As submitted to the Securities and Exchange Commission on June 29, 2016

XTI Aircraft Company

![]()

Up to 20,000,000 Shares of Common Stock

Minimum purchase:

350 Shares ($350)

We are offering up to 20,000,000 shares of common stock on a “best efforts” basis. Since there is no minimum amount of securities that must be purchased, all investor funds will be available to the company upon commencement of this Offering upon one or more closings, which may take place at the company’s discretion, and no investor funds will be returned if an insufficient amount of shares are sold to cover the expenses of this Offering and provide net proceeds to the company.

Generally, no sale may be made to you in this Offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov

Sale of these shares will commence after the Offering Statement filed with the Commission is qualified. We currently estimate that sale of these shares will commence on or about , 2016.

There is currently no trading market for our common stock.

These are speculative securities. Investing in our shares involves significant risks. You should purchase these securities only if you can afford a complete loss of your investment. See “Risk Factors” beginning on page 5.

1

| Underwriting | |||||||||||||||

| Number of | Price to | discount and | Proceeds to | Proceeds to | |||||||||||

| Shares | Public | commissions (1) | issuer (2) | other persons | |||||||||||

| Per share | 1 | $ | 1.00 | $ | 0.00 | $ | 1.00 | $ | 0.00 | ||||||

| Total Maximum | 20,000,000 | $ | 20,000,000 | $ | 0.00 | $ | 20,000,000 | $ | 0.00 |

| (1) |

We do not intend to use commissioned sales agents or underwriters. | |

| (2) |

Does not include expenses of the Offering, including costs of blue sky compliance, fees to be paid to FundAmerica Securities, LLC or David Bovino, Esq., and costs of posting offering information on StartEngine.com. At the maximum offering, the company estimates it will pay the following fees in cash: between $211,490 and $1,343,890 to FundAmerica depending on how many shares each investor purchases (the company has assumed it will pay $333,520 in the “Use of Proceeds to Issuer” below), $500,000 to StartEngine and $200,000 to David Bovino. In addition, the company assumes it will pay $1,003,174 to David Brody for the redemption of certain convertible notes and contingent payments at the maximum offering. However, under the Brody Note, the company will not owe anything to Mr. Brody unless and until $5 million is raised in this Offering. At any time after that amount is raised, and at the point when $10 million and $15 million is raised, the company will make payments of $250,000 each, if Mr. Brody does not convert all or part of the Note into shares of the company. See “Plan of Distribution” and “Interest of Management and Others in Certain Transactions”. |

The United States Securities and Exchange Commission does not pass upon the merits of or give its approval to any securities offered or the terms of the Offering, nor does it pass upon the accuracy or completeness of any Offering Circular or other solicitation materials. These securities are offered pursuant to an exemption from registration with the Commission; however, the Commission has not made an independent determination that the securities offered are exempt from registration.

The Offering will terminate at the earlier of: (1) the date at which the maximum offering amount has been sold, (2) the date which is one year from this Offering Statement being re-qualified by the Commission, or (3) the date at which the Offering is earlier terminated by the company in its sole discretion.

We are following the “Offering Circular” format of disclosure under Regulation A.

Centennial Airport, 13000 Control Tower Rd., Suite 217, Englewood, Colorado 80112 (303) 503-5660; www.xtiaircraft.com

The date of this Offering Circular is June XX, 2016

2

TABLE OF CONTENTS

THIS OFFERING CIRCULAR MAY CONTAIN FORWARD-LOOKING STATEMENTS AND INFORMATION RELATING TO, AMONG OTHER THINGS, THE COMPANY, ITS BUSINESS PLAN AND STRATEGY, AND ITS INDUSTRY. THESE FORWARD-LOOKING STATEMENTS ARE BASED ON THE BELIEFS OF, ASSUMPTIONS MADE BY, AND INFORMATION CURRENTLY AVAILABLE TO THE COMPANY’S MANAGEMENT. WHEN USED IN THE OFFERING MATERIALS, THE WORDS “ESTIMATE,” “PROJECT,” “BELIEVE,” “ANTICIPATE,” “INTEND,” “EXPECT” AND SIMILAR EXPRESSIONS ARE INTENDED TO IDENTIFY FORWARD-LOOKING STATEMENTS. THESE STATEMENTS REFLECT MANAGEMENT’S CURRENT VIEWS WITH RESPECT TO FUTURE EVENTS AND ARE SUBJECT TO RISKS AND UNCERTAINTIES THAT COULD CAUSE THE COMPANY’S ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE CONTAINED IN THE FORWARD-LOOKING STATEMENTS. INVESTORS ARE CAUTIONED NOT TO PLACE UNDUE RELIANCE ON THESE FORWARD-LOOKING STATEMENTS, WHICH SPEAK ONLY AS OF THE DATE ON WHICH THEY ARE MADE.

3

1. SUMMARY OF INFORMATION IN OFFERING CIRCULAR

The following summary highlights selected information contained in this Offering Circular. This summary does not contain all the information that may be important to you. You should read the more detailed information contained in this Offering Circular., including, but not limited to, the risk factors beginning on page . References to “XTI,” “we,” “us,” “our,” or the “company” mean XTI Aircraft Company.

Our Company

XTI Aircraft Company began operations in 2012. XTI is an aircraft manufacturer that is developing a “vertical takeoff airplane” – the TriFan 600. This first-of-its-kind fixed-wing airplane combines features of a private jet allowing high speed travel over long distances in comfort, with the capability to take off and land like a helicopter. A primary driver of why people choose to fly privately is the time they save traveling versus flying commercially. XTI analyzed the market for a vertical takeoff airplane. It determined that existing aircraft are unable to save as many travel hours as the TriFan 600, which potentially reduces total trip times by as much as half. XTI believes that offering a product that reaches over 20 times the number of U.S. airports than the airlines, over three times the number of airports than business jets can fly into, that departs and lands in remote locations without an airstrip, and translates to significant time savings, could result in a successful business within a multi-billion dollar industry.

This Offering

XTI recently conducted a best-efforts, minimum-maximum offering under Regulation A, but was unable to meet the $3 million minimum contingency and therefore terminated the offering and returned all funds to subscribers. The current Offering is substantially similar to that offering, with the exception that the current Offering has no minimum contingency.

| Securities offered | Maximum of 20,000,000 shares of common stock ($20,000,000) |

| Common stock | 35,869,565 shares |

| outstanding before the | |

| Offering | |

| Common stock | 55,869,565 shares |

| outstanding after the | |

| Offering (1) | |

| Use of proceeds |

The use of proceeds from the Offering will be used to fund four key areas: (i) hiring key members of the management team; (ii) pursuing additional funding; (iii) continuing development of the aircraft; and (iv) expanding sales and marketing to enable the company to take refundable customer deposits. |

| Risk factors |

Investing in our shares involves a high degree of risk. As an investor you should be able to bear a complete loss of your investment. You should carefully consider the information set forth in the “Risk Factors” section of this Offering Circular. |

| (1) Assumes the sale of 20,000,000 shares |

4

2. RISK FACTORS

Investing in our shares involves risk. In evaluating XTI Aircraft Company and an investment in the shares, careful consideration should be given to the following risk factors, in addition to the other information included in this Offering Circular. Each of these risk factors could materially adversely affect XTI’s business, operating results or financial condition, as well as adversely affect the value of an investment in our shares. The following is a summary of the most significant factors that make this Offering speculative or substantially risky. The company is still subject to all the same risks that all companies in its industry, and all companies in the economy, are exposed to. These include risks relating to economic downturns, political and economic events and technological developments (such as cyber-security). Additionally, early-stage companies are inherently more risky than more developed companies. You should consider general risks as well as specific risks when deciding whether to invest.

