An offering statement pursuant to Regulation A relating to these securities has been filed with the Securities and Exchange Commission. Information contained in this Preliminary Offering Circular is subject to completion or amendment. These securities may not be sold nor may offers to buy be accepted before the offering statement filed with the Commission is qualified. This Preliminary Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy nor may there be any sales of these securities in any state in which such offer, solicitation or sale would be unlawful before registration or qualification under the laws of any such state. We may elect to satisfy our obligation to deliver a Final Offering circular by sending you a notice within two business days after the completion of our sale to you that contains the URL where the Final Offering Circular or the offering statement in which such Final Offering Circular was filed may be obtained.

ViaDerma, Inc.

115,000,000 Shares of Common Stock

This offering is for up to 115,000,000 common shares of ViaDerma, Inc. (“Company,” “VDRM,” “ViaDerma,” “we,” “us,” and “our”) for a price per share of $______________ [$0.01-$0.05], for gross proceeds of up to $5,750,000.00, before deduction of offering expenses, assuming all shares are sold. From the total offering amount, 100,000,000 shares are being offered by the Company for up to $5,000,000 in gross offering proceeds, and 15,000,000 shares are being offered by selling shareholders for up to $750,000 in gross offering proceeds.

The minimum investment established for each investor purchasing from the Company is $10,000.00, unless such minimum is waived by the Company in its sole discretion, which may be done on a case-by-case basis. Selling shareholders will be entitled to keep all proceeds from their sale of shares. There is no minimum offering amount and no provision to escrow or return investor funds if any minimum amount of shares is not sold.

Shares offered by the Company will be sold by our directors and executive officers. We may also elect to engage licensed broker-dealers. No sales agents have yet been engaged to sell shares. Selling shareholder shares will be sold by the selling shareholders directly or through their respective broker-dealers. The Company will not pay for any selling expenses of the selling shareholders. All shares will be offered on a “best-efforts” basis.

The sale of shares will begin once the offering statement to which this circular relates is qualified by the Securities and Exchange Commission (“SEC”) and will terminate one year thereafter or once all offered securities are sold, whichever occurs first. Notwithstanding, the Company may extend the offering by an additional 90 days or terminate the offering at any time.

Our common stock is not now listed on any national securities exchange or the NASDAQ stock market; however, our stock is quoted on OTC Markets Pink marketplace under the trading symbol “VDRM.” There is currently only a limited market for our securities. There is no guarantee that our securities will ever trade on any listed exchange or be quoted on OTCQB or OTQX marketplaces. See “Securities Being Offered” on Page 24 for the rights and privileges associated with our common stock. We qualify as an “emerging growth company” as defined in the Jumpstart our Business Startups Act (“JOBS Act”).

This offering is being made pursuant to Tier 1 of Regulation A following the Offering Circular disclosure format.

| Title of each class of securities to be registered | Amount to be registered [1] | Proposed

maximum offering price per unit | Proposed maximum aggregate offering price | Commissions and Discounts | Proceeds to Company [2] | |||||||||||||||

| Common Stock offered by the Company | 100,000,000 | $ | 0.05 | $ | 5,000,000 | $ | 0 | $ | 5,000,000 | |||||||||||

| Common Stock offered by selling shareholders | 15,000,000 | $ | 0.05 | $ | 750,000 | $ | 0 | $ | 0 | |||||||||||

| (1) | Pursuant to Rule 416 under the Securities Act, the securities being registered hereunder include such indeterminate number of additional shares of common stock as may be issued after the date hereof as a result of stock splits, stock dividends or similar transactions. |

| (2) | There are no underwriting fees or commissions currently associated with this offering; however, the Company may engage sales associates after this offering commences. Nonetheless, the Company expects to spend approximately $23,000 in expenses relating to this offering, including legal, accounting, travel, printing and other misc. expenses. |

We hereby amend this offering circular on such date or dates as may be necessary to delay our effective date until we will file a further amendment which specifically states that this Offering circular shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Offering circular shall become effective on such date as the Commission, acting pursuant to Section 8(a) may determine.

This offering is highly speculative and these securities involve a high degree of risk and should be considered only by persons who can afford the loss of their entire investment. SEE “RISK FACTORS” ON PAGE 6.

THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OF OR GIVE ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SOLICITATION MATERIALS. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION.

4640 Admiralty Way, Suite 500, Marina Del Rey, CA 90292

310-496-5744; http://www.viadermalicensing.com

Offering Circular Date: February 20, 2018

| (1) |

| SUMMARY INFORMATION | 3 | ||

| RISK FACTORS | 7 | ||

| SPECIAL INFORMATION REGARDING FORWARD LOOKING STATEMENTS | 13 | ||

| DILUTION | 14 | ||

| PLAN OF DISTRIBUTION AND SELLING SHAREHOLDERS | 15 | ||

| USE OF PROCEEDS | 18 | ||

| DESCRIPTION OF BUSINESS | 19 | ||

| DESCRIPTION OF PROPERTY | 24 | ||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 25 | ||

| DIRECTORS, EXECUTIVE OFFICERS, AND SIGNIFICANT EMPLOYEES | 29 | ||

| COMPENSATION OF DIRECTORS EXECUTIVE OFFICERS | 30 | ||

| SECURITY OWNERSHIP OF MANAGEMENT AND CERTAIN SHAREHOLDERS | 31 | ||

| INTEREST OF MANAGEMENT AND OTHERS IN CERTAIN TRANSACTION | 32 | ||

| SECURITIES BEING OFFERED | 33 | ||

| DISCLOSURE OF COMMISSION POSITION ON INDEMNIFICATION FOR SECURITIES LIABILITIES | 37 | ||

| FINANCIAL STATEMENTS | 38 | ||

| EXHIBITS | 80 |

| (2) |

SUMMARY INFORMATION

This summary highlights some of the information in this circular. It is not complete and may not contain all of the information that you may want to consider. To understand this offering fully, you should carefully read the entire circular, including the section entitled “Risk Factors,” before making a decision to invest in our securities. Unless otherwise noted or unless the context otherwise requires, the terms “we,” “us,” “our,” the “Company,” and “ViaDerma” refer to ViaDerma, Inc. together with its wholly owned subsidiaries.

