|

Dakota Real Estate Investment Trust OFFERING CIRCULAR UNDER REGULATION A

300,000 Class A Voting Shares 150,000 Class B Non-Voting Shares 150,000 Class I Voting Shares

Issuable at $15.20 per Share Under the Distribution Reinvestment Plan |

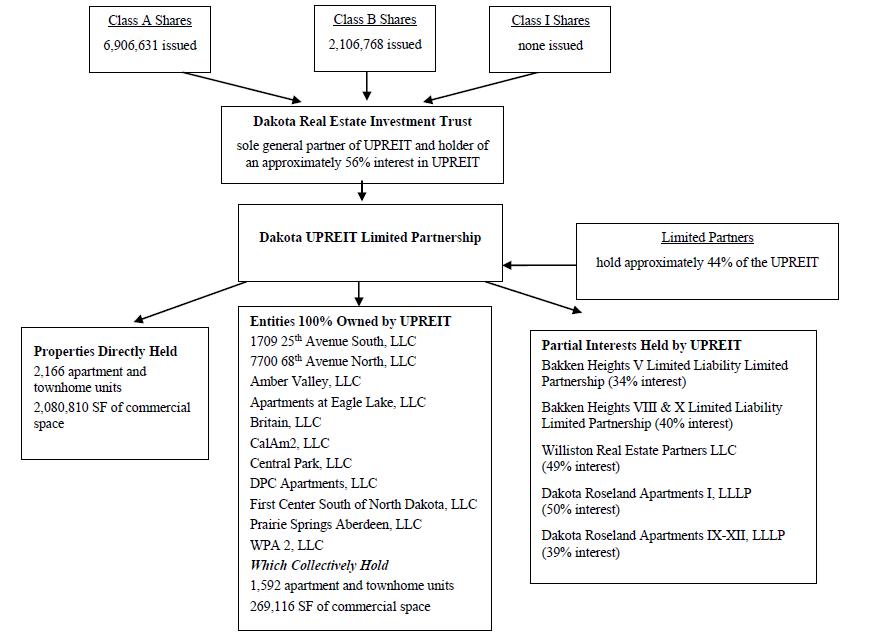

The Dakota Real Estate Investment Trust (the “Trust”) is a business trust organized under the laws of North Dakota. Our principal place of business is 3003 32nd Avenue South, Suite 250, Fargo, North Dakota 58103, our telephone number is (701) 239-6879 and our website is www.dakotareit.com. The Trust’s assets consist of a controlling interest in DAKOTA UPREIT LIMITED PARTNERSHIP (the “UPREIT”), a North Dakota limited partnership. The UPREIT invests in and operates real estate. The Trust is the General Partner of the UPREIT.

Pursuant to an Offering Statement (the “Offering Statement”) qualified with the Securities and Exchange Commission (the “SEC”) on the date hereof we are offering (the “Offering”) our Class A Voting Shares (the “Class A Shares”), our Class B Non-Voting Shares (the “Class B Shares”), and our Class I Voting Shares (the “Class I Shares” and collectively with the Class A Shares and Class B Shares, the “Shares”) to existing Shareholders of the Trust who or which elect to participate in our Distribution Reinvestment Plan (the “DRIP”) to apply distributions payable to them for the acquisition of Shares at the rate one share for each $15.20 of distribution payable to the participant. This Offering Circular is provided to participants in the DRIP for use in considering continuation of their participation in and to other shareholders considering becoming participants in the DRIP.

You should not acquire Shares if you cannot afford a complete loss of your investment. Investing in the Shares involves material risks (See “RISK FACTORS” beginning on page 3).

The Offering will terminate at the earlier of issuance of all of the Shares or July 31, 2022.

THE UNITED STATE’S SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OF OR GIVE ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF THIS OFFERING CIRCULAR OR OTHER SELLING LITERATURE. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE SEC; HOWEVER, THE SEC HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED HEREUNDER ARE EXEMPT FROM REGISTRATION.

THESE SECURITIES HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE SECURITIES COMMISION OF ANY STATE NOR HAS THE ACCURACY OR ADEQUACY OF THIS OFFERING CIRCULAR. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

| Price(1) | Sales Commission(2) | Proceeds to Us(3) | ||||||||||

| per Share(1) | $ | 15.20 | $ | 0.00 | $ | 15.20 | ||||||

| 300,000 of Class A Shares(1) | $ | 4,560,000 | $ | 0.00 | $ | 4,560,000 | ||||||

| 150,000 of Class B Shares(1) | $ | 2,280,000 | $ | 0.00 | $ | 2,280,000 | ||||||

| 150,000 of Class I Shares(1) | $ | 2,280,000 | $ | 0.00 | $ | 2,280,000 | ||||||

| Total Offering | $ | 9,120,000 | $ | 0.00 | $ | 9,120,000 | ||||||

| (1) | Participants in the DRIP may apply distributions due them to acquire Shares in the Offering at the rate of one share for each $15.20 of distribution taken in Shares in lieu of payment of the distribution. Fractional Shares out to one hundredth of a thousandth (i.e., four decimal points) will be issued. |

| (2) | No commissions will be paid with respect to such issuances of Shares. |

| (3) | We will receive no payments as a result of the Offering. To the extent an existing shareholder elects to participate in the DRIP, we will issue Shares to such participant in lieu of a cash payment of a distribution due such participant. As a result, funds which would otherwise be paid out as a distribution will be retained by the Trust. |

The date of this Offering Circular is _____ __, 2021

| i |

TABLE OF CONTENTS

| ii |

WHO MAY PARTICIPATE IN THE OFFERING

This Offering Circular does not constitute an offer to issue or a solicitation of an offer to acquire any securities offered hereby in any jurisdiction where, or to any person to whom, it is unlawful to make such an offer.

Required Residence / Domicile to Invest. This Offering is available to existing shareholders of the Trust who are residents of or entities domiciled in a state in which we have qualified the issuance of shares under the DRIP by registration or pursuant to an exemption from registration in accordance with laws of such state related to the offer and issuance of shares. Individuals are residents of the state in which they maintain their principal residence. A corporation, partnership, trust or other entity is domiciled in the state where the principal office of the entity is located.

Participation in the DRIP. To participate in the Offering, investors must be a participant in the DRIP and have their shareholder registration with the Trust reflect that the participant meets the residency / domicile requirements addressed above.

The Shares are offered subject to withdrawal or cancellation of the Offering at any time without prior notice. The Trust reserves the right to terminate the Offering of any of the Class A, Class B Shares or the Class I Shares and continue the Offering of the other class or classes of Shares.

IMPORTANT INFORMATION ABOUT THIS OFFERING CIRCULAR

Please carefully read the information in this Offering Circular and any supplements thereto. You should rely only upon the information in this Offering Circular as we have not authorized anyone to provide any different information regarding us or this Offering.

Offering Statement This Offering Circular is part of an offering statement we have filed with the SEC and may amend from time to time (the “Offering Statement”). We contemplate this being a “continuous offering” and thus we anticipate that we may prepare and distribute supplements or amendments and restatements to add or change information contained in the Offering Circular contained in our Offering Statement. Our Offering Statement includes exhibits that provide detailed information or documents discussed in this Offering Circular. You may access such information through the electronic data gathering, analysis and retrieval system found at https://www.sec.gov/edgar.

Cautionary Note Regarding Forward Looking Statements This Offering Circular contains forward-looking statements. All Statements other than statements of historical fact contained in this Offering Circular, including statements regarding our future results of operations and financial position, business strategy and plans and objectives of management for future operations, are forward looking-statements. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by these forward-looking statements.

Forward-looking statements are subject to risks and uncertainties, certain of which are beyond our control. Actual results could differ materially as a result of the factors described in “Risk Factors” in this Offering Circular.

| iii |

The following summary is qualified in its entirety by the detailed information appearing elsewhere in this Offering Circular.

SHARES BEING OFFERED

The Trust is offering to shareholders who or which have elected to participate in the Trust’s Distribution Reinvestment Plant (the “DRIP”) to receive up to Shares in lieu of receipt of payment of distributions on the class of Shares with respect to which they elect to participate. The Shares will be issued at a rate of one Share for each $15.20 of distribution taken in Shares rather than in a cash payment.