We are an early stage company and have not yet generated any revenues

XTI has had no net income, only a three-year operating history, and no revenues generated since its inception. There is no assurance that XTI will ever be profitable or generate sufficient revenue to pay dividends to the holders of the shares. XTI does not believe it will be able to generate revenues without successfully completing the certification of its proposed TriFan 600 aircraft, which involves substantial risk. As a result, XTI is dependent upon the proceeds of this Offering and additional fund raises to continue the TriFan 600 preliminary design and other operations. Even if XTI is successful in this Offering, XTI’s proposed business will require significant additional capital infusions. Based on XTI’s current estimates, XTI will require a minimum of $400 million in capital to fully implement its proposed business plan. If planned operating levels are changed, higher operating costs encountered, lower sales revenue received, more time is needed to implement the plan, or less funding received from customer deposits or sales, more funds than currently anticipated may be required. Additional difficulties may be encountered during this stage of development, such as unanticipated problems relating to development, testing, and initial and continuing regulatory compliance, vendor manufacturing costs, production and assembly, and the competitive and regulatory environments in which XTI intends to operate. If additional capital is not available when required, if at all, or is not available on acceptable terms, XTI may be forced to modify or abandon its business plan.

The company has realized significant operating losses to date and expects to incur losses in the future

The company has operated at a loss since inception, and these losses are likely to continue. XTI’s net losses for 2014 and 2015 were $331,937 and $1,256,881, respectively. Until the company achieves profitability, it will have to seek other sources of capital in order to continue operations.

The company’s auditor has issued a going concern opinion

XTI’s auditor has issued a “going concern” opinion on the company’s financial statements. The company has negative working capital, has incurred recurring losses and recurring negative cash flow from operating activities, and has an accumulated deficit which raises substantial doubt, in the opinion of the auditor, about its ability to continue as a going concern.

5

We are controlled by our Chairman, whose interests may differ from those of the other shareholders.

As of the date of this Offering Circular, David Brody owns the majority of shares of the company’s common stock, and his majority ownership might continue even after the issuance of the shares. Therefore, Mr. Brody is now and could be in the future in a position to elect or change the members of the board of directors and to control XTI’s business and affairs including certain significant corporate actions, including but not limited to acquisitions, the sale or purchase of assets and the issuance and sale of XTI’ shares. XTI also may be prevented from entering into transactions that could be beneficial to the other holders of the shares without Mr. Brody’s consent. Mr. Brody’s interests might differ from the interests of other shareholders.

The development period for the TriFan 600 will be lengthy

Even if it meets the development schedule, XTI does not expect to deliver certified aircraft until 2022 at the earliest. As a result, the receipt of significant revenues is not anticipated until that time and may occur later than projected. XTI depends on receiving large amounts of capital and other financing to complete its development work, with no assurance that XTI will be successful in completing its development work or becoming profitable.

The company will face significant market competition

The TriFan 600 potentially competes with a variety of aircraft manufactured in the United States and abroad. Further, XTI could face competition from competitors of whom XTI is not aware that have developed or are developing technologies that will offer alternatives to the TriFan 600. Competitors could develop an aircraft that renders the TriFan 600 less competitive than XTI believes it will become. Many existing potential competitors are well-established, have or may have longer-standing relationships with customers and potential business partners, have or may have greater name recognition, and have or may have access to significantly greater financial, technical and marketing resources. Although XTI is unaware of any other manufacturer developing an FAA-certified, light, fixed-wing, civil VTOL aircraft with performance similar to that of the TriFan 600, it is possible that another aircraft manufacturer is doing so in secret.

Delays in aircraft delivery schedules or cancellation of orders may adversely affect the company’s financial results

Once XTI begins its pre-sales program and begins receiving refundable deposits for TriFan 600 aircraft pursuant to its agreements, some or all deposit holders might not transition to non-refundable purchase contracts until prior to aircraft delivery, if at all. Aircraft customers might respond to weak economic conditions by canceling orders, resulting in lower demand for our aircraft and other materials, such as parts, or services, such as training, which the company expects to generate revenue. Such events would have a material adverse effect on XTI’s financial results.

Developing new products and technologies entails significant risks and uncertainties

XTI is currently in the preliminary engineering design phase of the TriFan 600. Delays or cost overruns in the development or certification of the TriFan 600 and failure of the product to meet its performance estimates could affect the company’s financial performance. Delays and increased costs may be caused by unanticipated technological hurdles, changes to design or failure on the part of XTI’s suppliers to deliver components as agreed.

6

Operations could be adversely affected by interruptions of production that are beyond the company’s control

XTI intends to produce the TriFan 600 and its derivatives using systems, components and parts developed and manufactured by third-party suppliers. XTI’s aircraft development and production could be affected by interruptions of production at such suppliers. Such suppliers may be subject to additional risks such as financial problems that limit their ability to conduct their operations. If any of these third parties experience difficulties, it may have a direct negative impact on XTI.

The company will require FAA certification

Certification by the Federal Aviation Administration will be required for the sale of the TriFan 600 in the civil or commercial market in the United States. The process to obtain such certification is expensive and time consuming and has inherent engineering risks. These include (but are not limited to) ground test risks such as structural strength and fatigue resistance, and structural flutter modes. Flight test risks include (but are not limited to) stability and handling over the desired center-of-gravity range, performance extremes (stalls, balked-landing climb, single-engine climb), and flutter control effectiveness (aircraft roll effectiveness, controllability, various control failure safety). Delays in FAA certification might result in XTI incurring increased costs in attempting to correct any issues causing such delays. Also, the impact of new or changed laws or regulations on the TriFan 600’s certification or the costs of complying with such laws and regulations cannot be predicted. Since XTI will not be permitted to deliver commercially produced aircraft to civilian customers until obtaining certification, no significant revenues will be generated from such sales to fund operations prior to certification.

We depend on key personnel

XTI’s future success depends on the efforts of key personnel, including its senior executive team. XTI does not currently carry any key man life insurance on its key personnel or its senior executive team. However, XTI intends to obtain such insurance upon closing this Offering. Regardless of such insurance, the loss of services of any of these or other key personnel may have an adverse effect on XTI. There can be no assurance that XTI will be successful in attracting and retaining the personnel XTI requires to develop and market the proposed TriFan 600 aircraft and conduct XTI’s proposed operations.

The company’s estimates of market demand may be inaccurate

XTI has projected the market for the TriFan 600 based upon a variety of internal and external market data. The estimates involve significant assumptions, which may not be realized in fact. There can be no assurance that XTI’s estimates for the number of TriFan 600 aircraft that may be sold in the market will be as anticipated. In the event that XTI has not accurately estimated the market size for and the number of TriFan 600 aircraft that may be sold, it could have a material adverse effect upon XTI, its results from operations, and an investment in the shares.

7

The company will require intellectual property protection and may be subject to the intellectual property claims of others

Although the company has applied for patents to protect its TriFan 600 technology, the issuance of such patents is up to the US Patent and Trademark Office (USPTO). The company has received one design patent (D741247) for the TriFan 600. However, there is no guarantee that the company will receive one or more of the additional patents for which it has applied. If one or more of such patents are issued and if a third party challenges the validity of the XTI patents or makes a claim of infringement against XTI, the federal courts would determine whether XTI is entitled to patent protection. If XTI fails to successfully enforce its proprietary technology or otherwise maintain the proprietary nature of its intellectual property used in the TriFan 600 aircraft, its competitive position could suffer. Notwithstanding XTI’s efforts to protect its intellectual property, its competitors may independently develop similar or alternative technologies or products that are equal to or superior to XTI’s TriFan 600 technology without infringing on any of XTI’s intellectual property rights or design around our proprietary technologies. There is no guarantee that the USPTO will issue one or more additional patents to XTI or that any court will rule in XTI’s favor in the event of a dispute related to XTI’s intellectual property. In the absence of patent protection, it may be more difficult for XTI to achieve commercial production of the TriFan 600.