The Company

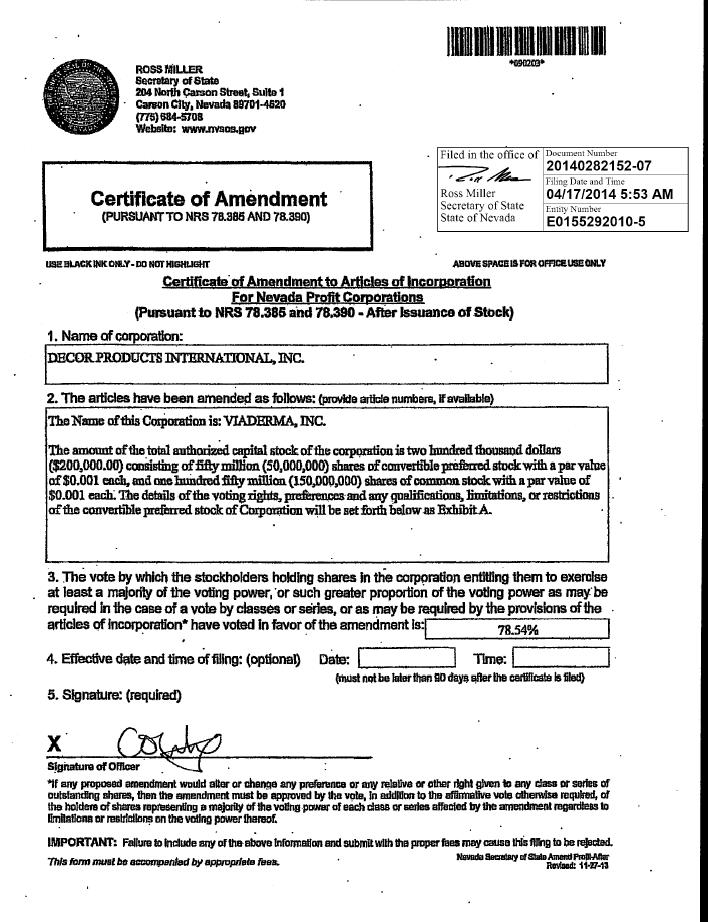

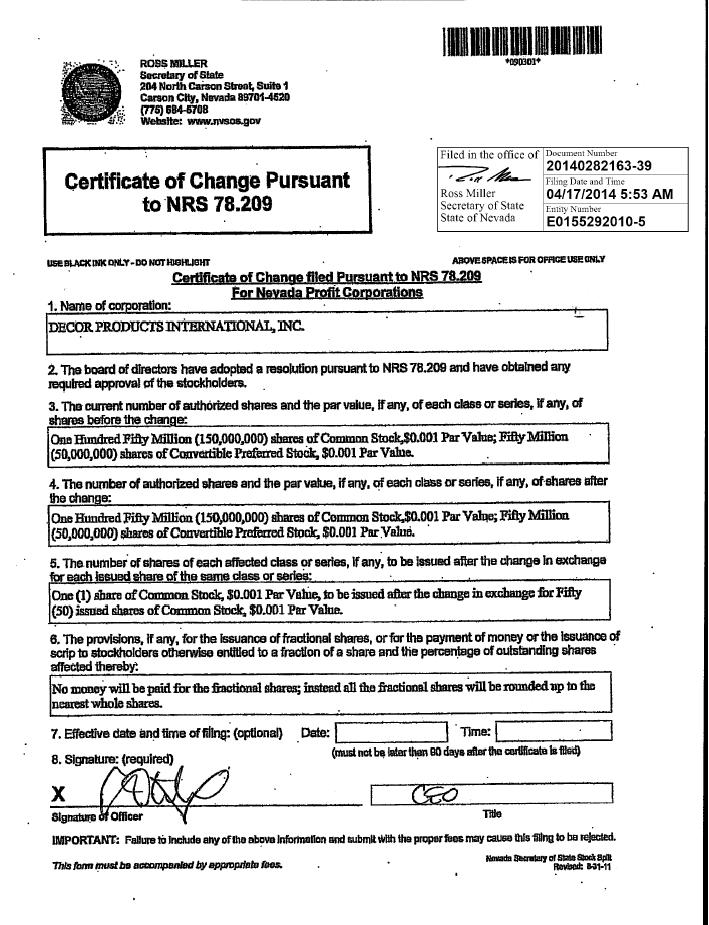

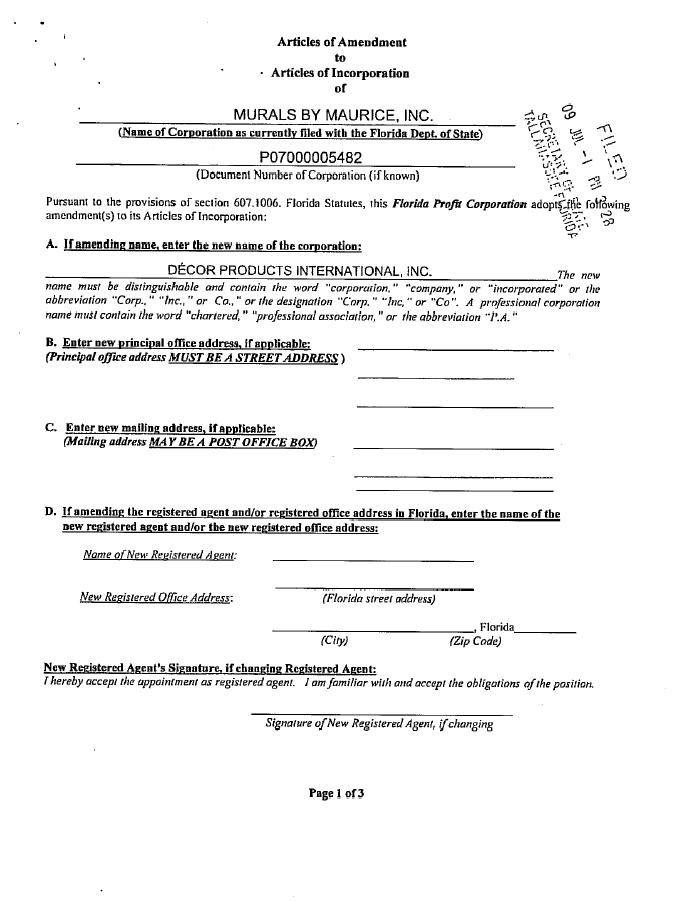

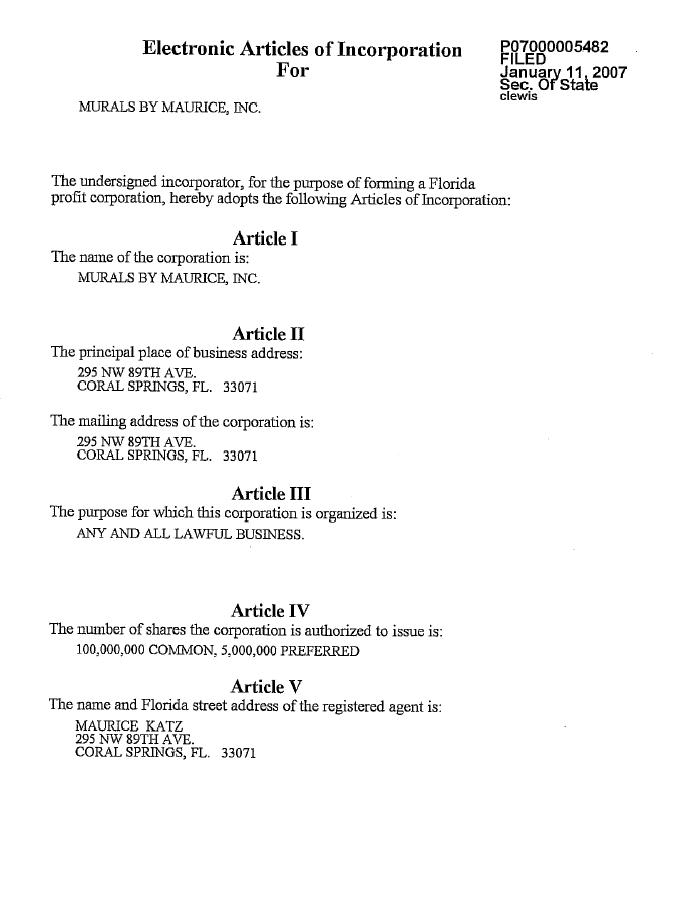

ViaDerma, Inc. was incorporated in the State of Florida on January 11, 2007 in the name of Murals By Maurice, Inc. On July 1, 2009, the Company changed its name to Décor International Products, Inc. On January 20, 2010 the Company filed Articles of Merger with the Secretary of State of Florida to effect a merger with Wide Broad Group, LTD a corporation incorporated in the British Virgin Islands. On May 13, 2010, Décor International Products, Inc. filed articles of merger and redomicile to the State of Nevada with DCRD Merger Sub, Inc. The resulting entity, newly domiciled in Nevada remained Décor Products International, Inc. until May 6, 2014 when it changed its name to ViaDerma, Inc.

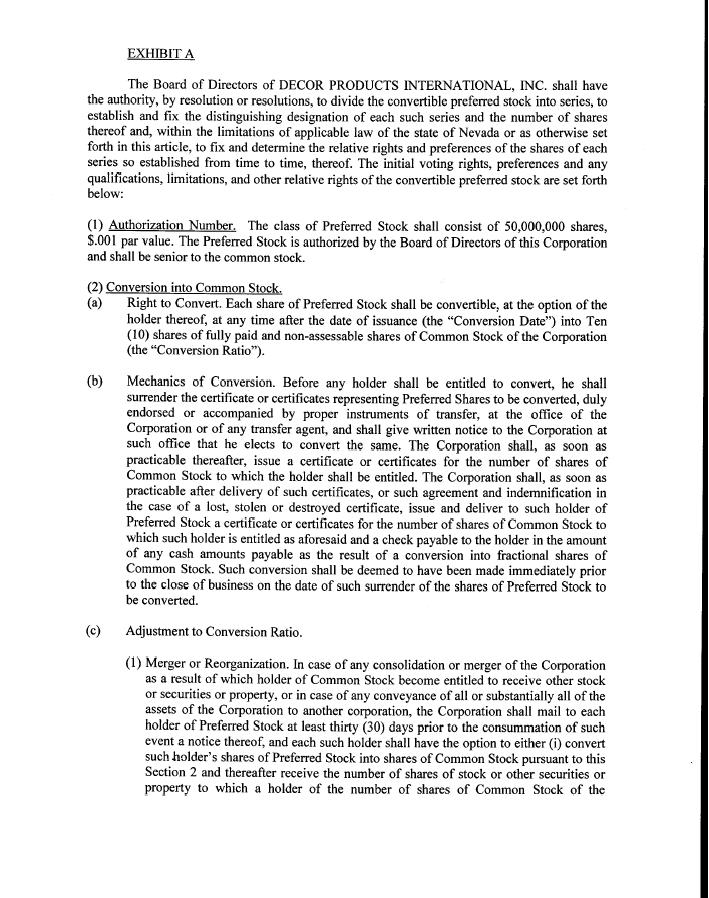

The Company is currently authorized to issue a total of 15,000,000 shares of common stock, par value $0.001, and 50,000,000 shares of Convertible Preferred Stock, par value of $0.001. As of December 29, 2017, the Company had approximately 467,086,221 shares of common stock and 31,000,000 shares of Convertible Preferred Stock outstanding.