Under its Declaration of Trust (the “Declaration of Trust”), the Trust is authorized to issue one or more classes of Shares. The Declaration of Trust recognizes Class A, Class B and Class I Shares. Each Class shares equal rights to participate in distributions while only Class A and Class I Shares come with voting rights. As of March 31, 2021, there were approximately 6,973,154 Class A Shares, approximately 2,136,342 Class B Shares and 195,564 Class I Shares outstanding.

terms of the distribution reinvestment plan

The Trust has adopted the DRIP to permit shareholders who or which elect to participate in the plan the opportunity to invest their cash distributions otherwise payable to the shareholder in the purchase of Shares of the same class with respect to which the distribution is payable. Participation is made by completion of an election to participate. For individuals initially subscribing to purchase Shares, the subscription to be tendered includes an election provision. For existing shareholders, the election is made in a Shareholder Change Form reflecting the election to participate. Participants in the DRIP may discontinue their participation by completing and submitting to the Trust of a Shareholder Change Form reflecting the election to discontinue participating.

Issuance of Shares under the DRIP is subject to the Trust having in effect qualification for the issuance under both applicable federal and state laws regulating the offer and issuance of securities with respect to the Shares. If there is not such a qualification in effect when a distribution is payable, the Trust may elect to either: (i) issue payment of the distribution in cash; or (ii) hold the distribution pending qualification of the issuance under applicable law.

The rate of issuance of Shares in lieu of a cash payment of a distribution is currently 95% of the per share offering price for the Shares then being offered by the Trust (exclusive of any commissions or other fees a subscriber may be required to pay) rounded up to the next full cent. As the Trust has established $16.00 as its current offering price for its Shares, the issuance rate currently in effect under the DRIP is $15.20 per share.

The TRUST

The Trust began business operations in 1997. The Trust is an unincorporated, but registered business trust under North Dakota law. The Trust has an indefinite term of existence consistent with North Dakota law (that is the Trust is not required to discontinue its existence at a specified future date. The Trust is the sole general partner of the UPREIT and makes all of the investment decisions of the UPREIT. The Trust will invest in properties that the Board of Trustees considers suitable investments. Properties can and may include commercial properties and multi-family residential properties, such as apartment buildings. The Trust has had no business activities other than the ownership of real estate and interests in entities owning real estate.

The Trust is registered as required by the laws of North Dakota and is structured to comply with the requirements under Internal Revenue Code Section 856 which requires that 75% of the assets of a real estate investment trust must consist of real estate assets and that 75% of its gross income must be derived from real estate. The Trust believes it qualifies as a real estate investment trust but has not received confirmation of its qualification from the Internal Revenue Service. (See “FEDERAL INCOME TAX CONSIDERATIONS”).

ADVISOR

The advisor of the Trust is Dakota REIT Management, LLC (the “Advisor”), which was formed for such purpose in April 2008. The Advisor manages the affairs of the Trust, subject to the review and overall control of the Board of Trustees, who may remove the Advisor without cause.

| 1 |

THE UPREIT

The Trust’s assets consist almost entirely of our general partnership interest in Dakota UPREIT Limited Partnership (the “UPREIT”), a North Dakota limited partnership. The UPREIT utilizes its assets to invest either directly in real estate properties or in ownership interests in entities that hold real estate properties. The Trust is the general partner of the UPREIT. As of December 31, 2020 our interest in the UPREIT represented an approximately 56% ownership interest with the remaining approximately 44% in interests being held by approximately 163 holders of limited partnership interests.

INVESTMENT OBJECTIVES

The Trust’s investment objectives are (i) to preserve, protect and return shareholder capital, (ii) provide cash distributions on a quarterly basis at the discretion of the Board of Trustees, a portion of which (due to depreciation) may not constitute current taxable income, and (iii) provide growth of capital investment through potential appreciation in the value of the Trust’s properties. There is no assurance that such objectives will be attained.

THE PROPERTIES

As of December 31, 2020, the UPREIT held residential apartment projects comprising a total of 3,527 apartment units, 122 residential rental townhome units and 2,332,691 square feet of commercial rental property. In 2020, the UPREIT acquired a 59,323 SF retail commercial property located in Fargo, ND. In 2020, the UPREIT sold two single tenant properties, one was a 25,614 SF retail site located in New Prague, MN and a 23,206 SF retail/industrial facility located in De Pere, WI. It is anticipated that UPREIT will continue to seek to acquire properties or interests in properties involving both residential and commercial real estate (See “DESCRIPTION OF PROPERTIES”).

SUMMARY OF RISK FACTORS

Investing in this Offering through participation in the DRIP involves significant risks. A more detailed listing of risk factors you should consider prior to investing in the Shares is set out in the section entitled “RISK FACTORS.”

| ● | There is currently no trading market for our Shares and we do not anticipate one developing. The Shares issued in this Offering will be pursuant to Regulation A of the Securities and Exchange Commission and thus are eligible for resale or transfer, but there can be no assurance that a holder will be able to identify a buyer for their Shares. In order to provide shareholders with liquidity, the Trust has maintained a share repurchase arrangement permitting shareholders who have held their Shares for at least one year to request to have their shares redeemed in accordance with the procedures of our Share Repurchase Program. The program has involved a repurchase fee in the form of a 10% of the then applicable offering price for Shares as the per share repurchase price paid. There can, however, be no assurance as to the funds the Board of Trustees allocate for repurchase in the future, that the Share Repurchase Program will remain in effect or that we will not change its terms. In response to potential reduction in operating revenue as a result of the COVID-19 pandemic, the Board of Trustees suspended the repurchase of shares in April 2020, but then reinstated the repurchases in October 2020. |

| ● | The $15.20 issuance rate per share for participants in the DRIP has been arbitrarily determined by the Board of Trustees. The book value of the Trust as of December 31, 2020 was approximately $6.49 per share. Accordingly, the offering price is substantially greater than the book value per share. |

| ● | The Trust invests in real estate and thus an investment in the Trust involves the risks associated with making real estate investments. In making its investments, the Trust uses substantial amounts of borrowed funds. As of December 31, 2020, we owed approximately $398,201,000 under notes secured by mortgages on our properties. |

| ● | Dakota REIT Management, LLC (the “Advisor”) acts as an advisor to the Trust under an agreement between the Advisor and the Trust. The Advisor and its affiliates will receive various fees for performing property management and other services, and the determination of such compensation has been made without the benefit of arm’s-length negotiations with the Board of Trustees (See “COMPENSATION PAID TO ADVISOR AND OTHER PROPERTY MANAGERS”). |

| ● | Members of our management or their affiliates are subject to conflicts of interest in respect to their relationships and agreements with the Trust (See “INTERESTS OF MANAGEMENT AND OTHERS IN CERTAIN TRANSACTIONS”). |

| ● | There is no guarantee that the Trust will continue to declare distributions in the future. |

| ● | Economic conditions, which the Trust cannot predict or control, may have a negative impact on the value of the Trust’s assets. |

| ● | The Trust will be taxed as a corporation if it fails to qualify as a REIT. |

| 2 |

The acquisition of Shares in the Offering pursuant to an election to participate in the DRIP involves various risks. Existing and prospective participants in the DRIP should carefully consider the following risks, among others, before making a decision to accept Shares in lieu of cash payment of distributions. An investment in the Trust is speculative and involves a high degree of risk and should be considered only by persons who can afford the loss of their entire investment.

RISKS RELATED TO INVESTING IN THE TRUST AND PARTICIPATING IN THIS OFFERING

The UPREIT Has Not Identified Properties to Acquire in the Future

The future real estate investments and properties to be acquired by the UPREIT are yet to be determined. Because future acquisitions have not been identified, the participants in the DRIP will have no information to assist in making the investment decision based on the identification or location of, or as to the operating histories of, or other relevant economic and financial data pertaining to, the properties to be purchased by the UPREIT, and must rely entirely on the investment judgment of the Advisor and the Board of Trustees.