There is no current market for the company’s shares

There is no formal marketplace for the resale of XTI’s common stock. The shares may be traded on the over-the-counter market to the extent any demand exists. However, we do not have plans to apply for or otherwise seek trading or quotation of the company’s shares on an over-the-counter market. Investors should assume that they may not be able to liquidate their investment for some time, or be able to pledge their shares as collateral.

3. DILUTION

If you invest in our shares, your interest will be diluted to the extent of the difference between the public offering price per share of our common stock and the as adjusted net tangible book value per share of our capital stock after this Offering. The following table demonstrates the dilution that new investors will experience relative to the company’s net tangible book value as of December 31, 2015 of $(1,359,185). Net tangible book value is the aggregate amount of the company’s tangible assets, less its total liabilities. The table presents three scenarios: a $3 million raise from this Offering, a $10 million raise from this Offering and a fully subscribed $20 million raise from this Offering.

8

| $3MM Raise | $10MM Raise | $20MM Raise | |||||||

| Price per Share | $ | 1.0000 | $ | 1.0000 | $ | 1.0000 | |||

| Shares Issued | 3,000,000 | 10,000,000 | 20,000,000 | ||||||

| Capital Raised | $ | 3,000,000 | $ | 10,000,000 | $ | 20,000,000 | |||

| Less: Offering Costs | $ | (325,865 | ) | $ | (1,117,240 | ) | $ | (2,036,694 | ) |

| Net Offering Proceeds | $ | 2,674,135 | $ | 8,882,760 | $ | 17,963,306 | |||

| Net Tangible Book Value Pre-Financing | $ | (1,359,185 | ) | $ | (1,359,185 | ) | (1,359,185 | ) | |

| Net Tangible Book Value Post-Financing | $ | 1,314,950 | $ | 7,523,575 | $ | 16,604,121 | |||

| Shares Issued and Outstanding Pre-Financing | 35,869,565 | 35,869,565 | 35,869,565 | ||||||

| Post-Financing Shares Issued and Outstanding | 38,869,565 | 45,869,565 | 55,869,565 | ||||||

| Net Tangible Book Value per Share Prior to Offering | $ | (0.0379 | ) | $ | (0.0379 | ) | $ | (0.0379 | ) |

| Increase/(Decrease) per Share Attributable to New Investors | 0.0717 | 0.2019 | 0.3351 | ||||||

| Net Tangible Book Value per Share After Offering | $ | 0.0338 | $ | 0.1640 | $ | 0.2972 | |||

| Dilution to NBV per Share to New Investors | $ | 0.9662 | $ | 0.8360 | $ | 0.7028 |

The following table summarizes the differences between the existing shareholders and the new investors with respect to the number of shares of common stock purchased, the total consideration paid, and the average price per share paid, if the maximum offering price is reached:

Maximum Offering:

| Shares Purchased | Total Consideration | Average Price | |||||||||||||

| Number | Percent | Amount | Percent | Per Share | |||||||||||

| Founders | 35,869,565 | 64.2% | 386,217 | 1.9% | $ | 0.01 | |||||||||

| New Investors | 20,000,000 | 35.8% | 20,000,000 | 98.1% | $ | 1.00 | |||||||||

| Total | 55,869,565 | 100.0% | 20,386,217 | 100.0% | $ | 0.36 | |||||||||

Another important way of looking at dilution is the dilution that happens due to future actions by the company. The investor’s stake in a company could be diluted due to the company issuing additional shares. In other words, when the company issues more shares, the percentage of the company that you own will go down, even though the value of the company may go up. You will own a smaller piece of a larger company. This increase in number of shares outstanding could result from a stock offering (such as an initial public offering, another crowd funding round, a venture capital round, angel investment), employees exercising stock options, or by conversion of certain instruments (e.g. convertible bonds, preferred shares or warrants) into stock.

If the company decides to issue more shares, an investor could experience value dilution, with each share being worth less than before, and control dilution, with the total percentage an investor owns being less than before. The company has authorized and issued only one class or type of shares, common stock. Therefore, all of the company’s current shareholders and the investors in this Offering will experience the same dilution if the company decides to issue more shares in the future.

4. PLAN OF DISTRIBUTION AND SELLING SECURITY HOLDERS

We are offering a maximum of 20,000,000 shares of common stock on a “best efforts” basis. All subscribers will be instructed by the company or its agents to transfer funds by wire or ACH transfer directly to the escrow account established for this Offering or deliver checks made payable to “FundAmerica Securities, LLC, as Agent to XTI Aircraft Company Escrow Account” which FundAmerica Securities LLC shall deposit into such escrow account no later than noon the next business day after receipt. The company may terminate the Offering at any time for any reason at its sole discretion.

9

After the Offering Statement has been re-qualified by the Securities and Exchange Commission, the company will accept tenders of funds to purchase the shares. The company may close on investments in one or more Closings at its discretion by instructing the Escrow Agent to disburse funds. Closings may take place on a “rolling” basis (so not all investors will receive their shares on the same date). The funds tendered by potential investors will be held by the Escrow Agent, and will be transferred to the company upon Closing. Each time the company accepts funds (either transferred from the Escrow Agent or directly from the investors) is defined as a “Closing”. The fact that the company can set one or more Closings at its discretion means that investor funds will be available to it as soon as this Offering is qualified by the Commission. As mentioned earlier and described in greater detail below, the company has engaged FundAmerica Securities, LLC, as escrow agent and the escrow agreement can be found in Exhibit 8 to the Offering Statement of which this Offering Circular is a part.

We are not selling the shares through commissioned sales agents or underwriters. We will use our existing website, www.xtiaircraft.com, to provide notification of the Offering. Persons who desire information will be directed to http's://www.startengine.com/startup/xti, a website owned and operated by an unaffiliated third party that provides technology support to issuers engaging in Regulation A offerings.

The company will pay Start Engine for its services in hosting the Offering of the shares on its online platform. This compensation consists of $50 per investor in cash and $50 per investor in warrants (calculated at the same price paid by such investor), paid (or issued) when such investor deposits funds into escrow. Start Engine does not directly solicit or communicate with investors with respect to offerings posted on its site, although it does advertise the existence of its platform, which may include identifying a broad selection of issuers listed on the platform.

This Offering Circular will be furnished to prospective investors via download 24 hours per day, 7 days per week on the startengine.com website.

The company has entered into a consulting agreement with Mr. David Bovino for the provision of certain marketing, advertising and advisory services in support of the Offering. The agreement contains a payment of $200,000 to Mr. Bovino at the completion of this Offering and the issuance of $50,000 of shares in the company’s common stock valued at the same price as this Offering. Mr. Bovino is not affiliated with the company or its officers and directors in any way.

You will be required to complete a subscription agreement in order to invest. The subscription agreement includes a representation by the investor to the effect that, if you are not an “accredited investor” as defined under securities law, you are investing an amount that does not exceed the greater of 10% of your annual income or 10% of your net worth (excluding your principal residence).