Business Overview

ViaDerma, Inc.’s lead product is an FDA registered topical antibiotic called that will be sold under the brand name Vitastem™. The Company also has products in development in the following fields; anti-aging skin care, pain management, hair-loss, and toenail fungus. The products are based on a patent pending delivery system technology that allows for rapid mass transfer of the pharmaceutical active ingredient across the skin and into the body to provide immediate localized therapy. Detailed product information is available online by accessing the Government website, DailyMed.

| (3) |

Emerging Growth Company

We are an emerging growth company under the JOBS Act. We shall continue to be deemed an emerging growth company until the earliest of:

| (a) | the last day of the fiscal year of the issuer during which it had total annual gross revenues of $1,500,000,000 (as such amount is indexed for inflation every five years by the Commission to reflect the change in the Consumer Price Index for All Urban Consumers published by the Bureau of Labor Statistics, setting the threshold to the nearest 1,000,000) or more; | |

| (b) | the last day of the fiscal year of the issuer following the fifth anniversary of the date of the first sale of common equity securities of the issuer pursuant to an effective IPO registration statement; | |

| (c) | the date on which such issuer has, during the previous three-year period, issued more than $1,500,000,000 in nonconvertible debt; or | |

| (d) | the date on which such issuer is deemed to be a ‘large accelerated filer’, as defined in section 240.12b-2 of title 17, Code of Federal Regulations, or any successor thereto.’ |

The Section 107 of the JOBS Act provides that we may elect to utilize the extended transition period for complying with new or revised accounting standards and such election is irrevocable if made. As such, we have made the election to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(1) of the JOBS Act. Please refer to a discussion under “Risk Factors” of the effect on our financial statements of such election.

As an emerging growth company we are exempt from Section 404(b) of Sarbanes Oxley. Section 404(a) requires Issuers to publish information in their annual reports concerning the scope and adequacy of the internal control structure and procedures for financial reporting. This statement shall also assess the effectiveness of such internal controls and procedures. Section 404(b) requires that the registered accounting firm shall, in the same report, attest to and report on the assessment on the effectiveness of the internal control structure and procedures for financial reporting. As an emerging growth company we are also exempt from Section 14A (a) and (b) of the Securities Exchange Act of 1934 which require the shareholder approval of executive compensation and golden parachutes.

We have elected to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(2) of the JOBS Act, that allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result of this election, our financial statements may not be comparable to companies that comply with public company effective dates.

| (4) |

Going Concern

As of September 30, 2017, the Company was in default on the repayment of certain convertible notes and promissory notes with an aggregate principal amount of $266,000, which are immediately due and payable. The continuation of the Company as a going concern through December 31, 2017 is dependent upon the continuing financial support from its stockholders or negotiation of repayment term. Management believes the existing shareholders will provide the additional cash to meet the Company’s obligations as they become due. These factors raise substantial doubt about the Company’s ability to continue as a going concern.

The Offering

This circular relates to the offering of up to 115,000,000 shares of our common stock, of which 100,000,000 shares are being offered by the Company and 15,000,000 shares are being offered by selling shareholders. Shares will be sold for $______________ [$0.01-$0.05] per share, for total offering proceeds of up to $5,750,000 ($5,000,000 to Company and $750,000 to selling shareholders) if all offered shares are sold.

The minimum amount established for investors purchasing from the Company is $10,000, unless such minimum is waived by the Company, in its sole discretion, on a case-by-case basis. Sales by selling shareholders will be privately negotiated or through their respective broker dealers and the selling shareholders will be entitled to keep all proceeds from their sale of shares. There is no minimum offering amount and no provision to escrow or return investor funds if any minimum number of shares is not sold. All funds raised by the Company from this offering will be immediately available for the Company’s use.

Shares offered by the Company will be sold by our directors and executive officers. We may also elect to engage licensed broker-dealers. No sales agents have yet been engaged to sell shares. The Company will not pay for any selling expenses of the selling shareholders. All shares will be offered on a “best-efforts” basis. Investors may be publicly solicited provided the “blue sky” regulations in the states in which the Company solicits investors allow such solicitation.

This offering will terminate at the earlier to occur of: (i) all shares offered hereby are sold, or (ii) one year from the date this offering circular is qualified with the SEC. Notwithstanding the foregoing, the Company may terminate this offering at any time or extend this offering by 90 days, in its sole discretion.

| (5) |

ABOUT THIS CIRCULAR

We have prepared this offering circular to be filed with the SEC for our offering of securities. The offering circular includes exhibits that provide more detailed descriptions of the matters discussed in this circular. You should rely only on the information contained in this circular and its exhibits. We have not authorized any person to provide you with any information different from that contained in this circular. The information contained in this circular is complete and accurate only as of the date of this circular, regardless of the time of delivery of this circular or sale of our shares. This circular contains summaries of certain other documents, but reference is hereby made to the full text of the actual documents for complete information concerning the rights and obligations of the parties thereto. All documents relating to this offering and related documents and agreements, if readily available to us, will be made available to a prospective investor or its representatives upon request.

INDUSTRY AND MARKET DATA

The industry and market data used throughout this circular have been obtained from our own research, surveys or studies conducted by third parties and industry or general publications. Industry publications and surveys generally state that they have obtained information from sources believed to be reliable, but do not guarantee the accuracy and completeness of such information. We believe that each of these studies and publications is reliable. We have not engaged any person or entity to provide us with industry or market data.

TAX CONSIDERATIONS

No information contained herein, nor in any prior, contemporaneous or subsequent communication should be construed by a prospective investor as legal or tax advice. We are not providing any tax advice as to the acquisition, holding or disposition of the securities offered herein. In making an investment decision, investors are strongly encouraged to consult their own tax advisor to determine the U.S. Federal, state and any applicable foreign tax consequences relating to their investment in our securities. This written communication is not intended to be “written advice,” as defined in Circular 230 published by the U.S. Treasury Department.

| (6) |

RISK FACTORS

In addition to the other information provided in this circular, you should carefully consider the following risk factors in evaluating our business and before purchasing any of our common stock. All material risks identified by the Company are discussed in this section.

Risks Related to our Business

Our accountant has indicated doubt about our ability to continue as a going concern.

Our accountant has expressed doubt about our ability to continue as a going concern. Our financial statements do not include adjustments that might result from the outcome of this uncertainty. If we are unable to generate significant revenue or secure financing we may be required to cease or curtail our operations.

We will need a significant amount of capital to carry out our proposed business plan and, unless we are able to raise sufficient funds or generate sufficient revenues, we may be forced to discontinue our operations.

We currently have sufficient capital to carry the Company for approximately 1 month, at which time the Company will require additional capital, either from this offering, revenues or from alternative sources, which alternative sources may include debt or equity financing on more favorable terms than those offered pursuant to this offering statement. Our ability to obtain the necessary financing to execute our business plan is subject to a number of factors, including general market conditions and investor acceptance of our business plan. These factors may make the timing, amount, terms and conditions of such financing unattractive or unavailable to us. If we are unable to raise sufficient funds or generate them through revenues, we will have to significantly reduce our spending, delay or cancel our planned activities or substantially change our current corporate structure. There is no guarantee that we will be able to obtain any funding or that we will have sufficient resources to continue to conduct our operations as projected, any of which could mean that we will be forced to discontinue our operations.

We are currently engaged in a lawsuit over the intellectual property used to deliver our products.

The plaintiff in such lawsuit has alleged that he had a licensing arrangement with Dr. Howard Phillips for some of the patents related to the first-generation transdermal delivery system that were licensed by Dr. Phillips to the Company. The lawsuit further alleges that, through a separate consulting agreement Dr. Chris Otiko had with Thru Pharma, LLC, an entity related to the plaintiff, that Dr. Chris Otiko should need to assign the rights of the transdermal patent to the plaintiff. Should the plaintiff be successful in his suit, it could materially, negatively impact the Company and its manufacture and sale of its products.