The Shares Are an Illiquid Investment

There is currently no trading market for the Shares, and we do not anticipate such a market will develop and have no intention to seek to list the Shares upon any stock exchange. Without the benefit of an established public trading market, the Shares should be viewed as relatively illiquid. Consequently, the purchase of Shares should be considered only as a long-term investment. Furthermore, even if a market for the sale of Shares were to develop, no assurance can be given as to the price at which Shares would be sold in such market.

The Trust has no plans to liquidate and, absent the Trustees or the shareholders (the Amended and Restated Declaration of Trust allows for a majority vote of shareholders with voting rights to require liquidation) taking action to liquidate the Trust, the Trust will continue in existence for an indeterminate time. Accordingly, an investor in the Shares pursuant to the DRIP, should not anticipate liquidity from the liquidation of the Trust.

To provide shareholders access to liquidate their holdings in the Trust, we have maintained a share repurchase program. (See - “SECURITIES BEING OFFERD – Share Repurchase Plan” for information related to such arrangements). Such plan has restrictions and limitations, including the level of funding approved for use under the plan.

Shareholders Must Rely on Management to Act on Their Behalf

The Advisor and the Trustees are accountable to the Trust as fiduciaries and must exercise good faith and integrity in handling Trust affairs. The Trustees have the authority to approve or disapprove all investments recommended to the UPREIT by the Advisor. The Trustees will have ultimate control over the management of the Trust and the conduct of Trust affairs, including management of the business of the UPREIT and the acquisition and disposition of the UPREIT’s assets, but the success of the Trust and UPREIT will depend, to a large extent, on the services and performance of the Advisor.

Shareholders have no right or power to take part in the direct management of the Trust or the UPREIT. Holders of Shares with voting rights (Class A and Class I Shares) vote on election of members of the Board of Trustees amendments to Declaration of Trust, most changes to the Bylaws, liquidation, roll-up transactions, and certain sales of assets of the Trust. Holders of Shares with voting rights also have the right to demand a special meeting of shareholders.

Subject to some conditions and limitations, the Declaration of Trust limits the liability of, and provides for the Trust to indemnify, the Trustees, the Advisor and their affiliates, and to provide insurance coverage and pay for all premiums thereon to protect the Board of Trustees while acting for and on behalf of the Trust (See “BOARD OF TRUSTEES, EXECUTIVE OFFICERS AND SIGNIFICANT EMPLOYEES – Organizational Structure”).

None of the Officers appointed by the Trust or members of the Board of Trustees devote their full time and attention to the operation of the Trust. Each has their own businesses and investments, and in some instances, employment which places demands upon their available time.

| 3 |

RISKS RELATED TO OUR INVESTMENTS

Borrowing Risks

The UPREIT makes extensive use of borrowed funds in connection with its investments, generally seeking to maintain a level of financing equal to 75% of the appraised value of our properties. As of December 31, 2020 the mortgage notes payable were approximately $398,201,000. Use of borrowed funds permits the UPREIT to acquire additional properties than what might otherwise have been acquired only with available cash; however, should the value of the acquired property decrease, we may owe more on the borrowing than we can realize from the operation or sale of the property.

Certain of the borrowing used to finance acquisition of properties is under longer term fixed rate arrangements, but substantial portions of our borrowing involve “balloon payments” where the loan amount is not fully amortized prior to the maturity date or periodic readjustment of the interest rates. If general borrowing conditions result in a rise in interest rate or if lenders perceive lending to us has grown in risk, we may face increased interest rates or other adverse changes to the terms under which we may borrow funds that may impair our operating results. In connection with your consideration of these risks you may wish to know that we have the following loans maturing this year and in the next two calendar years:

| ● | 9 loans have or will come due in 2021 with an estimated principal at maturity of approximately $41,713,500; |

| ● | 7 of loans will be due in 2022 with an estimated principal at maturity of approximately $44,552,000; and |

| ● | 8 of loans will be due in 2023 with an estimated principal at maturity of approximately $27,002,500. |

Risk That Tenants Will Terminate Their Leases

Tenants may for various reasons be unable to pay the rent due us under their lease. When a tenant of one of our leases for an apartment or townhome fails to pay the tenant typically vacates the property or we may be required to commence legal proceedings to force such a vacation resulting in the unit being available for renting to a new tenant. As we have expanded our holdings in commercial real estate, we have experienced different economic circumstances associated with commercial real estate. These include changes in operations in our tenant’s businesses, including the complete termination and liquidation of our tenant’s business.

The lead times are often longer and we may incur additional expenses (such as brokerage fees and provision of improvement allowances) in leasing our commercial properties which we do not experience with our residential properties. As of December 31, 2020 of our approximately 2,332,691 square feet of commercial real estate, approximately 302,656 square feet (or approximately 12.9% of the total) was not under a lease with a tenant.

Risk That Tenants Will Not Renew Their Leases

Tenants of our residential real estate typically lease their apartment or townhome for an initial term of from six to twelve months with month-to-month terms thereafter. There can be no assurance that our residential tenants will renew their leases with us at the end of the term of their lease. Opportunities for purchase of residential properties by those residing in our apartments and townhome properties and tenants relocating outside of the area due to reduced employment opportunities may affect the choice by our tenants to continue their occupancy. As well, tenants may view newer properties or those with different amenities or lower rents as attractive. In addition to loss of revenues while a residential unit is vacant, a vacancy typically results in additional operating expenses associated with preparing the unit for rental and in the marketing of the unit.

Our commercial properties are typically leased for terms from one to twenty years with options to renew the term. Of the approximately 305 leases currently in effect for the approximately 2,030,035 square feet of commercial real estate, five of the leases (for an aggregate of approximately 59,997 square feet) are under month to month terms and 79 of the leases (for approximately 242,993 square feet) are scheduled to end by the end of December 2021. The table below identifies the leases, as of December 31, 2020 scheduled to expire the years indicated. This does not include the approximately 302,656 square feet of commercial property available for leasing.

| Year of Expiration | Number of Leases | Approximate

Square Footage Leased | ||||||

| 2021 | 79 | 242,008 | ||||||

| 2022 | 71 | 327,776 | ||||||

| 2023 | 45 | 214,932 | ||||||

| 2024 | 29 | 316,111 | ||||||

| 2025 | 30 | 481,646 | ||||||

| 2026 | 11 | 117,758 | ||||||

| 2027 | 11 | 107,680 | ||||||

| 2028 | 2 | 19,397 | ||||||

| 2029 | 1 | 27,834 | ||||||

| 2030 | 5 | 45,573 | ||||||

| 2031 | 1 | 10,000 | ||||||

| 2033 | 1 | 59,323 | ||||||

In general, commercial real estate requires additional costs to secure a new tenant or the renewal of a tenant’s lease when compared with residential real estate due to the granting of concessions to the tenant for undertaking the lease of the property. Such concessions include abatement of rent for periods of time and contributions to costs of the tenant making improvements or relocating its operations.

As well, certain commercial property may be for specialized uses that are not compatible with the needs of potential replacement tenants. This may cause a delay in locating a subsequent tenant or require substantial contributions to a tenant’s cost of modification of the property to meet their needs.

Our Investment in Real Estate will be Subject to General Risks Associated with Real Estate Investments

The real estate properties and interests in entities holding real estate properties invested in by the UPREIT will be subject to risks typically associated with real estate, including:

| ● | natural disasters such as storms and floods; |

| ● | adverse changes in national, regional or local economic or real estate conditions; |

| ● | oversupply or reductions in demand for rental properties which may adversely affect renewals of leases by existing tenants; |

| ● | uninsured or under insured casualty losses; |

| ● | unanticipated costs to maintain properties (See discussion of improvements and related matters in “MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS – Capital Expenditures”); and |

| ● | tenants who are unable to pay rent as agreed or who or which fail to comply with their obligations to properly use and care for the property they lease |

The Trust’s Assets are not Diversified and have Limited Liquidity

Through the UPREIT, the Trust invests in real estate. All real estate investments are subject to some degree of risk. Such investments will be subject to risks such as adverse changes in general and local economic conditions or local conditions such as excessive building resulting in an oversupply of existing space or a decrease in employment reducing the demand for space. Such investments will also be subject to other factors affecting real estate values, including (i) possible federal, state or local regulations and controls affecting lending, rents, price of goods, fuel and energy consumption and prices, water, and environmental restrictions affecting new construction, (ii) increasing labor and material costs, (iii) the attractiveness of the property to tenants in the neighborhood, and (iv) state and federal income tax liability. Economic conditions, which the Trust cannot predict or control, may have a negative impact on the value of the UPREIT’s assets.