10

We have engaged FundAmerica Securities, LLC (“FundAmerica Securities”), a broker-dealer registered with the Securities and Exchange Commission and a member of the Financial Industry Regulatory Authority (“FINRA”), to perform the following administrative functions in connection with this Offering in addition to acting as the escrow agent:

| • | Advise us as to permitted investment limits for investors pursuant to Regulation A, Tier 2: | |

| • | Communicate with us and/or our agents, if needed, to gather additional information or clarification from investors: | |

| • |

Serve as a registered agent where required for state blue sky requirements, but in no circumstance will FundAmerica Securities solicit a securities transaction, recommend our securities, or provide investment advice to any prospective investor: and | |

| • | Transmit the subscription information data to FundAmerica Securities Transfer LLC, our transfer agent and an affiliate of FundAmerica Securities. |

As compensation for the services listed above, we have agreed to pay FundAmerica Securities $2 per domestic investor for the anti-money laundering check and a facilitation and technology services fee equal to 1.0% of the gross proceeds from the sale of the shares offered hereby. If we elect to terminate the Offering prior to its completion, we have agreed to reimburse FundAmerica Securities for its out-of-pocket expenses incurred in connection with the services provided under this engagement (including costs of counsel and related expenses). In addition, we will pay FundAmerica Securities $225 for account set up, $25 per month for so long as the Offering is being conducted, but in no event longer than two years ($600 in total fees), and up to $15 per investor for processing incoming funds. We will pay FundAmerica Technologies LLC, a technology service provider, $3 for each subscription agreement executed via electronic signature. FundAmerica Securities Transfer LLC, an affiliate of FundAmerica Securities, will serve as transfer agent to maintain stockholder information on a book-entry basis; there are no set up costs for this service, fees for this service will be limited to secondary market activity. If each investor were only to invest the minimum subscription amount of $350 (or 350 shares) per investor, we estimate the maximum fee that could be due to FundAmerica Securities for the aforementioned internal fees would be $1,143,890 if we achieved the maximum offering proceeds. However, the company estimates that it will pay fees totaling $133,520 to FundAmerica Securities if we achieve the maximum offering based on an average subscription amount of $2,000 (or 2,000 shares) per investor. This assumption for the average investment amount was used in estimating the fees due in the “Use of Proceeds to Issuer” below.

FundAmerica Securities, LLC is not participating as an underwriter of the Offering and under no circumstance will it solicit any investment in the company, recommend the company’s securities or provide investment advice to any prospective investor. Rather, FundAmerica Securities involvement in the Offering is limited to acting as an accommodating broker-dealer. Based upon FundAmerica Securities's limited role in this offering, it has not and will not conduct extensive due diligence of this securities Offering and no investor should rely on FundAmerica Securities involvement in this Offering as any basis for a belief that it has done extensive due diligence. FundAmerica Securities, LLC does not expressly or impliedly affirm the completeness or accuracy of the Offering Circular presented to investors by the issuer in this Offering. All inquiries regarding this Offering or services provided by FundAmerica Securities and its affiliates should be made directly to the company.

There are no selling security holders. No officer, director or employee of the company will participate in the sale of securities pursuant to this Offering.

5. USE OF PROCEEDS TO ISSUER

We estimate that, at a per share price of $1.00, the net proceeds from the sale of the 20,000,000 shares in this Offering will be approximately $17,965,000, after deducting the estimated offering expenses of approximately $2,035,000. At the maximum offering, the company estimates it will pay the following fees in cash: between $211,490 and $1,343,890 to FundAmerica depending on how many shares each investor purchases (the company has assumed it will pay $333,520 in the table below), $500,000 to StartEngine and $200,000 to David Bovino.

The calculation of net proceeds reflects payments made to Mr. Brody in his capacity as the holder of a convertible promissory note from the company described in “Interest of Management and Others in Certain Transactions” (the “Brody Note”). We have assumed that Mr. Brody will receive cash payments totalling $1,003,174 if the maximum offering is achieved, representing repayment of the convertible note and payment of the consulting agreement. Mr. Brody will not receive any cash payments for the above agreements if the company does not raise at least $5 million.

The net proceeds of this Offering will be used in four key areas: (i) hiring key members of the management team; (ii) pursuing additional funding; (iii) continuing development of the aircraft; and (iv) expanding sales and marketing to enable the company to take refundable customer deposits.

Accordingly, we expect to use the net proceeds, estimated as discussed above, as follows, if we raise the maximum offering amount:

11

| Maximum Offering | ||||||||

| Amount | Percentage | |||||||

| Engineering | $ | 12,465,000 | 69.4% | |||||

| Fundraising | $ | 1,000,000 | 5.6% | |||||

| Sales & Marketing | $ | 2,500,000 | 13.9% | |||||

| Working Capital (1) | $ | 2,000,000 | 11.1% | |||||

|

Total |

$ | 17,965,000 | 100.0% | |||||

_________________

(1) A portion of working capital will be

used for officers’ salaries.

Because the Offering is being made on a “best-efforts” basis, without a minimum offering amount, we may close the Offering without sufficient funds for all the intended proceeds set out above.

If the Offering size were to be $3 million, the net proceeds will be approximately $2,675,000 after deducting estimated offering expenses of $325,000. The company estimates that it will pay the following fees in cash in that event: between $32,656 and $202,410 to FundAmerica depending on how many shares each investor purchases (the company has assumed it will pay $50,865 for this section), $75,000 to StartEngine and $200,000 to David Bovino.

In the event of an Offering of that size, we expect to use the net proceeds as follows: Approximately $1,175,000 on engineering, approximately $750,000 million on additional fundraising efforts and approximately $750,000 for working capital.

If the Offering were to be less than $3 million, the company plans to use the first approximately $750,000 raised for salaries, travel and the pursuit of additional funding. The next approximately $100,000 would be used to pay vendors. The next approximately $400,000 would be used for engineering expenses and the following approximately $1.5 million would be used for outstanding vendor payments and further engineering.

The foregoing information is an estimate based on our current business plan. We may find it necessary or advisable to re-allocate portions of the net proceeds reserved for one category or another, and we will have broad discretion in doing so. Pending these uses, we intend to invest the net proceeds of this Offering in short-term, interest-bearing securities.

The company reserves the right to change the above use of proceeds if management believes it is in the best interests of the company.

6. DESCRIPTION OF BUSINESS

Background

XTI is an early-stage aircraft

manufacturer that is creating a revolutionary solution for the business aviation

industry. Based in Denver, Colorado, the company’s mission is to develop

innovative solutions to universal business aviation problems by enabling true

point-to-point air travel over long distances. Almost 84% of primary reasons why

organizations use business aircraft are aimed at reducing total trip times or

reaching remote locations not served by scheduled airlines – both dominant

features of the TriFan 600. Our vertical takeoff airplane has unique advantages over existing

private airplanes which still require time-consuming trips to and from a limited

number of airports, and over helicopters which fly at much slower speeds,

significantly shorter distances, and in less comfort than typical business jets.

We are rethinking how people travel by developing an aircraft that combines a

helicopter’s ability to take off and land from almost anywhere, with the speed

and range of a private jet. The TriFan 600 will offer true point-to-point travel

over longer distances --greatly reducing total travel time by departing from or

arriving into locations that are much closer to the customer’s point of

departure and/or destination, including remote locations -- almost eliminating

time spent driving to and from an airport, with the potential of adding back

hours to those whose time is valued by the number of meetings or destinations

they can reach in a single day.

TriFan 600

The TriFan 600 is an airplane with two

turbine jet engines that will have the speed, range and comfort of a business

jet and will takeoff and land vertically like a helicopter. The aircraft will

seat up to six passengers and be capable of cruising at speeds and altitudes of

business jets. Depending on the number of passengers onboard, the TriFan 600 is

expected to be able to fly up to 1,600 miles while taking off and landing

vertically at both ends of the trip.

In designing the TriFan 600, we identified certain goals and guidelines for the performance and capabilities for the airplane, including:

12

| • |

Using a proven fixed-wing airplane configuration, not a helicopter platform, and developing ducted fan technology for vertical take-off and landing. This approach was pursued because we believe that ducted fans are safer and more compact than helicopter rotors and that the aircraft will be able to achieve the speed, range and comfort of a fixed-wing aircraft while being safer and easier to operate. | |

| • |

Creating a sleek luxury aircraft which will seat six people, cruise at around 375 miles an hour, and with a range competitive with light to medium-sized fixed-wing business jets. | |

| • | Minimizing down wash from the fans so the aircraft can land and take off from existing helipads and heliports. | |

| • | Designing the aircraft with sufficient redundancy in the critical components to maximize safety and increase the likelihood of securing FAA certification. | |

| • |

Incorporating advanced technology and materials, including an all-composite carbon-fiber airframe, computer-assisted take-off and landing, and advanced, pilot-friendly safety technologies available to provide a safe, enjoyable flying experience for the pilot and passengers. | |

| • | Designing the aircraft to achieve balance, control, and safety during vertical takeoff and landing and during transitions to and from forward flight. | |

| • | Designing the aircraft’s exterior and interior to be aesthetically appealing and to provide maximum luxury and convenience to the passengers. |

As a result of the advances in materials, computers, engines, and other technologies over the past few decades, combined with our innovative team, we accomplished all of the above objectives in the conceptual design of the TriFan 600 and are now advancing these objectives in preliminary design engineering.