We may incur substantial costs as a result of litigation or other proceedings relating to patent and other intellectual property rights.

A third party may sue us or one of our strategic collaborators for infringing its intellectual property rights. Likewise, we may need to resort to litigation to enforce licensed rights or to determine the scope and validity of third-party intellectual property rights.

The cost to us of any litigation or other proceeding relating to intellectual property rights, even if resolved in our favor, could be substantial, and the litigation would divert our efforts. Some of our competitors may be able to sustain the costs of complex patent litigation more effectively than we can because they have substantially greater resources. If we do not prevail in this type of litigation, we or our strategic collaborators may be required to pay monetary damages; stop commercial activities relating to the affected products or services; obtain a license in order to continue manufacturing or marketing the affected products or services; or attempt to compete in the market with a substantially similar product.

| (7) |

Uncertainties resulting from the initiation and continuation of any litigation could limit our ability to continue some of our operations. In addition, a court may require that we pay expenses or damages, and litigation could disrupt our commercial activities.

Any inability to protect our intellectual property rights could reduce the value of our technologies and brand, which could adversely affect our financial condition, results of operations and business.

Our business is partly dependent upon our licensed patents, trademarks, trade secrets, copyrights and other intellectual property rights. Effective intellectual property rights protection, however, may not be available under the laws of every country in which we and our sub-licensees may operate. There is a risk of certain valuable trade secrets, beyond what is described publicly in patents, being exposed to potential infringers. Regardless of the Company’s technology being protected by patents or otherwise, there is a risk that other companies may employ the technology without authorization and without recompensing us.

The efforts we have taken to protect our proprietary rights may not be sufficient or effective. Any significant impairment of our intellectual property rights could harm our business or our ability to compete. In addition, protecting our intellectual property rights is costly and time consuming. There is a risk that we may have insufficient resources to counter adequately such infringements through negotiation or the use of legal remedies. It may not be practicable or cost effective for us to fully protect our intellectual property rights in some countries or jurisdictions. If we are unable to successfully identify and stop unauthorized use of our intellectual property, we could lose potential revenue and experience increased operational and enforcement costs, which could adversely affect our financial condition, results of operations and business.

The intellectual property behind our technology may include unpublished know-how as well as existing and pending patent protection. All patent protection eventually expires, and unpublished know-how is dependent on key individuals.

The commercialization of our technology is partially dependent upon know-how and trade secrets held by certain individuals working with and for us. Because the expertise runs deep in these few individuals, if something were to happen to any or all of them, the ability to properly operate our technologies without compromising quality and performance could be diminished greatly.

Knowledge published in the form of patents has finite protection, as all patents have a limited life and an expiration date. While continuous efforts will be made to apply for additional patents if appropriate, there is no guarantee that additional patents will be granted. The expiration of patents relating to our technology may hinder our ability to sub-license or sell the technology for a long period of time without the development of a more complex licensing strategy.

Our potential for rapid growth and our entry into new markets make it difficult for us to evaluate our current and future business prospects, and we may be unable to effectively manage any growth associated with these new markets, which may increase the risk of your investment and could harm our business, financial condition, results of operations and cash flow.

Our proliferation into new markets may place a significant strain on our resources and increase demands on our executive management, personnel and systems, and our operational, administrative and financial resources may be inadequate. We may also not be able to effectively manage any expanded operations, or achieve planned growth on a timely or profitable basis, particularly if the number of customers using our technology significantly increases or their demands and needs change as our business expands. If we are unable to manage expanded operations effectively, we may experience operating inefficiencies, the quality of our products and services could deteriorate, and our business and results of operations could be materially adversely affected.

If we are unable to keep up with rapid technological changes, our processes, products or services may become obsolete.

The market for our technologies is characterized by significant and rapid change. Although we will continue to expand our technological capabilities in order to remain competitive, research and discoveries by others may make our processes, products or services less attractive or even obsolete.

| (8) |

Competition could adversely affect our business.

Our industry in general is competitive. It is possible that future competitors could enter our market, thereby causing us to move market share and revenues. Further, we are aware of several competitors, each with more resources and market share than us. In addition, some of our current or future competitors may have significantly greater financial, technical, marketing and other resources than we do or may have more experience or advantages in the markets in which we will compete that will allow them to offer lower prices or higher quality technologies, products or services. If we do not successfully compete with these providers, we could fail to develop market share and our future business prospects could be adversely affected.

If we are unable to develop and maintain our brand and reputation for our product offerings, our business and prospects could be materially harmed.

Our business and prospects depend, in part, on developing and then maintaining and strengthening our brand and reputation in the markets we serve. If problems with our technologies cause end users to experience operational disruption or failure or delays in the delivery of their products and services to their customers, our brand and reputation could be diminished. If we fail to develop, promote and maintain our brand and reputation successfully, our business and prospects could be materially harmed.

The development of new products by us involves considerable costs and any new product may not generate sufficient consumer interest and sales to become a profitable brand or to cover the costs of its development and subsequent promotions

We are subject to government regulation, and unfavorable changes could substantially harm our business and results of operations.

We are subject to general business regulations and laws as well as regulations and laws specifically governing our industries in the U.S. and other countries in which we operate. Existing and future laws and regulations may impede our services and increase the cost of providing such services. These regulations and laws may cover taxation, tariffs, user pricing, distribution, consumer protection and the characteristics and quality of services.

General economic conditions could affect our profitability.

A general economic downturn or sudden disruption in business conditions may affect consumer purchases of discretionary items and/or the financial strength of our customers that are retailers, which could adversely affect our financial results

The Company could be effected by a change in the availability of the components used to make its products.

In the event of a significant disruption in the supply of the materials used in the manufacture of our products, we might not be able to locate alternative suppliers of materials of comparable quality at an acceptable price.

We may be subject to product liability claims if people or properties are harmed by the products we sell.

Claims, recalls or actions could be based on allegations that, among other things, the products sold by us are misbranded, contain contaminants or impermissible ingredients, provide inadequate instructions regarding their use or misuse, or include inadequate warnings concerning flammability or interactions with other substances. A significant product liability judgment or a widespread product recall may negatively impact on sales and profitability of the affected brand or all brands for a period of time depending on product availability, competitive reaction and consumer attitudes.

We may be subject to federal regulation, prosecution and civil forfeiture as a result of our CBD infused products.

Cannabis and cannabis derivatives illegal under federal law pursuant to the Controlled Substances Act, as amended (“CSA”). Our CBD is derived from industrial hemp. It is unclear under current federal law to what extent CBD products derived from industrial hemp are subject to the CSA. Any federal enforcement against the Company could materially negatively impact its operations and revenues. The Company intends to limit its sale of CBD products to states in which such activity is legal.

Risks Related to this Offering and Our Securities

The offering price of our shares has been arbitrarily determined.

Our management has determined the shares offered by the Company. The price of the shares we are offering was arbitrarily determined based upon the current market value, illiquidity and volatility of our common stock, our current financial condition and the prospects for our future cash flows and earnings, and market and economic conditions at the time of the offering. The offering price for the common stock sold in this offering may be more or less than the fair market value for our common stock.

| (9) |

We may not register or qualify our securities with any state agency pursuant to blue sky regulations.

The holders of our shares of common stock and persons who desire to purchase them in the future should be aware that there may be significant state law restrictions upon the ability of investors to resell our shares. We currently do not intend to and may not be able to qualify securities for resale in states which require shares to be qualified before they can be resold by our shareholders.

We have broad discretion in the use of the net proceeds from this offering and may not use them effectively.

Our management will have broad discretion in the application of the net proceeds and may spend or invest these proceeds in a way with which our stockholders disagree. The failure by our management to apply these funds effectively could harm our business and financial condition. Pending their use, we may invest the net proceeds from this offering in a manner that does not produce income or that loses value.

Investors may have difficulty in reselling their shares due to the lack of market.

Our common stock is not currently traded on any exchange, but is quoted on OTC Markets Pink marketplace under the trading symbol “VDRM.” There is a limited trading market for our common stock. There is no guarantee that any significant market for our securities will ever develop. Further, the state securities laws may make it difficult or impossible to resell our shares in certain states. Accordingly, our securities should be considered highly illiquid.

We will be subject to penny stock regulations and restrictions and you may have difficulty selling shares of our common stock.