We currently own properties in the states of Iowa, Nebraska, Minnesota, North Dakota and South Dakota (See “DESCRIPTION OF PROPERTIES”). As of December 31, 2020, most of our holdings were located in North Dakota (22 residential properties with 2,533 units and 20 commercial properties with 1,068,648 square feet of space of the total holdings of 34 residential properties with 3,649 units and 41 commercial properties with approximately 2,332,691 square feet of space). Accordingly, you may view our investment in real property as concentrated within a limited geographic area.

Our real estate investments have primarily been in residential rental properties; however, we have increased our holdings of commercial real estate. Of the 2,332,691 square feet of commercial real estate held on December 31, 2020, approximately 45% was retail (including approximately 257,000 square feet being small shopping centers with a grocery store anchor tenant, and approximately 183,000 square feet being small shopping centers with a “big box” retailer as anchor tenant and approximately 59,000 square feet being a grocery store); approximately 35% being office space; approximately 18% being “flex space” where the tenant may allocate the space among warehouse, production and office uses; and approximately 1.5% being self-storage space.

The Trust will have very little opportunity to vary its portfolio promptly in response to changing economic, financial and investment conditions.

| 4 |

Significant Increases in Property Taxes Could Adversely Affect the Trust

With respect to some of our commercial real estate, we pass through to the tenant the obligation to pay property taxes assessed upon the property subject to their lease; however, most of our leases (most notably our residential leases) do not provide for such shifting of the risk of increased property taxes to the tenants. Accordingly, significant increases in property taxes payable with respect to our properties could have a material adverse effect on our operating results. Further, as a significant increase in taxes payable with respect to our properties would reduce the operating profitability, the values we may obtain from a sale of properties subject to the increased tax burden would be reduced.

Regulations and Public and Private Use Restrictions on Our Properties May Affect our Operations

Local governmental agencies may impose controls or restrictions on rental charges or otherwise adopt regulations which could have a material adverse effect upon our operations. In addition, costs of compliance with regulations such as those pertaining to environmental matters or accessibility to those with physical disabilities (such as the American with Disabilities Act) may also adversely affect our operations.

In addition to regulations, zoning and other use restrictions of local governmental agencies as well as covenants that may be established by private parties that apply to our properties. These public and private restrictions may include the types of uses that may be made with the property as well as impose operating conditions, such as numbers of required parking spaces that must be maintained based on the size of the property and the appearance (“architectural controls”) of the property.

Such taxes, regulations and controls may impair the operating profitability of our properties and thus the values we obtain from a sale of such properties would be reduced.

Real Estate Investments of the UPREIT Face Competition From Other Real Estate Properties

The results of operation of the Trust will depend upon the availability of suitable real estate investment opportunities for the UPREIT, and on the yields available from time to time on real estate and other investments, which, in turn, depends to a large extent on the type of investment involved, the condition of capital markets, the nature and geographic location of the property, and competition and other factors, none of which can be predicted with certainty. Even though the Advisor and its Affiliates have years of experience of acquiring properties suitable for investment, the UPREIT will be competing for acceptable investments with private investors and other real estate investment programs. Many of these competitors have greater experience and resources than the UPREIT.

Ownership of Real Estate Carries Risk of Uninsured Losses and Environmental Liabilities

The Trust intends to maintain what it believes to be adequate property damage, flood, fire loss and liability insurance. However, there are certain types of losses (generally of a catastrophic nature), which may be uninsurable or which may be economically unfeasible to insure. Such excluded risks may include war, earthquake, hurricane, terrorism, certain environmental hazards and floods. Should such events occur, (i) the UPREIT and the Trust might suffer a loss of capital invested, (ii) tenants of spaces may suffer losses and may be unable to pay rent for the spaces, and (iii) UPREIT and the Trust may suffer loss of profits which might be anticipated from one or more properties.

Federal law (and the laws of some states in which the UPREIT holds or may acquire properties) imposes liability on a landowner for the presence on the premises of hazardous substances or wastes (as defined by present and future federal and state laws and regulations). This liability is without regard to fault or knowledge of the presence of such substances and may be imposed jointly and severally upon all succeeding landowners. If such hazardous substances are discovered on a property owned by UPREIT, UPREIT could incur liability for the removal of the substances and the cleanup of the property. There can be no assurance that UPREIT would have effective remedies against prior owners of the property. In addition, UPREIT may be liable to tenants and may find it difficult or impossible to sell the property either prior to or following any such cleanup.

| 5 |

We Rely Upon Services of Property Management Companies

We engage the Advisor and various independent property management companies to manage our real estate properties (See “DESCRIPTION OF BUSINESS – ADVISOR AND PROPERTY MANAGERS”). In 2019 and in 2020, we paid $2,269,609 and $2,283,836 in property management fees (including $263,607 and $304,307 to the Advisor). We also paid to the Advisor advisory management fees of $1,800,383 in 2019 and $1,914,450 in 2020 for administrative services (See “COMPENSATION PAID TO ADVISOR AND OTHER PROPERTY MANAGERS”).

While the Advisor does not act as a property manager for any other property owners, the rest of the property management companies we use do manage properties for other parties which properties may compete for tenants with our properties. While we seek to monitor the effectiveness of our property managers, there can be no assurance that owners of competing properties may receive better services than do we. While we have rights to terminate the agreements, we are also subject to termination of the property management agreements by the managers upon very limited notice.

Increases in Expenses May Reduce Cash Flow and Thus Funds Available for the Making of Distribution Payments and for Additional Acquisitions of Investments

Our income from operations was approximately $5.9 million in 2019 and approximately $4.4 million in 2020. Such income represents income from the rental of our residential and commercial properties less the expenses from our operations and the costs of administration of the Trust. We declared distributions to our shareholders of $6,652,801 in 2019 and $7,056,622 in 2020 and the UPREIT declared distributions to its limited partners of $5,337,791 in 2019 and $5,575,232 in 2020. The amount of the declared distributions paid was substantially less due to the election by shareholders and limited partners to reinvest their distribution to acquire shares or limited partnership units. Shareholders received shares in lieu of approximately 61.4% and 56.9% of distributions due them and limited partners received limited partnership units in lieu of approximately 22.7% and 20.6% of distributions due them in 2019 and 2020, respectively.

If our operating expenses or the cost of the administration of the Trust increase without corresponding increases in our income from rental of our properties, our operating net income would decrease and our ability to continue to make distributions the Shareholders of the Trust and limited partners of the UPREIT and our ability to use cash flows from operation to invest in additional properties could be impaired. In addition, reduction in our distributions may reduce the levels of participation by shareholders of the Trust and by limited partners in the UPREIT in the reinvestment plans each maintains (in 2020, $4,015,507 was reinvested in the acquisition of shares of the Trust and $1,147,330 was reinvested in the acquisition of limited partnership units of the UPREIT). Under the terms of the Trust’s and the UPREIT’s Distribution Reinvestment Plans, participants may revoke their election and choose to receive cash payment of their distributions or distributions. Reductions in our operating income may affect a shareholder’s determination to participate in the plan.

Delays in Connection With Construction of Improvements to Our Properties

It has been our practice to acquire properties that have been in operation rather than undertaking to build and develop properties. As such, we have limited our exposure to risks associated with uncertainties in the development of real estate properties, such as unanticipated delays in the completion of construction of the improvements due to issues with suppliers of the materials or services used in the construction of the property.

We have, however, invested in properties under development through the making of loans to or acquisition of non-controlling equity interests in a property developer constructing a property. In addition, from time to time, we engage in the renovation or improvement of our properties (See the discussion of improvements and maintenance expenditures in “MANAGEMENT’S DISCUSSION AND ANYALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS” – “Capital Expenditures”).