Engineering and Development to Date

XTI expects that

the TriFan 600 will be a fully certified, high performance, civilian fixed-wing

vertical takeoff airplane. We completed initial configuration and engineering

analysis for the TriFan 600 in April 2014, and are currently engaged in

preliminary design, including computational fluid dynamics analysis. We expect

that these development efforts will result in the creation of a flying, 65% subscale

proof of concept aircraft within approximately two years of raising the first $15 million. Thereafter,

XTI will develop a full scale proof of concept aircraft and seek certification with the Federal Aviation Administration (“FAA”),

which we expect will take an additional 7–9 years to complete. If the company is

able to secure FAA certification of the TriFan 600 and completion of all phases

up to and including commercial production, we believe that this aircraft will be

the first civil, FAA-certified vertical takeoff airplane in aviation history.

Management

XTI is guided by a leadership team with

decades of experience, a deep well of expertise in fixed wing and vertical

takeoff and landing aircraft, and a successful track record of bringing new

aircraft to market. XTI has assembled a management team that includes aviation

industry executives and professionals with decades of experience from the

largest fixed wing and rotary wing aircraft companies in the world.

Charlie Johnson, former president and COO of Cessna Aircraft Company, is an

active outside director of the company and the company’s Interim CEO. David Brody, former CEO and Chairman of

AVX Aircraft Company, is Chairman of the board, president and secretary, and the

founder of XTI, and Dr. Dennis Olcott, former Chief Engineer of Adam Aircraft

and the PiperJet, is a board member and XTI’s Senior Vice President of

Engineering and Chief Engineer.

13

The company believes that this management team knows what is required to finance, design, certify and launch a program of this magnitude. This management team brings to XTI decades of sound management experience developing and executing strategic business and aircraft development plans, and technical and financial expertise, in enterprises of various scales in both helicopter and airplane markets. In their roles at Cessna, AVX, Piper, and other companies over the past 30 years, they have each designed, led and championed several new aircraft concepts and programs. Mr. Johnson has managed and overseen approximately 25 FAA certifications during his career at Cessna.

Technology

XTI is not developing basic new

technology; rather, the TriFan 600 is an evolution in the application of existing

technology. Our proprietary patented design and configuration primarily utilizes

advanced technologies, components and systems which are widely in use throughout

the civil aviation industry today. As a result, most of the underlying

technology is well established and understood, which we expect will reduce the

risk associated with manufacturing and certifying the TriFan 600.

Over 50 years ago, the US military funded the development of vertical takeoff and landing airplanes using rotating, ducted fans, much like the TriFan 600. These included the Bell X-22 and the Doak VZ-4, which had fixed wings. Both of these planes were capable of taking off vertically, transitioning to forward flight, and then transitioning to a hover before landing vertically. However, neither of these aircraft went into commercial production because the technology available at the time limited the performance capabilities of the aircraft, making them economically unviable and difficult to operate.

Over the past 50 years, aircraft technologies and materials have advanced significantly. Current engines are dramatically lighter, more fuel-efficient, and provide greater power performance than prior versions. Composite materials are available that allow aircraft structures to be much lighter and stronger than previously. And finally, advances in software technology allow airplanes to be controlled largely by computers, increasing controllability, reliability, and safety. All of these advanced technologies are widely used in today’s civil aviation market. By combining these technologies with our patented proprietary design in a unique and revolutionary configuration, we believe the TriFan 600 will be a commercially successful product for the business aviation market. In other words, the technology of today has caught up with the long-held idea or concept of a vertical takeoff airplane.

The Market

The business aviation market is a global

market that focuses on high net worth individuals and companies as its primary

customer base. These users place a significant premium on the value of their

time and have demonstrated a willingness to pay for the time-saving features

that private aviation can deliver. By avoiding long security lines at commercial

airports and eliminating the need to arrive at least one hour prior to

departure, often combined with the ability to utilize airports or landing strips

that are closer to their ultimate destination, private aircraft users are able

to dramatically reduce the total time of a trip. Business aircraft also offer

individuals the flexibility to determine their own schedule and travel

itinerary.

14

As a result of these time saving and convenience factors, high net worth individuals and businesses purchased an estimated 6,125 aircraft between 2004 and 2013, valued at over $161 billion according to JetNet iQ. This represents an average annual aircraft volume for light, medium and large private aircraft of approximately 612 aircraft deliveries and an annual market value of over $16 billion. JetNet iQ forecasted that this market will grow by roughly 3%-4% per year over the next twenty years.

Total Addressable Market

We expect that existing

owners of business aircraft will be the primary customer for the TriFan 600.

While some individuals and businesses that do not currently own an aircraft will

be interested in a TriFan 600, we have excluded these new owners from our

analysis of the addressable market for conservatism. Among existing owners, a

significant number own both airplanes and helicopters. We will focus our initial

efforts on these dual owners because they have demonstrated a demand for both

vertical lift capabilities and for the speed, range and comfort of a business

jet. Because of the way aircraft are generally owned or titled, the number of

aircraft owned by dual owners is not readily available at this time.

As reflected in the table below, there are currently over 61,000 business airplanes and helicopters in operation worldwide. North America accounts for more than half of the total existing market and annual aircraft deliveries in the world.

| All Jets & | ||||

| Region | Turboprops | Helicopters | Total Aircraft | |

| North America | 20,955 | 12,224 | 33,179 | |

| Rest of World | 11,179 | 16,785 | 27,964 | |

| Total | 32,134 | 29,009 | 61,143 |

Source: AvData, Inc. by ARGUS International, 2014

TriFan 600 addresses primary market driver of reducing total

trip time

The industry’s leading trade organization, National Business

Aviation Association (“NBAA”), often reports that decisions to utilize business

aviation depend on a variety of factors, including the unavailability of

commercial airline service, both at the site of origin and travel destinations;

the number of sites to be visited in a single day; the requirement to move vital

assets rapidly; and a host of other considerations focused on traveler time

savings. (1)As illustrated in the table below, reducing total transportation

time amounts to 84% of reasons for why business aircraft are used. Surveys

conducted by other industry sources, such as Business Jet Traveler magazine,

have similarly reported that the two most important reasons readers cite for why

they choose to fly privately are to save time, and for service to destinations

not served by airlines.

_________________________________

1 Source: 2014

NBAA Business Aviation Fact Book.

15

| Primary Reason for Use | Related to | |||

| of Business Aircraft | Saving Time? | Other | % of Total | |

| Support schedules not met | X | 64% | ||

| with scheduled airlines | ||||

| Reach locations scheduled | X | 19% | ||

| airlines do not serve | ||||

| Make connections with | ||||

| scheduled airline flights | X | 1% | ||

| Industrial or personal | X | 6% | ||

| security reasons | ||||

| Other | X | 10% | ||

| Total | 84% | 16% | 100% |

Source: 2014 NBAA Business Aviation Fact Book.

No traditional airplane or helicopter can fully serve the needs of executive travelers, because neither of them alone or in combination can fly its passengers directly from point A to point B with the same speed, range or operational flexibility as the TriFan 600. With TriFan 600, executive travelers will have the ability to bypass highways and runways, lifting up from any helipad or helipad-sized paved surface, and proceeding directly to their destination, they could potentially save hundreds of hours a year, achieve more, and avoid missing what’s important.