The SEC has adopted regulations which generally define so-called “penny stocks” to be an equity security that has a market price less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exemptions. Our common stock is a “penny stock”, and we are subject to Rule 15g-9 under the Exchange Act, or the “Penny Stock Rule”. This rule imposes additional sales practice requirements on broker-dealers that sell such securities to persons other than established customers. For transactions covered by Rule 15g-9, a broker-dealer must make a special suitability determination for the purchaser and have received the purchaser’s written consent to the transaction prior to sale. As a result, this rule may affect the ability of broker-dealers to sell our securities and may affect the ability of purchasers to sell any of our securities in the secondary market.

For any transaction involving a penny stock, unless exempt, the rules require delivery, prior to any transaction in a penny stock, of a disclosure schedule prepared by the SEC relating to the penny stock market. Disclosure is also required to be made about sales commissions payable to both the broker-dealer and the registered representative and current quotations for the securities. Finally, monthly statements are required to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stock.

We do not anticipate that our common stock will qualify for exemption from the Penny Stock Rule. In any event, even if our common stock were exempt from the Penny Stock Rule, we would remain subject to Section 15(b)(6) of the Exchange Act, which gives the SEC the authority to restrict any person from participating in a distribution of penny stock, if the SEC finds that such a restriction would be in the public interest.

We are an “emerging growth company,” and we cannot be certain if the reduced reporting requirements applicable to emerging growth companies will make our common stock less attractive to investors.

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act, or the JOBS Act. The Section 107 of the JOBS Act provides that we may elect to utilize the extended transition period for complying with new or revised accounting standards and such election is irrevocable if made. As such, we have made the election to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(1) of the JOBS Act.

| (10) |

As an emerging growth company we are exempt from Section 404(b) of Sarbanes Oxley. Section 404(a) requires Issuers to publish information in their annual reports concerning the scope and adequacy of the internal control structure and procedures for financial reporting. This statement shall also assess the effectiveness of such internal controls and procedures. Section 404(b) requires that the registered accounting firm shall, in the same report, attest to and report on the assessment on the effectiveness of the internal control structure and procedures for financial reporting. As an emerging growth company we are also exempt from Section 14A (a) and (b) of the Securities Exchange Act of 1934 which require the shareholder approval of executive compensation and golden parachutes.

We have elected to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(2) of the JOBS Act, that allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result of this election, our financial statements may not be comparable to companies that comply with public company effective dates.

If securities or industry analysts publish inaccurate or unfavorable research about our business, our stock price could decline.

The trading market for our common stock will depend in part on the research and reports that securities or industry analysts publish about us or our business. If one or more of the analysts who cover us downgrade our common stock or publish inaccurate or unfavorable research about our business, our common stock price would likely decline.

We do not intend to pay dividends for the foreseeable future.

We currently intend to retain any future earnings to finance the operation and expansion of our business, and we do not expect to declare or pay any dividends on our common stock in the foreseeable future.

The market price for our common stock is volatile, which could lead to wide fluctuations in our share price.

Our stock price is particularly volatile when compared to the shares of larger, more established companies that trade on a national securities exchange and have large public floats. The volatility in our share price is attributable to a number of factors. First, our common stock is sporadically and thinly traded. As a consequence of this limited liquidity, the trading of relatively small quantities of shares by our shareholders may disproportionately influence the price of those shares in either direction. The price for our shares could decline precipitously in the event that a large number of our common stock is sold on the market without commensurate demand. Secondly, we are a speculative or “risky” investment due to our limited operating history and lack of significant profits to date, and uncertainty of future market acceptance for our products. Many of these factors are beyond our control and may decrease the market price of our common stock, regardless of our operating performance. We cannot make any predictions or projections as to what the prevailing market price for our common stock will be at any time. Moreover, the OTC Pink marketplace is not a liquid market in contrast to the major stock exchanges. Consequently, you may be unable to sell your common stock at or above your purchase price, which may result in substantial losses to you.

Purchasers of our common stock may experience immediate dilution and/or future dilution.

Our Board of Directors has the authority to cause us to issue additional shares of common stock without consent of any of our stockholders and there are shares of preferred stock that may be converted to common stock. Consequently, the common stockholders may experience dilution in their ownership of our stock in the future and as a result of this offering.

Risks Related to Management and Personnel

We depend heavily on key personnel, and turnover of key senior management could harm our business.

Our future business and results of operations depend in significant part upon the continued contributions of our senior management personnel. If we lose their services or if they fail to perform in their current positions, or if we are not able to attract and retain skilled personnel as needed, our business could suffer. Significant turnover in our senior management could significantly deplete our institutional knowledge held by our existing senior management team. We depend on the skills and abilities of these key personnel in managing the product acquisition, marketing and sales aspects of our business, any part of which could be harmed by turnover in the future. We may not have written employment agreements with all of our senior management. We do not have any key person insurance.

| (11) |

Our management has limited experience in managing the day to day operations of a public company and, as a result, we may incur additional expenses associated with the management of our Company.

The management team is responsible for the operations and reporting of the Company. The requirements of operating as a small public company are many and sometimes difficult to navigate. This may require us to obtain outside assistance from legal, accounting, investor relations, or other professionals that could be more costly than planned. If we lack cash resources to cover these costs of being a public company in the future, our failure to comply with reporting requirements and other provisions of securities laws could negatively affect our stock price and adversely affect our potential results of operations, cash flow and financial condition after we commence operations.

Because we do not have an audit or compensation committee, shareholders will have to rely on the entire board of directors to perform these functions.

We do not have an audit or compensation committee and these functions are performed by the board of directors as a whole. Thus, there is a potential conflict in that board members who are also part of management will participate in discussions concerning management compensation and audit issues that may affect management decisions.

Certain of our stockholders hold a significant percentage of our outstanding voting securities, which could reduce the ability of minority shareholders to effect certain corporate actions.

Our sole officers and directors are the beneficial owners of a majority of our outstanding voting securities. As a result, they possess significant influence over Company elections and votes. As a result, their ownership and control may have the effect of facilitating and expediting a future change in control, merger, consolidation, takeover or other business combination, or encouraging a potential acquirer to make a tender offer. Their ownership and control may also have the effect of delaying, impeding, or preventing a future change in control, merger, consolidation, takeover or other business combination, or discouraging a potential acquirer from making a tender offer.

| (12) |

SPECIAL INFORMATION REGARDING FORWARD LOOKING STATEMENTS

Some of the statements in this circular are “forward-looking statements.” These forward-looking statements involve certain known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by these forward-looking statements. These factors include, among others, the factors set forth above under “Risk Factors.” The words “believe,” “expect,” “anticipate,” “intend,” “plan,” and similar expressions identify forward-looking statements. Forward-looking statements contained in this Memorandum include, but are not limited to, statements about:

| • | risks and uncertainties associated with our research and development activities; |

| • | the timing or likelihood of regulatory filing and approvals or of alternative regulatory pathways for our products; |

| • | the potential market opportunities for commercializing our products; |

| • | our expectations regarding the potential market size and the size of the consumer populations for our products, and our ability to serve such markets; |

| • | estimates of our expenses, future revenue, capital requirements and our needs for additional financing; |

| • | the implementation of our business model and strategic plans for our business and products; |

| • | the initiation, cost, timing, progress and results of future research and development programs; |

| • | the terms of future licensing arrangements, and whether we can enter into such arrangements at all; |

| • | timing and receipt of revenues, if any; |

| • | the scope of protection we are able to establish and maintain for intellectual property rights covering our products and our ability to operate our business without infringing the intellectual property rights of others; |

| • | regulatory developments in the United States; |

| • | the performance of our third party suppliers and manufacturers; |

| • | our ability to maintain and establish collaborations or obtain additional funding; |

| • | the success of competing therapies that are currently or may become available; |

| • | our use of proceeds from this offering; |

| • | our financial performance; and |

| • | developments and projections relating to our competitors and our industry. |

We caution you that the forward-looking statements highlighted above do not encompass all of the forward-looking statements made in this circular. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties, and other factors described in the section of this circular entitled “Risk Factors” and elsewhere in this circular. Moreover, we operate in a very competitive and challenging environment. New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this circular. We cannot assure you that the results, events and circumstances reflected in the forward-looking statements will be achieved or occur, and actual results, events or circumstances could differ materially from those described in the forward-looking statements.

We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures, other strategic transactions or investments we may make.