Delays in completion of improvements to our properties may arise for a variety of reasons over which we will have no control. Such delays may result in additional costs being incurred as well as in loss of income due to the delay in completion of the improvements.

| 6 |

RISKS RELATED TO ADVISOR AND CONFLICTS OF INTEREST

We are Dependent on the Advisor, the Principals of which have other Business Interests

The Advisor is responsible for the day to day management of the operation of the Trust and of the UPREIT. As such, we are dependent upon the services of the Advisor. George Gaukler, Jim Knutson and Matthew Pedersen, who are each members of the Trust’s Board of Trustees are owners of the Advisor, but have other business interests (See the biographical information for Mr. Gaukler, Mr. Knutson and Mr. Pedersen under “BOARD OF TRUSTEES, EXECUTIVE OFFICERS AND SIGNFICANT EMPLOYEES” for information related to those other interests).

Mr. Gaukler and Mr. Knutson currently devote less of their time in performing their functions as managers of the Advisor with Mr. Pedersen (who is now President of the Trust) and Danel Jung devote substantially all of their time to the discharge of their duties as managers of the Advisor or as officers of the Trust.

While many of the employees of the Advisor have been with the Advisor for extended periods of time, there can be no assurance that they will continue their employment or that the Advisor would be successful in retaining services of successors should existing staff no longer continue their employment. Neither the Trust nor the Advisor maintains “key person” life insurance policies on any members of the staff of the Advisor. Accordingly, in the event of the death of a key staff member of the Advisor, we and the Advisor would not receive proceeds of a life insurance policy to assist in covering costs which might be incurred in connection with securing a replacement for the loss of a deceased key staff member.

Conflicts of Interest in General

Various conflicts of interest exist – and will arise in the future – as a result of the transactions between the Trust and: (i) the Advisor; (ii) members of the Board of Trustees; or (iii) affiliates of a Trustee (See “INTERESTS OF MANAGEMENT AND OTHERS IN CERTAIN TRANSACTIONS”). These conflicts present the risk to holders of Shares that the transactions between the Trust and such parties have not been negotiated at arm’s-length. As a consequence, agreements between related parties do not carry the indicia of fairness that a transaction negotiated between unrelated parties would have and bear closer scrutiny by investors.

No Assurances that Transactions between the Trust and Affiliated Parties will be as Favorable to the Trust as those not with Affiliated Parties

The UPREIT has engaged in transactions with members of the Board of Trustees or their affiliates (See “COMPENSATION PAID TO ADVISOR AND OTHER PROPERTY MANAGERS – Affiliates of the Trust Participating in Service Providers” and “Interests of Management and Others in Certain Transactions” for information regarding such transactions). The transactions have included: (i) provision of property management services to the Trust; (ii) provision of real estate brokerage services to the Trust; (iii) the acquisition of real estate from such affiliates (iv) the making of loans to finance real estate developments by the affiliates; and (v) the acquisition of equity interests in entities owned or controlled by such affiliates.

While in each instance, the member of the Board of Trustees who is engaging directly or (through an affiliate) indirectly with the UPREIT is required to disclose their interest in the transaction to the Board of Trustees and, under the Declaration of Trust, by a majority vote of the Independent Trustees, it must be determined that:

| ● | the transactions is fair and reasonable; | |

| ● | the transaction involves terms no less favorable to the Trust as available in an arm’s length transaction; and | |

| ● | (if property is being acquired by the Trust) the appraised value of property being acquired is at least equal to if not greater than the consideration being paid for the property by the UPREIT; |

there can be no assurance that past and future transactions are not as favorable to the Trust as might have been or be obtained in a transaction with a completely independent party rather than with an affiliate of one of our Trustees.

Affiliates Managing Our Properties. Of the nine property managers we currently engage to manage our properties, five are affiliated with members of our Board of Trustees. George Gaukler, Jim Knutson and Matthew Pedersen are owners of the Advisor. Mr. Gaukler is an owner of Valley Rental Services, Inc. and Horizon Real Estate Group, LLC (Mr. Knutson was an owner of Valley Rental Services, Inc. and of Horizon Real Estate Group, LLC until December 31, 2018). Kevin Christianson is the owner of Property Resources Group, Inc. Craig Lloyd is an owner of Lloyd Property Management Company. In 2019 and in 2020 we paid $2,269,609 and $2,283,836, respectively in management fees to such management companies. Of those fees, the above named management companies affiliated with Trustees were:

| 7 |

| Management Company | Fees in 2019 | Fees in 2020 | ||||||

| Dakota REIT Management, LLC | $ | 263,607 | $ | 304,307 | ||||

| Valley Rental Service, Inc. | $ | 891,576 | $ | 1,064,881 | ||||

| Horizon Real Estate Group, LLC | $ | 77,313 | -0- | |||||

| Property Resources Group, LLC | $ | 157,900 | $ | 163,742 | ||||

| Lloyd Property Management Company | $ | 187,715 | $ | 172,389 | ||||

Affiliates Compensated for Commercial Leasing. In 2019 and in 2020 we paid commissions of $314,392 and $81,004, respectively, to real estate brokers in connection with their having participated in the long term leasing of space in our commercial properties. Three of such brokers are affiliates of current members of our Board of Trustees. They were Horizon Real Estate Group, LLC (an affiliate of George Gaukler and, until December 31, 2018, an affiliate of Jim Knutson) Property Resources Group (an affiliate of Kevin Christianson) and Lloyd Companies, Inc. (an affiliate of Craig Lloyd). The fees paid to such brokers for services in leasing of space in our commercial properties in 2019 and 2020 were:

| Real Estate Broker | Fees in 2019 | Fees in 2020 | ||||||

| Horizon Real Estate Group, LLC | $ | 45,105 | $ | 3,000 | ||||

| Property Resources Group, LLC | $ | 23,287 | $ | 78,004 | ||||

| Lloyd Companies, Inc. | $ | 246,000 | -0- | |||||

Properties Acquired from Affiliates. Of the 75 properties we owned as of December 31, 2020, 30 (or approximately 40%) were acquired from a member of our Board of Trustees or from an entity owned - at least in part - by a member of our Board of Trustees (See tables listing our properties and the column indicating acquisition from a Trustee under “DESCRIPTION OF PROPERTIES” for information related to which of our properties were acquired from affiliates and see “Acquisitions from Affiliates” in “Interests of Management and Others in Certain Transactions.”

Loans to Affiliates. We have from time to time made loans to affiliates of members of our Board of Trustees in connection with real estate development. In 2020, we loaned $1,000,000 to The Rowe at 57th, LLC, an affiliate of Craig Lloyd. The loan was made to fund certain costs of constructing a 144 Unit apartment complex the borrower is developing in Sioux Falls, South Dakota. The loan is to be repaid on or before February 23, 2023. We contemplate that we may continue to make real estate development loans to our affiliates.

Investment in Affiliates. We currently own non-controlling interests in five limited liability companies or limited partnerships (See table in the “General Overview” section of “MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS” for identification of the entities and our ownership interests in them), each of which has or had George Gaukler as one of its owners. Each operates apartment buildings located in Williston, North Dakota. We have invested an aggregate of $6.275 million in such entities. We also were an owner of One Oak II Limited Liability Limited Partnership and thereby had an indirect interest in another limited liability limited partnership which was developing the One Oak Place senior living facility in Fargo, North Dakota, but in August 2015, the UPREIT acquired ownership of the property for a purchase price of $45.7 million and we effectively converted our $2.5 million investment in the property into a full ownership position.