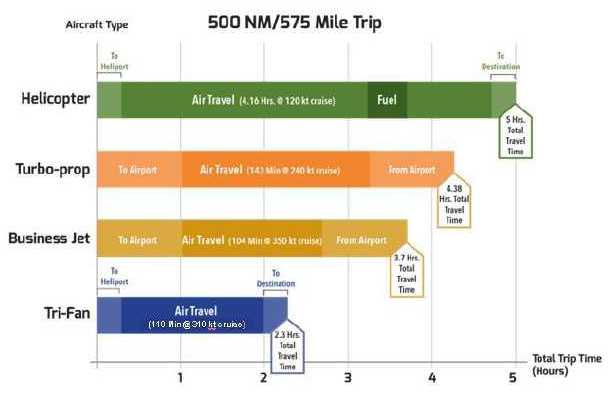

The TriFan 600 will help individuals and business executives reduce total travel time dramatically. The figure below shows how the TriFan 600 can save an executive nearly half his or her total trip time for a 500 nautical mile trip, even compared to a business jet, because of the TriFan 600’s ability to reduce or eliminate time wasted traveling to and from airports. We chose a 500 nautical mile trip as the comparison point because the average trip length for most flights in private aircraft is less than this distance, even if the aircraft is capable of going further without the need to stop to refuel.

16

Sample flight illustrating how TriFan 600 enables shorter trip times

Based on the company’s estimates, TriFan 600will be able to deliver these impressive time savings while still being able to accomplish the vast majority of flight plans flown with private aviation. The table below shows the average flight length flown in private aircraft by class of aircraft. This data was provided by ARGUS International. This clearly illustrates that the TriFan 600 can provide the range capability that most users of private aviation require. While the TriFan 600 won’t be able to accomplish all missions conducted with private aviation, we believe that our ability to cover most requirements while also improving the convenience and time savings of customers will allow us to capture a meaningful share of the existing market of over 60,000 business aircraft.

| Average Trip Length | |

| Aircraft Type | (Nautical Miles) |

| Mid-Sized Jet | 538 |

| Light Jet | 401 |

| Turboprop | 259 |

| Turbine Helicopter | 72 |

| Piston Helicopter | 52 |

| XTI TriFan 600 Range | 825 |

Tri-Fan is priced competitively with what business aircraft

owners are paying

Currently, the only way for individuals using business

aircraft to get from one place to another in a shorter period of time is by

flying in a faster aircraft. Generally, the larger the size of the aircraft, the

faster it can travel, and the more expensive the aircraft. Business jet owners

consistently pay millions of dollars more for increased speed (among other

features). However, as shown in the figure above, more speed does not always

equal more time. True time savings can only be achieved by taking off vertically

like a helicopter, cruising at altitudes and speeds of airplanes, and landing

vertically near a final destination.

17

The TriFan 600 design combines the best aspects of each platform (airplane and helicopter), enabling what the company believes will be a dramatic reduction in total trip time, at a price point that is competitive to market prices. Purchase prices for aircraft in this market can range up to $18 million, with a high correlation between speed and cost. There is a clear connection between the ability to save time through faster transportation and a willingness to pay more for this capability.

| Purchase Price Range ($MM) | ||||||

| Aircraft Type | Low | High | ||||

| Mid-Sized Jet | $ | 12 | $ | 18 | ||

| Light Jet | $ | 4 | $ | 11 | ||

| Turboprop | $ | 2 | $ | 8 | ||

| Turbine Helicopter | $ | 4 | $ | 10 | ||

| Piston Helicopter | $ | 1 | $ | 4 | ||

| TriFan 600 | $ | 10 | $ | 12 | ||

Achievable market share

It is difficult to compare

the TriFan 600 directly to existing aircraft and historical sales levels of

similar aircraft because there is no aircraft with the same performance

capabilities as the TriFan 600. In order to estimate the number of aircraft we

believe we can sell each year, we conducted a market analysis based on the

TriFan 600’s performance characteristics relative to existing alternatives.

To conduct the analysis, we identified the likely objections that buyers of a particular type of aircraft would have when considering the purchase of a TriFan 600. We then estimated what percentage of those buyer segments would object to the TriFan 600 because of each of the considerations (i.e., those that would object because it could not seat enough passengers or because it could not fly a long enough distance, etc.). This resulted in a percentage of each buyer segment that would not object to the TriFan 600 relative to aircraft in that class, leaving the expected portion of each market that we could capture.

With the potential share for each market estimated, we then analyzed market forecast data from Teal Group, an industry leading market forecasting company. This data identified the number of units, by type of aircraft, which are expected to be sold over the next several years. Applying the market share of each aircraft type we expect to capture to the number of aircraft expected to be delivered in each category per year, we estimated that we can expect to sell between 85 – 95 aircraft each year. This analysis only considered sales to civilian users, and does not include military or commercial use forecasts.

After completing our internal analysis, our management team, board of directors, aviation marketing companies and other industry participants all reviewed those findings and provided input as to the reasonableness of the company’conclusion or expectation of selling 85-95 TriFan 600 aircraft each year. Based on the totality of the data and those conversations, we feel that this estimate is achievable. However, for the purpose of creating our business plan, we have assumed a lower more conservative number of annual aircraft deliveries.

18

Production Plan and Suppliers

XTI intends to use a

horizontally integrated manufacturing strategy whereby the company maintains

control of all planning, design and final assembly aspects of the process, but

outsource's the manufacture of the vast majority of components (i.e., fuselage,

engines, transmission, avionics, landing gear, etc.). XTI would only seek to

design and manufacture a limited number of certain critical components, if any.

We intend to utilize the professional networks of our executive team, gained from decades of experience in the industry, to secure favorable supply agreements with leading manufactures. These suppliers will design and fabricate components to XTI’s design specifications for incorporation into a final product. The majority of these components will be largely off-the-shelf systems used in other aircraft, with only limited customization or design features that are specifically required for the TriFan 600.

Under this plan, the company intends to focus its efforts on the most critical components for our success, while enjoying cost savings from using specialists in areas that are not as critical or customized. This will also allow the company to choose between multiple suppliers, reducing any potential dependence on a small set of suppliers.

Research and Development

The company’s primary

activity to date has been to conduct research and development associated with

our core vertical takeoff and landing configuration for the TriFan 600. This

includes the completion of our preliminary design, computational fluid dynamics,

executing our patent and IP strategy, developing additional technical

capabilities and analysis, and other R&D activities to determine the

feasibility of our financial and technical aspects of our aircraft and program.

To date, the company has expended over $1.5 million on engineering, marketing,

legal, and a variety of other G&A.

Employees and Consultants

The company has used and

continues to use a number of consultants during our history to limit our

operating expenses and allow us to scale as necessary. Currently, the company

does not have any full time employees. The company intends to hire a number of

employees after the Offering primarily to support our engineering and

development efforts.

Aviation Regulations

In the U.S., civil aviation is

regulated by the Federal Aviation Administration (the “FAA”), which controls

virtually every aspect of flight from pilot licensing to aircraft design and

construction. The FAA requires that every civilian aircraft that flies in the

U.S. must carry a valid type certificate and airworthiness certificate issued by

the FAA or a foreign civil aviation authority.

The company will seek to obtain approval for the design of the TriFan 600 by obtaining a standard Type Certificate under the Federal Aviation Regulations. The FAA will conduct extensive testing and analysis of the company’s TriFan 600 to determine the safety, stability, reliability and performance of the aircraft and that the aircraft complies with the applicable airworthiness standards for the TriFan 600’s category of airplane. If the TriFan 600 is approved by the FAA, XTI will be issued a type certificate for it.