We undertake no obligation to update and revise any forward-looking statements or to publicly announce the result of any revisions to any of the forward-looking statements in this document to reflect any future or developments. However, the Private Securities Litigation Reform Act of 1995 is not available to us as a non-reporting issuer. Further, Section 27A(b)(2)(D) of the Securities Act and Section 21E(b)(2)(D) of the Securities Exchange Act expressly state that the safe harbor for forward looking statements does not apply to statements made in connection with an initial public offering.

| (13) |

DILUTION

Investors in this offering will experience immediate dilution, as exampled below, from the sale of shares by the Company. If you invest in our shares, your interest will be diluted to the extent of the difference between the public offering price per share of our common stock and the as adjusted net tangible book value per share of our capital stock after this offering. Net tangible book value per share represents our total tangible assets less total liabilities, divided by the number of shares of common stock outstanding. Net tangible book value dilution per share of common stock to new investors represents the difference between the amount per share paid by purchasers in this offering and the as adjusted net tangible book value per share of common stock immediately after completion of this offering.

As of September 30, 2017, our net tangible book value was estimated at approximately $408,028, or approximately $0.00096869 per share. After giving effect to our sale of the maximum offering amount of 5,000,000 in securities, assuming no other changes since September 30, 2017, our as-adjusted net tangible book value would be approximately $5,408,028, or $0.0104 per share. At an assumed offering price of $0.05 per share, this represents an immediate decrease in net tangible book value of $0. 0396 per share to investors of this offering, as illustrated in the following table:

| Public offering price per share | $ | 0.05 | ||||||

| Net tangible book value per share | $ | 0.00096869 | ||||||

| Change in net tangible book value per share attributable to new investors | $ | 0.009 | ||||||

| Adjusted net tangible book value per share | $ | 0.0104 | ||||||

| Dilution to new investors in this offering | $ | 0.0396 |

The above calculations are based on 421,214,603 common shares issued and outstanding as of September 30, 2017 before adjustments and 521,214,603 common shares outstanding after adjustment, assuming the Company sells all 100,000,000 of its offered shares without additional shares issued, assets acquired or liabilities incurred, which assumption is made for purposes of the above calculations only.

| (14) |

PLAN OF DISTRIBUTION AND SELLING SHAREHOLDERS

We are offering up to 100,000,000 shares of our common stock at a price of $______________ [$0.01-$0.05] per share, for total offering proceeds of up to $5,000,000 if all offered shares are sold. The minimum amount established for investors is $10,000, unless such minimum is waived by the Company, in its sole discretion, on a case-by-case basis.

There is no minimum offering amount or provision to escrow or return investor funds if any minimum number of shares is not sold, and we may sell significantly fewer shares of common stock than those offered hereby. In fact, there can be no assurances that the Company will sell any or all of the offered shares. All funds received from the Company will be immediately available for its use.

Upon this circular being qualified by the SEC, the Company may offer and sell shares from time to time until all of the shares registered are sold; however, this offering will terminate one year from the initial qualification date of this circular, unless extended or terminated by the Company. The Company may terminate this offering at any time and may also extend the offering term by 90 days.

Currently, we plan to have our directors and executive officers and directors sell the shares offered hereby on a self-underwritten basis. They will receive no discounts or commissions. Our executive officers will deliver this circular to those persons who they believe might have interest in purchasing all or a part of this offering. The Company may generally solicit investors; however, it must abide by the “blue sky” regulations relating to investor solicitation in the states where it will solicit investors. All shares will be sold on a “best efforts” basis.

Our directors and officers will not register as broker-dealers under Section 15 of the Securities Exchange Act of 1934 in reliance upon Rule 3a4-1. Rule 3a4-1 sets forth those conditions under which a person associated with an issuer may participate in the offering of the issuer’s securities and not be deemed to be a broker-dealer. The conditions are that:

| | the person is not statutorily disqualified, as that term is defined in Section 3(a)(39) of the Act, at the time of his participation; and |

| | the person is not at the time of their participation an associated person of a broker-dealer; and |

| | the person meets the conditions of paragraph (a)(4)(ii) of Rule 3a4-1 of the Exchange Act, in that he (i) primarily performs, or is intended primarily to perform at the end of the offering, substantial duties for or on behalf of the issuer otherwise than in connection with transactions in securities; and (ii) is not a broker or dealer, or an associated person of a broker or dealer, within the preceding 12 months; and (iii) does not participate in selling and offering of securities for any issuer more than once every 12 months other than in reliance on paragraphs (a)(4)(i) or (a)(4)(iii) of Rule 3a4-1 of the Exchange Act. |

Our officers and directors are not statutorily disqualified, are not being compensated, and are not associated with a broker-dealer. They are and will continue to hold their positions as officers or directors following the completion of the offering and have not been during the past 12 months and are currently not brokers or dealers or associated with brokers or dealers. They have not nor will they participate in the sale of securities of any issuer more than once every 12 months.

As of the date of this circular, we have not entered into any arrangements with any selling agents for the sale of the securities; however, we may engage one or more selling agents to sell the securities in the future. If we elect to do so, we will supplement this circular as appropriate.

In various states, the securities may not be sold unless these securities have been registered or qualified for sale in such state or an exemption from registration or qualification is available and is complied with. We have not yet applied for “blue sky” registration in any state, and there can be no assurance that we will be able to apply, or that our application will be approved and our securities will be registered, in any state in the US. We intend to sell the shares only in the states in which this offering has been qualified or an exemption from the registration requirements is available, and purchases of shares may be made only in those states.

All subscription agreements and checks received by the Company for the purchase of shares are irrevocable until accepted or rejected by the Company and should be delivered to the Company as provided in the subscription agreement. A subscription agreement executed by a subscriber is not binding on the Company until it is accepted on our behalf by the Company’s CEO or by specific resolution of our Board of Directors. Any subscription not accepted within 30 days will be automatically deemed rejected. Once accepted, the Company will deliver a stock certificate to a purchaser within five days from request by the purchaser; otherwise purchasers’ shares will be noted and held on the book records of the Company.

| (15) |

Selling Shareholders

The persons and entities named below are the “selling shareholders.” The table assumes that all of the securities will be sold in this offering. However, any or all of the securities listed below may be retained by any of the selling shareholders, and therefore, no accurate forecast can be made as to the number of securities that will be held by the selling shareholders upon termination of this offering.

Selling shareholders are offering up to 15,000,000 shares of common stock at a price of $______________ [$0.01-$0.05] per share, for total offering proceeds of up to $750,000 if all offered shares are sold. We will not receive proceeds from the sale of shares from the selling shareholders.

Selling shareholders in this offering may be considered underwriters, as that term is defined in Section 2(a)(11) of the Securities Act. We are not aware of any underwriting arrangements that have been entered into by the selling shareholders. The distribution of the securities by the selling shareholders may be effected in one or more transactions that may take place in the OTC Markets, including broker's transactions or privately negotiated transactions.

The selling shareholders may pledge all or a portion of the securities owned as collateral for margin accounts or in loan transactions, and the securities may be resold pursuant to the terms of such pledges, margin accounts or loan transactions. Upon default by such selling shareholders, the pledge in such loan transaction would have the same rights of sale as the selling shareholders under this circular. The selling shareholders may also enter into exchange traded listed option transactions, which require the delivery of the securities listed under this circular. The selling shareholders may also transfer securities owned in other ways not involving market makers or established trading markets, including directly by gift, distribution, or other transfer without consideration, and upon any such transfer the transferee would have the same rights of sale as such selling shareholders under this circular.

Each of the selling shareholders will be affected by the applicable provisions of the Securities Exchange Act of 1934, including, without limitation, Regulation M, which may limit the timing of purchases and sales of any of the securities held by the selling shareholders or any such other person. We have instructed our selling shareholders that they may not purchase any of our securities while they are selling shares under this offering statement.

We will not pay for any expenses relating to the sale of shares by the selling shareholders except the fee for this offering statement, edgarizing and other expenses related to filing this offering statement.

Except as noted, we believe that the selling shareholders holders listed in the table have sole voting and investment powers with respect to the securities indicated. The selling shareholders each have an agreement with the Company to register their shares in consideration for bridge financing previously provided by the selling shareholders. We will not receive any proceeds from the sale of the securities by the selling shareholders. None of our selling shareholders is, or is affiliated with, a broker-dealer.

| Selling Shareholder | Holdings of Selling Shareholder Prior to Offering [1] | Percent of Outstanding Stock Held by Selling Shareholder [2] | Securities Being Offered by Selling Shareholder [3] | Holdings of Selling Shareholder After Offering |

| The Thomas Group LLC [4] | 136,500 | 0.13% | 15,000,000 | 0 |

| Selling shareholders as a group | 136,500 | 0.13% | 15,000,000 | 0 |

(1) Assumes the full conversion of the convertible promissory note held by the selling shareholder as of January 18, 2018. Prior to conversion, the selling shareholder does not hold any shares in the Company.