RISKS RELATED TO ECONOMIC CONDITIONS

Economic Conditions Resulting from COVID-19 Pandemic

We anticipated that the disruptions in employment, reduction in certain retail sales and other challenges resulting from the COVID-19 pandemic would have an adverse impact on our tenants and their ability to pay the rent due under their leases. For the year ended December 31, 2020, our funds from operations was down approximately $289,000 (an approximately 1.5% reduction) compared to our prior year. As we emerge from the pandemic, we see signs of encouragement including having entered into or renewed more than 60 leases for our commercial space. We are, however, unable to predict if our operations will continue to improve or actions we may need to take in response to economic conditions attributable to the pandemic.

| 8 |

Economic Conditions May Limit the Ability of the UPREIT to Purchase Properties or of Tenants to Pay Rent

Periods of tight credit and high interest rates may adversely affect the ability of the UPREIT to acquire or sell properties. The inability of the UPREIT to acquire new properties or to sell certain of its existing properties further constrains the Trust’s diversification and growth. During times of economic recession the ability of tenants to rent spaces from the UPREIT and timely pay rent when due may be adversely affected. This would limit the income available to the UPREIT for distribution to the Trust and, consequently, limit the Trust’s ability to make distributions to our shareholders.

There may be future shortages or increased costs of fuel, natural gas, water, or electric power, or allocations thereof by suppliers or governmental regulatory bodies in the areas where property purchased by the UPREIT is located. In the event that any such shortages, price increases or allocations occur, the financial condition of tenants of the UPREIT may be adversely affected. The Trust is unable to predict the extent, if any, to which such shortages, increased prices or allocations would influence the ability of tenants to make rent payments and the Trust to make cash distributions to shareholders.

Risk of Downturn in Real Estate Market

While we are exposed to risks of adverse development in the economy in general, the real estate market we participate may have its own adverse economic developments. Due to numerous conditions over which we will have no control, the market values of properties we own may decrease. Such decreases will adversely affect our abilities to refinance mortgage indebtedness on such properties (See footnotes to the “DESCRIPTION OF PROPERTIES” for information regarding mortgage indebtedness against our properties) which could provide significant issues for properties we have financed on terms involving “balloon payments” of the unpaid principal balance at a maturity date which occurs prior to complete payment of the debt based upon the payment schedule.

If such downturns in the real estate markets occur, we may find that we are unable to sell properties we determine to sell or, if we are able to sell a property, we may receive an amount which is less than we have invested in acquiring and operating the property. We may even find that the debt we owe at the time of sale, exceeds the amount we can obtain from a purchaser.

Risks of Disruptions in the Financial Markets

The success of our business is significantly related to general economic conditions, but in particular, we are dependent upon the condition of the banking and financial markets. Rising interest rates and the decreasing availability of funding for real estate investments could have a materially adverse effect on our operations and on our abilities to acquire additional properties, refinance mortgage indebtedness and sell properties we hold.

Tenant Bankruptcies

Economic conditions affecting tenants leasing our properties may result in filing of bankruptcy by tenants. In particular, this may have a more significant adverse impact on our operations and financial condition with respect to our commercial real estate where the properties have fewer tenants than are associated with our residential rental real estate. In addition, we may incur legal fees and other costs in seeking to protect our interests in the event of a filing of bankruptcy by a tenant.

RISKS RELATED TO OUR STRUCTURE AND THE OFFERING

There is No Assurance That Shareholders Will Receive Cash Distributions or Benefit from Property Appreciation

While we have had a history of paying quarterly distributions, there is no assurance as to whether cash distributions can continue to be available for distribution to shareholders (See “SECURITIES BEING OFFERED – Distribution” for distribution declared and paid since 2010. There is no assurance that the Trust will operate at a profit or that any properties acquired by the UPREIT will appreciate in value or can ever be sold at a profit. The value and marketability of the UPREIT’s properties will depend upon many factors beyond the control of the Trust or the UPREIT, and there is no assurance that there will be a ready market for the properties owned by the UPREIT since investments in real property are generally non-liquid. Operating expenses of the Trust, including certain compensation to the Advisor will be incurred and must be paid irrespective of the Trust’s profitability.

| 9 |

Even if the Trust operates on a profitable basis, our ability to pay cash distributions may be impaired. In each of 2019 and 2020 we declared aggregate distributions to shareholders of the Trust and to limited partners of the UPREIT of $11,990,592 and $12,631,854 (after reinvestment of declared distributions to acquire shares or limited partnership units, the net distributions/distributions paid were $6,692,456 and $7,469,017) compared to net cash from operating activities of $19,212,639 and $17,645,621, respectively. Shareholders of the Trust and limited partners of the UPREIT participating in reinvestment of their distributions or distributions may terminate such participation with minimal notice and such termination by a substantial number of the participants could require us to use cash rather than our shares or the Trust’s limited partnership units to satisfy the rights to distributions or distributions, as applicable.

Further, if we were not successful in refinancing our mortgage indebtedness when the loans mature, we would need to use net operating cash flow to satisfy the “balloon payments” due at the maturities of our loans. For information regarding the amounts coming due under our mortgage indebtedness see the footnotes to the table of our “DESCRIPTION OF PROPERTIES.” In connection with your consideration of these risks you may wish to know that we have the following loans maturing this year and in the next two calendar years:

| ● | 9 loans have or will come due in 2021 with an estimated principal at maturity of approximately $41,713,500; |

| ● | 7 of loans will be due in 2022 with an estimated principal at maturity of approximately $44,552,000; and |

| ● | 8 of loans will be due in 2023 with an estimated principal at maturity of approximately $27,002,500. |

Investments in the Trust are Subject to Dilution by Future Sales of Securities by Both the Trust and the UPREIT

Under the terms of the UPREIT Limited Partnership Agreement, the UPREIT is authorized to issue limited partnership interests in the UPREIT in exchange for real estate or interests in real estate. Such exchanges have occurred and are expected to continue to occur during and after the Offering. We intend for the UPREIT to continue to seek contributions of property in exchange for Partnership Interests in the UPREIT. Additionally, the Trust will, continue to seek investors in to acquire Shares in exchange for cash investment in the Trust. These additional investments will dilute the percentage ownership interests of current investors of the Trust, including those that reinvest their distributions to acquire additional shares.

No Assurance that we will Continue our Share Repurchase Plan

To provide shareholders with an opportunity for liquidity with respect to our Shares, we have from time to time maintained arrangements permitting shareholders who have held their Shares for at least one year the right to request the repurchase by the Trust of all or a portion of their Shares (See - “SECURITIES BEING OFFERD – Share Repurchase Plan” for information related to such arrangements).

The Board of Trustees reserves the absolute right to terminate, suspend or amend the Share Repurchase Program at any time without shareholder approval, but subject to advance notification to the shareholders, if the Trustees believe such action is in the best interest of the Trust or if they determine the funds otherwise available to fund our Share repurchase are needed for other purposes. In response to potential reduction in operating revenue as a result of the COVID-19 pandemic, the Board of Trustees determined in April 2020 to suspended the repurchase of shares, but in October 2020 the suspension was terminated and share repurchases were commenced under the Share Repurchase Plan.

RISKS RELATED TO OUR STATUS AS A REAL ESTATE INVESTMENT TRUST

The Trust May Limit Ownership of Shares in Order to Remain Qualified as a REIT

In order for the Trust to qualify as a REIT, no more than 50% of the outstanding Shares may be owned, directly or indirectly, by five or fewer individuals at any time during the last half of the Trust’s taxable year. To ensure that the Trust will not fail to qualify as a REIT under this test, the Declaration of Trust authorizes the Trustees to take such actions as may be required to preserve its qualification as a REIT, and limits any person to direct or indirect ownership of no more than a limited percentage of the outstanding Shares of the Trust. While these restrictions are designed to prevent any five individuals from owning more than 50% of the Shares, they would also make virtually impossible a change of control of the Trust. The restrictions and provisions may also (i) deter individuals and entities from making tender offers for Shares, which offers may be attractive to shareholders, or (ii) limit the opportunity for shareholders to receive a premium for their Shares in the event an investor is making purchases of Shares in order to acquire a block of Shares.

| 10 |

Compliance with REIT Qualification Requirements may Impair our Operations

The Declaration of Trust directs the Board of Trustees to maintain our qualification under applicable law as a REIT. It is possible that the requirements may limit the investments which may be pursued by the Trust or even require a liquidation of investments the Board of Trustees views as being attractive.