19

The FAA also issues standard airworthiness certificates to each aircraft that is manufactured in accordance with an approved design or type certificate. Rather than test each aircraft that is built, the FAA allows manufacturers to prove that their manufacturing process and quality control system produces conforming aircraft each time. Only a company that owns a type certificate is entitled to this authorization, called a production certificate. If the FAA approves of XTI’s manufacturing process, the company will be issued a production certificate and each aircraft manufactured by XTI in accordance with the type certificate will receive an airworthiness certificate.

The process of obtaining a valid type certificate, production certificate and airworthiness certificate for the TriFan 600 will take several years. XTI is not permitted to deliver commercially produced aircraft to civilian customers until obtaining FAA certification, which effectively means that no significant revenue will be generated from civilian aircraft sales to fund operations until that time. Any delay in the certification process will negatively impact the company by requiring additional funds to be spent on the certification process and by delaying the company’s ability to sell aircraft.

In addition to the FAA, operation of the TriFan 600 will be regulated by various state, county and municipal agencies. Specifically, flight of the TriFan 600 will be regulated by the FAA, while the ability to takeoff and land will be governed by the FAA and various zoning restrictions imposed by non-federal agencies in each location where an owner of the TriFan 600 intends to operate.These restrictions will vary by location and may limit the TriFan 600 to landing in already zoned areas. However, there are currently over 3,000 helipads in the U.S. where helicopters are already allowed to land. So the company expects that the TriFan 600 will also be able to land legally and safely in these locations and at thousands of smaller general aviation airports unavailable to jets. Unlike jet aircraft, the TriFan 600 is not limited by runway length, clear landing approaches, and the sophistication of the electronic landing aids that serve larger general aviation airports. The TriFan 600 is both VTOL (vertical takeoff and landing) capable and STOL (short takeoff and landing capable). Because it can takeoff and land from any paved general aviation airport –with or without use of a runway -- TriFan 600’s operational versatility makes it uniquely possible to utilize any one of the thousands of smaller airports in the U.S. with runways otherwise unavailable to other business jets. There are also thousands of privately-owned locations in the U.S. and the world (driveways, lots, job sites, and other paved surfaces) that will not all be limited by local regulations. As a result, the company expects there will be sufficient locations for the TriFan 600to takeoff and land.

Intellectual Property

The company’s intellectual

property includes one issued patent (D741247), “utility” patent applications,

copyrights, trademarks and trade secrets. Protection is supported by patent and

copyright laws. Employee and third-party consultants have signed non-disclosure

agreements with the company to further protect its proprietary rights. The

company is continuing to develop intellectual property, and it intends to aggressively protect its position in key

technologies. The company owns several trademarks protecting the company’s name

and logo, as well as extensive data, engineering analyses, and other

intellectual property.

The company’s patent and patent applications cover various embodiments of a vertical take-off and landing aircraft. In general terms, a “utility patent” protects the way an article is used and works, while a “design patent” protects the way an article looks. The company is seeking broad patent protection in both respects.

20

Furthermore, the company is preparing to file one or more foreign patent applications where the aircraft will be sold and widely used. Legal counsel also filed a Patent Cooperation Treaty (“PCT”) application that claims priority back to the filing date for the provisional patent application. The PCT currently covers 141 countries that can be designated for protection, including a European and African patent.

David Brody, founder and Chairman of XTI, developed the TriFan 600 configuration and basic performance objectives, filed for the patents. Dr. Dennis Olcott, XTI’s Senior Vice President for Engineering and Chief Engineer, is co-inventor on certain patent applications. Mr. Brody and Dr. Olcott have assigned all patents, patent applications and other intellectual property to XTI.

Litigation

The company is not involved in any litigation, and its management is not aware of any pending or threatened legal actions relating to its intellectual property, conduct of its business activities, or otherwise.

7. DESCRIPTION OF PROPERTY

The company’s physical property and other physical assets consist of various scale models of the TriFan 600, including a one-third scale model (which includes electric motors and moving parts to demonstrate the TriFan 600 operations), a four-foot wingspan model and many 18-inch wingspan models, as well as some furniture and various physical books and records. No physical or intangible assets of the company are encumbered.

8. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The company was incorporated in October 2009. No operations occurred until the fourth quarter of 2012. Since then we have been engaged primarily in developing the design and engineering concepts for the TriFan 600 and seeking funds from investors to fund that development. We are considered to be a development stage company, since we are devoting substantially all of our efforts to establishing our business and planned principal operations have not commenced. We completed the conceptual engineering report for the TriFan 600 in April 2014 and completed our business model in December 2014.

Operating Results

We have not yet generated any revenues and do not expect to do so until after receiving FAA certification for the TriFan 600. Such certification may not come until 2022 or later.

Year Ended December 31, 2015 Compared to Year Ended December 31, 2014. Operating expenses for the 2015 fiscal year increased by 285% over the 2014 fiscal year, reflecting a significant increase in our activity and efforts to advance the TriFan 600. Conceptual design costs increased from $151,320 to $242,590 (60%) as a result of increased spending on engineering and design work. Marketing costs increased from $69,621 to $391,809 (463%) due to the company’s acceleration of marketing activities in 2015. General and administrative costs increased from $107,319 to $604,641 (463%) primarily as a result of increased legal fees related to preparing the company for future fundraising efforts.

21

Interest expense increased from $3,677 in 2014 to $17,841 in 2015 as a result of the revolver put into place in 2014 and drawn upon in 2015 (discussed below).

As a result, our net loss for the 2015 fiscal year was $1,256,880 as compared to a net loss of $331,937 for the 2014 fiscal year, an increase of 279%. Our accumulated deficit at December 31, 2015 was $1,677,476.

Liquidity and Capital Resources

December 31, 2015. As of December 31, 2015, we had cash of $0 and a working capital deficit of $1,359,185 as compared to cash of $12,618 and a working capital deficit of $356,245 at December 31, 2014. The decrease in working capital was primarily due to the net loss for 2015. Included in the current liabilities is a balance of $860,444 advanced under a convertible note. The convertible note matures at the occurrence of certain fundraising milestones (discussed below).

In 2015, we funded our operations primarily through a revolving loan agreement with our founder, Mr. Brody. This revolver allowed the company to borrow, repay and re borrow up to $750,000 in principal beginning on January 1, 2014. Borrowings under the credit revolver accrued interest at a rate of 3.0% per annum.

In August 2015, the revolving loan agreement was superseded and replaced by a convertible note agreement. The principal amount and accrued but unpaid interest under the revolver were converted into principal in the new convertible note. Mr. Brody is also the lender under this agreement. The convertible note has a principal amount of $763,176 and accrues interest at a rate of 3.0% per annum. The convertible note has different maturity dates contingent upon the company securing different levels of investment from third parties. Mr. Brody has the right to receive repayment of the note upon maturity in either cash or in shares of common stock of the company. The loan with Mr. Brody is more fully described below in “Interest of Management and Others in Certain Transactions” and in Exhibit 6.9 to the Offering Statement of which this Offering Circular forms a part.

22

In September 2015, the company entered into a convertible demand note with Mr. Jeffrey Pino, who recently passed away. The note has a principal amount of $47,268 and bears interest at a rate of 3.0% per annum. In December 2015 the company entered into a further convertible demand note with Mr. Pino in the principal amount of $50,000 at the same interest rate. The notes do not carry a specific maturity date, but Mr. Pino (or his estate) may demand repayment of the notes at any time and has the option to receive repayment of the note in either cash or in shares of common stock of the company. The loans with Mr. Pino are more fully described below in “Interest of Management and Others in Certain Transactions” and in Exhibits 6.10 and 6.11 to the Offering Statement of which this Offering Circular forms a part.