(2) The percentages in the above table are based on 473,222,721 common shares outstanding, which includes 467,086,221 common shares outstanding as of December 29, 2017 and the 6,136,500 shares presumed converted by the selling shareholder as detailed in note 1 above.

(3) In order to sell any shares pursuant to this offering circular, each selling shareholder must first convert all or part of its convertible promissory note into common shares of the Company. The conversion price is variable based on the market price of the Company’s common stock. The Company is registering 15,000,000 shares on behalf of the selling shareholder to account for fluctuations in the Company’s common stock, which will in turn affect the number of shares available to be sold by the selling shareholder.

(4) The Thomas Group, LLC is a Florida limited liability company controlled by Alan C. Thomas.

| (16) |

OTC Markets Considerations

Our common stock is not now listed on any national securities exchange or the NASDAQ stock market; however, the Company’s common stock is quoted on OTC Markets Pink marketplace. There is currently only a limited market for our securities and there is no guarantee that a more substantial or active trading market will develop in the future. There is also no guarantee that our securities will ever trade on any listed exchange. Accordingly, our shares should be considered highly illiquid, which inhibits investors’ ability to resell their shares.

The OTC Markets is separate and distinct from the NASDAQ stock market or other national exchange. NASDAQ has no business relationship with issuers of securities quoted on the OTC Markets. The SEC’s order handling rules, which apply to NASDAQ-listed securities, do not apply to securities quoted on the OTC Markets.

Although the NASDAQ and other national stock markets have rigorous listing standards to ensure the high quality of their issuers, and can delist issuers for not meeting those standards; the OTC Markets has no listing standards. Rather, it is the market maker who chooses to quote a security on the system, files the application, and is obligated to comply with keeping information about the issuer in its files.

Investors may have greater difficulty in getting orders filled than if we were on NASDAQ or other exchanges. Trading activity in general is not conducted as efficiently and effectively on OTC Markets as with exchange-listed securities. Also, because OTC Markets stocks are usually not followed by analysts, there may be lower trading volume than for NASDAQ-listed securities.

| (17) |

USE OF PROCEEDS

The following table illustrates the amount of net proceeds to be received by the Company on the sale of shares by the Company and the intended uses of such proceeds over an approximate 12 month period. The Company will not receive any proceeds from the sale of shares by the selling shareholders.

| Capital Sources and Uses | ||||

| 100 | % | |||

| Gross Offering Proceeds | $ | 5,000,000 | ||

| Use of Proceeds: | ||||

| Offering Expenses(1) | $ | 23,000 | ||

| Inventory (2) | $ | 1,000,000 | ||

| Research and Development(3) | $ | 50,000 | ||

| Salaries to Officers and Directors(4) | $ | 500,000 | ||

| Investor Relations(5) | $ | 6,000 | ||

| Accounting(6) | $ | 3,000 | ||

| Travel(7) | $ | 25,000 | ||

| Marketing(8) | $ | 750,000 | ||

| Legal Expenses(9) | $ | 250,000 | ||

| Working Capital Reserves(10) | $ | 2,393,000 |

________________

| (1) | The Company expects to pay approximately $23,000 in expenses relating to this offering including legal fees, accounting fees, printing, travel and reimbursements for these expenses previously incurred by the Company’s management. |

| (2) | Assuming a fully funded offering, the Company intends to acquire approximately $1,000,000.00 in inventory. |

| (3) | The Company expects to spend approximately $50,000.00 in offering proceeds on researching and developing new products. |

| (4) | The Company intends to clean up its balance sheet by paying Dr. Chris Ayo Otiko for compensation which is owed to him and has been deferred. |

| (5) |

The Company intends to utilize $6,000.00 to pay consultants providing IR services for the Company. |

| (6) | The Company expects to utilize up to $3,000.00 in offering proceeds for its ongoing accounting fees. |

| (7) | The Company anticipates travel expenses relating to promoting the Company and its products to the public. |

(8)

|

The Company intends to apply offering proceeds towards marketing campaigns for its products, with a focus towards distributor promotions. |

| (9) | The Company intends to allocate approximately 250,000.00 towards legal expenses related protecting its intellectual property rights and its commercial transactions. |

| (10) | The Company will use working capital to pay for miscellaneous and general operating expenses. |

In the event the Company does not sell all shares offered hereby, it intends to reduce the allocation to working capital. Once no proceeds are available for allocation to working capital reserves, the Company intends to proportionately reduce the amount of proceeds allocated to each other category above, which are listed in order of priority.

The allocation of the use of proceeds among the categories of anticipated expenditures represents management’s best estimates based on the current status of the Company’s proposed operations, plans, investment objectives, capital requirements, and financial conditions. Future events, including changes in economic or competitive conditions of our business plan or the completion of less than the total offering, may cause the Company to modify the above-described allocation of proceeds. The Company’s use of proceeds may vary significantly in the event any of the Company’s assumptions prove inaccurate. We reserve the right to change the allocation of net proceeds from the offering as unanticipated events or opportunities arise.

| (18) |

DESCRIPTION OF BUSINESS

Organization

ViaDerma, Inc. was incorporated in the State of Florida on January 11, 2007 in name of Murals By Maurice, Inc. On July 1, 2009, the Company changed its name to Décor International Products, Inc. On January 20, 2010 the Company filed Articles of Merger with the Secretary of State of Florida to effect a merger with Wide Broad Group, LTD a corporation incorporated in the British Virgin Islands. On May 13, 2010, Décor International Products, Inc. filed articles of merger and redomicile to the State of Nevada with DCRD Merger Sub, Inc. The resulting entity, newly domiciled in Nevada remained Décor Products International, Inc. until May 6, 2014 when it changed its name to ViaDerma, Inc.

Business

ViaDerma, Inc’s lead product is an FDA registered topical antibiotic called Viabecline or Vitastem™. The Company also has products in development in the following fields; anti-aging skin care, pain management, hair-loss, and toenail fungus. The products are based on a patent pending delivery system technology that allows for rapid mass transfer of the pharmaceutical active ingredient across the skin and into the body to provide immediate localized therapy. Detailed product information about Viabecline is available online by accessing the Government website, DailyMed.

The Company utilizes a specific Trade Secret Formulation System in the manufacture of all the products. On January 31, 2014, the Company purchased an exclusive license (the "License") on the patent pending technology from Dr. Howard Phillips represented by US Patent application #20130190274. The Company amended the License on January 20, 2017 such that it is now a non-exclusive distribution and licensing agreement.

Apart from the technology licensed from Dr. Howard Phillips, the Company is currently using a second-generation transdermal technology to manufacture and develop its products. This technology was exclusively licensed from a related party. During 2016, provisional patents were filed on this technology. The Company received provisional patent #62433964 ‘AQUEOUS TOPICAL SOLUTIONS for this technology. The Company believes the newer technology has additional benefits and plans to incorporate this topical delivery system into most, if not all of its future products.

In June 2017, the Company received notification that its newer product Prolayed (15ml), was also registered with the FDA.

| (19) |

The Company is in the early development stage of a medical cannabis product containing cannabidiol (“CBD”) that can be absorbed through the skin with our proprietary transdermal delivery system. A provisional patent application using the combination of CBD and THC with the delivery system was filed in 2017 (Provisional Patent # 62466209). The use of CBD is aimed at the reduction of inflammation and for the treatment of several diseases, such as, nicotine addiction, fibromyalgia, Cohn's disease, schizophrenia, migraine headaches, pain management for cancer and Multiple Sclerosis.

In addition, the Company has filed with the Food and Drug Administration (FDA) for a new over the counter or OTC version of a "Premature Ejaculation Drug". The new "OTC Drug" received FDA registration during the second quarter of 2017 (NDC:69006-010-00) and the Company's name of the new drug will portray prolonged endurance. The Company's recent testing of the drug has shown to be successful in retarding the onset of ejaculation during sexual intercourse.

The Company recently engaged an Operations Manager, effective on March 1, 2017, for an initial Go-to-Market strategy. The Operation Manager will initially be responsible for overseeing product manufacturing and development. He will additionally oversee the storage, delivery and fulfillment of our products.

Currently, the Company’s products are sold to local medical practitioners, and patients in clinics primarily in the Los Angeles, California area; however, the Company is moving towards a wholesale distributor model. The Company’s primary goal during 2017 has been to commercially manufacture the product on a larger scale and seek wholesale distribution partners that will carry and sell the product. The Company is presently using a manufacturing partner on the East Coast of the United States. During November 2017, the Company received its first finished order of Vitastem (bottle sizes range from 5ml to 15ml). The Company, along with its wholesale partners, will attempt to sell and distribute the product in several key areas during the next quarter.