If the Trust Fails to Qualify as a Real Estate Investment Trust, the Trust and Investors May Suffer Adverse Tax Consequences. The Trust and Investors May Also Suffer Adverse Tax Consequences from Other Unanticipated Events

Although management believes that the Trust has been organized and operated to qualify as a REIT under the Code, no assurance can be given that the Trust has in fact operated or will be able to continue to operate in a manner to qualify or remain so qualified. Qualification as a REIT involves the application of highly technical and complex Code provisions for which there are only limited judicial or administrative interpretations, and the determination of various factual matters and circumstances not entirely within the Trust’s control (See – “Requirements for Qualification – General,” “Income Tests,” “Asset Tests” and “Annual Distribution Requirements” under “FEDERAL INCOME TAX CONSIDERATIONS”). For example, in order to qualify as a REIT: the Trust must be owned by at least 100 or more persons; at least 95% of the Trust’s taxable gross income in any year must be derived from qualifying sources; the Trust must make distributions to shareholders aggregating annually at least 90% of its REIT taxable income (excluding net capital gains); and at least 75% of our assets must be “real estate assets,” cash or U.S. government securities. To the extent we fail these requirements, unless certain relief provisions apply, we may have a loss of our status. Such a loss could have a material adverse effect on the Trust and its ability to make distributions to you and to pay amounts due on its debt. Additionally, to the extent UPREIT was determined to be taxable as a corporation, the Trust would not qualify as a REIT, which could have a material adverse effect on the Trust and its ability to make distributions to you and to pay amounts due on its debt. Finally, no assurance can be given that new legislation, new regulations, administrative interpretations or court decisions will not change the tax laws with respect to qualification as a REIT or the federal income tax consequences of such qualification.

If the Trust fails to qualify as a REIT, it will be subject to federal income tax (including any applicable alternative minimum tax) on its taxable income at corporate rates, which would likely have a material adverse effect on the Trust and its ability to make distributions to shareholders and to pay amounts due on its debt. In addition, unless entitled to relief under certain statutory provisions, the Trust would also be disqualified from treatment as a REIT for the four taxable years following the year during which qualification is lost. This treatment would reduce funds available for investment or distributions to shareholders because of the additional tax liability to the Trust for the year or years involved. In addition, the Trust would no longer be required to make distributions to shareholders. To the extent that distributions to shareholders would have been made in anticipation of qualifying as a REIT, the Trust might be required to borrow funds or to liquidate certain investments to pay the applicable tax.

For a further discussion of income tax issues, see “FEDERAL INCOME TAX CONSIDERATIONS.”

| 11 |

This Offering is being made to existing shareholders of the Trust who are residents of or entities domiciled in a state in which we have qualified the issuance of Shares under the DRIP in accordance with laws of such state related to the offer and issuance of securities. Individuals are residents of the state in which they maintain their principal residence. A corporation, partnership, trust or other entity is domiciled in the state where the principal office of the entity is located. With respect to shareholders residing in or domiciled in certain states, the number of shares which may be issued may be limited such that the Trust may need to decline to accept requests for reinvestment of distributions that would involve our exceeding such limitations.

Duration of Offering. This Offering will end on the earlier of: (i) July 31, 2022; (ii) when all Shares and been issued; or (iii) when we may elect to terminate the Offering one or more of the classes of Shares. We may, however, elect to obtain authorization from the SEC and applicable state securities administrators to extend the term of the Offering or otherwise amend its terms.

No Broker/Dealers are Engaged to Solicit Participation in the Plan. The Trust is directly, without the engagement of broker/dealers, offering the Shares in this Offering under the Trust’s DRIP (See “SECURITIES BEING OFFERED – Distribution Reinvestment Plan”).

State of Residence or Domicile for Plan Participation by a Shareholder. This Offering is available only to shareholders of the Trust who are residents of or entities domiciled in a state in which we have qualified the issuance of share under the DRIP in accordance with laws of such state related to the offer and issuance of shares. Individuals are residents of the state in which they maintain their principal residence. A corporation, partnership, trust or other entity is domiciled in the state where the principal office of the entity is located.

Participation in the DRIP. To participate in the Offering, investors must be a participant in the DRIP and have their shareholder registration with the Trust reflect that the participant meets the residency / domicile requirements addressed above.

The Trust will receive no cash proceeds from the issuance of Shares to participants in the DRIP. Such issuance, however, will permit the Trust to retain funds within the UPREIT which would otherwise be applied to payment of cash distributions. Such retained funds can be used by the UPREIT to acquire additional properties, repay indebtedness and for expenditure in operations of the business of the Trust and the UPREIT.

As of the date of this Offering Circular, we have not identified any specific property or properties we will seek to acquire with any additional cash retained as a result of issuance of Shares in lieu of payment of distributions in cash to participants in the DRIP. Acquisitions and investments by the UPREIT will be determined by the Board of Trustees of the Trust and we anticipate that we will continue to use our capital and proceeds from borrowings to invest in real estate (See “DESCRIPTION OF BUSINESS – Investment Policies and Objectives of the Trust”).

| 12 |

THE TRUST

The Trust is an unincorporated business trust registered under the laws of North Dakota with the office of the North Dakota Secretary of State and is set up to meet the requirements under Internal Revenue Code Section 856 as a real estate investment trust (a “REIT”). Internal Revenue Code Section 856 requires that 75% of the assets of a REIT, either directly or indirectly, must consist of real estate assets and that 75% of its gross income must be derived from real estate. As a REIT, the Trust is generally not subject to U.S. federal corporate income tax on its net taxable income that is distributed to the shareholders of the Trust.

The Trust began operations in 1997 and in 2000 the Trust formed the UPREIT to acquire income-producing real estate properties and investments in entities holding income-producing real estate. Through the UPREIT, for which the Trust is the General Partner, the Trust seeks to invest in income-producing real estate that will provide cash flow and capital appreciation opportunities. The Trust intends to invest in the upper Midwest region and, as of the date of this Offering Circular, the properties we hold in are primarily located in North Dakota, we also have properties in Iowa, Minnesota, Nebraska, and South Dakota. Of those properties, (based on the amounts we invested in them) approximately 50% are commercial and 50% are residential (See “DESCRIPTION OF PROPERTIES”).

The principal governing document for the Trust is its Declaration of Trust, which was amended as of November 19, 2020 to remove the requirement that the Trust terminate upon the expiration of 21 years after the death of the last survivor of the original eight members of the Board of Trustees. Accordingly, the Trust will continue until terminated as a result of action initiated by the voting shareholders or the Board of Trustees.

THE UPREIT

The UPREIT is a limited partnership established under the laws of North Dakota. The Trust is the general partner of the UPREIT. As of December 31, 2020 there were approximately 163 holders of limited partnership interests in the UPREIT holding an aggregate of 6,992,036 Partnership Units. In our consolidated financial statements, our general partnership interests are referred to as “Beneficial Interests” while the limited partnership interests are referred to as “Noncontrolling Interests.”

Most of the real estate properties we have invested in are held directly by the UPREIT, but certain properties are held by one of ten entities for which the UPREIT is the sole owner/member. This has been done to satisfy a requirement of mortgage lenders who finance the acquisition or holding of the properties. In addition, the UPREIT holds minority interests in real estate holding entities and has made loans to developers of real estate projects the UPREIT may acquire.

The UPREIT acquires real properties through both purchase and in exchange for issuance of limited partnership interests to owners of the real estate being acquired through such an exchange. By exchanging property for limited partnership interests, rather than selling the property to the UPREIT for cash, the owner may defer the recognition of the taxable gain on the property if the value of the property exceeds the tax basis the owner has in the property.

ADVISOR AND PROPERTY MANAGERS

Neither the Trust nor the UPREIT has employees. The Trust has an advisory contract with Dakota REIT Management, LLC (the “Advisor”) under which the Advisor carries out the daily operations of the Trust including its responsibilities as the general partner of the UPREIT (for information regarding the qualifications of the Advisor, see “SIGNIFICANT EMPLOYEES OF THE ADVISOR”). The Advisor is paid fees under the advisory contract (See “COMPENSATION PAID TO ADVISOR AND OTHER PROPERTY MANAGERS”).