Plan of Operations

The company has developed

a detailed plan to complete its preliminary design phase, hire key members

of its management team, expand sales and marketing efforts and complete

detailed design and development work to support the production of a

flying 65% subscale proof of concept aircraft. It is expected to

take approximately 2.0 years to produce the 65% subscale proof of

concept aircraft and the company will require $15million in total

funding during this period. Once the proof of concept has been

completed and demonstrated, the company will develop and fly a

full scale proof of concept aircraft, seek FAA certification

for the TriFan 600 and begin preparations for production and

manufacturing of the aircraft. The exact time and cost to secure

FAA certification and commence production is not known, but we

estimate that it will take 6 to 8 years and require at least $400

million in additional funding after completion of the 65% subscale

proof of concept. We are now seeking $20 million in funding from

this Regulation A Offering to fund our 2.0 year plan to produce a 65%

subscale flying proof of concept. If we experience any delays in securing

the $15million in total funding necessary to complete our plan of operations,

our timeline will be extended, perhaps materially, depending on the length of the delay.

Upon completion of this Offering, the company will focus its resources in four key areas: (i) hiring key members of its management team; (ii) pursuing additional funding; (iii) continuing development of the aircraft; and (iv) expanding sales and marketing to enable the company to take refundable customer deposits.

We will seek to hire Dennis Olcott as our full time and dedicated Senior VP of Engineering immediately after this Offering. This will be a key milestone for the company. Other key hires will include a permanent CEO, VP of Sales, VP of Supply Chain and an additional VP of Engineering.

We will continue our design and development efforts by engaging key supply partners to assist in the creation of a 65% subscale technology demonstrator. This subscale aircraft will help to identify and solve potential challenges in certain critical path systems of the aircraft including the engines, transmission and fly-by-wire system. Key milestones for this process will include:

| • | Initiate dialogue with vendors of key components of the 65% subscale aircraft | |

| • | Commission and complete trade studies | |

| • | Complete preliminary design of critical path systems | |

| • | Complete and fly 65% subscale aircraft |

We will develop an internal and external sales and marketing capability to increase awareness of the aircraft and position the company to begin taking refundable customer deposits and pre-sales orders. This will be accomplished with the following milestones:

| • | Continue existing sales and marketing efforts | |

| • | Build and fly a 10% subscale airplane | |

| • | Attend and exhibit at one major international trade show | |

| • | Receive refundable, escrowed deposit orders for the TriFan 600 |

We believe that increasing awareness of the aircraft and demonstrating customer demand through orders will enable the company to raise additional capital in the future more easily. The company will not be able to use these refundable, escrowed deposits until near the time of FAA certification when the deposits will become non-refundable.

23

The milestones identified above assume that we are able to raise the full $20 million from this Offering. In that event, the company would expect to accomplish all of the above milestones within the first 24 months. However, we have developed our spending plans in each of these areas to be scalable to the amount of money that we raise in this Offering. As a result, we do not anticipate needing to raise additional funds in the six months after the completion of this Offering. We will need additional capital to complete our development of the proof of concept and beyond as discussed above and are pursuing multiple options for such funding, rather than relying on one source. We believe funding will come from a combination of short-term and long-term sources, including potential industry partners and suppliers.

9. DIRECTORS, EXECUTIVE OFFICERS AND SIGNIFICANT EMPLOYEES

XTI has assembled an experienced management team including aviation industry executives and professionals with decades of experience from the largest fixed wing and rotary wing aircraft companies in the world. Charlie Johnson, former president and COO of Cessna Aircraft Company (from 1997-2003), is an outside director of the company and the current Interim CEO. David Brody, founder and former CEO and Chairman of AVX Aircraft Company (from 2005-2013), is Chairman of the Board, president, secretary, and the founder of XTI. Dennis Olcott, Ph.D., former Chief Engineer of Adam Aircraft (from 2001 – 2006) and at Piper Aircraft (from 2008 - 2009), is a board member and XTI’s Chief Engineer and Senior VP for Engineering.

The table below lists our directors and executive officers, their ages as of December 31, 2015, and the date of their first appointment to such positions. Each position is currently held with an indefinite term of office.

24

| Name | Position | Age | Date of First |

| Appointment | |||

| Executive Officers | |||

| David Brody | Founder, Chairman, | 66 | October, 2009 |

| President and Secretary | |||

| Dennis Olcott | Senior VP for Engineering | 48 | December, 2014 |

| Andrew Woglom | Chief Financial Officer and | 37 | December, 2014 |

| Chief Accounting Officer | |||

| Directors | |||

| David Brody | Director | 66 | October 2009 |

| Charles Johnson | Director | 72 | December, 2014 |

| Dennis Olcott | Director | 47 | December, 2014 |

The company anticipates that Mr. Johnson will assume executive positions within the company after closing the financing under this Offering and will lead the selection, together with the board members, of the individuals for other unfilled executive positions. Mr. Johnson was appointed to the position of Interim CEO by the company’s board following the death of Jeffrey Pino on February 5, 2016.

Executive Officers

David Brody, founder and Chairman of XTI. Mr. Brody has had a life-long passion for aircraft, science and technology. Beginning in 2012, he developed the Tri-Fan configuration and basic performance objectives, organized XTI as a Delaware corporation, and filed for patents. After developing the company’s basic strategic plan, he recruited XTI’s Board members and executive and engineering team to expand, refine, and execute the plan. Mr. Brody was also the founder of an advanced technology helicopter company in 2005 (AVX Aircraft Company), and served as Chairman and CEO of AVX, and remains on the AVX board. He has practiced law in Denver with Hogan Lovells US LLP from January 2013 to the present. Prior to that time he was a partner in Patton Boggs, LLP, another international law firm, for 14 years. He has several patents issued in his name for inventions in aircraft technology and other fields, and has written three books, including a national Book-of-the-Month Club best seller on science and technology, “The Science Class You Wish You Had, The Seven Greatest Scientific Discoveries in History and the People Who Made Them” (Putnam Berkeley, New York 1997, 2nd edition, 2013). The company has not yet determined whether, after the company receives financing under this Offering, Mr. Brody will become a full-time or part-time consultant or employee of the company.

Dr. Dennis Olcott, PhD, PE, Senior Vice President for Engineering and Chief Engineer and Director. Dr. Olcott is an expert on structures, systems definitions, flight test, and FAA certification. He was Chief Engineer at Adam Aircraft from 2001 to 2006, where he led over 100 engineers and technicians covering all phases of aircraft development through certification. At Piper Aircraft he was Vice President of Engineering from 2009 to 2010 and the Chief Engineer on the Piper Jet from 2008 to 2009, and led over 150 Piper engineers supporting production as well as new development projects. In addition to his role at XTI, he is currently (and has been for the past three years) the chief executive of Answer Engineering, Inc., an aerospace engineering consulting company providing engineering services to XTI. After the company receives financing, Mr. Olcott will become a full-time employee of XTI.

25

Andrew Woglom, Chief Financial Officer and Chief Accounting Officer of XTI. Mr. Woglom has diverse experience in investment banking, private equity and operations. From 2009 to 2013, he was Chief Financial Officer for the NEK group of companies (NEK), an international portfolio of businesses spanning aviation, defense contracting, construction, software development start-ups and real estate holdings. He led NEK’s stockholders through a successful exit in 2012. From 2013 to present, Mr. Woglom has worked as a consultant, assisting clients with strategic planning, operational improvements, M&A transactions and capital raising. Prior to NEK, he was a Vice President at Gallagher Industries from 2004 to 2009, a Denver based private equity firm. Before that, from 2000 to 2004, he spent several years in New York in investment banking at both Tri Artisan Partners and at Lehman Brothers. In addition to his role at XTI, he is currently (and has been for the past two years) the principal of Acuity Advisors, LLC, a CFO and advisory services company offering strategic guidance in accounting and finance to clients. After the company receives financing, it is not yet known whether Mr. Woglom will become a full-time or part-time consultant or employee of the company.

Directors