In addition to the primary plan of developing and selling new products to the market, the Company is exploring the possibility of licensing the technology to other pharmaceutical companies. As of the date of this filing, the Company has entered into two licensing and distribution agreements as follows:

On January 1, 2017, the Company entered into a licensing and distribution agreement with Biogenx, Inc. for the purpose of commercializing and distributing a topical antibiotic product to be branded VitaStem. The product will carry the Company’s tetracycline-based technology. This product will be separately registered with the FDA. Pursuant to the agreement, the Company will receive 50% of gross profit from sales of Vitastem. For purposes of the agreement, gross profit is defined as total revenues less cost of production, distribution and marketing. In addition ViaDerma will receive an additional 5% of gross sales as a licensing fee. The agreement will terminate on December 31, 2022 unless extended by both parties. Biogenx, Inc. has the right to terminate the agreement early with two month notice if it deems the arrangement to not be financially viable.

On January 1, 2017, the Company entered into a licensing and distribution agreement with Vage Nigeria, Ltd. for the purpose of commercializing and distributing a topical antibiotic product to be branded Dermafix. The product will carry the Company’s tetracycline-based technology. This product will be separately registered with the FDA. Pursuant to the agreement, the Company will receive 50% of the net sales from Dermafix. For purposes of the agreement, net sales is defined as total revenues less cost of production, distribution and marketing (which includes taxes, discounts, allowances, credits for returns, rebates, import duties and other governmental charges, freight and transportation). The agreement will terminate on December 31, 2022 unless extended by both parties. Vage Nigeria, Ltd. has the right to terminate the agreement early with two month notice if it deems the arrangement to not be financially viable.

| (20) |

Intellectual Property

The following table summarizes the intellectual property currently held or applied for by the Company:

| Type of Intellectual Property | Name | Identification Number | Status |

| Trademark | BIOGENX | 87290961 | Live |

| Trademark | VITASTEM | 87227123 | Live |

| Provisional Patent | AQUEOUS TOPICAL SOLUTIONS | 62433964 | |

| Provisional Patent | Medical Marijuana topical ointment | 62466209 | |

| FDA NDC # (ViaDerma) | PROLAYED | 69006-010 | |

| FDA NDC # (ViaDerma) | VIABECLINE 15 ML | 69006-005-00 | |

| FDA NDC # (ViaDerma) | VIABECLINE 28 ML | 69006-005-01 | |

| FDA NDC # (Biogenx) | VITASTEM 5 ML | 71262-002-00 | |

| FDA NDC # (Biogenx) | VITASTEM 15 ML | 71262-002-15 |

Market Information

There are numerous competitors in our segment of the OTC drug market that have greater market share and resources than we do. We believe our competitive edge will be our patent-pending delivery system which we believe significant increases efficacy of normal OTC medications.

The Company’s transdermal delivery system allows for mass transport of active ingredients in medications across the skin faster and more effectively than most other topical medications. This gives the Company the ability to produce a pipeline of OTC topical products that are world-class relatively quickly and inexpensively. For example, Vitastem and Viabecline is one of the world’s strongest broad spectrum topical antibiotic for cuts, scrapes, wounds, infections, infection prevention and burns, infected insect bites and diabetic ulcers and general non-healing wounds. It has been able to heal wounds that have been resistant to even the strongest prescription medication. In addition to our own products, licensing opportunities may arise later with other manufacturers to formulate new versions of their drugs using the Company’s delivery system.

Research and Development

The Company estimates that, combined with Dr. Howard Philipps, $100,000 has been spent over the past three years towards research and development of our products. Dr. Phillips also used his lab facilities and staff towards the development of our delivery system.

Employees

The Company has no full time employees and 1 part time employee to support production and sales support.

| (21) |

Bankruptcy or Receivership

During 2014, the Company defaulted on a note payable to a creditor which resulted in a legal action to issue 520,000 common shares and 1,666,667 preferred shares to the creditor. During the year ended December 31, 2015, 666,667 shares of preferred stock of the Company were converted into 6,666,670 shares of common stock at the ratio of 10:1 upon the request from the preferred shareholder.

Legal Proceedings

The Company is not currently a party to any legal proceedings.

Material Agreements

In addition to the licensing, marketing and distribution agreements relating to its products, the Company has entered into various agreements which may have a material impact on our business operations if they were terminated prior to their expiration date. Below are descriptions of such agreements.

The Company entered into an Employment Agreement with Dr. Chris A. Otiko on January 1, 2017 (the “Employment Agreement”), which is attached hereto as Exhibit 6.1 and is incorporated herein by reference. Pursuant to the Employment Agreement, Dr. Otiko agreed to act as the Company’s President until January 1, 2020. Dr. Otiko is also currently the Company’s sole Director. If Dr. Otiko or the Company should resign or terminate the Employment Agreement prior to January 1, 2020, the Company will have to immediately invest money, time and effort in identifying a new President for the Company.

On March 1, 2017, the Company entered into an Independent Contractor Agreement (the “Contractor Agreement”) with Ivan Klarich. The Contractor Agreement is attached hereto as Exhibit 6.2 and is incorporated herein by reference. Pursuant to the Contractor Agreement, Mr. Klarich agreed to serve as Operations Manager of the Company for a term of one (1) year. Though Mr. Klarich is only considered an independent contractor of the Company, he provides valuable services and the Company would be required to promptly invest money, time and effort in identifying a new Operations Manager for the Company if Mr. Klarich resigned or terminated his Contractor Agreeemnt before the end of its term.

The Company entered into a Financial Advisory Agreement dated April 20, 2017 (the “Advisory Agreement”) with Greentree Financial Group, Inc. (“Greentree”). Pursuant to the Advisory Agreement, which is attached hereto as Exhibit 6.3 and is incorporated herein by reference, Greentree agreed, inter alia, to assist the Company with the preparation of its quarterly and annual reports for the fiscal year 2017. If Greentree should terminate the Advisory agreement prior to the end of its term on December 31, 2017, the Company may not be able to timely file its periodic reports until a replacement for Greentree can be engaged.

Reports to Security Holders

We file alternative reports with OTC Markets. Our filings are available to you free of charge at www.otcmarkets.com.

Government Regulation

The Company is not aware of any government regulations that could adversely affect its products. The active ingredients in its products have been available and approved by the FDA for several decades and the components of the delivery systems are also approved for use by the FDA.

| (22) |

DESCRIPTION OF PROPERTY

The Company leases an office located at 18740 Ventura Blvd, Suite 102, Tarzana, CA 91356 which we use for daily operations, marketing, research and development. The office is approximately 800 square feet with annual rental expense of approximately $10,000. We believe the current office space is sufficient for the next 12 months.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Issuer’s Plan of Operation for the next twelve months.

ViaDerma, Inc. is a specialty pharmaceutical company committed to bringing new products to the pharmaceutical industry through innovative research and development. The Company attempts to license and sell products in fields of medicine ranging from infectious diseases to stem-cell therapy. The Company’s products are normally applied topically using a patent-pending delivery system technology originally created by Dr. Phillips and Dr. Chris Ayo Otiko. Presently, the products are used within the OTC drug market, i.e. non-prescription. However, the Company believes the delivery system can be used for the prescription medication market as well not only for topical prescription medications but also to turn certain oral medications into topically based medications.

In addition to the primary plan of developing and selling new products to the market, the Company is exploring the possibility of licensing the technology to other pharmaceutical companies. As of the date of this filing, the Company has entered into two licensing and distribution agreements as discussed elsewhere in this circular. The Company has also engaged an operations manager to assist it implement its goals.

For the three and nine months ended September 30, 2017 and 2016 (Unaudited)

Revenues and Cost of Sales

The Company had revenues of $7,002 and $26,802 for the three and nine months ended September 30, 2017, respectively, as compared with $83,500 and $209,573 for the same periods in 2016. The decrease was primarily due to the Company’s strategy to shift selling focus to wholesale distributors instead of mostly local physicians. The Company believes this strategy will be a key component to achieve significant revenue growth. Thus far, the Company has entered into agreements with two distributors during the first nine months of the year and plans to enter into additional agreements during the fourth quarter. Although new orders from these distributors have not been placed to date, the Company believes initial volume indications are very encouraging. The Company experienced a delay in receiving its first large-scale order of its products from its new manufacturer as and such some initial new orders needed to be pushed back until the product arrives. The Company received this order in November 2017 and is now ready and available to fulfill product orders.