The Advisor has never controlled or provided services to any other real estate investment trust, a real estate investment limited partnership or other investment program which provides flow-through tax consequences to investors. Thus, the Advisor has never participated in the offering of investments by such an entity which disclosed when the investment entity might be liquidated and thus there can be no disclosure as to whether such liquidation was completed as disclosed.

The UPREIT engages services of the property management companies in connection with the management of the properties owned by the UPREIT or its wholly owned subsidiaries, five of which are affiliates or members of our Board of Trustees (See “Property Management Agreements” for more information).

| 13 |

INVESTMENT POLICIES AND OBJECTIVES OF THE TRUST

Currently, all of the real estate investments of the Trust are made through the UPREIT. As general partner of the UPREIT, the Trust determines whether any properties are to be acquired or disposed of with such investment decisions being made through action of the Trust’s Board of Trustees. Currently, the Board of Trustees of the Trust intends to invest in properties located in growth markets in the upper Midwest. The Board of Trustees intends for the UPREIT to invest in multi-family apartments and commercial properties (industrial, grocery / grocery anchored retail and office space) located in communities that appear to involve a stable market for particular investments.

In 2019, we made three acquisitions and one disposition of properties. Two of the acquisitions were office warehouse facilities (one in January for $5,500,000 and the other in March for $11,850,000). In October we sold a 39,120 square foot retail property located in Sioux Falls, South Dakota for $4,100,000 which we had acquired in 2015 for $4,500,000. In November, we acquired five separate multi-family residential properties in a single transaction for $24,000,000.

In 2020, we made two dispositions and one acquisition of properties. In May, we sold a 25,614 square foot retail property located in New Prague, Minnesota for $1,285,000 which we had acquired in 2011 for $2,720,000. In June we sold a 23,206 square foot industrial property located in De Pere, Wisconsin for $1,825,000 which we had acquired in 2013 for $1,595,000. In September, we purchased a 59,323 square foot building located in Fargo, North Dakota as a grocery store for approximately $11,464,000.

In the first six months of 2021, we made three acquisition and four dispositions of properties. In January, we purchased a 72 unit apartment building located in Fargo, North Dakota for $7.4 million. In February, we sold two properties, an industrial warehouse located in Hastings, Minnesota for $800,000 which we had acquired in 2014 for $875,000 and a storage facility located in Minot, North Dakota for $1,075,000 which we had acquired in 2011 for $1,510,000. In April, we sold an 84 unit apartment building located in Fargo, North Dakota for $3,965,500 which we had acquired in 2014 for $3,760,000. In May, we acquired a 79,200 square feet industrial property located in Bismarck, ND and we sold a 28,347 square foot office building located in Bismarck, ND for $1,254,016 which we had acquired in 2010 for $1,400,000. In June, we purchased an 88 unit multifamily apartment building located in Johnston, Iowa for $12 million

For listings of the properties held either directly by the UPREIT or through an entity wholly owned by the UPREIT, as of December 31, 2020, see “DESCRIPTION OF PROPERTIES.”

The UPREIT does not currently intend to invest in mortgages loans originated by others, although we have made loans to finance the development of real estate properties we contemplate acquiring. The Declaration of Trust sets forth restrictions on investment in mortgage loans, including limitations on deferral of payment of accrued interest and the making of loans that result in indebtedness against the property exceeding 85% of its appraised value absent substantial justification (such as credit enhancements in the form of a guaranty by a financially strong third party).

The UPREIT has made investments in limited partnerships, limited liability companies and other limited liability entities that own and operate real estate which is of a type the UPREIT would hold.

The investment objectives of the Trust are to provide to its shareholders (i) preservation, protection and eventual return of the shareholder’s investment, (ii) annual cash distributions of cash from operations, a portion of which (due to depreciation) may be a return of capital for tax purposes rather than taxable income, and (iii) realization of long-term appreciation in value of the properties acquired by the Trust. There is no assurance that such objectives will be attained.

When considering properties to be included in the portfolio of the UPREIT, the Board of Trustees of the Trust uses the following criteria for selection:

| ● | Income Production Capacity. A property must be anticipated to be capable of producing adequate income and cash flow to allow for payment of distributions to partners of the UPREIT and thereby fund distribution payments to shareholders of the Trust. Historical vacancy rates no greater than 5% for multi-family properties, and 5-10% for commercial properties are desirable. Historical and anticipated operating expenses, such as property management fees and repairs and maintenance costs are important factors. |

| 14 |

| ● | General Economic Criteria. The properties located in areas with a stable or growing market for the type of property under consideration are preferable. The number of potential new properties that may be developed under permits that have been granted and competitive properties under construction are factors to be considered. |

| ● | Potential for Appreciation in Value. Although the anticipated income generation capacity is typically of greater importance, the long-term potential for a property’s value to appreciate and provide a capital gain will be considered. |

| ● | Condition of the Property. Newer properties or, if older, properties that have been well maintained and in good condition are preferred. The Board of Trustees has, however, approved the acquisition of properties that need to be refurbished when there is an expectation for considerable asset appreciation from such renovations. |

| ● | Size of the Property. The Board of Trustees will consider the size of a property considered for acquisition, primarily from a management view. Larger complexes are easier to manage, although a single property in close proximity to other properties of the UPREIT would be considered. Location will be considered as it relates to distance from services, transportation, and the market it intends to serve. |

| ● | Transaction Costs. In addition to the purchase price of the property, associated costs such as acquisition fees, appraisals, Phase I environmental reports, title insurance, and loan costs are considered. |

In making its investment decisions, the Board of Trustees is subject to terms of the Declaration of Trust (See “BOARD OF TRUSTEES, EXECUTIVE OFFICERS AND SIGNIFICANT EMPLOYEES – Organizational Structure”) which restricts the Trust from:

| ● | investing in commodities or commodity future contracts; |

| ● | investing more than ten percent (10%) of its total assets in unimproved real property or indebtedness secured by a real estate mortgage loan on unimproved real property; |

| ● | engaging in any short sale; |

| ● | borrowing on an unsecured basis if such borrowings will result in an asset coverage of less than three hundred percent (300%); “asset coverage,” means the ratio which the value of the total assets of the Trust, less all liabilities and indebtedness except indebtedness for unsecured borrowings, reserve for depreciation and amortization, bears to the aggregate amount of all unsecured borrowings of the Trust; |

| ● | engaging in trading as compared with investment activities; |

| ● | acquiring securities in any company holding investments or engaging in activities prohibited by these restrictions; |

| ● | engaging in underwriting or the agency distribution of securities issued by others; |

| ● | issuing equity securities redeemable at the option of the holder, or |

| ● | issuing debt securities unless the historical debt service coverage (in the most recently completed fiscal year) as adjusted for known changes is sufficient to properly service the higher level of debt. |

The Declaration of Trust also requires the Board of Trustees to approve acquisition at prices the Board of Trustees determines to be the fair market value of the property. Due to requirements of mortgage lenders and to comply with an accounting standard discussed in “MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS – Results of Operations,” independent appraisals of property are obtained. The Declaration of Trust requires the purchase from an affiliate of the Trust to be not greater than the appraised value determined by an independent appraiser. Further, a majority of the independent trustees may require use of the appraised value when the purchase is from any other seller (See “BOARD OF TRUSTEES, EXECUTIVE OFFICERS AND SIGNIFICANT EMPLOYEES – Members of the Trust’s Board of Trustees and Executive Officers”).

| 15 |

SUMMARY description OF the UPREIT limited PARTNERSHIP AGREEMENT

The Limited Partnership Agreement (the “Partnership Agreement”) is the governing document for the UPREIT. The Trust is the sole general partner of the UPREIT and as of December 31, 2020, the UPREIT had 163 limited partners of the UPREIT. The following is a summary of the material terms of the Partnership Agreement. Any descriptions are qualified in their entirety by reference to the Partnership Agreement. A copy of the Partnership Agreement currently in effect has been filed as an exhibit to the Offering Statement the Trust has filed with the SEC of which this Offering Circular is a part.

MANAGEMENT