserving capital for our investors by supporting the maintenance and viability of properties we acquire in the future. If reserves and any other available income become insufficient to cover our operating expenses and liabilities, it may be necessary to obtain additional funds by borrowing, refinancing properties, liquidating our investment in one or more assets or raising more equity capital. There is no assurance that such funds will be available, or if available, that the terms will be acceptable to us. Additionally, our ability to borrow additional funds will be limited by the restrictions placed on our and our subsidiaries' borrowing activities by our lenders.

Results of Operation

Having not commenced active operations, we have not acquired any properties or other assets, our management is not aware of any material trends or uncertainties, favorable or unfavorable, other than economic conditions affecting our targeted portfolio, the commercial and residential rental real estate industry and real estate generally, which may be reasonably anticipated to have a material impact on the capital resources and the revenue or income to be derived from the operation of our assets.

Liquidity and Capital Resources

We are offering and selling to the public in this offering up to $50,000,000 of membership interests. Our principal demands for cash will be for acquisition costs, including the purchase price of any properties and assets we acquire, improvement costs, real estate commissions, the payment of our operating and administrative expenses, and all continuing debt service obligations. Generally, we will fund our acquisitions from the net proceeds of this offering. We intend to acquire our assets with cash and mortgage or other debt, but we also may acquire assets free and clear of permanent mortgage or other indebtedness by paying the entire purchase price for the asset in cash.

We expect to use debt financing as a source of capital. We have no limits on the amount of leverage we may employ and we expect to use the maximum available leverage.

We anticipate that adequate cash will be generated from operations to fund our operating and administrative expenses, and all continuing debt service obligations. However, our ability to finance our operations is subject to some uncertainties. Our ability to generate working capital is dependent on our ability to attract and retain tenants and the economic and business environments of the various markets in which our properties are located. Our ability to sell our assets is partially dependent upon the state of real estate markets and the ability of purchasers to obtain financing at reasonable commercial rates. In general, we intend to pay debt service from cash flow from operations.

| 20 |

Potential future sources of capital include secured or unsecured financings from banks or other lenders, establishing additional lines of credit, proceeds from the sale of properties, undistributed cash flow, and additional equity investments. Note that, currently, we have not identified any source of financing, other than the proceeds of this offering, and there is no assurance that such sources of financing will be available on favorable terms or at all.

We operate under the direction of our Managing Member, which is responsible for managing our day-to-day affairs, and implementing our investment strategy. Our Managing Member is wholly owned and controlled by TwinRock Partners, LLC, which is wholly owned and controlled by Alexander Philips and Michael L. Meyer.

TwinRock Partners, headquartered in Newport Beach, California, is a real estate investment company, primarily focused on investing in unique or “contrarian” opportunities while providing best-in-class management services to its investors.

Founders Michael Meyer and Alexander Philips incorporated TwinRock Partners in 2006, and brought more than 50 years of investment experience to the new company. Mr. Phillips, a former Director in the North American Equity Investments group with GE Capital, is TwinRock’s Chief Executive and Investment Officer. Mr. Meyer, who now serves as TwinRock’s Chairman, had retired after nearly 35 years as managing partner of the Orange County offices of EYKL. He began investing in Japanese notes in 1998, and switched to real estate in 2002.

From those early days, Mssrs. Meyer and Phillips have used a contrarian investment strategy that has brought the company its success to date. The firm routinely seeks investment offerings that are low, taking advantage of opportunistic offerings while mitigating risk and exposure.

As one of the first entrants into the single-family, buy-to-rent market, TwinRock invested approximately $50 million throughout the Western United States. Over the years, TwinRock’s proprietary systems and procedures have led to excellence in the complexities of acquiring, renovating, managing, and leasing residential homes, which was the catalyst and provided the foundation to the company’s multi-family platform. TwinRock’s dedicated team of professionals continues to provide these services for multi-family and student housing strategies.

With this strong company growth, TwinRock was able to launch and now manages a successful Value Opportunity Hedge Fund. Additionally, TwinRock remains on the cutting edge of emerging student housing investments.

To date TwinRock has invested nearly $750 million in real estate with high net-worth, ultra-high net-worth, family offices and institutional partners. As a leading private real estate investment firm, TwinRock’s investments have consistently produced above-average returns.

Managing Members of TwinRock Partners, LLC

Neither us or our Managing Member has any employees. As of the date of this offering circular, the managers and key employees of TwinRock Partners, LLC, the managing member of our Managing Member, are as follows:

Name |

Age | Position | Term |

| Alexander Philips | 39 | Managing Member | 2006 - Present |

| Michael M. Meyer | 77 | Managing Member | 2006 - Present |

| Shelley McCullough | 46 | Director of Operations | January 2013 - Present |

| Viet Bui | 28 | Associate Director of Investor Relations | August 2013 - Present |